Native Starch Market Size, Share, Trends and Forecast by End Use, Feedstock, and Region, 2026-2034

Native Starch Market Size, Share, Trends & Forecast (2026-2034)

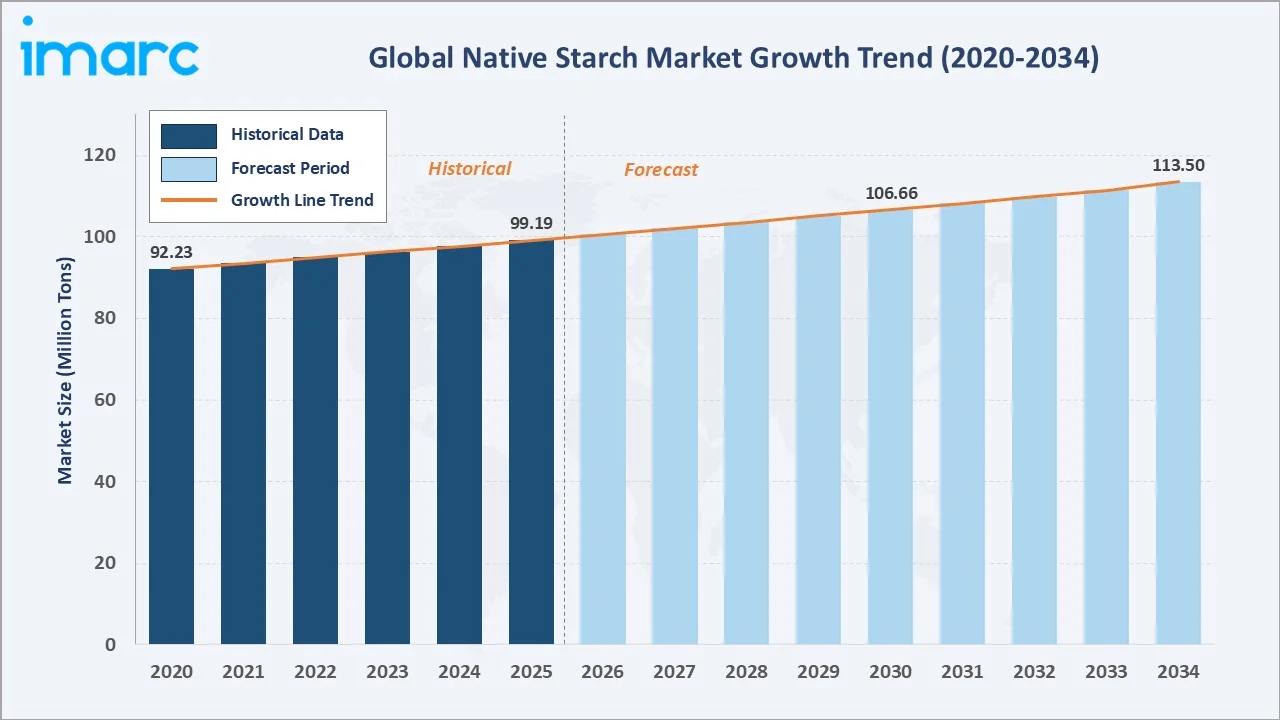

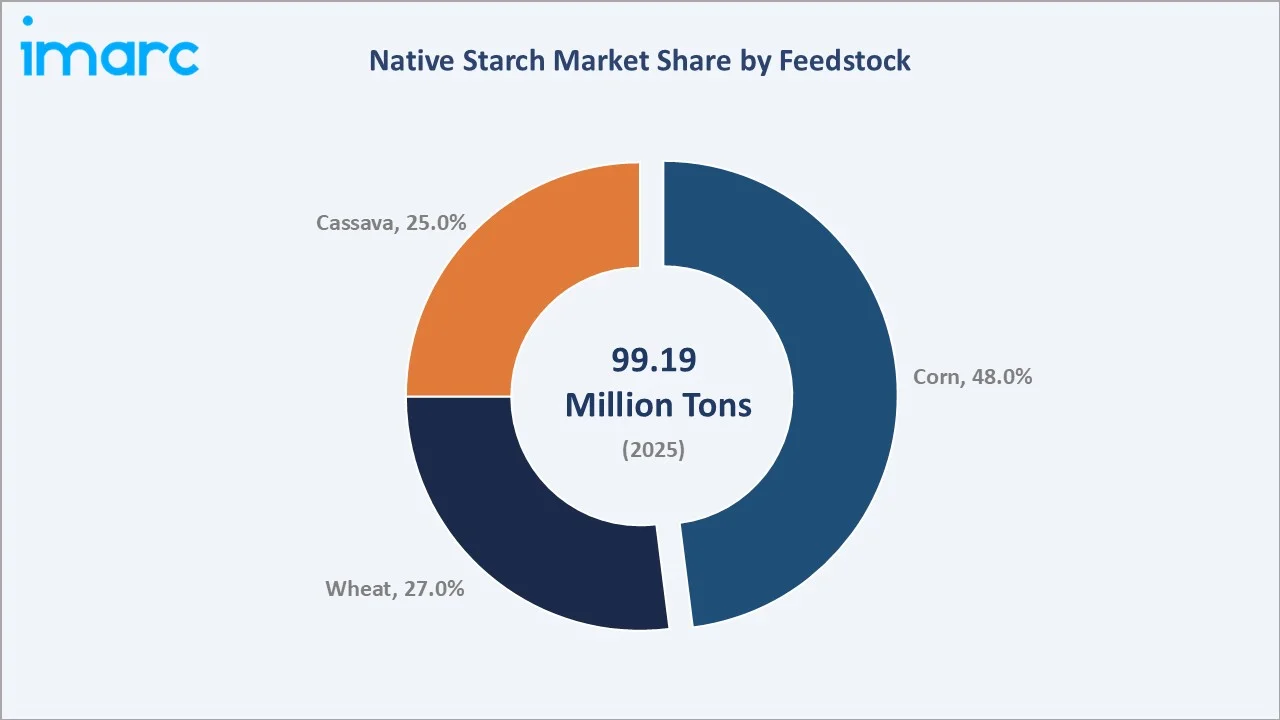

The global native starch market reached 99.19 Million Tons in 2025 and is projected to reach 113.50 Million Tons by 2034, growing at a CAGR of 1.46% during 2026-2034. Steady demand from the food processing, sweetener, ethanol, and paper industries, sustained feedstock availability from corn, wheat, and cassava crops, and the growing clean-label ingredient trend favoring native over chemically modified starches are the primary forces sustaining consistent volumetric growth throughout the forecast period.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

99.19 Million Tons |

|

Forecast Market Size (2034) |

113.50 Million Tons |

|

CAGR (2026-2034) |

1.46% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

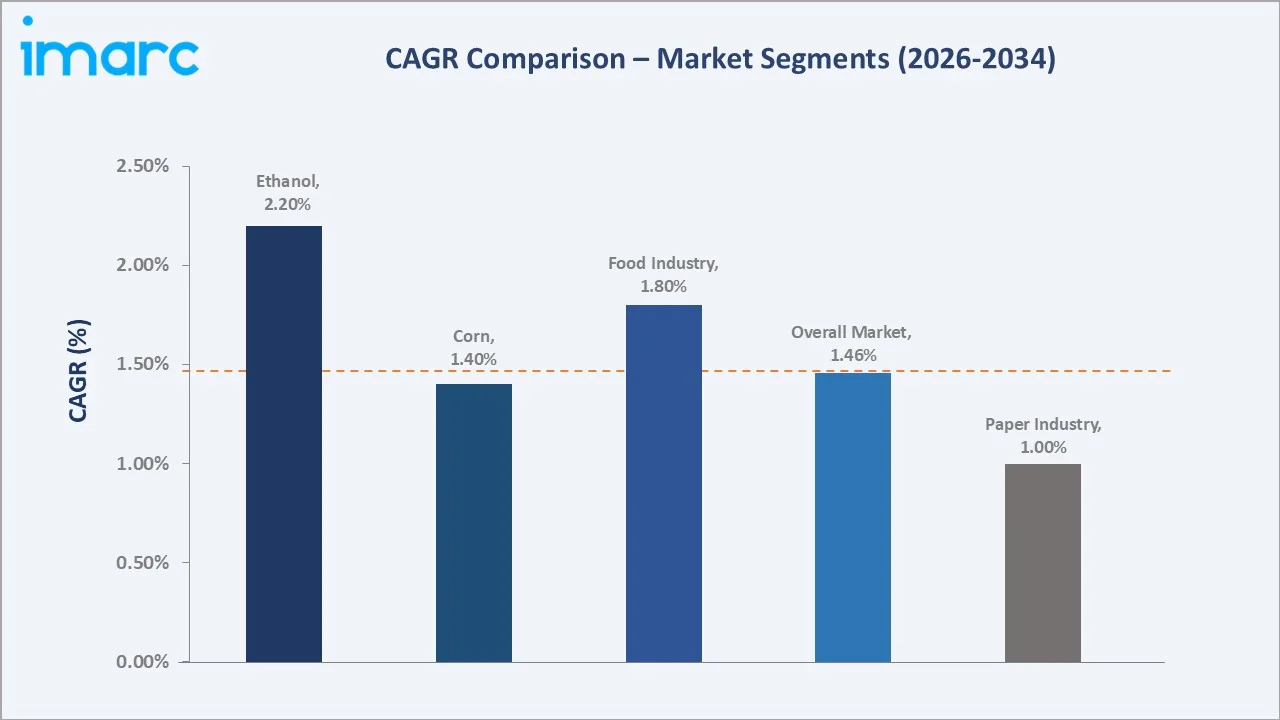

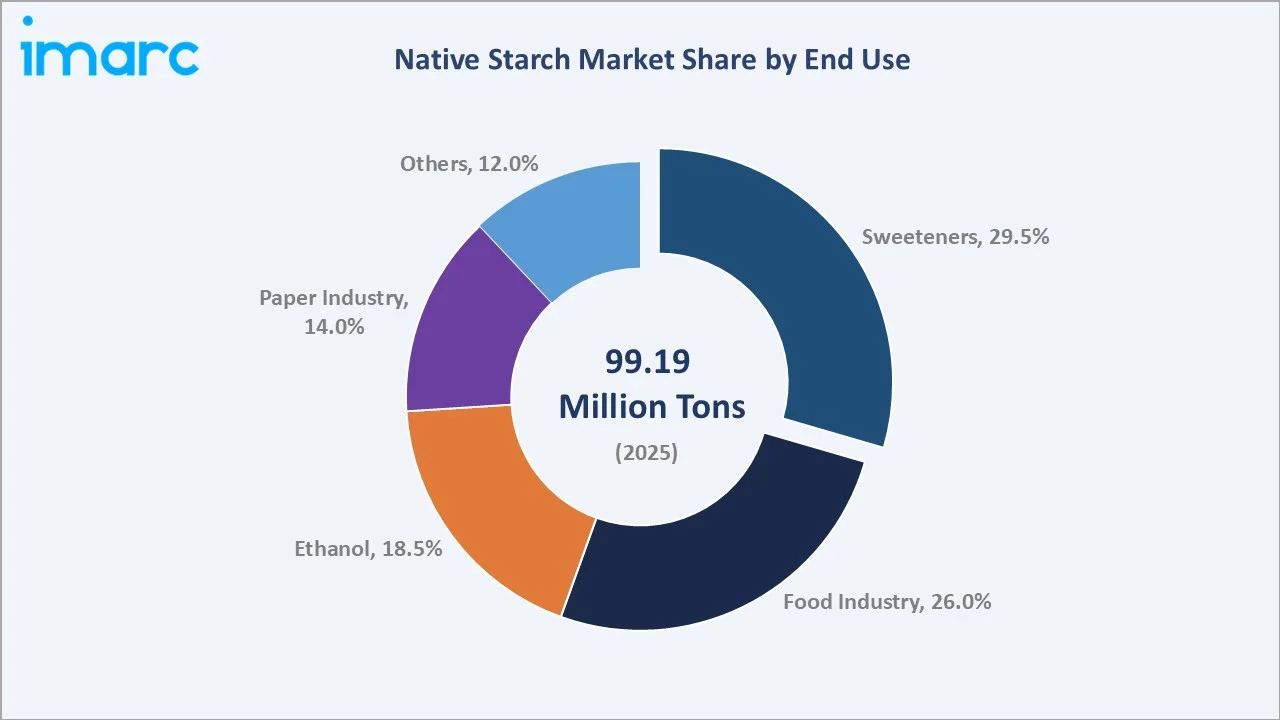

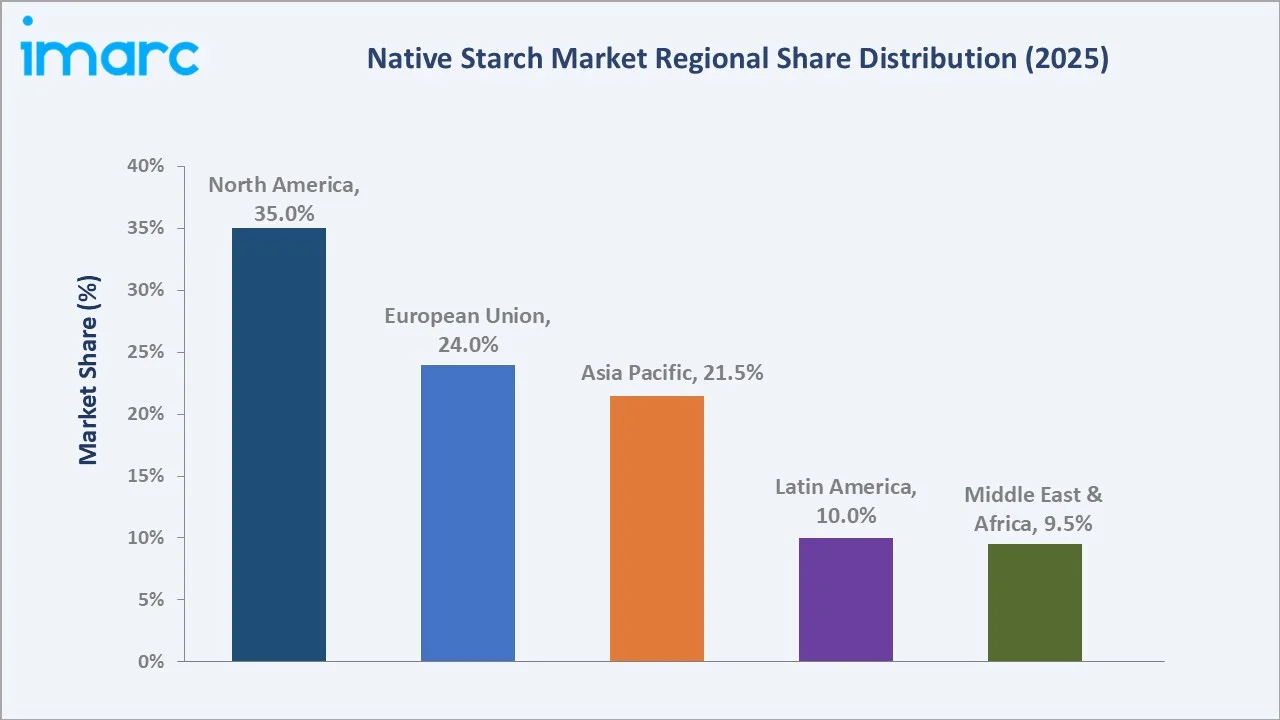

North America leads regionally with a 35.0% market share in 2025, anchored by the US Corn Belt's integrated wet milling infrastructure. Sweeteners command the largest end use share at 29.5%, while corn dominates the feedstock segment at 48.0%. Ethanol is the fastest-growing end use at ~2.2% CAGR, driven by US, Brazilian, and EU biofuel mandates expanding starch-to-ethanol fermentation demand.

To get more information on this market, Request Sample

The global native starch market grew from 92.23 Million Tons in 2020 to 99.19 Million Tons in 2025, an increase of 6.96 Million Tons over five years, driven by consistent underlying demand from food processing and sweetener industries. The market is forecast to reach 113.50 Million Tons by 2034, reflecting the crop-linked and relatively inelastic demand profile that characterizes the native starch industry, a mature, volume-stable commodity with growth driven primarily by population increases, emerging market food processing expansion, and biofuel policy mandates.

Executive Summary

The global native starch market is expanding at a steady 1.46% CAGR, reflecting its mature commodity profile with demand growth closely tied to global food production, biofuel policy mandates, and industrial applications. The market accounted for 99.19 Million Tons in 2025 and is forecast to reach 113.50 Million Tons by 2034.

Sweeteners dominate end use at 29.5% in 2025, as high-fructose corn syrup (HFCS) and glucose syrup production from corn and wheat starch sustains North America's and Europe's large-scale sweetener manufacturing base. Food industry applications at 26.0% reflect native starch's essential role as a thickener, binder, and texture modifier in soups, sauces, bakery, and dairy products.

Corn dominates feedstock at 48.0%, supported by the world's most efficient wet milling infrastructure in the US Corn Belt. Wheat at 27.0% serves Europe's food-grade starch market, while cassava at 25.0% is growing in the Asia Pacific and Africa.

Key Market Insights

|

Insight |

Data |

|

Largest End Use |

Sweeteners – 29.5% share (2025) |

|

Fastest Growing End Use |

Ethanol – ~2.2% CAGR (2026-2034) |

|

Largest Feedstock |

Corn – 48.0% share (2025) |

|

Fastest Growing Feedstock |

Cassava – ~1.8% CAGR (2026–2034) |

|

Leading Region |

North America – 35.0% share (2025) |

|

Top Companies |

Cargill, Incorporated, Ingredion Incorporated, Archer Daniels Midland Company, and Roquette Frères |

Key Analytical Observations Supporting The Above Data:

- Sweeteners at 29.5% (2025) reflect native starch's primary industrial conversion pathway, corn starch hydrolysis to glucose syrups, and HFCS underpins the North American sweetener industry, while wheat starch hydrolysis produces maltose and glucose syrups in Europe.

- Corn at 48.0% (2025) dominates feedstocks because of the US wet milling industry's unmatched scale and efficiency. Multiple organizations in the market operate wet milling facilities with individual plant capacities exceeding 1 Million Tons of starch per year.

- North America at 35.0% (2025) reflects the US's position as the world's largest corn starch producer and consumer, anchored by Iowa, Nebraska, and Illinois corn wet milling complexes that supply sweetener, ethanol, and food ingredient industries simultaneously from integrated multi-product facilities.

- Ethanol at ~2.2% CAGR is the fastest-growing end use, driven by US ethanol blending mandates capped at 15 Billion gallons annually under RFS2, Brazil's anhydrous ethanol blend mandate of 30%, and EU RED III's 2.6% advanced biofuel sub-mandate. Corn and wheat starch remain the primary feedstocks for grain-based ethanol across these mandated volumes.

Native Starch Market Overview

Native starch, unmodified starch extracted directly from agricultural feedstocks, is a fundamental food and industrial ingredient produced by the wet milling of corn, wheat, cassava, potato, and other starch-rich crops. The native starch industry is vertically integrated, with leading processors operating from grain origination through finished starch, glucose syrup, and co-product (gluten, germ oil, feed) manufacturing at single-site multi-product complexes.

The native starch industry's value chain is characterized by high capital intensity, scale-dependent economics, and geographic concentration near primary feedstock production areas. US corn wet milling facilities represent USD 15+ Billion in collective replacement asset value. European wheat starch facilities in France, Germany, and the Netherlands benefit from EU agricultural policy price support and proximity to the continent's food-processing industrial base.

Market Dynamics

To evaluate market opportunities, Request Sample

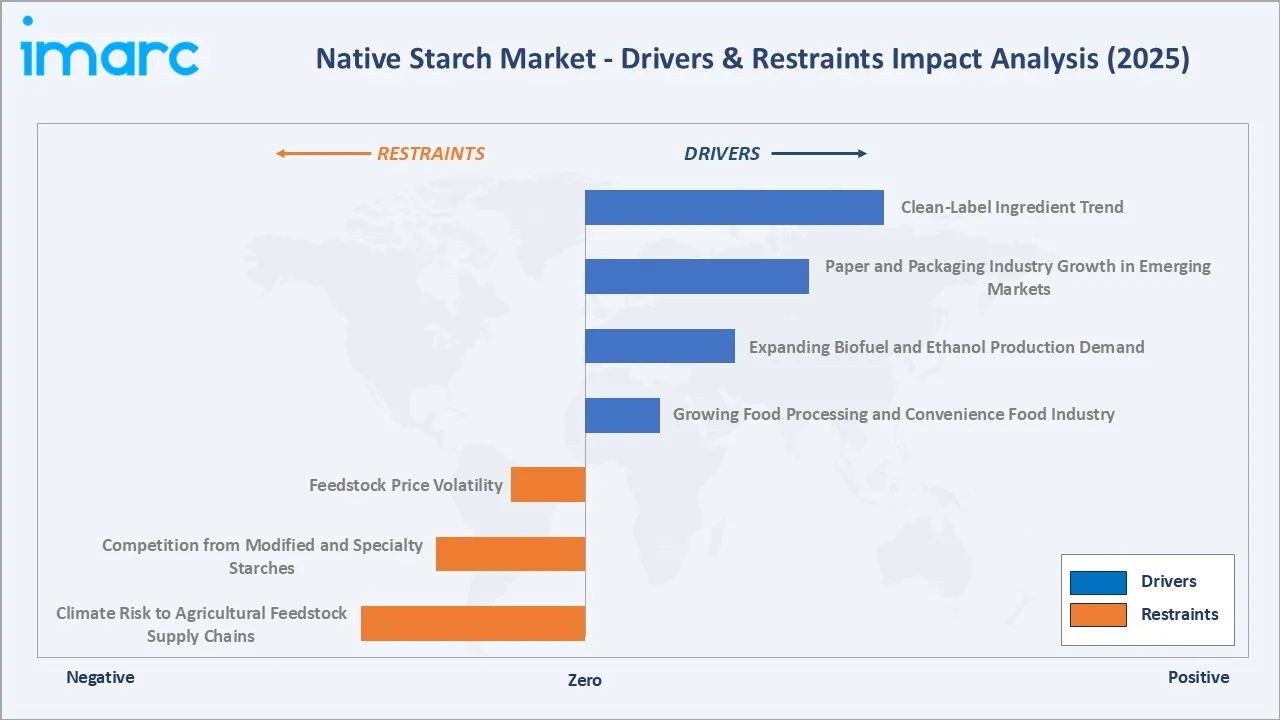

Market Drivers

- Growing Food Processing and Convenience Food Industry: Global processed food output grew at approximately 4.2% CAGR between 2020 and 2025, with starch serving as an essential functional ingredient in soups, sauces, bakery products, dairy desserts, and ready meals.

- Expanding Biofuel and Ethanol Production Demand: In March 2026, U.S. ethanol producers used 474 million bushels of corn, representing an increase compared with March 2025, according to the USDA’s May Grain Crushings and Co-Products Production report.

- Paper and Packaging Industry Growth in Emerging Markets: E-commerce packaging demand grew at 15%+ CAGR globally in 2022–2025, driving corrugated board production and starch adhesive consumption. Native starch is the primary coating and sizing agent for paper and paperboard.

- Clean-Label Ingredient Trend in Food Formulation: Consumer preference for food products with recognizable, non-chemical ingredients is driving food manufacturers to replace modified starch with native starch in clean-label reformulations.

Market Restraints

- Feedstock Price Volatility: Global corn prices declined by over 20% from the start of 2025 to their summer lows. Prices later recovered gradually, supported by supply shortages in Europe and strong U.S. exports. However, at the start of 2026, the corn prices came under pressure again amid favorable weather conditions in South America and an upward revision to U.S. production in the January World Agricultural Supply and Demand Estimates report.

- Competition from Modified and Specialty Starches: Modified starches offer superior functional performance that native starches cannot match. Specialty starch companies are cannibalizing native starch volume in high-value food applications by offering functional systems that reduce total ingredient usage per unit of food produced.

- Climate Risk to Agricultural Feedstock Supply Chains: Extreme weather events, the 2022 US Midwest drought, the 2023 European heat wave affecting French wheat yields, and Thailand’s drought reducing cassava production demonstrate the physical climate risk to native starch production volumes.

Market Opportunities

- Bio-Based Packaging and Biodegradable Plastics: Native starch is a primary feedstock for biodegradable and compostable packaging films, loose-fill packaging peanuts, and food service items. The global starch-based bioplastics market is projected to reach USD 4.0 Billion by 2034, growing at 7.43% CAGR from 2026 to 2034.

- Cassava Starch Expansion in Asia Pacific and Africa: World Bank and African Development Bank programs to build cassava wet milling infrastructure in Nigeria, Ghana, and Mozambique represent a multi-decade feedstock diversification opportunity that could add 5–8 Million Tons of African cassava starch capacity by 2035.

Market Challenges

- Margin Compression from Commodity Price Cycles and Energy Costs: Native starch wet milling is energy-intensive; electricity, steam, and natural gas represent 18–25% of total production costs. European energy cost fluctuations directly impact compressed wheat starch margins by 15–20%.

- Regulatory Complexity in Food Safety and Sustainability Compliance: FSSAI (India), FDA (US), EFSA (EU), and national food safety authorities maintain distinct specifications for food-grade native starch moisture, ash, sulfur dioxide content, and microbiological limits.

Emerging Market Trends

1. Clean-Label and Organic Native Starch Premiumization

In February 2024, Ingredion Incorporated introduced NOVATION Indulge 2940, the first non‑GMO, functional native, clean‑label corn starch that delivers improved gelling, texture, and mouthfeel for dairy, alternative dairy, and dessert products. Organic native starch commands a 35–60% price premium over conventional native starch, with demand growing at 6.5% CAGR as food manufacturers reformulate to meet organic certification requirements.

2. Cassava Starch Integration into Asian and African Supply Chains

In 2025, Thailand’s cassava sector performed strongly, exporting more than 8 million tons of cassava products valued at over THB 95 billion, marking a 26% year-on-year increase. This is driven by growing demand from Chinese paper mills and Southeast Asian food processors. In April 2026, a new US $20 million cassava processing plant broke ground in Kampong Speu province, Cambodia, aiming to boost domestic value‑added production and support farmers and export growth.

3. AI and Precision Agriculture Optimization for Feedstock Quality

In January 2023, the U.S. Department of Energy’s Idaho National Laboratory developed Crop AIQ, an AI‑driven yield‑mapping tool that uses publicly available satellite imagery to generate high‑resolution crop yield maps at the subfield level, enabling farmers to forecast expected yields and adjust management practices for precision input use.

Industry Value Chain Analysis

The global native starch value chain operates through vertically integrated wet milling complexes that process agricultural feedstocks into a portfolio of starch, sweetener, protein, fiber, and oil co-products, maximizing the economic value extracted per unit of feedstock through multi-product facility design.

|

Stage |

Key Players / Examples |

|

Feedstock Sourcing |

Corn, wheat, and cassava farmers; agricultural commodity traders; cooperative grain elevators; contract farming operators |

|

Wet Milling & Extraction |

Large-scale wet milling facilities; starch separation centrifuges; gluten and germ extraction co-product streams |

|

Purification & Drying |

Hydrocyclone washing systems; vacuum belt filters; flash dryers and rotary kilns producing dry native starch powder |

|

Quality Testing & Grading |

In-house food safety laboratories; third-party testing for moisture, ash, pH, viscosity, and microbial compliance certifications |

|

Packaging & Storage |

Bulk tanker trucks, multi-wall bags, big bags; temperature-controlled warehouses and silos at port and inland distribution hubs |

|

Distribution & End Use |

Food processors, sweetener manufacturers, paper mills, and ethanol producers; commodity traders for spot and forward contract procurement |

Technology Landscape in the Native Starch Industry

Wet Milling Process Technology and Efficiency Innovation

Modern corn wet milling facilities achieve starch extraction yields of 64–67% of corn dry weight, versus 60–62% for facilities built before 2000. Continuous steeping technology, high-pressure counter-current washing systems, and automated centrifuge cascade control have reduced energy consumption per ton of starch produced by 18% over the 2015–2025 period.

Enzymatic Modification and Native Starch Functionality Enhancement

Leading processors are commercializing enzymatic treatments that modify native starch functionality without chemical reagents, achieving clean-label functionalization at process costs 30–40% below traditional chemical modification. These 'enzyme-converted' native starches maintain regulatory classification as 'native' or 'natural' starch in major food regulatory frameworks while delivering freeze-thaw stability equivalent to modified starch.

Sustainability and Water Conservation Technology

Corn wet milling is water-intensive; traditional processes consume 4–6 liters of water per kilogram of starch produced. This has encouraged native starch manufacturers to adopt water recycling, closed-loop processing, and advanced filtration systems to reduce freshwater consumption. Growing focus on sustainability and resource efficiency is further driving investment in water conservation technologies across starch processing facilities.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

End Use |

Sweeteners |

29.5% |

2025 |

|

Feedstock |

Corn |

48.0% |

2025 |

|

Region |

North America |

35.0% |

2025 |

By End Use

Sweeteners dominate at 29.5% in 2025. Native starch hydrolysis is the foundation of the global sweetener industry. Corn starch-derived HFCS commands approximately 45% of US caloric sweetener consumption. Food industry applications at 26.0% encompass native starch's role as a thickener, binder, film former, and encapsulant in processed foods.

To access detailed market analysis, Request Sample

Ethanol at 18.5% is growing fastest at ~2.2% CAGR, as US corn ethanol production of 15 Billion gallons requires roughly 5.4 billion bushels of corn, weighing about 150 million tons. The paper industry at 14.0% uses native starch as a surface sizing and coating agent, with the global paper industry consuming 8–10 Million Tons of starch annually.

By Feedstock

Corn leads at 48.0% in 2025. The US accounts for 33% of global production, with a total output of approximately 432.34 million metric tons in 2025/2026, and 10–12% directed to wet milling for starch production. Corn's high starch yield, established infrastructure, and multi-product co-processing economics sustain its feedstock leadership.

Wheat at 27.0% is primary in European starch production, with France producing approximately 1.5 Million Tons of wheat starch annually. Cassava at 25.0% (2025) is grown in tropical regions of Thailand, Vietnam, Nigeria, Brazil, and India, with Thailand producing 28-31 million tons of cassava across 8-9 million hectares annually.

Regional Market Insights

North America's market leadership (35.0%, 2025) reflects the U.S. corn's notably higher starch yields, ranging from 68% to 70%, compared with 64% to 66% in South American corn. The US's integrated corn processing complex in Iowa, Illinois, Nebraska, and Indiana represents the world's most concentrated and efficient native starch production cluster.

The European Union at 24.0% (2025) is characterized by wheat starch dominance and strong sustainable sourcing mandates. Asia Pacific at 21.5% is the fastest-growing region at ~2.0% CAGR, driven by China's corn wet milling expansion and Southeast Asia's cassava processing scale-up.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

35.0% |

US ethanol mandate driving corn starch demand; HFCS sweetener production at scale; strong paper and paperboard industry in Canada and the Southeast US |

|

European Union |

24.0% |

Wheat starch dominance from France, Germany, and the Netherlands; EU biofuel directive sustaining starch-to-ethanol demand; food-grade wheat starch for the baking and pasta industry |

|

Asia Pacific |

21.5% |

Thailand and Vietnam leading cassava starch production and export; China's large-scale corn wet milling expansion; India's growing food processing industry driving starch demand |

|

Latin America |

10.0% |

Brazil's corn starch expansion alongside soy and sugar agribusiness; growing domestic food processing and bakery industry; cassava starch production for regional food markets |

|

Middle East & Africa |

9.5% |

Nigeria and Ghana's cassava starch development as an import substitution strategy; GCC food manufacturing growth driving starch imports; Egypt's corn wet milling industry serving MENA food processors |

Competitive Landscape

The global native starch market is moderately concentrated, with the top producers controlling approximately 60–70% of global organized wet milling capacity. The remaining 30–40% of production is fragmented across hundreds of national and regional processors, particularly in the cassava starch sector of Southeast Asia and Sub-Saharan Africa.

|

Company Name |

Brands/Products |

Market Position |

Core Strength |

|

|

AmyloGel, CreamGel, DryGel, Gel, C*Gel |

Market Leader |

World's largest agricultural commodity processor; vertically integrated from grain to end-use; strong industrial and food starch portfolio |

|

|

NOVATION |

Market Leader |

Broadest global starch ingredient portfolio; leading food texture and stabilization expertise |

|

|

Texperien True |

Strong Challenger |

Largest US grain handler; integrated starch, sweetener, and ethanol production; global origination and logistics |

|

|

CLEARGUM, PREGEFLO, TACKIDEX |

Challenger |

Vertically integrated from grain to specialty ingredients; pioneering plant-based protein from starch co-products |

Key Company Profiles

Cargill, Incorporated

Cargill, Incorporated, is one of the world's largest privately held food and agricultural companies and the leading global native starch producer.

- Product Portfolio: AmyloGel, CreamGel, DryGel, Gel, C*Gel, native corn starch for food and industrial applications, corn gluten meal, germ oil, and corn ethanol.

- Recent Developments: In March 2025, Cargill, Incorporated, inaugurated a new corn milling plant in Gwalior, Madhya Pradesh, India, in a business arrangement with Saatvik Agro Processors to produce starch derivatives and meet rising domestic demand. The facility has an initial capacity of 500 tons per day (expandable to 1,000) and aims to strengthen local supply while potentially supporting future exports.

- Strategic Focus: Sustainability-linked procurement; closed-loop water recirculation facility; expansion of specialty and clean-label starch derivatives for the premium food ingredient market.

Ingredion Incorporated

Ingredion Incorporated is a global ingredient solutions company with a comprehensive starch portfolio spanning native corn, wheat, tapioca, and potato starches, alongside a leading specialty and modified starch range.

- Product Portfolio: NOVATION functional native starch range.

- Recent Developments: In February 2024, Ingredion Incorporated launched NOVATION Indulge 2940, the first functional native clean‑label corn starch designed to provide better texture, gel strength, and mouthfeel in food applications without chemical modification.

- Strategic Focus: Specialty and functional native starch premiumization; NOVATION organic starch range scaling; tapioca and specialty starch sourcing diversification in Southeast Asia.

Market Concentration Analysis

The native starch market exhibits moderate-to-high concentration in the corn starch segment and low concentration in the cassava starch segment. The market consolidation has slowed since 2015, as the capital intensity of greenfield wet milling development limits organic expansion. Future consolidation is more likely to go through targeted acquisitions of cassava processors in Southeast Asia and Africa, seeking to diversify feedstock risk and capture the Asia Pacific market growth.

Investment & Growth Opportunities

Fastest Growing Segments

Ethanol (~2.2% CAGR), food industry (~1.8% CAGR), and bio-based packaging starch (~8% CAGR from a low base) represent the primary growth vectors through 2034. Bioplastics and starch-based biodegradable materials represent the highest value-add growth opportunity, where starch converted to bioplastic films commands USD 1,500–3,500/ton versus USD 280–420/ton for commodity native starch, creating a USD 15+ per ton margin uplift for integrated processors.

Emerging Market Expansion

Asia Pacific's 21.5% regional share has the highest absolute growth potential, with India's cassava starch industry in Tamil Nadu and Gujarat scaling for export and Thailand and Vietnam targeting 15 Million Tons of combined cassava starch capacity by 2030. These expansions will shift the global production center of gravity from North America-Europe toward the Asia Pacific by 2032.

Investment and Capacity Trend

- In May 2026, Sanstar commissioned its expanded native starch manufacturing capacity at its Dhule, Maharashtra facility in India, boosting total installed capacity from 1,100 TPD to 2,350 TPD as part of its growth plan funded by IPO proceeds. This expansion positions the company to better serve rising domestic and international demand in maize‑based specialty products.

Future Market Outlook (2026-2034)

The global native starch market will expand from 99.19 Million Tons in 2025 to 113.50 Million Tons by 2034 at a 1.46% CAGR. North America will retain volume leadership through the forecast period, but Asia Pacific's share will increase from 21.5% to approximately 26% by 2034 as China and India expand wet milling capacity. Ethanol will be the fastest-growing end use, while sweeteners will remain the largest application by volume.

By 2034, the native starch industry will face three structural transitions: feedstock diversification away from corn monoculture risk through cassava and sorghum starch development, bio-based materials creating a premium-priced growth lane for starch that offsets commodity price pressure, and AI-driven crop monitoring and precision fermentation technologies improving yield efficiency by 5–10% above 2025 baselines, effectively unlocking additional output from existing feedstock areas.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 75 industry participants in 2024–2025, including wet milling process engineers, commodity traders, food ingredient buyers, sustainability managers, and agricultural economists across the US, France, Germany, Thailand, and Brazil.

Secondary Research

Secondary research covered FAO crop production and trade statistics, USDA ERS starch and sweetener databases, European Commission agricultural commodity market reports, Thai Tapioca Trade Association export statistics, Starch Europe industry data, and company annual reports for all market participants.

Forecasting Models

Volume estimations used bottom-up feedstock crop production forecasting, incorporating yield trend analysis, wet milling capacity utilization rates, co-product economics, and end-use demand sector growth projections. A CAGR of 1.46% reflects consensus cross-validated against FAO Agricultural Outlook 2024–2033 and IMARC's primary expert panel validation.

Native Starch Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons, Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| End Uses Covered | Sweeteners, Ethanol, Food Industry, Paper Industry, Others |

| Feedstocks Covered | Corn, Wheat, Cassava |

| Regions Covered | Production: United States, European Union, China, Others Consumption: North America, European Union, Asia Pacific, Latin America, Middle East and Africa |

| Companies Covered | Cargill Incorporated, Ingredion Incorporated, Archer Daniels Midland Company, Roquette Frères, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the native starch market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global native starch market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the native starch industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Native Starch Market Report

The market reached 99.19 Million Tons in 2025 and is forecast to reach 113.50 Million Tons by 2034 at a 1.46% CAGR.

Sweeteners lead at 29.5% in 2025, as corn and wheat starch hydrolysis into glucose syrups, HFCS, and dextrose underpins the global sweetener manufacturing industry.

Corn dominates at 48.0% in 2025, driven by the US Corn Belt's unmatched wet milling infrastructure and corn's superior starch yield (65–70% of kernel dry weight) and multi-product co-processing economics.

North America leads at 35.0% in 2025, anchored by the US corn wet milling complex in Iowa, Illinois, Nebraska, and Indiana, the world's most concentrated and efficient native starch production cluster.

Some of the key players in the market include Cargill, Incorporated, Ingredion Incorporated, Archer Daniels Midland Company, and Roquette Frères.

Ethanol is the fastest-growing end use at ~2.2% CAGR, driven by US RFS2 corn ethanol mandates, Brazil's RenovaBio blending targets, and EU RED III biofuel requirements through 2030.

Growing food processing industry demand, expanding biofuel ethanol mandates, paper and packaging industry growth in emerging markets, and the clean-label ingredient trend favoring native starch in food reformulation are the primary drivers.

Feedstock price volatility (corn, wheat, cassava), competition from modified and specialty starches in high-value food applications, climate risk to agricultural feedstock supply chains, energy cost pressure on wet milling economics, and regulatory complexity across 80+ national food safety frameworks.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade