Nitro Cellulose Price Update: Sustained Growth Across Key Markets in Q1 2026

31-Oct-2025

Nitro cellulose is a flammable compound. Made by nitrating purified cotton linters with mixed nitric and sulfuric acids, the polymer varies by nitrogen content, which in turn governs its solubility, viscosity, and film-forming behavior. Across paints, wood coatings, printing inks, nail lacquers, and propellants, nitro cellulose prices respond to where that downstream demand sits. On the cost side, the levers are simpler: cotton linter feedstock, nitration energy, ocean freight, and coatings demand.

Global Market Overview:

Globally, the nitro cellulose industry was valued at USD 944.89 Million in 2025. Market projections indicate steady growth, with the industry expected to reach USD 1,373.27 Million by 2034, with a compound annual growth rate (CAGR) of 4.24% during 2026-2034. Coatings and inks anchor the base load. Where high-solids, fast-drying formulations dominate, the nitro cellulose price trend keeps firming, and newer specialty-manufacturing uses slowly widen the customer pool.

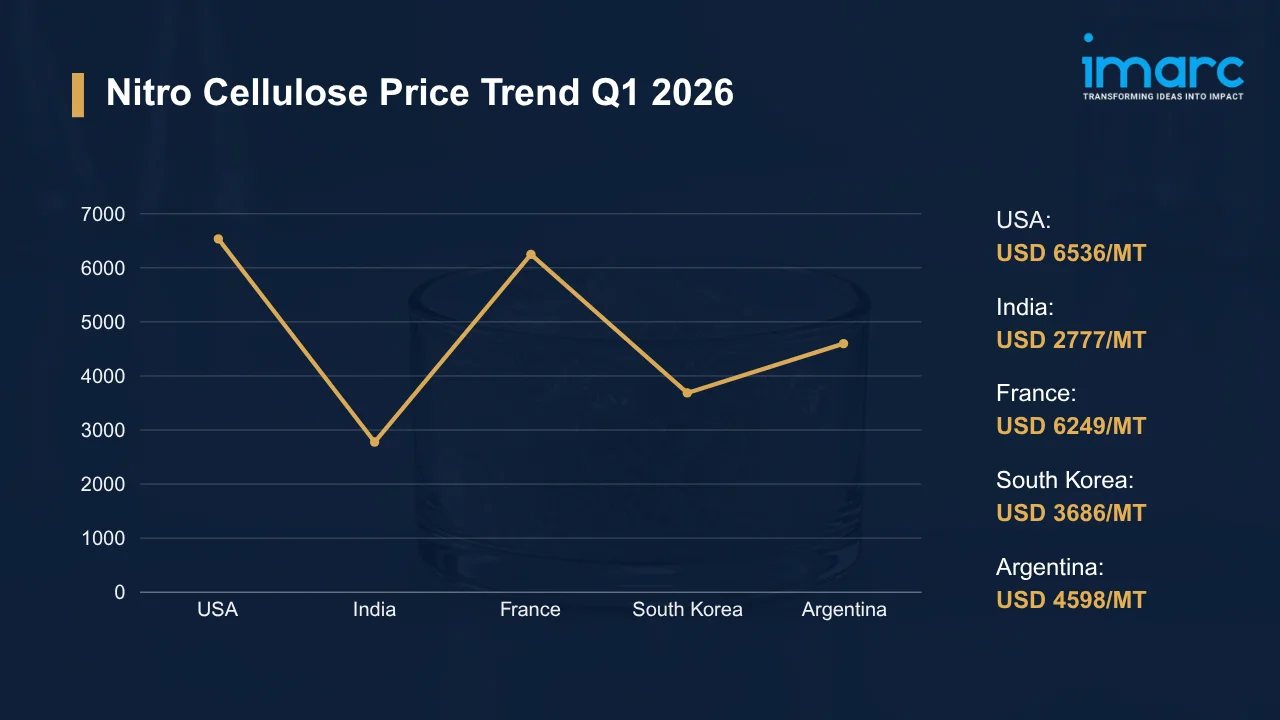

Nitro Cellulose Price Trend Q1 2026:

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| USA | 6,536 | +1.89% | ↑ |

| India | 2,777 | -0.85% | ↓ |

| France | 6,249 | +2.12% | ↑ |

| South Korea | 3,686 | +3.34% | ↑ |

| Argentina | 4,598 | +4.46% | ↑ |

To access real-time prices Request Sample

What Moved Prices:

USA:

- In Q1 2026, nitro cellulose prices in the USA climbed to USD 6,536/MT, up 1.89% QoQ. Refinish, wood-coating, and ink producers stocked up ahead of peak season. Feedstock stayed tight throughout the period. Weather-pressured cotton-linter yields across the southern states kept converters competing for purified grades, and that scramble for feedstock reinforced the upward push right through the quarter.

- Gulf Coast and Midwest corridors saw inland freight and storage fees rise, lifting delivered costs at conversion units even as better rail availability steadied outbound flow. It did not offset the cost climb. The nitro cellulose price chart traced a firm upward path across consuming sectors.

India:

- During Q1 2026, nitro cellulose prices in India eased to USD 2,777/MT, down 0.85% QoQ. Coating, ink, and adhesive makers trimmed restocking once the post-monsoon industrial push faded, and steady domestic output left the main coatings and printing clusters comfortably covered. Spot sentiment across hubs stayed soft. Competitively priced Chinese-origin material added to the slack.

- Port-served manufacturing zones reported lighter printing-ink offtake, which weighed on spot pricing. Lower internal trucking costs trimmed landed values. Distributors ran lean inventories, cautious about soft near-term construction-linked coatings demand, while low-cost imports from China kept capping any meaningful move higher in assessed values.

France:

- In the first quarter of 2026, nitro cellulose prices in France advanced to USD 6,249/MT, up 2.12% QoQ. Specialty-coatings and auto-refinish demand clearly firmed. Slower inflows of cellulose-based feedstocks into western European chemical parks tightened availability and nudged suppliers toward higher quotations, and rising energy-linked processing costs added to the pressure.

- Refinishing clusters in southern France took more material across multiple grades. Buffer stocks thinned at Antwerp and Le Havre. Slimmer inbound flows exposed importers to short lead-time gaps, and with chemical-park operating costs elevated and cross-border demand steady, suppliers held their offers firm into late March.

South Korea:

- During Q1 2026, nitro cellulose prices in South Korea rose to USD 3,686/MT, up 3.34% QoQ. Electronics-grade coatings and industrial-printing makers lifted their buying. Fast-drying grades drew steady buyer interest. Import-reliant buyers swallowed higher landed costs as regional shipping constraints pushed freight up on the key inbound routes that feed local formulators and finishing lines.

- Port-adjacent storage and handling charges nudged delivered values up. Export-oriented finishing lines kept on ordering. Local formulators sourcing high-clarity grades took the incremental increases to lock in timely replenishment before scheduled production runs, and most held their inventory discipline tight throughout the period.

Argentina:

- In Q1 2026, nitro cellulose prices in Argentina jumped to USD 4,598/MT, up 4.46% QoQ. Thin domestic processing capacity deepened the reliance on imports. Peso swings made matters noticeably worse. Currency volatility inflated procurement costs, and inland logistics bottlenecks slowed deliveries to finishing plants in Buenos Aires and Santa Fe, where wood-coating and packaging demand stayed solid.

- Import parity pricing, driven by the currency, lifted landed costs above regional norms. Distributors locked in forward volumes to hedge ARS swings. Premium-grade supply remained patchy across the region. Fuel-handling limits and tight transport capacity on the inland trucking routes piled on more delivered-cost pressure, which reinforced the firm upward direction running through the quarter.

Drivers Influencing the Market:

Several factors continue to shape nitro cellulose pricing and market behavior:

- Coatings, Inks, and Wood-Finishing Demand: Automotive refinish, decorative coatings, printing inks, and wood-finishing lines keep the baseline order book full for nitro cellulose. Export-oriented plants amplify the seasonal swings. Shifts across these end-use sectors flow straight into the nitro cellulose price index, with order books and converter run rates steering procurement volumes from one quarter to the next.

- Cotton Linter and Cellulose Feedstock Costs: Production economics hinge on cotton linter and dissolving-grade cellulose costs, which track global cotton supply. As per the USDA, the 2025/26 average US upland cotton farm price was estimated at 60 cents per pound, down from 63 cents a season earlier. Cheaper fiber eased part of the feedstock burden. The purified-linter grades, however, stayed tight.

- Energy Expenditure in Nitration and Processing: Nitration, washing, and stabilization all draw heavy energy. Because power and gas tariffs sit near the heart of producer margins, any rise in regional energy costs squeezes spreads and feeds quickly into quotations. High-nitrogen grades carry a steeper energy load still.

- Ocean Freight and Logistics Economics: Shipping nitro cellulose and its inputs ties delivered costs to container-freight moves on the Asia-Europe and Transpacific lanes. Drewry's World Container Index rose 12% to USD 2,182 per 40-foot container in mid-December 2025, a third straight weekly gain led by firmer Transpacific and Asia-Europe rates. Higher box rates feed straight into landed costs for import-reliant buyers.

- Hazardous Material Handling and Regulatory Compliance: Being highly flammable, nitro cellulose comes with strict storage, transport, and handling rules. Insurers price that flammability risk too. Registration and safety-testing demands under tightening chemical frameworks pile on administrative and documentation costs, and those costs filter into pricing wherever hazardous-material and wet-storage enforcement runs strict.

- Trade Policy and Currency Dynamics: Import tariffs, export licensing for energetic grades, and currency moves all shape cross-border nitro cellulose trade. In import-reliant economies, weaker local currencies bite hardest, inflating procurement costs and widening regional price gaps that buyers rarely claw back inside one reporting quarter. Dual-use controls then tack on approval delays.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In November 2025, researchers at Malaysia's National Defence University built new stabilizers for nitro cellulose-based propellants. They benchmarked nitrogen-bearing candidates against conventional diphenylamine. Differential scanning calorimetry and vacuum stability tests showed the newer molecules raising decomposition onset temperatures and cutting gas evolution, a result pointing to safer long-term storage for cellulose nitrate propellants.

Outlook & Strategic Takeaways:

Looking ahead, the nitro cellulose market is expected to grow steadily through 2034, carried by automotive refinishing, industrial coatings, printing inks, and wood-finishing demand alongside newer specialty and high-solids uses. Feedstock cotton-linter trajectories, energy tariffs, and freight conditions will stay the decisive levers behind the nitro cellulose price forecast and supplier margins.

To navigate this complex landscape, stakeholders should:

- Evaluate Downstream Demand Indicators: Track coatings, ink, and wood-finishing order books across the main consuming regions each quarter. Match those demand signals to procurement cycles, tightening inventory positioning so overstocking does not creep in.

- Assess Freight Market Developments: Track container-rate moves on the Asia-Europe and Transpacific corridors to read landed-cost shifts early. Build rate-adjustment clauses into logistics contracts so they flex with prevailing spot-market conditions.

- Monitor Regional Price Differentials: Track quarterly price gaps across the USA, France, South Korea, India, and Argentina to surface cost-saving windows. Benchmark nitro cellulose price per MT against live contract rates before any sourcing decision goes ahead.

- Review Regulatory Compliance Costs: Audit storage, transport, and handling spend tied to flammable cellulose nitrate duties across every site. Hunt for operational efficiencies that ease the regulatory load without cutting into chemical-safety or wet-storage standards.

- Strengthen Currency Exposure Management: Hedge procurement billed in volatile currencies such as the Argentine peso to steady landed-cost projections. Sync treasury and procurement timelines so foreign-exchange cover lines up with expected import payments.

- Explore Emerging Application Segments: Probe growth openings in electronics-grade coatings, high-solids formulations, and specialty propellant uses to diversify the portfolio. Bring in research partners to weigh the commercial viability of novel nitro cellulose grades.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates: 12 deliverables/year

- Quarterly Updates: 4 deliverables/year

- Biannual Updates: 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)