mRNA Vaccines and Therapeutics Market Size, Share, Trends and Forecast by Vaccine Type, Treatment Type, Vaccine Manufacturing, Application, End-User, and Region 2026-2034

Global mRNA Vaccines and Therapeutics Market Size, Share, Trends and Forecast (2026-2034)

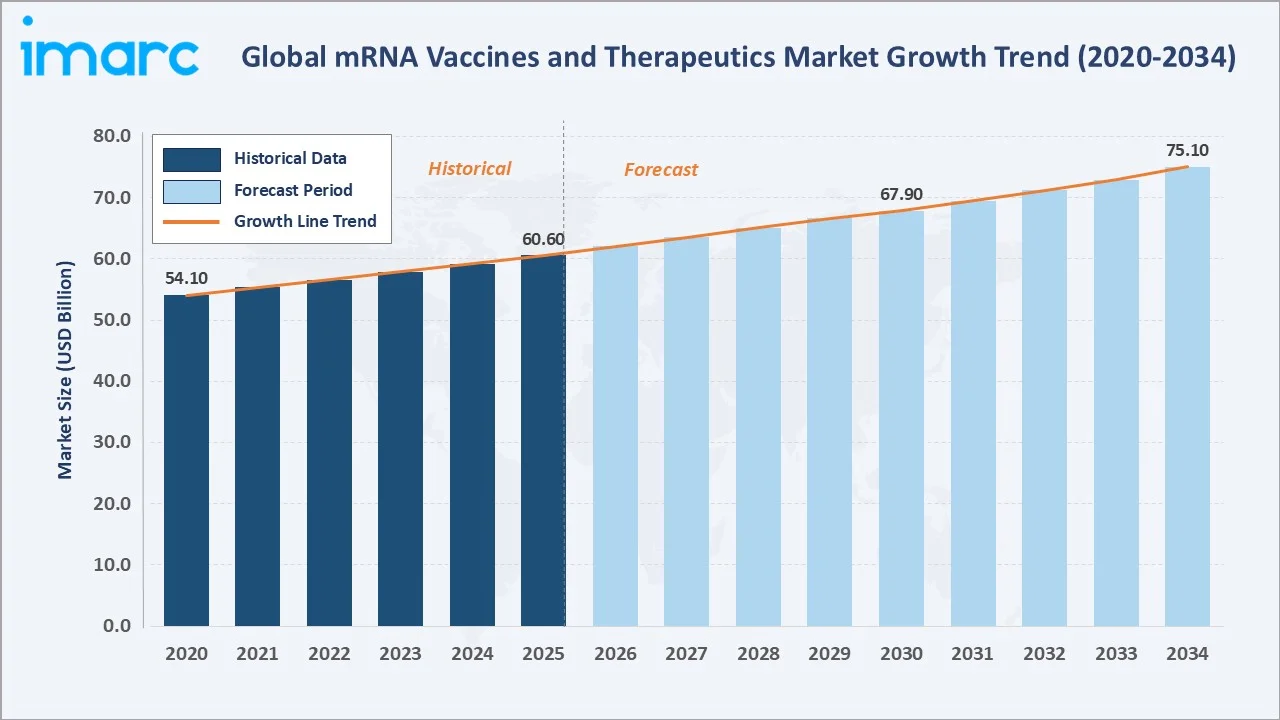

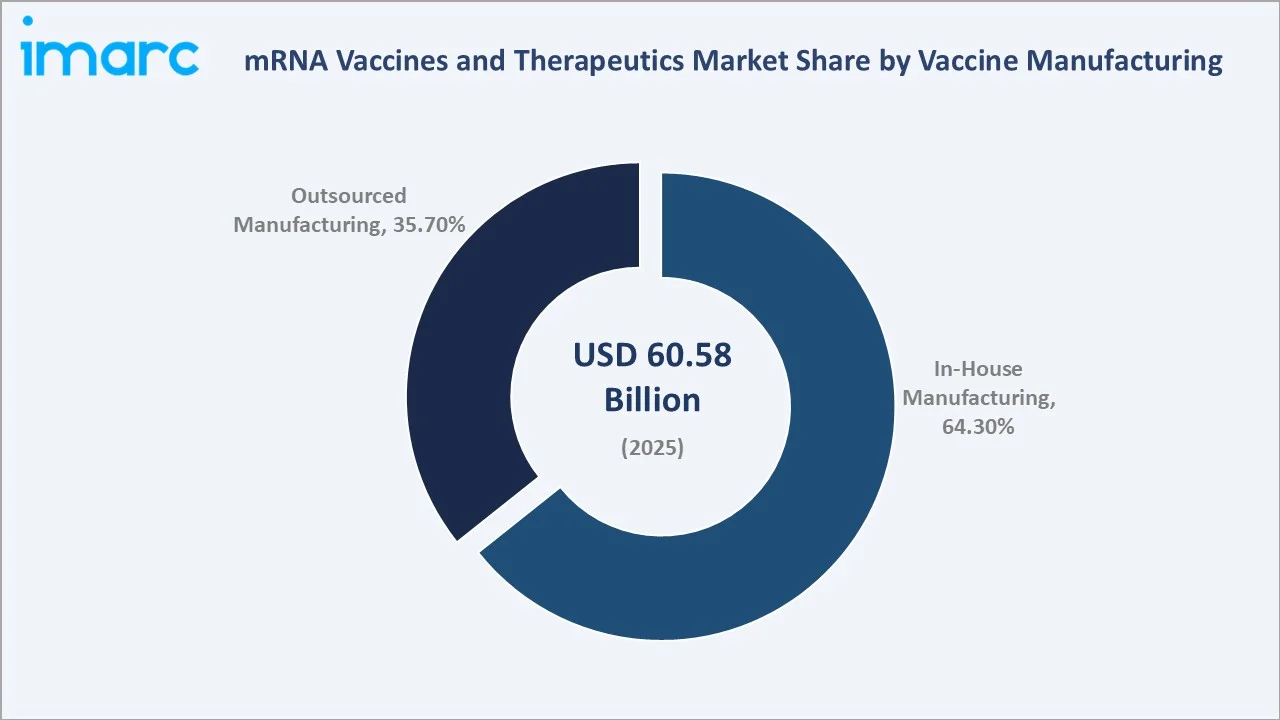

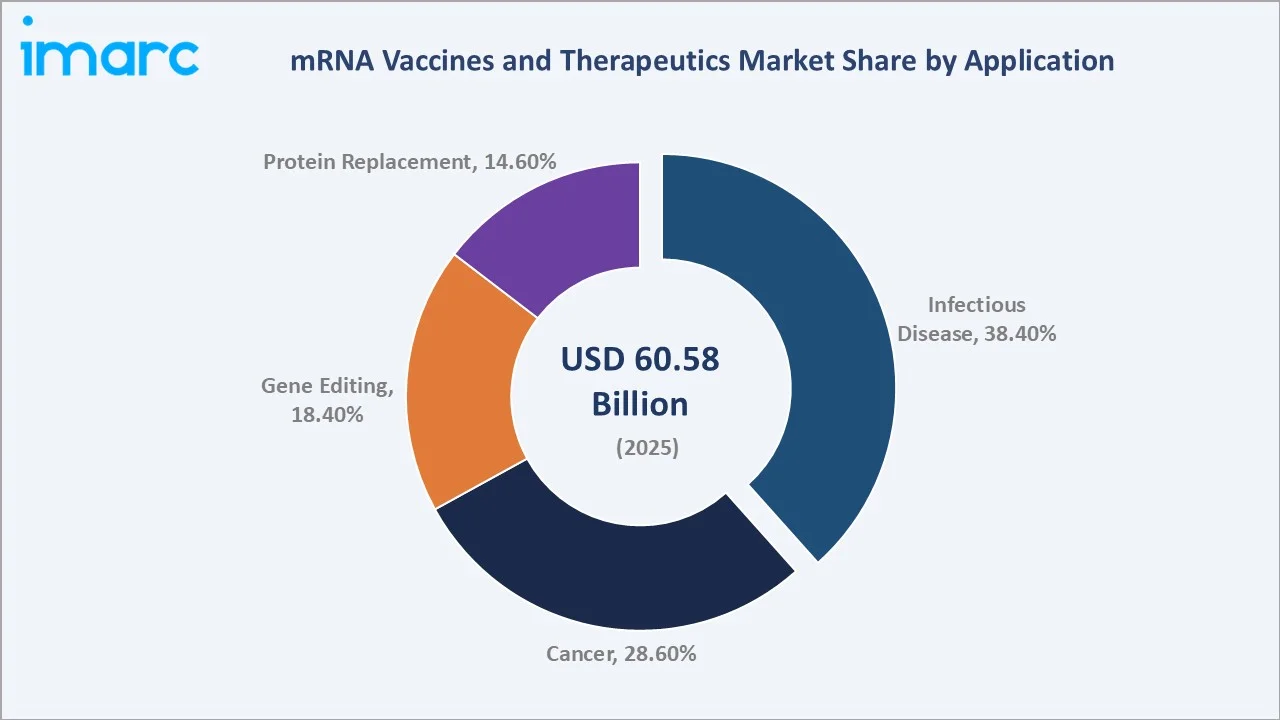

The global mRNA vaccines and therapeutics market reached a value of USD 60.58 Billion in 2025. IMARC Group expects the market to reach USD 75.11 Billion by 2034, exhibiting a CAGR of 2.30% during 2026-2034. Market growth is driven by rising global demand for rapid-response vaccines, expanding oncology pipelines, and surging investment in lipid nanoparticle (LNP) delivery technologies.

Market Snapshot

|

Metric |

Value |

|

Market Size 2025 |

USD 60.58 Billion |

|

Forecast Market Size 2034 |

USD 75.11 Billion |

|

CAGR 2026-2034 |

2.30% |

|

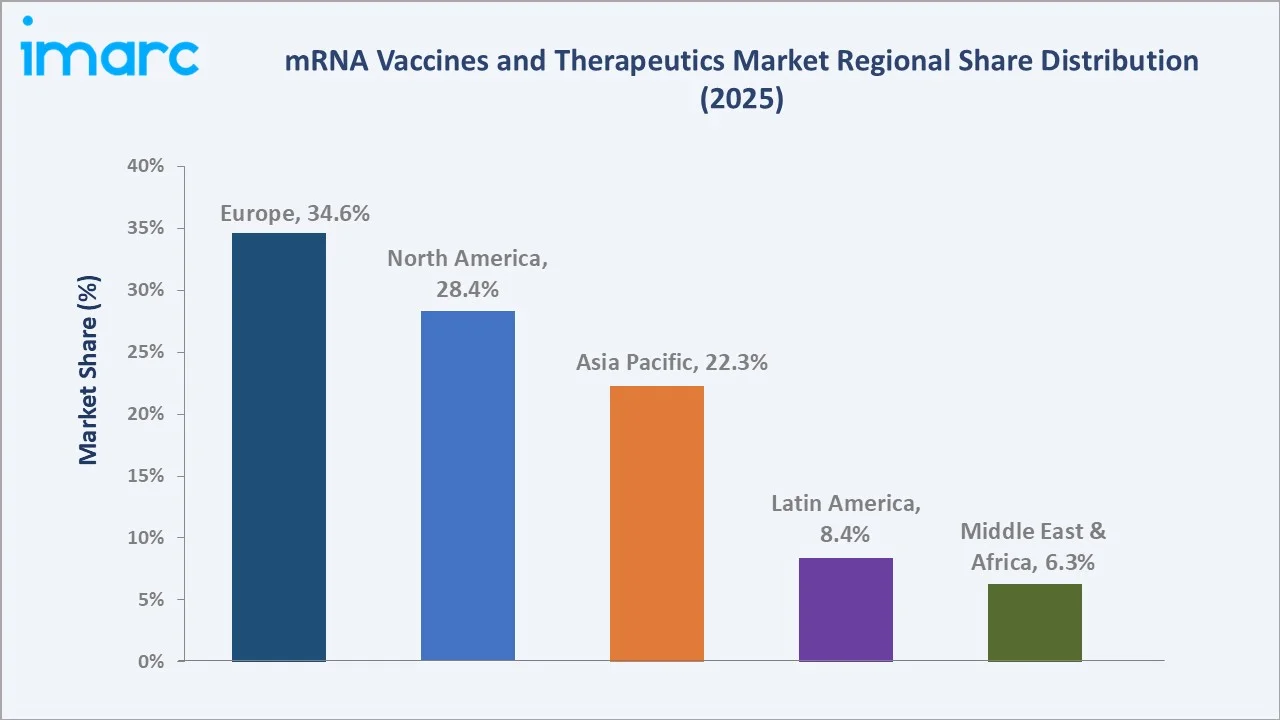

Largest Region |

Europe (34.6%, 2025) |

|

Largest Application |

Infectious Disease (38.4%, 2025) |

|

Leading Vaccine Manufacturing |

In-House (64.3%, 2025) |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

The mRNA vaccines and therapeutics market growth outlook is reinforced by continued COVID-19 booster programs, expanding clinical trials for mRNA-based cancer vaccines, and robust pipeline activity across infectious diseases, genetic disorders, and gene editing. LNP delivery advancements are enabling broader, safer therapeutic applications.

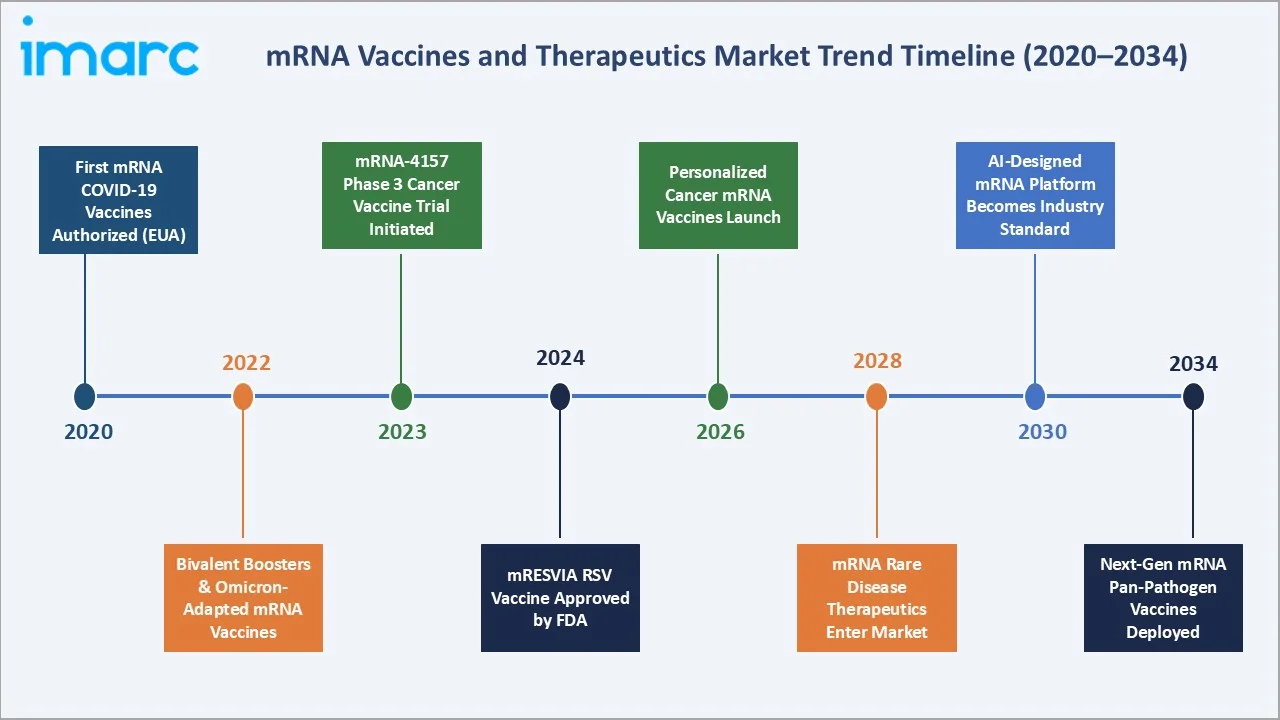

Each year in the United States, respiratory syncytial virus (RSV) kills up to 10,000 people, including 100 to 300 children. About 1 or 2 of every 100 children will be hospitalized with a lower respiratory tract infection caused by RSV in the first six months of life. The significant health burden of respiratory syncytial virus (RSV) in the United States, including substantial mortality among vulnerable populations and frequent hospitalizations in infants, highlights the urgent need for more effective and rapidly deployable preventive and therapeutic solutions. This has strengthened the case for mRNA-based vaccines and therapeutics, which offer advantages such as faster development timelines, adaptability to emerging viral strains, and the ability to induce targeted immune responses. As a result, rising RSV-related risks are contributing to increased demand and investment in mRNA platforms for both vaccination and treatment strategies.

To get more information on this market, Request Sample

The 2.30% CAGR reflects steady market expansion as initial COVID-19 vaccine revenues normalize and are supplemented by growing mRNA cancer therapeutics revenues. The mRNA vaccines market forecast points to a broadening therapeutic applications base through 2034.

Executive Summary

The global mRNA vaccines and therapeutics market stood at USD 60.58 Billion in 2025, anchored by Infectious Disease applications (38.4%), strong in-house manufacturing (64.3%), and Europe's leading regional share (34.6%). The market is projected to reach USD 75.11 Billion by 2034 at a CAGR of 2.30%.

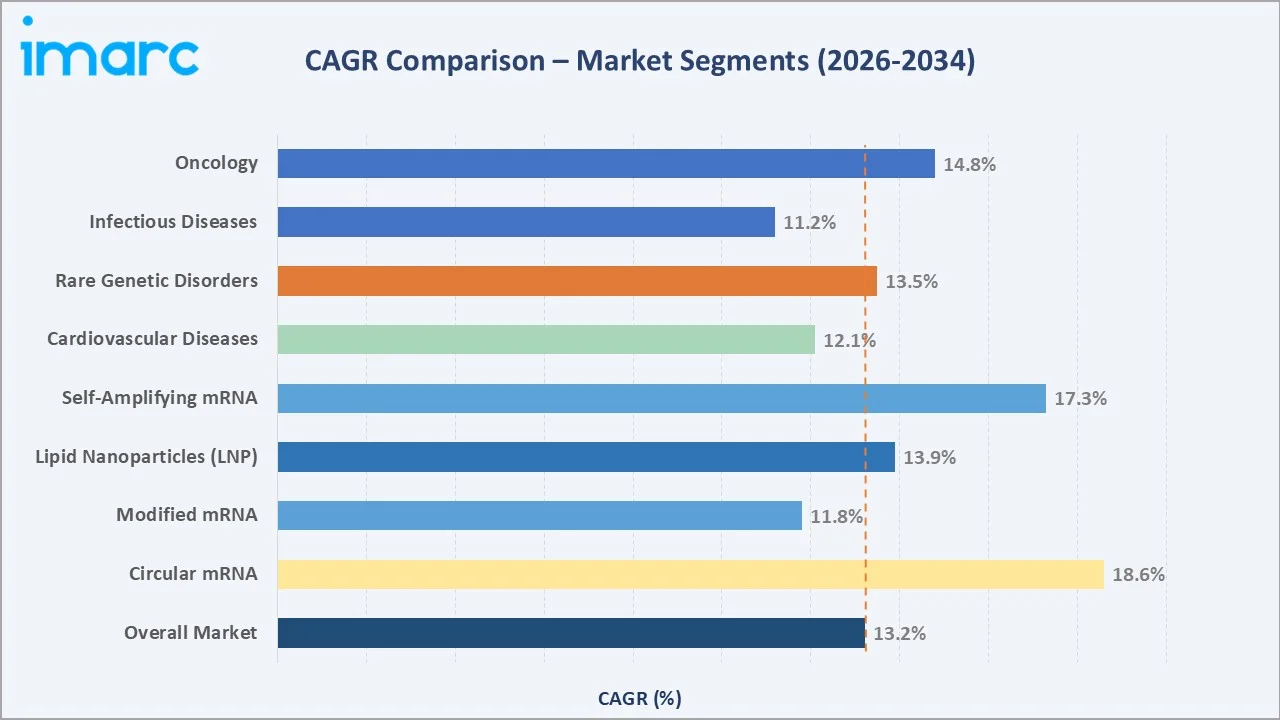

By application, Cancer (28.6%) is the second largest and fastest-expanding segment, driven by personalized mRNA cancer vaccine pipelines from Moderna and BioNTech. Gene Editing (18.4%) and Protein Replacement (14.6%) segments are gaining traction through advancing clinical programs.

North America (28.4%), Asia Pacific (22.3%), Latin America (8.4%), and Middle East & Africa (6.3%) complete the regional landscape. Key growth trends include AI-assisted mRNA sequence design, self-amplifying mRNA platforms, and expanded manufacturing capacity across emerging markets.

Key Market Insights

|

Insight |

Data |

|

Largest Application |

Infectious Disease – 38.4% 2025 |

|

Fastest Growing Segment |

Cancer mRNA Therapeutics |

|

Leading Region |

Europe – 34.6% 2025 |

|

Dominant Manufacturing Mode |

In-House – 64.3% 2025 |

|

Key Companies |

Moderna, BioNTech, Pfizer, CureVac, GSK, Arcturus |

|

Key Opportunity |

Personalized mRNA cancer vaccines |

Key Analytical Observations:

- Infectious Disease's 38.4% share 2025 reflects COVID-19 booster demand, RSV vaccine approvals, and expanding influenza mRNA programmes across major markets.

- Europe's 34.6% leadership reflects Germany's biotech ecosystem, the UK's personalized medicine programme, and the EU's strong regulatory framework for mRNA approvals.

- In-House manufacturing at 64.3% demonstrates major pharma's preference for proprietary mRNA production control, protecting IP and ensuring supply chain security.

Global mRNA Vaccines and Therapeutics Market Overview

mRNA vaccines and therapeutics leverage the body's cellular machinery to produce proteins that trigger immune responses or treat diseases. Developed into a platform technology during the COVID-19 pandemic by Moderna and Pfizer-BioNTech, mRNA now addresses oncology, rare diseases, and gene therapy applications.

In July 2025, NIST launched RGTM 10202 FLuc mRNA, a reference material for quality assessment of mRNA therapeutics, supporting standardization across labs. Growing investments in lipid nanoparticle delivery, self-amplifying mRNA platforms, and AI-assisted sequence design are broadening the mRNA vaccines market trends landscape.

Market Dynamics

To evaluate market opportunities, Request Sample

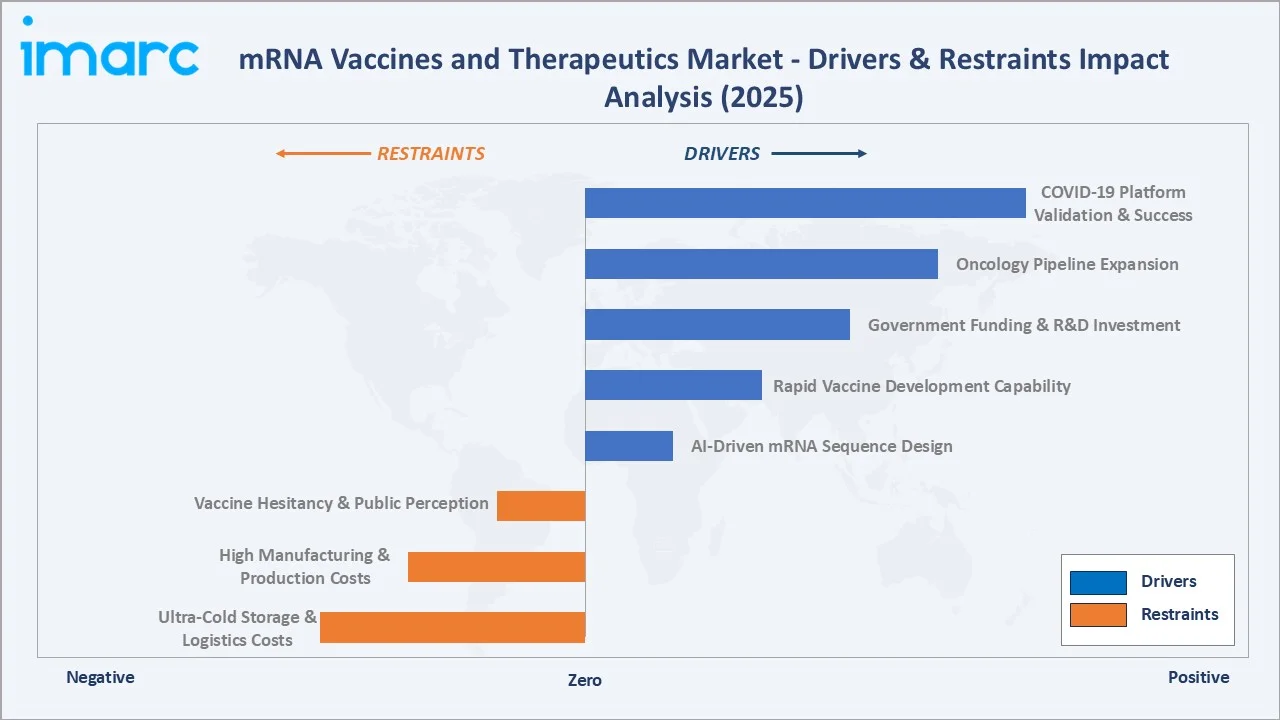

Market Drivers

- Growing Incidence of Chronic and Infectious Diseases: Rising cancer rates and re-emerging infectious diseases are fuelling demand for mRNA therapeutics. Cancer cases are expected to reach 35 million globally by 2050, driving personalized mRNA cancer vaccine development by Moderna and BioNTech.

- Advancements in Delivery Technology: LNP delivery system innovations are improving mRNA stability and cellular uptake. In August 2025, FDA approved Pfizer-BioNTech's LP.8.1-adapted COVID-19 vaccine, demonstrating evolving platform adaptability and regulatory confidence in mRNA delivery.

- Rising Demand for Personalized Medicine: mRNA's programmable nature enables patient-specific cancer vaccines. BioNTech's UK government collaboration targets personalized mRNA cancer immunotherapies for 10,000 patients by 2030, validating commercial personalized medicine pipeline expansion.

- Rapid Regulatory Approvals: Streamlined FDA, EMA, and PMDA pathways are accelerating mRNA product commercialization. The mRNA vaccines market outlook benefits from post-pandemic institutional trust in the platform's safety and efficacy profile across multiple indications.

Market Restraints

- Cold Chain Requirements: mRNA products require ultra-cold storage (-70°C to -20°C), raising distribution costs in low-resource regions and limiting market accessibility, particularly across Sub-Saharan Africa and Southeast Asia.

- High Development and Manufacturing Costs: BioNTech-Pfizer's mRNA vaccines cost USD 19.5 per dose in the United States, limiting bulk government procurement in emerging economies and restricting equitable global distribution of mRNA-based therapeutics.

Market Opportunities

- mRNA Cancer Vaccine Pipelines: Personalized oncology vaccines represent the highest-growth opportunity. Moderna's mRNA-4157 cancer vaccine demonstrated 44% reduction in melanoma recurrence risk in Phase 2b trials , opening a multi-billion-dollar precision oncology opportunity.

- Emerging Market Expansion: In December 2023, BioNTech opened an mRNA vaccine production facility in Rwanda, targeting African market access. Asia Pacific investment surges in Japan, India, and South Korea are expanding regional mRNA manufacturing capacity.

Market Challenges

- Intellectual Property Disputes: Ongoing patent conflicts between Moderna and Pfizer-BioNTech over COVID-19 mRNA vaccine technology create legal uncertainty, potentially restricting technology sharing and cross-licensing needed for next-generation product development.

- Public Hesitancy and Misinformation: Lingering vaccine hesitancy in certain demographics and misinformation about mRNA technology safety continue suppressing uptake in key markets, requiring sustained health communication investment.

Emerging Market Trends

The global mRNA vaccines market growth is being reshaped by three key converging trends that are redefining the product pipeline, delivery infrastructure, and competitive dynamics through 2034.

1. AI-Powered mRNA Sequence Design and Optimization

Artificial intelligence is transforming mRNA vaccine development by dramatically accelerating sequence optimization. Machine learning models now predict mRNA structure-stability relationships that previously required months of laboratory iteration. GenScript's May 2025 launch of GMP-like mRNA manufacturing services, designed for preclinical and IND-enabling research, underscores how digital-biology integration is shortening development timelines. AI-enabled codon optimization and secondary structure prediction are reducing immunogenicity while boosting translational efficiency. This trend is expected to halve development timelines for next-generation mRNA cancer vaccines.

2. Self-Amplifying mRNA (saRNA) Platform Emergence

Self-amplifying mRNA platforms enable lower dose levels by replicating within cells, reducing manufacturing requirements and enhancing cost efficiency. CSL Limited's November 2022 collaboration with Arcturus Therapeutics to access the late-stage saRNA vaccine platform marked a significant commercial validation. saRNA vaccines demonstrate equivalent immune responses at doses 10–100x lower than conventional mRNA, enabling mass production at markedly reduced cost per dose. This technology is emerging as a game-changer for pandemic preparedness programmes and emerging market vaccine access.

3. Expansion into Rare Genetic Diseases and Gene Therapy

mRNA therapeutics are advancing beyond infectious disease vaccines into rare genetic disorders and gene therapy. In September 2023, Moderna expanded mRNA research across oncology, respiratory, and rare diseases. Protein replacement therapy using mRNA now targets enzyme deficiency conditions previously reliant on expensive recombinant protein infusions. mRNA vaccines market trends show clinical programmes for cystic fibrosis, propionic acidaemia, and metabolic disorders entering Phase 2 trials. This diversification represents the next major market inflection, substantially broadening the mRNA therapeutic addressable market beyond vaccines.

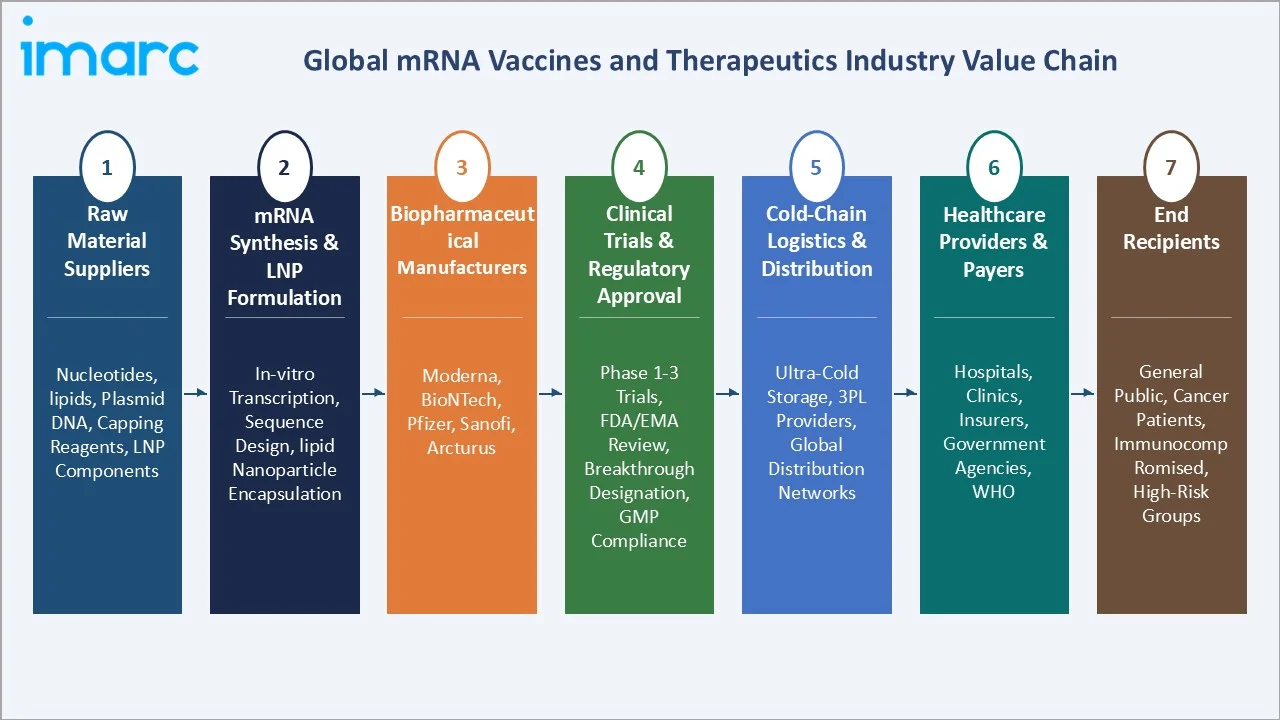

Industry Value Chain Analysis

The mRNA vaccines and therapeutics industry value chain encompasses six interconnected stages from raw material sourcing through to clinical and commercial delivery across global healthcare systems.

|

Stage |

Key Activities |

Representative Players |

|

Raw Material Sourcing |

Nucleoside procurement, lipid supply, capping reagents |

Thermo Fisher, Merck KGaA, Evonik |

|

mRNA Synthesis |

In vitro transcription, sequence design, purification |

GenScript, Lonza, Wacker Chemie |

|

LNP Formulation |

Lipid nanoparticle encapsulation, stability testing |

Acuitas Therapeutics |

|

Clinical Development |

Phase 1–3 trials, regulatory submissions, approvals |

Moderna, BioNTech, CureVac, Arcturus |

|

Manufacturing & Fill-Finish |

GMP production, vial filling, cold-chain packaging |

Lonza, Catalent |

|

Distribution & End-Use |

Cold-chain logistics, hospital/clinic administration |

Hospitals, Research Orgs, Clinics globally |

The LNP formulation and clinical development stages represent the primary value creation and IP concentration points, where proprietary delivery system innovations command significant pricing power and competitive differentiation across all major market participants.

Technology Landscape

Lipid Nanoparticle (LNP) Delivery Systems

LNPs remain the dominant mRNA delivery platform, protecting mRNA from degradation and enabling efficient cellular uptake. Ionizable lipids enable endosomal escape, facilitating cytoplasmic mRNA release. NIST's July 2025 RGTM 10202 FLuc mRNA reference material initiative is standardizing LNP assessment methods across global laboratories, accelerating regulatory harmonization for next-generation LNP-formulated mRNA therapeutics.

AI and Bioinformatics in Sequence Optimization

Machine learning platforms are now central to mRNA codon optimization, UTR design, and immunogenicity prediction. BioNTech's January 2023 acquisition of InstaDeep Ltd. strengthened its AI-powered drug discovery and mRNA design capabilities. These computational tools reduce mRNA design cycles from months to days, supporting rapid-response pandemic preparedness and personalized oncology vaccine development.

Manufacturing Scale-Up and GMP Technologies

Automated in vitro transcription bioreactors and continuous manufacturing platforms are reducing production costs. Many companies are expanding dedicated mRNA contract manufacturing facilities, addressing surging CDMO demand from oncology and rare disease mRNA pipeline holders.

Market Segmentation Analysis

IMARC Group provides an analysis of the key trends in each segment of the global mRNA vaccines and therapeutics market, along with forecasts at the global, regional, and country levels from 2026–2034. The market has been categorized based on vaccine manufacturing and application.

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Vaccine Type |

Conventional Non-Amplifying mRNA-Based Vaccines |

🔒 |

2025 |

|

Treatment Type |

Bioengineered Vaccine |

🔒 |

2025 |

|

Vaccine Manufacturing |

In-House |

64.3% |

2025 |

|

Application |

Infectious Disease |

38.4% |

2025 |

| End-User | Hospitals and Clinics | 🔒 | 2025 |

|

Region |

Europe |

34.6% |

2025 |

By Vaccine Manufacturing

To access detailed market analysis, Request Sample

In-House vaccine manufacturing dominates with a 64.3% share in 2025, as major pharmaceutical companies prioritize proprietary manufacturing control to protect mRNA IP, ensure quality oversight, and maintain supply chain flexibility. Moderna, BioNTech, and Pfizer have collectively invested over USD 8 Billion in dedicated in-house mRNA manufacturing infrastructure since 2020. Stringent regulatory requirements for GMP compliance and the need for rapid scale-up during outbreak scenarios further reinforce in-house manufacturing preference.

In February 2026, Ethris announced a strategic collaboration with the German Center for Infection Research (DZIF) to develop mRNA-based vaccines aimed at preventing and treating infectious diseases. The partnership combines Ethris’ proprietary mRNA and lipid nanoparticle technologies with DZIF’s expertise in translational vaccine research across a wide range of pathogens. As part of the agreement, DZIF will gain access to Ethris’ advanced mRNA platforms, while vaccine materials will be manufactured through industry partners to support research and clinical development. The collaboration focuses on advancing next-generation mRNA vaccines with improved stability, targeted delivery, and broader, more durable protection.

Out-Sourced manufacturing (35.7%) is expanding as CDMO capabilities improve, offering smaller biotech firms access to validated mRNA production without capital-intensive infrastructure investment.

By Application

Infectious Disease leads with a 38.4% share in 2025, reflecting ongoing COVID-19 booster programmes, RSV vaccine rollouts, and advancing influenza mRNA vaccine clinical programmes. In 2024, a total of 151 Zika virus disease (ZVD) cases were reported in India (from Maharashtra, Karnataka, and Gujarat States). Maharashtra reported 140 cases (125 cases from Pune), Karnataka 10 cases (7 cases from Bengaluru) and Gujarat 1 case (1 case from Gandhinagar) respectively. This epidemiological trend underscores a growing need for advanced and scalable vaccine technologies, thereby supporting demand in the mRNA vaccines and therapeutics market.

In August 2025, FDA approved Pfizer-BioNTech's LP.8.1-adapted COVID-19 vaccine, reinforcing the segment's commercial leadership.

Cancer (28.6%) is the fastest-growing application, driven by Moderna's mRNA-4157 cancer vaccine pipeline demonstrating clinical efficacy. Gene Editing (18.4%) and Protein Replacement (14.6%) reflect expanding mRNA applications into genetic diseases and enzyme-deficiency disorders, diversifying the market beyond infectious disease vaccines across the mRNA vaccines market forecast period.

Regional Market Insights

The global mRNA vaccines and therapeutics market exhibits distinct regional dynamics. Europe leads in revenue share and regulatory maturity, while Asia Pacific represents the highest-growth frontier opportunity through 2034.

Europe dominates with a 34.6% revenue share (2025), anchored by Germany's world-leading mRNA biotechnology ecosystem, home to BioNTech SE and CureVac, combined with the UK's NHS-backed personalised cancer vaccine programme. The European Medicines Agency's adaptive licensing pathways and substantial EU Horizon Europe funding for mRNA research are reinforcing regional leadership in mRNA vaccines market growth.

North America holds a 28.4% market share (2025), led by the United States as home to Moderna, Pfizer, and Arcturus Therapeutics. Expanding oncology clinical programmes are driving next-phase market momentum.

Competitive Landscape

The global mRNA vaccines and therapeutics competitive landscape is led by a concentrated group of multinational pharmaceutical and biotechnology companies, with Moderna, BioNTech, and Pfizer collectively accounting for the majority of current market revenues.

|

Company |

Position |

Key Product |

Primary Strategy |

|

Moderna, Inc. |

Global Leader |

Spikevax, mRNA-4157 |

Oncology pipeline, platform diversification |

|

BioNTech SE |

Global Leader |

Comirnaty, BNT111, BNT122 |

Personalized cancer vaccines, AI-guided neoantigen design |

|

Pfizer Inc. |

Global Leader |

Comirnaty |

Distribution scale, BioNTech partnership, next-gen COVID vaccines |

|

GSK plc |

Established |

mRNA flu pipeline |

Full control via CureVac licensing agreement (July 2024); respiratory mRNA focus |

|

Arcturus Therapeutics |

Innovator |

KOSTAIVE/ ARCT-154 (sa-mRNA) |

Self-amplifying mRNA (sa-mRNA), CSL Seqirus collaboration; first approved sa-mRNA COVID vaccine (EU, 2025) |

|

Sanofi |

Established |

mRNA flu vaccine, mRNA respiratory pipeline |

$3.2B Translate Bio acquisition; mRNA Center of Excellence; modified mRNA platform for flu, chlamydia, and respiratory diseases |

|

Merck & Co. |

Established |

mRNA-4157/V940 + KEYTRUDA |

Co-development with Moderna on personalized mRNA cancer vaccine |

The key companies include Arcturus Therapeutics, Inc., BioNTech SE, GSK plc, Moderna, Inc., Pfizer Inc., Sanofi, Merck & Co., and others.

Key Company Profiles

Moderna, Inc.

Moderna is the world's leading independent mRNA company, operating a fully integrated platform from sequence design through clinical development, manufacturing, and global distribution of mRNA vaccines and therapeutics.

- Product Portfolio: Spikevax (COVID-19), mRESVIA (RSV), influenza mRNA vaccine, and rare disease pipeline including mRNA-3927.

- Recent Developments: In September 2023, expanded mRNA research pipeline into oncology, respiratory, and rare diseases. mRNA-4157 demonstrated 49% reduction in melanoma recurrence risk in Phase 2b combination with Keytruda.

- Strategic Focus: Platform diversification beyond COVID-19 into oncology, respiratory, and rare genetic diseases; manufacturing scale-up; and AI-accelerated sequence design capabilities.

BioNTech SE

BioNTech is Germany's leading mRNA biotechnology company, renowned for pioneering the Comirnaty COVID-19 vaccine in partnership with Pfizer and advancing the world's most extensive personalised cancer mRNA pipeline.

- Product Portfolio: Comirnaty (COVID-19), BNT111 (melanoma), BNT122, mRNA-4157 (personalised cancer), and infectious disease mRNA pipeline including RSV and malaria.

- Recent Developments: January 2023 collaboration with UK government for personalised mRNA cancer immunotherapies targeting 10,000 patients by 2030; InstaDeep acquisition bolstering AI-powered drug design.

- Strategic Focus: Immuno-oncology leadership, AI-driven mRNA design, African manufacturing expansion via Rwanda facility, and personalised medicine at scale.

Sanofi

Sanofi is a global biopharmaceutical leader that has made a significant strategic commitment to mRNA technology through its $3.2 billion acquisition of Translate Bio in 2021, establishing one of the largest privately owned lipid nanoparticle (LNP) libraries and a dedicated mRNA Center of Excellence to accelerate next-generation vaccine development.

- Product Portfolio: mRNA seasonal influenza vaccine (Phase 2), mRNA-based COVID-19 booster candidates, early-stage mRNA programs targeting chlamydia, respiratory syncytial virus (RSV), and acne; rare pulmonary disease therapeutics leveraging the Translate Bio platform.

- Recent Developments: Launched mRNA Center of Excellence in 2021 integrating Translate Bio's platform with Sanofi Pasteur's antigen design and manufacturing expertise. On track to advance multiple mRNA clinical trials across infectious diseases. Transitioned to modified mRNA (modRNA) platform for improved immunogenicity and tolerability.

- Strategic Focus: Building a fully proprietary modified mRNA platform beyond COVID-19; targeting infectious diseases with high unmet medical need; leveraging Translate Bio's LNP delivery expertise for both vaccine and therapeutic applications; and scaling modRNA manufacturing capabilities for global supply.

Merck & Co.

Merck & Co., known as MSD outside the United States and Canada, is one of the world's largest biopharmaceutical companies, whose mRNA strategy centres on its equal co-development and co-commercialisation partnership with Moderna for the individualised neoantigen therapy mRNA-4157 (V940) — branded intismeran autogene — in combination with its blockbuster anti-PD-1 immunotherapy KEYTRUDA (pembrolizumab).

- Product Portfolio: mRNA-4157/V940 (intismeran autogene) is an mRNA-based individualised neoantigen therapy encoding up to 34 patient-specific neoantigens, designed and produced based on the unique mutational signature of the patient's tumour DNA.

- Recent Developments: In February 2023, the FDA granted Breakthrough Therapy Designation to mRNA-4157/V940 in combination with KEYTRUDA for the adjuvant treatment of patients with high-risk melanoma following complete resection, based on data from the Phase 2b KEYNOTE-942 trial.

- Strategic Focus: As KEYTRUDA faces patent expiry in 2028, Merck has pivoted to a multimodality, diversified oncology pipeline structured around three pillars — improving immune responses (led by mRNA-4157), targeted tumour-killing therapies, and precision targeting — with mRNA-4157 described as the "star of the show" in the immune response pillar.

Market Concentration Analysis

The global mRNA vaccines and therapeutics market is moderately concentrated. Moderna, Pfizer-BioNTech, and CureVac-GSK collectively account for approximately 64% of current market revenues, primarily through COVID-19 vaccine sales and booster programmes.

The oncology and rare disease segments exhibit greater fragmentation, with dozens of biotech firms operating early-to-mid stage mRNA therapeutic programmes. Consolidation through strategic partnerships and licensing is expected to increase as programmes progress to commercialization through 2034.

Investment & Growth Opportunities

Fastest Growing Segments

mRNA cancer vaccines and rare genetic disease therapeutics represent the highest-growth investment vectors through 2034. Personalized oncology, including mRNA-4157 and BNT122, addresses a total addressable market exceeding USD 12 Billion by 2034 as trial programmes progress to approval.

Emerging Market Expansion

Asia Pacific is the fastest-growing region. Japan, South Korea, and India represent high-growth opportunities for mRNA vaccine manufacturers seeking regional manufacturing partnerships. Africa's nascent mRNA capacity, led by BioNTech's Rwanda facility, opens large-population markets previously inaccessible to premium mRNA products.

Technology and Innovation Investment Trends

- Self-amplifying mRNA (saRNA) platforms enabling lower-dose vaccines are attracting significant investment from vaccine developers and CDMOs seeking manufacturing cost advantages in high-volume outbreak scenarios.

- AI and computational biology platforms for mRNA sequence optimization represent critical investment targets, enabling 10x acceleration of vaccine design and broader pipeline breadth across therapeutic areas.

- Lipid nanoparticle delivery system innovation, including organ-targeted and extrahepatic delivery, is a key differentiation frontier, with companies like Acuitas and Precision NanoSystems attracting venture and pharma partnership investment.

Future Market Outlook (2026-2034)

The global mRNA vaccines and therapeutics market is positioned for sustained growth through 2034, anchored by oncology pipeline commercialisation, self-amplifying mRNA platform adoption, and expanding therapeutic applications into gene therapy and rare diseases.

Product innovation will remain the primary competitive battleground. Firms navigating the transition from infectious disease vaccine revenues to diversified oncology and genetic disease therapeutic revenues will define the next phase of market leadership. Personalised mRNA cancer vaccines entering commercial markets by 2027–2029 represent the highest near-term revenue inflection opportunity.

Research Methodology

Primary Research

Primary research for this report included structured interviews with industry participants across pharma companies, CDMO operators, regulatory consultants, hospital pharmacies, and research institutions across North America, Europe, and Asia Pacific during 2024–2025.

Secondary Research

Secondary research encompassed comprehensive review of regulatory filings, company press releases, WHO/FDA/EMA public disclosures, clinical trial databases (ClinicalTrials.gov), trade publications, and government healthcare expenditure datasets. Over 200 secondary sources were reviewed.

Forecasting Methodology

Market size estimations used a combination of top-down demand analysis incorporating epidemiological disease burden data and bottom-up pipeline commercialization modelling, triangulated against clinical trial phase progression and pricing intelligence from regulatory filings.

mRNA Vaccines and Therapeutics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Vaccine Types Covered | Self-amplifying mRNA-Based Vaccines, Conventional Non-Amplifying mRNA-Based Vaccines |

| Treatment Types Covered | Bioengineered Vaccine, Gene Therapy, Gene Transcription, Cell Therapy, Monoclonal Antibody, Others |

| Vaccine Manufacturings Covered | In-House, Out-Sourced |

| Applications Covered | Cancer, Infectious Disease, Gene Editing, Protein Replacement |

| End-Users Covered | Hospitals and Clinics, Research Organizations, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Moderna, Inc., BioNTech SE, Pfizer Inc., GSK plc, Arcturus Therapeutics, Sanofi, Merck & Co., etc |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the mRNA vaccines and therapeutics market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global mRNA vaccines and therapeutics market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the mRNA vaccines and therapeutics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the mRNA Vaccines and Therapeutics Market Report

The global mRNA vaccines and therapeutics market was valued at USD 60.58 Billion in 2025.

The mRNA vaccines and therapeutics market is projected to exhibit a CAGR of 2.30% during 2026-2034, reaching USD 75.11 Billion by 2034.

Key drivers include the growing incidence of cancer and infectious diseases, advancements in LNP delivery systems and synthetic biology, rising demand for personalized medicine, and favourable regulatory pathways supporting rapid mRNA product approvals globally.

Europe currently dominates the mRNA vaccines and therapeutics market, accounting for a share of 34.6% in 2025, driven by Germany's mRNA biotech ecosystem (BioNTech, CureVac), UK's personalised medicine programme, and strong EU regulatory frameworks.

Some of the major players in the mRNA vaccines and therapeutics market include Arcturus Therapeutics, Inc., BioNTech SE, GSK plc, Moderna, Inc., Pfizer Inc., Sanofi, Merck & Co., and others.

Key challenges include cold-chain storage requirements, high production costs, scalability constraints, and concerns related to long-term safety and stability of mRNA formulations.

mRNA technology is increasingly being explored for applications such as cancer immunotherapy, rare genetic disease treatment, protein replacement therapies, and regenerative medicine.

Ongoing advancements in delivery systems (such as lipid nanoparticles), sequence optimization, and manufacturing processes are improving efficacy, stability, and accessibility, thereby expanding the scope and commercialization potential of mRNA-based solutions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)