Nanocellulose Market Size, Share, Trends and Forecast by Product Type, Application, and Region, 2026-2034

Nanocellulose Market Size and Share:

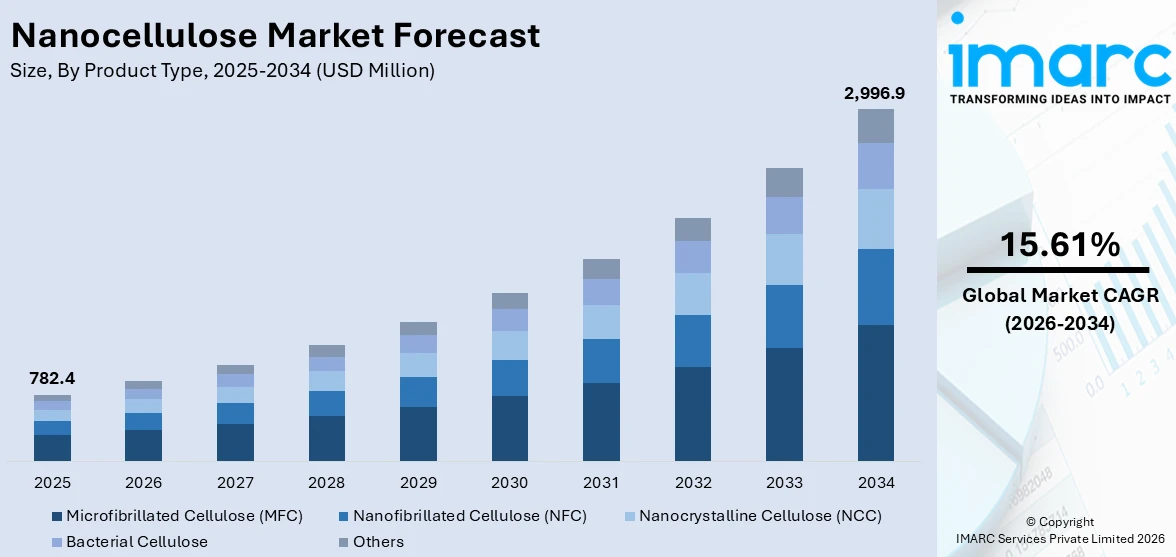

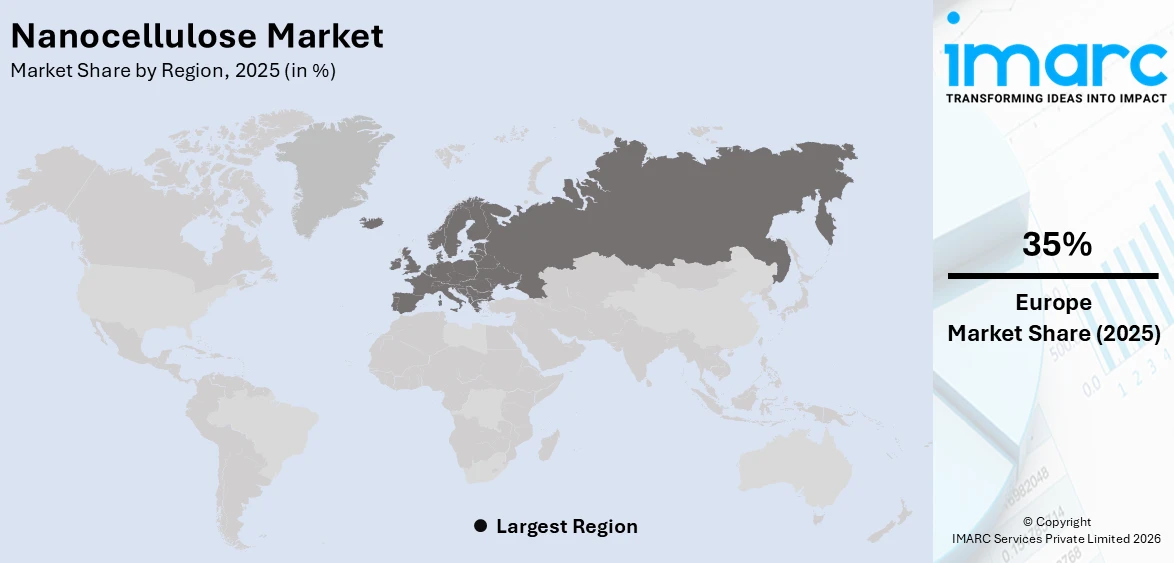

The global nanocellulose market size was valued at USD 782.4 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 2,996.9 Million by 2034, exhibiting a CAGR of 15.61% during 2026-2034. Europe currently dominates the market, holding a market share of over 35% in 2025. The market is driven by increased need for biodegradable and sustainable materials, propelling innovation in various sectors, from packaging to electronics, automotive, and healthcare. Nanocellulose is high-strength, lightweight, and highly functional, which makes it a great candidate for composites, films, and biomedical purposes. Emerging product introductions, such as injectable hydrogels for medical devices, exemplify its growing potential, responsible for the gradual growth of nanocellulose market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 782.4 Million |

|

Market Forecast in 2034

|

USD 2,996.9 Million |

| Market Growth Rate 2026-2034 | 15.61% |

The global need for eco-friendly and sustainable material is a key driving force for the nanocellulose market. With industries focusing more on minimizing environmental footprint, nanocellulose is a versatile substitute to traditional materials that has better strength, lightness, and biodegradability. Its end uses cover all manner of industries, ranging from packaging, electronics, automobile, and healthcare, where its potential for enhancing mechanical properties and stability gains great importance. Moreover, pressures from regulations towards using renewable and non-toxic materials further drive its use. Manufacturers and researchers are putting efforts into innovation to improve production techniques, lower cost, and increase the applicability of nanocellulose towards future composites and coatings. Global awareness of climate change and the demand for circular economy applications are underpinning investments in nanocellulose technology. These combined factors make up for the steady expansion of the market, with nanocellulose becoming a fundamental material for the shift towards sustainable industrial processes.

To get more information on this market Request Sample

Increased demand in the paper and packaging sectors in the United States is fueling growth in the nanocellulose market with a share if 81% in 2024. Manufacturers are progressively adding nanocellulose to paper and board products to increase strength, lighten the load, and become more recyclable, following sustainability objectives and regulatory standards. Also, the increasing emphasis on high-tech healthcare uses, such as wound care, drug delivery systems, and tissue engineering, is supporting uptake. The biocompatibility and functional versatility of nanocellulose mean that it is a sought-after material for medical equipment and pharmaceutical formulations. As per sources, in October 2024, UPM Biomedicals launched FibGel™, the global’s first injectable nanocellulose hydrogel for medical devices, providing a sustainable, biocompatible solution for applications in soft tissue repair and regenerative medicine. Moreover, research programs funded by public and private agencies are increasingly driving innovation, encouraging new applications in coatings, films, and composites designed for U.S. industrial requirements. The focus on minimizing the environmental impact, along with growing consumer interest in sustainable materials, has been a driving force in several sectors. These efforts taken together form a positive atmosphere that facilitates steady market growth and the use of nanocellulose in the United States.

Nanocellulose Market Trends:

Growing Demand for Bio-Based and Sustainable Materials

The increasing demand for sustainable and bio-based materials across industries such as paper and packaging, healthcare, and cosmetics is a major driver of growth in the nanocellulose market trend. Consumers are becoming more aware of the environmental footprint of what they buy, and according to a 2024 U.S. survey, 80% of consumers would be willing to pay more for environmentally friendly products. This realignment of customer choice is accompanied by strict government policies prohibiting non-biodegradable packaging, especially for food and beverages, forcing manufacturers to shift to long-lasting and light materials. Nanocellulose products are catching on as they are sustainable without compromising on performance levels. Fast adoption of these materials in sheet form for windows and electrical displays is opening up new sources of income. Further, increasing industrial use of bio-based materials is indicative of an amplifying trend towards sustainable manufacturing. Overall, these drivers are propelling the market towards huge growth while encouraging sustainability across industries.

Technological Advancements and Sophisticated Applications

Nanocellulose technological improvements in the process and application areas are significantly influencing market forces and opening new avenues. Nanocellulose sensors are increasingly being used to scan bridges, buildings, and other vital infrastructure, delivering accurate stress and structural integrity measurements. This technology has opened up the material's use from conventional packaging into engineering and construction. In medicine, nanocellulose's high adsorption value and non-toxicity make it a perfect ingredient in wound dressings and sanitary materials, contributing enhanced safety and efficiency. In addition, improvements in manufacturing technologies, such as increased efficiency of paper machines and filler content, are making it possible to produce high-quality materials at lower costs and waste. Combining digital monitoring, automated systems, and process control advancements is also enhancing industrial uptake. These technological developments are driving product flexibility, stimulating growth in multiple end-use markets, and placing nanocellulose on the strategic material map for both industrial and consumer-driven applications.

Industrialization, Regulatory Assistance, and Market Growth

Industrialization coupled with regulatory assistance remain critical driving forces in expanding the market. Industrial development, as pointed out by the United Nations Industrial Development Organization with a 2.3% global rise in 2023, reflects continued investment in manufacturing, construction, and other industries, further enhancing demand for adaptable and sustainable materials. Simultaneously, increasing concern for the adverse environmental impacts of single-use plastics has stimulated the uptake of biodegradable and bio-based materials in packaging, healthcare, and consumer goods. Significant R&D efforts are also further improving product performance and enabling new markets, especially in construction, electrical, and sanitary applications. Governments globally are implementing policies and incentives in favor of sustainable materials and environmentally friendly manufacturing processes, which are fueling market penetration. The synergy of industrial development, regulatory support, and expanded R&D guarantees that the market is dynamic, resilient, and set for long-term growth, addressing changing industrial and consumer demands while ensuring sustainability.

Nanocellulose Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global nanocellulose market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product type, and application.

Analysis by Product Type:

- Nanofibrillated Cellulose (NFC)

- Nanocrystalline Cellulose (NCC)

- Bacterial Cellulose

- Microfibrillated Cellulose (MFC)

- Others

Microfibrillated cellulose (MFC) represented a strong 40% in 2025 of the global nanocellulose market growth due to its amplifying usage as a high-performance and eco-friendly material. The extremely fibrillated nature of MFC gives excellent mechanical strength, flexibility, and lightness, which makes MFC an ideal material for use in applications from packaging to composites. Its large surface area enables better compatibility with other polymers, leading to product improvement and durability. MFC is also highly regarded for being environmentally friendly, providing a substitute for synthetic fibers and reinforcing agents and promoting circularity efforts. The aqueous system compatibility of the material promotes innovative formulation in coatings, adhesives, and biomedicine. Companies are increasingly relying on MFC to enhance tensile strength, barrier properties, and production efficiency overall. As concern for sustainability increases, MFC is expected to be a top product form in the nanocellulose market, helping to spur innovation in green production and material use with high performance globally.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Pulp and Paperboard

- Composites

- Pharmaceuticals and Biomedical

- Electronics

- Food and Beverages

- Others

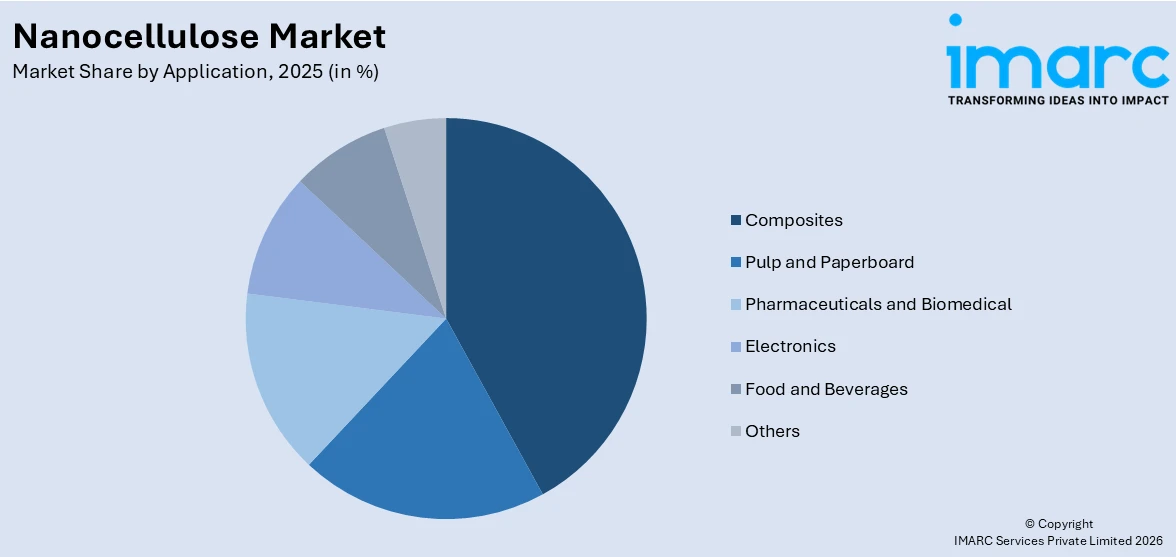

Composites dominate the nanocellulose market, holding a substantial 42% share. This leadership is driven by their exceptional mechanical strength, lightweight properties, and biodegradability, making them ideal for automotive, construction, and packaging applications. Growing demand for sustainable and high-performance materials further fuels market growth, as industries increasingly adopt nanocellulose composites to enhance product durability, efficiency, and environmental compliance.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Europe represented 35% in 2025 of the global nanocellulose market outlook, highlighting the continent's leading position in sustainable material uptake and industrial development. The European emphasis on green production, policy support, and high-tech research facilities has spurred adoption of nanocellulose in industries including packaging, automotive composites, and coatings. The renewable and biodegradable characteristics of the material complement environmental regulations and consumer demand for eco-friendly products. Cooperative research projects and pilot-scale production have helped the creation of region-specific nanocellulose products in response to local industrial requirements. Moreover, Europe's focus on the circular economy supports applications that minimize waste and maximize resource efficiency. The region's lead in proactive efforts guarantees ongoing development of nanocellulose technology and market growth. By integrating sustainability with high-performance characteristics, Europe retains its central position in formulating the global nanocellulose market forecast and influencing long-term uptake across various industries.

Key Regional Takeaways:

United States Nanocellulose Market Analysis

The United States nanocellulose market is dominated by increasing awareness and demand for sustainable, biodegradable, and renewable products. This is driving the uptake of nanocellulose widely in various industries. As companies look for alternatives to petrochemical-based products, nanocellulose presents a strong alternative because of its high strength-to-weight ratio, biodegradability, and availability from renewable sources like wood pulp. The packaging sector, in fact, is looking towards nanocellulose for its ability to create environment-friendly, lightweight, and high-barrier packaging materials. Also, the need for lightweight and tough materials for automotive and aerospace applications is further adding to the market potential of nanocellulose, especially with rising fuel efficiency requirements. For example, in June 2024, the United States Department of Transportation's (USDOT) National Highway Traffic Safety Administration released new fuel efficiency standards for vehicles that are expected to save consumers in the United States more than USD 23 Billion on fuel costs. According to this new rule, the fuel economy of passenger cars will increase by 2% per year for model years 2027–2031, and that of light trucks will boost by 2% per year for model years 2029–2031. By model year 2031, these increases are expected to lift the average light-duty vehicle fuel economy to approximately 50.4 miles per gallon. Apart from this, government patronage of sustainable innovation and higher research and development (R&D) investment are also playing a significant role in business growth.

Asia Pacific Nanocellulose Market Analysis

The Asia Pacific nanocellulose market is expanding due to rapid industrialization, growing environmental awareness, and strong demand for sustainable materials across diverse sectors. For instance, the Index of Industrial Production (IIP) in India recorded a growth of 2.9% in February 2025, highlighting the robust industrialization rate across the country, as per the Press Information Bureau (PIB). Moreover, countries such as Japan, China, and South Korea are investing heavily in advanced material research, fostering innovation in nanocellulose applications ranging from packaging and electronics to automotive and construction. Rising concerns over plastic pollution and increasing government regulations promoting eco-friendly alternatives are also propelling the shift toward biodegradable and renewable materials. For instance, with approximately 9.3 Million Tonnes of plastic waste every year, India accounts for 20% of plastic waste generated globally, as per a 2024 industry report. Besides this, strong collaboration between academic institutions, government agencies, and private companies further supports research and development (R&D) and commercialization efforts.

Europe Nanocellulose Market Analysis

The growth of the Europe nanocellulose market is largely driven by strong regulatory support for sustainable materials, coupled with the region's ambitious environmental goals and circular economy initiatives. With increasing pressure to reduce greenhouse gas emissions and reliance on fossil-based products, industries across Europe are actively seeking eco-friendly alternatives, positioning nanocellulose as a promising solution. According to reports, greenhouse gas emissions in the European Union recorded a decrease of 2.6% in Q2 2024 in comparison to Q2 2023. Moreover, the biodegradability and renewability of nanocellulose make it highly attractive for applications in packaging, particularly in countries with stringent single-use plastic bans. Additionally, the well-established pulp and paper industry in Europe provides a robust raw material base for nanocellulose production, enabling cost-effective scaling. According to a 2023 report by the Confederation of European Paper Industries, the pulp and paper industry in Europe generates 100 Billion Euros in revenue and contributed 20 Billion Euros to the EU’s GDP. Innovation is further supported by significant public and private investment in green technologies, fostering research into advanced nanocellulose applications in fields such as automotive components, building materials, cosmetics, and biomedical products. European research institutions and companies are also exploring nanocellulose-based aerogels, foams, and membranes for applications in water purification, filtration, and energy storage, further supporting market growth.

Latin America Nanocellulose Market Analysis

The Latin America nanocellulose market is experiencing robust growth due to the region’s rich natural resources, particularly its vast forest reserves, which provide an abundant and sustainable source of raw materials. For instance, 60% of Brazil’s land area was covered with natural forest in 2020, equating to 511Mha of natural forest, as per the Global Forest Watch. Moreover, growing interest in renewable and biodegradable products is encouraging industries to explore nanocellulose as an alternative to conventional plastics and synthetic materials. Countries such as Brazil and Chile are advancing in bioeconomy initiatives, promoting research and development (R&D) in green technologies. Besides this, government support for sustainable practices and rising export opportunities for eco-friendly products are also helping to stimulate market growth.

Middle East and Africa Nanocellulose Market Analysis

The Middle East and Africa nanocellulose market is significantly influenced by growing efforts to diversify economies, reduce dependence on oil, and invest in sustainable technologies. As countries in the region seek to develop green industries, nanocellulose is gaining attention for its potential in water treatment, packaging, construction, and agriculture. Water scarcity challenges are also prompting interest in nanocellulose-based filtration systems due to their efficiency and eco-friendliness. For instance, the annual absolute water scarcity per capita in Saudi Arabia is 500 cubic meters. Other than this, the construction sector is increasingly exploring nanocellulose-enhanced materials to improve durability and sustainability in building projects. Abundant agricultural residues across parts of Africa also present opportunities for cost-effective nanocellulose production.

Competitive Landscape:

The competitive environment of the nanocellulose market is determined by persistent innovation, technological developments, and diversification of applications across industry. Firms are concentrating on creating high-performance, sustainable products to capture increasing demand in areas like packaging, healthcare, construction, and electronics. Strategic research and development investments, and collaborations with material science and engineering professionals, are allowing players to increase their product offerings and improve process efficiencies. Production method innovation, such as enhanced filler content, energy-saving manufacturing, and being embedded with digital monitoring systems, is emerging as a differentiator. Further, growing use in niche applications like sensors, wound management, and eco-friendly packaging is driving competitive positioning. All these are driving a solid growth environment in which agility, technological competency, and product diversity define market leadership. In general, the nanocellulose market outlook indicates continued growth fueled by innovation and solutions-based offerings for industries.

The report provides a comprehensive analysis of the competitive landscape in the nanocellulose market with detailed profiles of all major companies, including:

- Borregaard AS

- Cellucomp Ltd

- CelluForce

- FiberLean Technologies Ltd

- GranBio Technologies

- Kruger Inc.

- Nippon Paper Industries Co. Ltd.

- Oji Holdings Corporation

- Sappi Ltd

- Stora Enso Oyj

Latest News and Developments:

- July 2025: A team of researchers headed by the Bioeconomy Science Institute's AgResearch Group announced plans to launch a biotechnology experiment into space in order to manufacture sophisticated biomaterials using just sunlight and bacteria. The initiative will primarily focus on the production of bacterial nanocellulose (BNC).

- July 2025: The Korvaa Consortium officially introduced its innovative concept shoe made from bacterial nanocellulose, mycelium, and biodegradable plastics at the 2025 Future Fabrics Expo in London. The design of the concept shoe demonstrates the viability of sustainable materials replacing traditional materials in intricate applications such as footwear.

- June 2025: AgriSea and Crown Research Institute Scion announced the launch of a seaweed biorefinery near Paeroa for the production of sustainable nanocellulose. The innovative biorefinery is expected to turn waste seaweed into valuable, environmentally friendly commodities with a global reach.

- February 2025: Modern Synthesis, a London-based manufacturer of biomaterials made from nanocellulose, successfully raised USD 5.5 Million in its latest funding round. The capital will be utilized to transform conventional production methods and have significant, large-scale effects.

- February 2025: Gozen officially launched its LUNAFORM range of short films. LUNAFORM is a nanocellulose biomaterial manufactured using the controlled fermentation method and supported by the company’s innovative BioCraft technology.

Nanocellulose Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Nanofibrillated Cellulose (NFC), Nanocrystalline Cellulose (NCC), Bacterial Cellulose, Microfibrillated Cellulose (MFC), Others |

| Applications Covered | Pulp and Paperboard, Composites, Pharmaceuticals and Biomedical, Electronics, Food and Beverages, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Borregaard AS, Cellucomp Ltd, CelluForce, FiberLean Technologies Ltd, GranBio Technologies, Kruger Inc., Nippon Paper Industries Co. Ltd., Oji Holdings Corporation, Sappi Ltd, Stora Enso Oyj, etc.. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the nanocellulose market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global nanocellulose market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the nanocellulose industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Nanocellulose Market Report

The nanocellulose market was valued at USD 782.4 Million in 2025.

The nanocellulose market is projected to exhibit a CAGR of 15.61% during 2026-2034, reaching a value of USD 2,996.9 Million by 2034.

The market for nanocellulose is mainly fueled by the amplifying use of sustainable and biodegradable materials by various industries. Its application increases strength, lightness, and barrier properties in packaging, composites, and pulp. Moreover, boosting demand for eco-friendly substitutes, development in production processes, and the widening range of applications in automotive, construction, and biomedical fields are further driving market growth internationally.

Europe currently dominates the nanocellulose market, accounting for a share of 35%. This dominance is complemented by stringent environmental regulations, high priority on green manufacturing, and sophisticated research and development infrastructure. Market adoption extends across packaging, pulp and paper, and composites, as increasing partnerships and pilot programs add further strength to Europe as the biggest and most dominant nanocellulose market in the global.

Some of the major players in the nanocellulose market include Borregaard AS, Cellucomp Ltd, CelluForce, FiberLean Technologies Ltd, GranBio Technologies, Kruger Inc., Nippon Paper Industries Co. Ltd., Oji Holdings Corporation, Sappi Ltd, Stora Enso Oyj, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)