Military Vehicle Electrification Market Report by Vehicle Type (Combat Vehicles, Support Vehicles, Unmanned Armoured Vehicles), Mode of Operation (Manned Vehicles, Autonomous/Semi-Autonomous), Technology (Hybrid, Fully Electric), Battery Type (Lithium-ion, Lead-acid, Nickel Metal Hydride, and Others), Voltage Type (Low Voltage, Medium Voltage, High Voltage), Region and Competitive Landscape (Market Share, Business Overview, Products Offered, Business Strategies, SWOT Analysis and Major News and Events) 2026-2034

Military Vehicle Electrification Market Size:

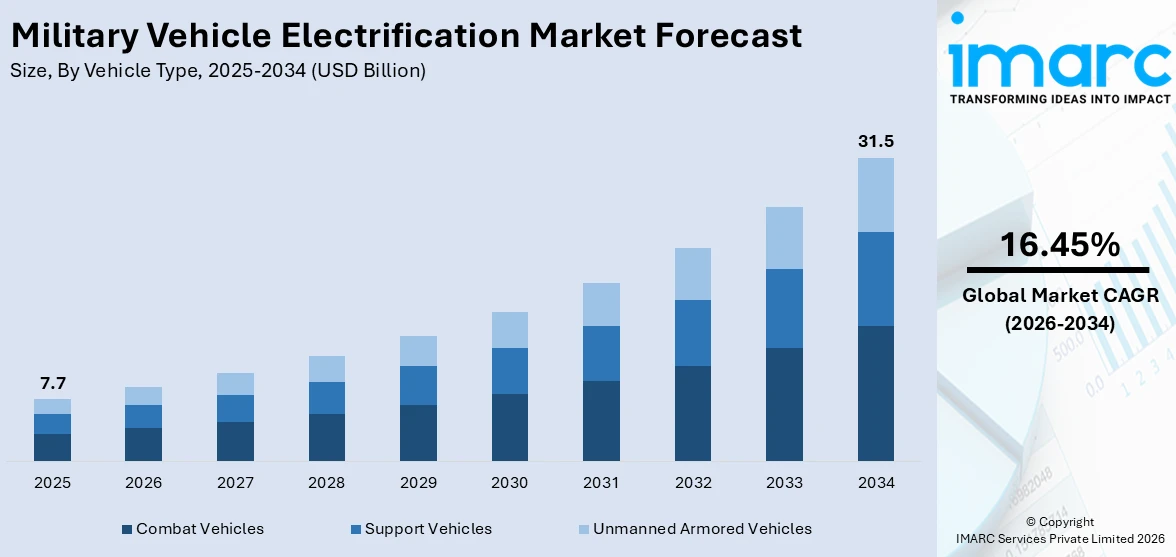

The global military vehicle electrification market size reached USD 7.7 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 31.5 Billion by 2034, exhibiting a growth rate (CAGR) of 16.45% during 2026-2034. The market is driven by advancements in battery technology, autonomous capabilities, and a strategic shift toward sustainable, efficient, and resilient defense operations.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 7.7 Billion |

| Market Forecast in 2034 | USD 31.5 Billion |

| Market Growth Rate (2026-2034) | 16.45% |

Military Vehicle Electrification Market Analysis:

- Market Growth and Size: The global military vehicle electrification market is witnessing substantial growth, propelled by increasing investments in modernizing defense fleets with sustainable, efficient technologies. This market expansion is underpinned by the rising awareness of the operational and strategic advantages of electric and hybrid vehicles in military applications, including reduced operational costs and enhanced stealth capabilities.

- Major Market Drivers: The shift toward vehicle electrification in the military sector is primarily driven by the global trend toward sustainability, governmental initiatives promoting green defense mechanisms, and the pressing need for energy-efficient and operationally effective military vehicles. These drivers are supported by advancements in battery technologies and the increasing demand for vehicles with lower noise, heat signatures, and maintenance requirements.

- Key Market Trends: Technological advancements in energy storage, autonomous driving capabilities, and intelligent power management systems are pivotal trends shaping the market. There is a noticeable shift toward integrating high-energy-density batteries and developing vehicles that can operate autonomously, enhancing the tactical and operational flexibility of armed forces.

- Geographical Trends: North America dominates the market, with significant investments from the US defense sector in electrification technologies. The Asia Pacific and Europe are also key regions showing rapid adoption, driven by regional security dynamics, indigenous defense manufacturing pushes, and stringent environmental regulations.

- Competitive Landscape: The market features a competitive landscape with key players focusing on innovation, strategic partnerships, and expanding their product portfolios to include electric and hybrid military vehicles. Companies are increasingly investing in R&D to enhance vehicle capabilities and integrate advanced technologies like AI and machine learning for autonomous operations.

- Challenges and Opportunities: While the market offers substantial opportunities through technological innovation and the shift toward sustainable military operations, challenges such as high initial costs, infrastructure requirements, and technological complexities persist. However, the ongoing advancements in battery technology, increasing government support, and the strategic importance of energy independence present significant growth opportunities for market players.

To get more information on this market Request Sample

Military Vehicle Electrification Market Drivers:

Global Trend Toward Electrification

The global trend toward electrification is significantly influencing the military vehicle sector, reflecting a broader shift in transportation toward more sustainable practices. This trend is driven by the need to reduce reliance on fossil fuels, enhance energy efficiency, and minimize the carbon footprint of military operations, leading to increased investment in electric military vehicles that promise lower operational costs and enhanced stealth capabilities due to reduced noise and thermal signatures.

Government Initiatives and Funding

Government initiatives and funding are pivotal in driving the military vehicle electrification market, as defense departments worldwide allocate substantial budgets to modernize and enhance the operational capabilities of their fleets. These initiatives often include financial incentives, research and development programs, and regulatory support, aiming to transition to a more sustainable, cost-effective, and future-proof military apparatus that aligns with broader governmental goals of reducing carbon emissions and fostering technological innovation.

Modularity and Adaptability

Modularity and adaptability are key factors propelling the electrification of military vehicles, enabling forces to customize and upgrade their fleets with various powertrains, battery packs, and other electric components. This flexibility allows for the development of vehicles that can be tailored to specific mission requirements, offering enhanced performance, reduced logistical burdens, and the ability to quickly integrate new technologies as they become available, thereby future-proofing military assets.

Technological Advancements & Environmental Concerns

Technological advancements and environmental concerns are jointly accelerating the shift toward military vehicle electrification. Innovations in battery technology, electric drivetrains, and energy management systems are making electric vehicles more viable for military use, offering improvements in range, durability, and power efficiency. Concurrently, growing awareness of environmental issues is prompting defense sectors to adopt eco-friendly alternatives, thus aligning military operational needs with global sustainability objectives.

Military Vehicle Electrification Market Opportunities

Innovation in Battery Technology

Innovations in battery technology present significant opportunities in the military vehicle electrification market, with advancements in higher energy density and faster charging capabilities leading the way. These technological improvements are crucial for extending the range, enhancing the payload capacity, and reducing the operational downtime of electric military vehicles. The development of more robust, efficient, and fast-charging batteries is essential for the widespread adoption and operational effectiveness of electrified military fleets, aligning with the strategic goals of modern armed forces.

Autonomous and Unmanned Vehicles

The integration of autonomous and unmanned vehicles within the electrified military fleet represents a substantial market opportunity, leveraging the compatibility of electric powertrains with advanced autonomous systems. This synergy enhances mission capabilities, operational safety, and efficiency, allowing for extended reconnaissance missions, reduced risk to personnel, and optimized logistics. The electrification of these vehicles facilitates quieter operation, increased situational awareness, and the potential for greater operational endurance, thereby expanding the tactical advantages of unmanned military operations.

Energy Independence and Resilience

Energy independence and resilience are key opportunities afforded by the electrification of military vehicles, offering strategic advantages in operational sustainability and logistic efficiency. Electrified vehicles can leverage various energy sources, reducing dependence on conventional fuel supply chains, which are often vulnerable to disruption. Enhanced energy resilience contributes to the overall readiness and effectiveness of the military forces, ensuring sustained operation capabilities in diverse and challenging environments while supporting the strategic goal of achieving a more secure and self-reliant defense infrastructure.

Key Technological Trends & Development

Advanced Energy Storage Systems

Advanced energy storage systems are at the forefront of technological trends in the military vehicle electrification market, with developments focusing on enhancing the energy density, durability, and safety of batteries. These systems are crucial for extending the operational range, improving payload capacity, and ensuring the reliability of electric military vehicles under harsh conditions. Innovations such as solid-state batteries and improved thermal management are pivotal, offering the potential for longer missions, reduced maintenance, and a lower logistical footprint.

Intelligent Power Management Systems

Intelligent power management systems represent a key technological development, optimizing the efficiency and longevity of electric military vehicles. These systems precisely control the distribution of electrical power to various vehicle components, enhancing overall performance, and energy utilization. They play a crucial role in extending mission duration, improving vehicle stealth through reduced thermal and acoustic signatures, and enabling the integration of renewable energy sources, thereby ensuring sustained operation and enhanced tactical advantages in the field.

Autonomous and Semi-Autonomous Capabilities

The advancement of autonomous and semi-autonomous capabilities in electrified military vehicles is a significant technological trend, enabling enhanced operational effectiveness, safety, and strategic flexibility. These capabilities facilitate remote operation, reduced crew requirements, and the execution of complex missions with minimal human intervention. Integration with electric vehicles offers advantages such as silent running, lower heat signatures, and improved reliability, thereby expanding the scope of missions these vehicles can undertake while maximizing strategic and tactical benefits.

Military Vehicle Electrification Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on vehicle type, mode of operation, technology, battery type, and voltage type.

Breakup by Vehicle Type:

- Combat Vehicles

- Support Vehicles

- Unmanned Armored Vehicles

Combat vehicles account for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the vehicle type. This includes combat vehicles, support vehicles, and unmanned armored vehicles. According to the report, combat vehicles represented the largest segment.

The combat vehicles segment is driven by the increasing demand for enhanced operational efficiency, reduced maintenance, and stealth capabilities in warfare scenarios. Electrified combat vehicles, including tanks and armored fighting vehicles, benefit from improved acceleration, lower noise levels, and reduced thermal signatures, offering strategic advantages on the battlefield. The shift toward electric powertrains in this segment reflects the prioritization of advanced technology to improve combat readiness and effectiveness while aligning with broader sustainability goals.

Support vehicles in the military vehicle electrification market encompass a range of logistics and utility vehicles, including transport trucks, fuel tankers, and medical evacuation vehicles. Electrification in this segment is focused on increasing operational efficiency, reducing logistical footprints, and enhancing energy independence. Electric support vehicles offer the advantage of silent operation, crucial for covert operations, and reduced dependency on conventional fuel supply chains, thereby improving the sustainability and resilience of military logistics in diverse operational environments.

Unmanned armored vehicles are an emerging segment in the military vehicle electrification market, highlighted by their increasing utilization for reconnaissance, surveillance, and targeted offensive operations. The integration of electric powertrains in these vehicles enhances their operational capabilities by enabling longer endurance, quieter movement, and lower heat signatures, which are vital for stealth and efficiency in mission-critical applications. The growth of this segment is fueled by continuous advancements in autonomous technology and the strategic value of unmanned systems in modern military strategies.

Breakup by Mode of Operation:

Access the comprehensive market breakdown Request Sample

- Manned Vehicles

- Autonomous/Semi-Autonomous

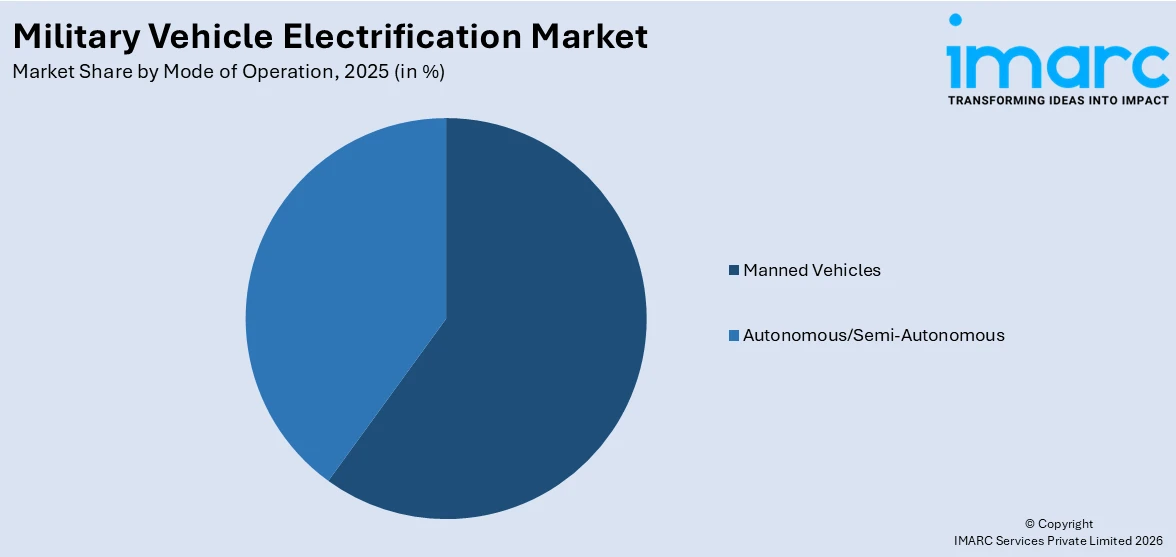

Manned vehicles hold the largest share in the industry

A detailed breakup and analysis of the market based on the mode of operation have also been provided in the report. This includes manned vehicles and autonomous/semi-autonomous. According to the report, manned vehicles accounted for the largest market share.

Manned vehicles constitute the largest segment in the military vehicle electrification market, primarily due to their extensive current deployment across various military operations and the immediate benefits they gain from electrification, such as reduced fuel consumption, lower maintenance costs, and enhanced stealth capabilities through quieter operation. The focus in this segment is on integrating electric powertrains into traditional crewed vehicles, enhancing their operational efficiency, and reducing their environmental impact while maintaining the essential human decision-making element in complex combat scenarios.

The autonomous/semi-autonomous segment is rapidly gaining traction in the military vehicle electrification market, driven by the convergence of electrification with advanced autonomous technologies. These vehicles are designed to operate with minimal or no human intervention, leveraging the benefits of electric powertrains, such as improved energy efficiency, reduced thermal signatures, and silent operation, to enhance mission effectiveness in reconnaissance, surveillance, and logistics. This growth in this segment is propelled by the increasing focus of the military on reducing personnel risk, optimizing operational capabilities, and the strategic advantage of deploying unmanned systems in contested or hazardous environments.

Breakup by Technology:

- Hybrid

- Fully Electric

Hybrid represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the technology. This includes hybrid and fully electric. According to the report, hybrid represented the largest segment.

Hybrid vehicles dominate the market segmentation by technology in the military vehicle electrification sector, primarily as they offer a balanced compromise between traditional and fully electric systems. These vehicles combine internal combustion engines with electric power, providing reliability, extended range, and the flexibility of dual fuel sources. This adaptability is crucial for phased transition strategies, enabling forces to leverage the benefits of electrification while maintaining operational capability across varied and unpredictable environments, thus ensuring mission readiness without full dependence on charging infrastructure.

Fully electric vehicles represent a growing segment in the military vehicle electrification market, driven by the push for zero-emission transportation solutions and the advantages of stealth, lower operational costs, and reduced logistic footprints. These vehicles are characterized by their reliance on battery power, offering silent operation, high torque, and minimal heat signature, which are significant tactical benefits in combat situations. The adoption of fully electric vehicles is accelerating as battery technology advances, charging infrastructure expands, and military strategies increasingly prioritize sustainability and technological superiority.

Breakup by Battery Type:

- Lithium-Ion

- Lead-Acid

- Nickel Metal Hydride

- Others

Lithium-ion exhibits a clear dominance in the market

A detailed breakup and analysis of the market based on the battery type have also been provided in the report. This includes lithium-ion, lead-acid, nickel metal hydride, and others. According to the report, lithium-ion accounted for the largest market share.

Lithium-ion batteries are favored for their high energy density, lightweight, and long lifespan, which are essential for the rigorous demands of military applications. These batteries support enhanced vehicle performance, greater range, and faster charging times, making them ideal for high-power and high-capacity requirements in modern electrified military vehicles. Their widespread adoption is driven by continuous improvements in battery technology, offering increasingly efficient, reliable, and durable power sources for a variety of military operations.

Lead-acid batteries, while older in technology, remain relevant in the military vehicle electrification market for specific applications that require robust, cost-effective, and well-understood energy storage solutions. Known for their reliability, high power output, and ability to deliver stable voltage, these batteries are particularly suited for vehicles where weight is less of a concern and the ruggedness of the battery is paramount. However, their heavier weight, lower energy density, and shorter lifespan compared to lithium-ion batteries limit their suitability for broader applications in modern electrified military fleets.

Nickel-metal hydride batteries are utilized in the military vehicle electrification market, particularly in applications where longer life cycles and a higher tolerance for deep cycling are required. They are less prone to memory effects compared to other battery types and provide a good balance between cost, energy density, and durability. While they are heavier and have a lower energy density than lithium-ion batteries, their robustness and reliability under varied environmental conditions make them a viable option for certain military applications.

The others category in battery segmentation includes various emerging and alternative battery technologies such as solid-state, lithium-sulfur, and zinc-air batteries, which are gradually gaining traction in the military vehicle electrification market. These technologies are being explored for their potential to offer improvements over conventional batteries in terms of energy density, safety, temperature resilience, and environmental friendliness. Although currently less common, these innovative battery types are expected to play a crucial role in future military applications, providing enhanced performance and operational capabilities.

Breakup by Voltage Type:

- Low Voltage

- Medium Voltage

- High Voltage

Medium voltage dominates the market

The report has provided a detailed breakup and analysis of the market based on the voltage type. This includes low voltage, medium voltage, and high voltage. According to the report, medium voltage represented the largest segment.

Medium voltage systems, typically ranging from 600V to 3kV, are favored for their optimal balance between power output and safety. This voltage range is ideal for a variety of military vehicles, offering sufficient power for propulsion and onboard systems without the complexities and safety concerns associated with high-voltage systems. Medium voltage strikes a balance, providing robust performance and energy efficiency, making it suitable for a wide range of military applications, from light armored vehicles to larger transport vehicles.

Low voltage systems, generally categorized as under 600V, are integral to the military vehicle electrification market, especially for lighter, smaller vehicles and auxiliary systems where safety and simplicity are paramount. These systems are less complex, easier to manage, and pose fewer risks in terms of electrical safety, making them suitable for applications that require less power but prioritize reliability and ease of maintenance. The adoption of low voltage systems is particularly prevalent in support and logistic vehicles, unmanned systems, and various non-combat applications where operational efficiency and safety are crucial.

High voltage systems, typically above 3kV, are utilized in the military vehicle electrification market for applications demanding high power output, such as heavy-duty armored vehicles or those requiring extended range capabilities. These systems enable more efficient power transmission over long distances with less energy loss, supporting larger electric motors and longer-range missions. However, they come with increased complexity and higher safety requirements. High voltage is essential for applications that require significant propulsion power, fast charging capabilities, and high-energy onboard systems, catering to the demanding needs of modern electrified military fleets.

Breakup by Region:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East

- Africa

North America leads the market, accounting for the largest military vehicle electrification market share

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Latin America (Brazil, Mexico, and others); the Middle East; and Africa. According to the report, North America accounted for the largest market share.

The market in North America is driven by substantial defense budgets, advanced technological infrastructure, and strong governmental support for military modernization and sustainability initiatives. The United States leads this segment with significant investments in electrifying its defense fleet, focusing on enhancing operational capabilities, energy efficiency, and reducing the carbon footprint, supported by a robust network of industry players and R&D institutions committed to advancing military vehicle technology.

The Asia Pacific region is experiencing rapid growth in the military vehicle electrification market, fueled by escalating regional security concerns, increasing defense expenditure, and a strong push toward indigenous defense manufacturing. Countries like China, India, and South Korea are actively investing in electrified military technologies to enhance their strategic autonomy, operational readiness, and technological self-reliance, with a keen focus on integrating advanced energy solutions and electric propulsion systems in their military vehicles.

The Europe military vehicle electrification market is characterized by a strong emphasis on reducing the environmental impact of defense activities, aligning with the stringent emission regulations and sustainability goals in the region. The presence of leading defense contractors and automotive manufacturers in the region, coupled with collaborative defense initiatives across EU member states, propels the development and adoption of electric and hybrid military vehicles.

The Latin America military vehicle electrification market is gradually evolving, influenced by increasing awareness of the benefits of electrification in terms of operational efficiency, maintenance, and alignment with global environmental standards. The focus in the region is on modernizing its military fleets, enhancing energy security, and reducing dependence on fossil fuels, with countries progressively exploring the adoption of electric and hybrid technologies in their defense sectors.

The Middle East is strategically investing in the military vehicle electrification market to enhance its defense capabilities, energy efficiency, and operational sustainability. The significant oil reserves juxtapose its push toward diversification and modernization in defense technologies, including the adoption of electric vehicles to ensure advanced, resilient, and future-ready military operations amidst growing geopolitical tensions and an emphasis on technological sovereignty.

The Africa military vehicle electrification market is emerging, driven by a growing recognition of the strategic benefits of electrification in enhancing operational effectiveness, logistical efficiency, and environmental sustainability. The market growth is tempered by budgetary constraints and varying levels of technological adoption, yet there is a steady interest in leveraging electrified military vehicles to modernize fleets, reduce operational costs, and improve the logistical agility of defense forces across the continent.

Analysis Covered Across Each Country

- Historical, current, and future market performance

- Historical, current, and future performance of the market based on vehicle type, mode of operation, technology, battery type, and voltage type

- Competitive landscape

- Government regulations

Leading Key Players in the Military Vehicle Electrification Industry:

The leading companies in the military vehicle electrification market are actively engaging in research and development to innovate advanced energy solutions, enhance autonomous and semi-autonomous functionalities, and improve the modularity of electric vehicles. They are forming strategic partnerships, investing in cutting-edge technologies, and securing government contracts to expand their market presence. These companies are also focusing on sustainability, aiming to reduce the carbon footprint of military operations while ensuring that the electrified vehicles meet the rigorous demands of modern warfare and operational readiness.

The market research report has provided a comprehensive analysis of the competitive landscape covering market structure, market share by key players, market player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant, among others. Detailed profiles of all major companies have also been provided. This includes business overview, product offerings, business strategies, SWOT analysis, financials, and major news and events. Some of the key players in the market include:

- ASELSAN A.Ş.

- BAE Systems

- Flensburger Fahrzeugbau Gesellschaft (FFG)

- General Dynamics Corporation

- GM Defense LLC (General Motors)

- QinetiQ

- Rheinmetall AG

- Textron Systems

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Analysis Covered for Each Player

- Market Share

- Business Overview

- Products Offered

- Business Strategies

- SWOT Analysis

- Major News and Events

Latest News:

- In June 2022, GM Defense, a subsidiary of General Motors, was chosen by the Defense Innovation Unit (DIU) to create a battery pack prototype using GM's advanced Ultium Platform for testing on US Department of Defense platforms. The Ultium Platform offers modular and scalable electric vehicle battery technology, providing adaptable power, range, and scalability for various military vehicle needs, aligning with the Department of Defense's goal of adopting commercial technology for military use.

- In December 2023, Mack Defense partnered with BAE Systems to provide an alternative propulsion solution for the US Army's Common Tactical Truck (CTT) prototype vehicles. BAE Systems will supply its Gen3 propulsion and power management systems to reduce fuel demand and enhance vehicle performance.

Military Vehicle Electrification Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Combat Vehicles, Support Vehicles, Unmanned Armored Vehicles |

| Modes of Operation Covered | Manned Vehicles, Autonomous/Semi-Autonomous |

| Technologies Covered | Hybrid, Fully Electric |

| Battery Types Covered | Lithium-ion, Lead-acid, Nickel Metal Hydride, Others |

| Voltage Types Covered | Low Voltage, Medium Voltage, High Voltage |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East, Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ASELSAN A.Ş., BAE Systems, Flensburger Fahrzeugbau Gesellschaft (FFG), General Dynamics Corporation, GM Defense LLC (General Motors), QinetiQ, Rheinmetall AG, Textron Systems, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global military vehicle electrification market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global military vehicle electrification market?

- What is the impact of each driver, restraint, and opportunity on the global military vehicle electrification market?

- What are the key regional markets?

- Which countries represent the most attractive military vehicle electrification market?

- What is the breakup of the market based on the vehicle type?

- Which is the most attractive vehicle type in the military vehicle electrification market?

- What is the breakup of the market based on the mode of operation?

- Which is the most attractive mode of operation in the military vehicle electrification market?

- What is the breakup of the market based on technology?

- Which is the most attractive technology in the military vehicle electrification market?

- What is the breakup of the market based on the battery type?

- Which is the most attractive battery type in the military vehicle electrification market?

- What is the breakup of the market based on the voltage type?

- Which is the most attractive voltage type in the military vehicle electrification market?

- What is the competitive structure of the market?

- Who are the key players/companies in the global military vehicle electrification market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the military vehicle electrification market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global military vehicle electrification market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the military vehicle electrification industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)