Nanomedicine Market Size, Share, Trends and Forecast by Nanomolecule Type, Product, Application, and Region, 2026-2034

Nanomedicine Market Size and Share:

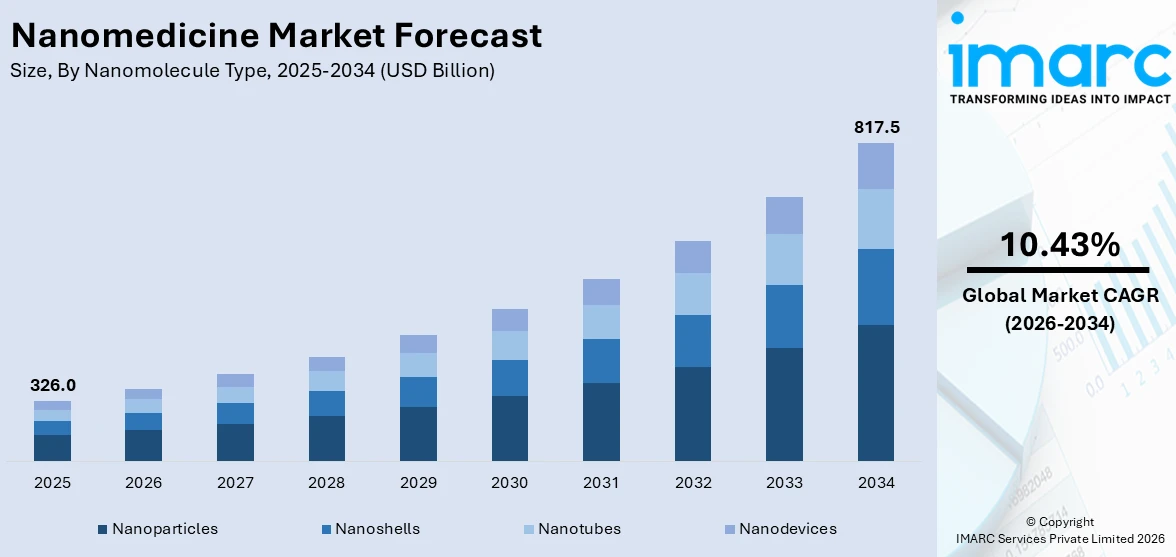

The global nanomedicine market size was valued at USD 326.0 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 817.5 Billion by 2034, exhibiting a CAGR of 10.43% during 2026-2034. North America currently dominates the market, holding a significant market share of 49.9% in 2025. The rising demand for targeted drug delivery, advancements in nanotechnology, increased prevalence of chronic diseases, expanding applications in diagnostics and therapeutics, and growing investments in research and development to create more effective, personalized, and minimally invasive medical treatments are some of the major factors fueling the nanomedicine market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 326.0 Billion |

|

Market Forecast in 2034

|

USD 817.5 Billion |

| Market Growth Rate 2026-2034 | 10.43% |

The market for nanomedicine is primarily fueled by advancements in nanotechnology and its growing integration into healthcare applications. The development of targeted drug delivery systems has increased the benefits of medical treatments and decreased the side effects mainly seen in cancers and heart and brain conditions. With the growing number of people having chronic diseases, the search for better treatments becomes more important. In addition, the use of nanotechnology for diagnostics, regenerative medicine and imaging is increasing, improving both early finding of diseases and tailored care. The economic growth of the market is supported by greater activity from both public and private sectors in nanomedicine research and development (R&D). Because of general support from regulators and new drug studies, nanomedicine is becoming a crucial aspect of future medical solutions globally.

To get more information on this market Request Sample

The nanomedicine market growth in the United States is propelled by advancements in nanotechnology, which have facilitated the development of targeted drug delivery systems and enhanced treatment efficacy and reducing side effects. The rising prevalence of chronic diseases, like cardiovascular conditions and cancer, has amplified the demand for innovative therapeutic solutions. According to the NIH, in 2025, approximately 2,041,910 new cancer cases are likely to be identified in the United States, with 618,120 individuals succumbing to the illness. Substantial investments from private and public sectors support extensive research and development (R&D) activities, fostering innovation in the field. The U.S. Food and Drug Administration (FDA) provides a favorable regulatory environment that facilitates the approval and commercialization of nanomedicine products. Additionally, the growing emphasis on personalized medicine and early disease detection has expanded the applications of nanotechnology in diagnostics and therapeutics, further driving market growth.

Nanomedicine Market Trends

Advancements in Nanotechnology

Ongoing innovations in nanotechnology are a primary force behind the expansion of the nanomedicine market. Researchers have developed nanoscale materials and devices that enable precise drug delivery, targeted therapy, and enhanced imaging techniques. These breakthroughs improve therapeutic outcomes by minimizing side effects and increasing treatment accuracy. Nanoparticles, liposomes, dendrimers, and nanorobots are being engineered for applications ranging from cancer treatment to tissue repair. The miniaturization of diagnostic tools has also made real-time monitoring and early disease detection more effective. As nanotechnology continues to evolve, it opens new possibilities for complex disease management, providing healthcare professionals with more refined, less invasive tools. According to the nanomedicine market forecast, these innovations are central to the increasing adoption and investment in nanomedicine across the healthcare industry. For instance, in May 2025, Nanoworx B.V., a nanomedicine-focused contract research organization, provided its extensive service portfolio for partners in academia and business. Nanoworx, a company established in Eindhoven, the Netherlands, advances the design, development, and scalability of nanoparticle-based solutions by utilizing cutting-edge machinery and extensive experience.

Growing Investments in Research and Development

Significant investments from both public and private sectors are fueling advancements in nanomedicine. Governments, research institutions, and pharmaceutical companies are allocating substantial funding to develop novel nanotechnology-based therapies, diagnostics, and drug delivery systems. These investments accelerate innovation and the transition of nanomedicine from the lab to clinical applications. Collaborations among universities, biotech firms, and healthcare providers are promoting interdisciplinary research, leading to new discoveries and faster commercialization of products. Moreover, venture capital support for nanotech startups is helping to bring early-stage innovations to market. This robust funding environment enables continued exploration of nano-based solutions for unmet medical needs, positioning nanomedicine as a key area of growth and technological leadership within the global healthcare landscape. For instance, in April 2024, CBC Co., Ltd. and Nanoform Finland Plc ("Nanoform") announced a strategic cooperation in which CBC would use its vast knowledge of the Japanese pharmaceutical sector to find opportunities for Nanoform's state-of-the-art nanomedicine engineering technology. It has been demonstrated that nano-formed medications, whether they are novel treatments or reformulated versions of existing goods, can increase patient acceptance by reducing dose size and pill load and resolving innovators' concerns about drug bioavailability.

Favorable Regulatory Support and Clinical Advancements

Supportive regulatory frameworks and ongoing clinical advancements are creating a positive nanomedicine market outlook. Regulatory bodies such as the U.S. FDA and EMA have created pathways to evaluate and approve nanotechnology-based products, fostering confidence among developers and consumers. Streamlined review processes, guidance documents, and regulatory clarity help accelerate product development and market entry. In parallel, increasing numbers of successful clinical trials for nanomedicine-based therapies validate their safety and effectiveness, building momentum in both public health and investor interest. Regulatory agencies also support post-market surveillance and quality control standards, ensuring continued patient safety. This combination of regulatory support and clinical validation enables wider adoption of nanomedicine products, reinforcing trust and facilitating broader integration into healthcare systems. For instance, in September 2024, researchers at the University of Chicago Medicine Comprehensive Cancer Center shaped a nanomedicine that efficiently destroys cancer cells in mice and improves the penetration and buildup of chemotherapy medications in tumor tissues.

Nanomedicine Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global nanomedicine market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on nanomolecule type, product, and application.

Analysis by Nanomolecule Type:

- Nanoparticles

- Metal and Metal Oxide Nanoparticles

- Liposomes

- Polymers and Polymer Drug Conjugates

- Hydrogel Nanoparticles

- Dendrimers

- Inorganic Nanoparticles

- Nanoshells

- Nanotubes

- Nanodevices

Nanoparticles stand as the largest nanomolecule type in 2025, holding 76.7% of the market due to their exceptional versatility, precision, and effectiveness in delivering therapeutic agents. Their small size allows them to penetrate biological barriers and accumulate in target tissues, particularly tumors, through enhanced permeability and retention (EPR) effects. This enables targeted drug delivery, reducing toxicity to healthy cells and improving treatment outcomes. Additionally, nanoparticles can be engineered with surface modifications to enhance the solubility, stability, and bioavailability of drugs. Their applications span a wide range of medical fields, including oncology, cardiology, infectious diseases, and neurology. With growing investments in research, continuous innovation, and increasing adoption in clinical trials, nanoparticles remain the preferred platform for developing next-generation nanomedicines across diagnostics, therapeutics, and regenerative medicine.

Analysis by Product:

- Therapeutics

- Regenerative Medicine

- In-Vitro Diagnostics

- In-Vivo Diagnostics

- Vaccines

Therapeutics leads the market with 34.7% of market share in 2025 due to their transformative role in enhancing treatment efficacy, reducing side effects, and enabling targeted drug delivery. Nanotherapeutics offer precise delivery of active pharmaceutical ingredients to specific cells or tissues, which is especially valuable in treating complex diseases such as cardiovascular disorders, cancer, and neurological conditions. This precision reduces damage to healthy cells and improves patient outcomes. Additionally, nanomedicine enables controlled and sustained drug release, increasing bioavailability and patient compliance. As chronic diseases become more prevalent globally, the demand for advanced therapeutic solutions continues to rise. Coupled with strong investment in research and development (R&D) and numerous ongoing clinical trials, the therapeutic segment remains the most commercially mature and widely adopted application within the nanomedicine market.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Clinical Oncology

- Infectious Diseases

- Clinical Cardiology

- Orthopedics

- Others

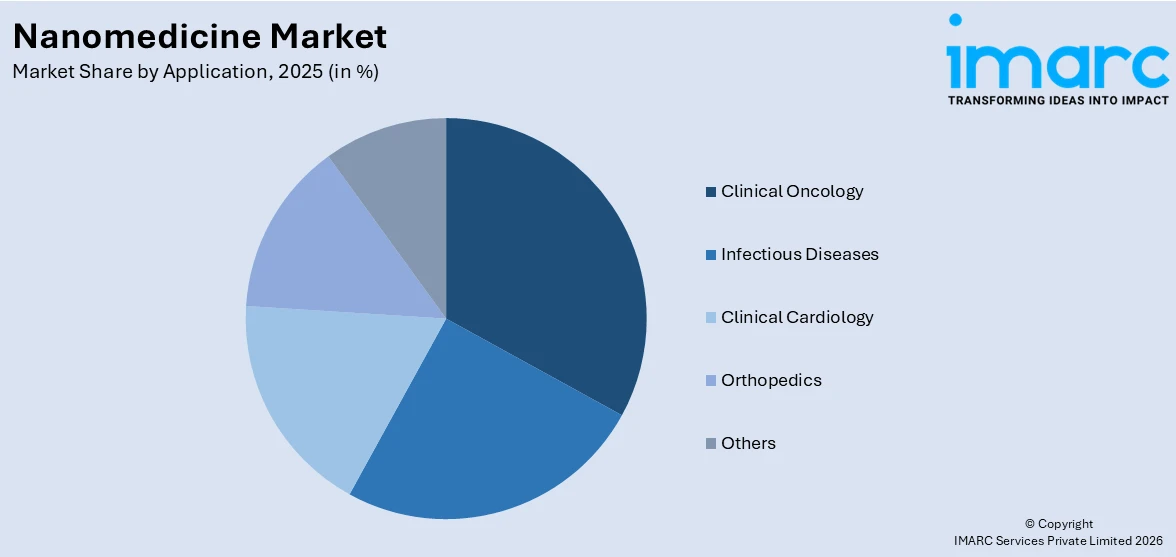

Clinical oncology leads the market with 32.5% of market share in 2025 due to the high demand for more effective and targeted cancer treatments. Nanomedicine enables the delivery of chemotherapeutic agents directly to tumor cells while minimizing exposure to healthy tissues, significantly reducing side effects and improving treatment outcomes. This precision is crucial in oncology, where conventional therapies often cause severe systemic toxicity. Additionally, nanocarriers improve drug solubility and bioavailability, and can bypass drug resistance mechanisms in tumors. The increasing global cancer burden has driven extensive research, development, and clinical adoption of nanotechnology-based therapies. With numerous nanomedicine oncology products already approved or in advanced clinical trials, this application continues to lead the market, supported by strong investment and regulatory interest in cancer innovation.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America accounted for the largest market share of 49.9%. The nanomedicine market demand in North America is influenced by a combination of advanced healthcare infrastructure, strong research capabilities, and significant investment in nanotechnology. The region benefits from a high prevalence of chronic diseases, like cardiovascular disorders and cancer, which increases demand for targeted and effective treatment options. Robust support from government agencies, including funding for nanomedicine research through institutions like the NIH, accelerates innovation and clinical translation. Additionally, the presence of leading pharmaceutical and biotechnology companies fosters the development and commercialization of nanomedicine products. Regulatory agencies like the FDA provide structured pathways for approval, encouraging product adoption. With growing awareness of precision medicine and early diagnosis, North America remains a global leader in nanomedicine research, development, and market share growth.

Key Regional Takeaways:

United States Nanomedicine Market Analysis

In 2025, the United States accounted for 92.60% of the nanomedicine market in North America. The United States nanomedicine market is mainly fueled by the increasing prevalence of chronic conditions, such as cancer and neurological disorders. According to the NCI, an estimated 2,041,910 new cancer cases and 618,120 cancer deaths are expected in the U.S. in 2025. The cancer incidence rate is 445.8 per 100,000 people annually (2018–2022), while the mortality rate is 145.4 per 100,000 people annually (2019–2023). By this, growing federal and private investment in nanotechnology R&D is accelerating innovation and commercialization in the sector. Similarly, the increasing presence of leading research institutions and academic partnerships is enabling efficient technology transfer and product development. Furthermore, continual regulatory advancements, including the FDA’s adaptive pathways for nanomedicines, are facilitating smoother clinical translation and impelling the market. Additionally, expanding applications in regenerative medicine, including stem cell nanocarriers and scaffold integration, are widening the market scope. The rising demand for precision therapies, encouraging the development of nanoparticle-based diagnostics and treatments, is strengthening the market demand. Likewise, strong industry participation in targeted delivery platforms is enhancing therapeutic efficacy and market appeal. Moreover, strategic collaborations and licensing deals are further accelerating innovation and market penetration.

Europe Nanomedicine Market Analysis

The market in Europe is experiencing growth due to rising public healthcare investment and strategic funding initiatives under Horizon Europe. According to Eurostat, in 2022, 51.3% of existing healthcare spending in the EU was funded through mandatory schemes and savings accounts, 30.0% by governmental programs, while the final 18.7% was provided by other funding sources. In line with this, expanding adoption of nanosensors in early disease detection technologies, supporting diagnostic accuracy and speed, is propelling the market growth. The region’s ongoing shift toward personalized healthcare is encouraging the uptake of targeted nanotherapies, especially in oncology and rare diseases. Furthermore, the well-regulated clinical trial environment across Europe is enabling efficient testing and approval of novel nanomedicine products. Furthermore, continual technological advances in nanoparticle design are allowing more controlled drug release, improving patient outcomes, and treatment adherence. Similarly, increasing collaboration between universities, biotech startups, and pharma firms is accelerating market expansion. The growing focus on non-invasive delivery platforms such as intranasal and transdermal nanoformulations is broadening market reach. Moreover, strong emphasis on research-driven innovation, solidifying Europe’s leadership in nanomedicine development, is creating lucrative market opportunities.

Asia Pacific Nanomedicine Market Analysis

The Asia Pacific nanomedicine market is majorly driven by rising healthcare expenditure and the increasing burden of chronic diseases across rapidly developing economies. In addition to this, government-supported nanotechnology programs in China, Japan, and South Korea are strengthening regional research infrastructure and translational capabilities, which is impelling the market. Similarly, the growing role of contract research and manufacturing organizations, enabling efficient and cost-effective development of nanomedicine solutions, is fostering market expansion. Furthermore, the rapid integration of artificial intelligence with nanotechnology for targeted drug delivery is enhancing treatment accuracy and personalization, thereby stimulating market appeal. Apart from this, the rise in medical tourism across countries such as India, Thailand, and Malaysia, generating demand for advanced, minimally invasive therapies, is providing an impetus to the market. According to data shared in the Parliament, foreign medical visitors to India reached nearly 6.6 lakh in 2023, reflecting steady post-pandemic growth.

Latin America Nanomedicine Market Analysis

In Latin America, the market is advancing due to rising government-backed initiatives focused on biotechnology and nanoscience through national development agendas. Similarly, the growth of public-private research collaborations, enhancing regional capacity for innovation and infrastructure development, is propelling the market growth. Furthermore, the increasing burden of infectious diseases is prompting healthcare systems to adopt nano-enabled diagnostics and drug delivery platforms for greater therapeutic precision. Moreover, the expansion of clinical trial networks in countries like Brazil and Argentina, supported by regulatory reforms and competitive operating costs, is attracting global investments in nanotechnology-driven healthcare solutions. According to the Regulatory Affairs Professionals Society (RAPS), as of April 2024, around 10,000 clinical studies were recorded in Brazil, positioning it as the frontrunner in clinical trials within Latin America, with Mexico trailing at approximately 5,000 and Argentina at 4,000.

Middle East and Africa Nanomedicine Market Analysis

The market in the Middle East and Africa is advancing with increased public investment in healthcare innovation, particularly through national transformation plans in countries like Saudi Arabia and the UAE. Furthermore, the rising burden of non-communicable diseases, such as cancer and diabetes, is encouraging the adoption of nanomedicine for targeted treatment and precision diagnostics. As per NCBI, the GCC countries saw an expected 42,475 new cases of cancer and 19,895 deaths in 2020; the age-standardized incidence and mortality rates were 96.5 and 52.3 per 100,000, respectively. Additionally, growing collaboration with global research institutions is enhancing regional access to cutting-edge nanotechnology and accelerating product development. Besides this, expanding interest in personalized healthcare solutions across urban medical centers supporting the integration of nanotherapeutics into mainstream treatment pathways is impacting market dynamics.

Competitive Landscape:

The nanomedicine market is highly competitive, characterized by a mix of established pharmaceutical companies, innovative biotech startups, and academic research institutions. Key players such as Pfizer, Johnson & Johnson, Abbott Laboratories, and Merck & Co. are actively investing in nanotechnology to enhance drug delivery systems and develop advanced therapies. Emerging companies like Nanoform, Nanobiotix, and Selecta Biosciences are gaining traction with specialized platforms for targeted treatment. Collaborations, licensing agreements, and strategic partnerships are common as firms seek to expand their technological capabilities and market reach. Continuous innovation, strong R&D pipelines, and a focus on oncology and chronic disease treatment are central to competitive positioning. Regulatory approvals and clinical trial progress play critical roles in shaping market leadership and driving commercial success.

The report provides a comprehensive analysis of the competitive landscape in the nanomedicine market with detailed profiles of all major companies, including:

- Abbott Laboratories

- Arrowhead Pharmaceuticals Inc.

- General Electric Company

- Luminex Corporation

- Merck & Co. Inc.

- Nanobiotix

- Novartis AG

- Pfizer Inc.

- Sanofi SA

- Starpharma Holdings Limited

Latest News and Developments:

- April 2025: Marama Labs launched CloudSpec, an instrument that dramatically accelerated the quantification of drug payloads in lipid nanoparticles (LNPs). Utilizing patented Scatter-Free Absorption (SFA) technology, CloudSpec delivers precise RNA or DNA measurements in just 15 seconds, eliminating the need for particle disruption or fluorescent dyes. This innovation addresses a critical bottleneck in developing gene therapies, vaccines, and cancer treatments, potentially transforming LNP-based drug development in nanomedicine applications.

- February 2025: Ardena acquired Catalent’s 50,000-square-feet Somerset drug product facility, expanding into North America and enhancing oral drug manufacturing and bioanalytical services. The site complements Ardena’s nanomedicine capabilities, integrating advanced drug formulation, cGMP production, and bioanalysis to support global clinical programs and complex molecule development.

- November 2024: Flashpoint Therapeutics partnered with KAIMRC in a USD 50 million deal to establish a Center of Excellence for Structural Nanomedicine in Saudi Arabia. The collaboration supports clinical trials and drug discovery, expanding Flashpoint’s nanomedicine pipeline, including FLASH-001 for cancer and novel therapies using nucleic acid and CRISPR technologies.

- November 2024: EVŌQ Nano expanded its antimicrobial medical device platform using EVQ-218, a novel non-ionic silver nanoparticle with a unique sulfur-sequestration mechanism. Demonstrating >99.99% efficacy against pathogens, EVQ-218 integrates across manufacturing stages without altering device properties, advancing nanomedicine applications in infection control and implantable medical device performance.

- September 2024: Cytiva launched an advanced RNA delivery LNP kit for NanoAssemblr Ignite systems. The kit enables rapid mRNA and saRNA vaccine development with ready-to-use ionizable lipids, GMP-compatible components, and proven scalability, supporting researchers from discovery to clinical evaluation in infectious disease applications.

Nanomedicine Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Nanomolecule Types Covered |

|

| Products Covered | Therapeutics, Regenerative Medicine, In-Vitro Diagnostics, In-Vivo Diagnostics, Vaccines |

| Applications Covered | Clinical Oncology, Infectious Diseases, Clinical Cardiology, Orthopedics, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Abbott Laboratories, Arrowhead Pharmaceuticals Inc., General Electric Company, Luminex Corporation, Merck & Co. Inc., Nanobiotix, Novartis AG, Pfizer Inc., Sanofi SA and Starpharma Holdings Limited |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the nanomedicine market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global nanomedicine market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the nanomedicine industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Nanomedicine Market Report

The nanomedicine market was valued at USD 326.0 Billion in 2025.

The nanomedicine market is projected to exhibit a CAGR of 10.43% during 2026-2034, reaching a value of USD 817.5 Billion by 2034.

Key factors driving the nanomedicine market include advancements in nanotechnology, rising prevalence of chronic diseases, increasing demand for targeted drug delivery, and growing investment in research and development. Supportive regulatory frameworks and expanding clinical applications also contribute to the market’s growth, especially in oncology, cardiovascular, and neurological treatments.

North America currently dominates the nanomedicine market due to advanced healthcare infrastructure, strong research and development (R&D) investment, high chronic disease burden, regulatory support, and leading pharmaceutical companies.

Some of the major players in the nanomedicine market include Abbott Laboratories, Arrowhead Pharmaceuticals Inc., General Electric Company, Luminex Corporation, Merck & Co. Inc., Nanobiotix, Novartis AG, Pfizer Inc., Sanofi SA, Starpharma Holdings Limited, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)