Oxygen Price Falls 16.4% In South America, Increases 23.6% In Europe — Q4 2025 Update

02-Sep-2025

Summary:

The fourth quarter of 2025 brought sharply contrasting pricing outcomes across the global industrial gas market, with regional supply and demand conditions driving divergent trends. Oxygen prices moved between a 16.4% decline and a 23.6% increase QoQ, driven by a combination of excess production capacity amid weakening industrial demand and elevated energy cost pressures. Approximately 20 Million barrels of oil and petroleum products transited the Strait of Hormuz daily in 2025, a flow that has since slowed to a trickle following the US-Israeli conflict with Iran. This echoes as an energy supply shock that is pushing power and feedstock costs higher and may reverse the current downward price trajectory in key oxygen markets.

Oxygen Price Q4 2025:

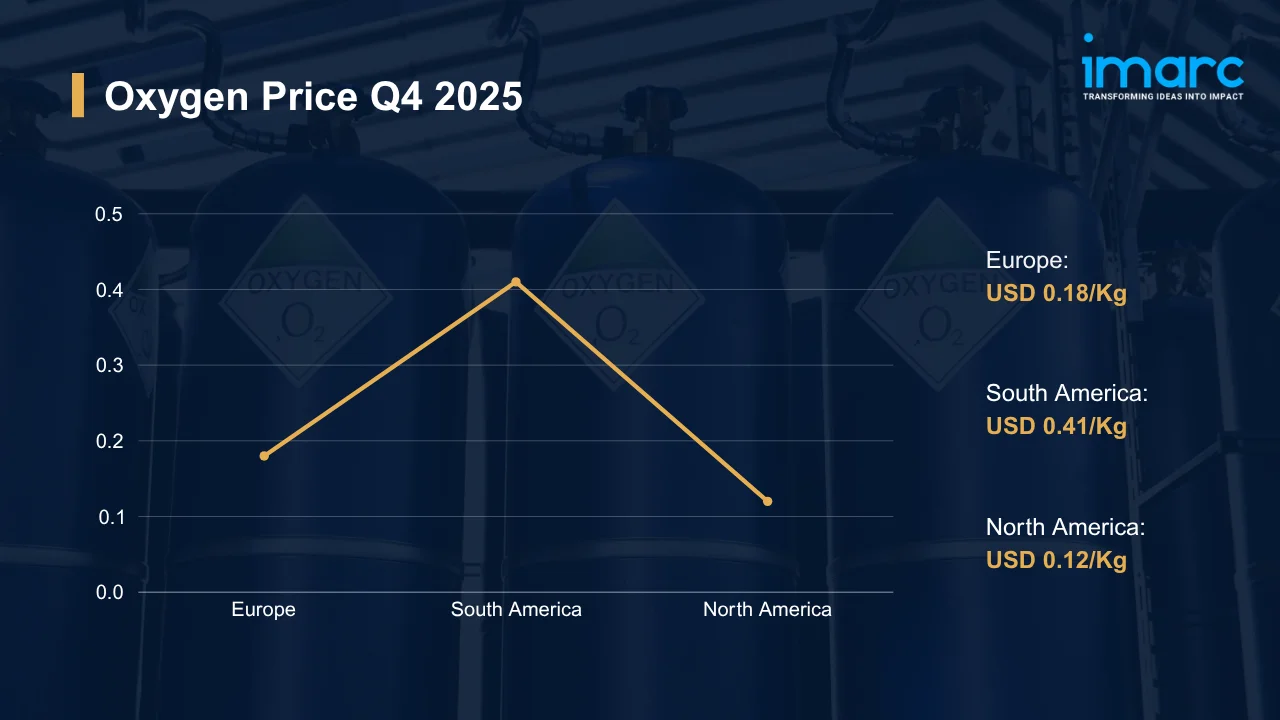

Regional prices (USD per KG) and QoQ changes Q4 vs Q3 2025:

| Region | Price (USD/KG) | QoQ Change | Direction |

|---|---|---|---|

| Europe | 0.18 | +23.6% | ↑ Growth |

| South America | 0.41 | -16.4% | ↓ Decline |

| North America | 0.12 | — | — |

To access real-time prices Request Sample

Kindly note: IMARC’s pricing database tracks oxygen price movements across major global markets.

What Moved Prices:

Europe:

- In Q4 2025, oxygen prices in Europe climbed to USD 0.18/KG, denoting a 23.6% QoQ advance driven primarily by sharply elevated power costs that weighed heavily on operators of energy-intensive cryogenic air separation units. Planned maintenance shutdowns at major industrial gas production facilities simultaneously tightened regional availability, reinforcing upward price pressure. The oxygen price chart for Europe shows a consistent upward trajectory throughout the quarter, underpinned by resilient procurement from steelmaking and metal fabrication customers.

- Healthcare and medical oxygen demand added meaningful offtake support, with rising patient volumes across European facilities sustaining procurement volumes above seasonal norms. Logistics and distribution cost inflation amplified ex-works pricing throughout the supply chain. Competitive import availability from outside the region provided limited relief, as European end users had little alternative to domestic sourcing amid tight plant capacity.

South America:

- During Q4 2025, oxygen prices in South America fell to USD 0.41/KG, down 16.4% QoQ, as a combination of softened steel and metals demand and newly commissioned air separation unit capacity pushed market conditions decisively bearish. Industrial gas producers faced reduced purchase volumes from their largest customers amid slower regional output, leaving the market structurally long on supply through much of the period.

- Declining upstream energy costs reduced production expense, limiting the floor under supplier pricing. Elevated distributor inventory positions prompted competitive discounting as stockists worked to clear holdings. Mining and chemical processing segments delivered subdued offtake, extending the market’s bearish tone. The oxygen price trend across South America reflected a broad market correction following a period of demand-driven firmness in the prior quarter.

North America:

- In Q4 2025, the oxygen trend in North America remained stable, with prices holding at USD 0.12/KG, reflecting a market operating near equilibrium rather than under genuine directional pressure. Throughout the quarter, the steel sector's offtake and healthcare procurement stayed steady, giving domestic producers a stable baseload demand to adjust output. Prominent industrial gas suppliers ensured sufficient distribution without surplus accumulation by maintaining dependable throughput from well-established air separation equipment.

- By keeping production costs under control, moderating energy costs supported stable pricing conditions without causing changes in the competitive landscape. The market equilibrium was strengthened by the steady secondary demand from the welding, cutting, and wastewater treatment segments. Significant price movement in either direction was constrained by the close alignment of supply and demand dynamics. Industrial gas supply chains continued to function without significant disturbance throughout this period, and converter run rates remained consistent.

Oxygen Price Outlook After the Israel–Iran–USA Conflict:

Rising Power Costs and Feedstock Pressure on Oxygen Production: Cryogenic air separation, which is the dominant production method for industrial oxygen, is among the most electricity-intensive processes in the industrial gas sector. As the conflict drives crude oil and natural gas prices sharply higher, European and Asian power markets are already registering elevated wholesale rates. According to Goldman Sachs, Brent crude climbed from around USD 65 in early June 2025 to the low USD 80s when US and Israeli forces struck Iran’s nuclear infrastructure, with the current conflict driving risk premiums an additional USD 14 per barrel above pre-conflict levels. This cost pressure flows directly into oxygen production economics and might push ASU operating prices meaningfully higher in energy-import-dependent regions.

Geopolitical Exposure and Oxygen Price Volatility Across Key Regions: The conflict introduces structural price uncertainty for oxygen markets in regions heavily exposed to Middle Eastern energy flows. Europe, which sources significant LNG volumes through the Strait of Hormuz corridor, faces the prospect of sustained power price volatility that might amplify the Q4 upward trend rather than allowing any correction. In South America, where energy cost reductions had been a key bearish factor, the conflict might reverse that tailwind if oil prices remain elevated. North America’s comparatively stable market might see renewed upward cost pressure if domestic energy prices respond to sustained global supply disruption.

Immediate Market Reaction:

As the conflict intensifies, oxygen markets are responding to the cascade of energy input cost increases that air separation unit (ASU) operators cannot readily absorb without price pass-through. Industrial gas producers in Europe are already contending with power rates trending well above quarterly averages, constraining their ability to offer competitive spot pricing. The oxygen price index remains under upward pressure across energy-import-dependent markets, where feedstock cost volatility is translating into tighter supplier margins and reduced willingness to offer discounted contract terms. Healthcare and steelmaking buyers, which represent the largest oxygen demand segments globally, might face tighter procurement conditions if production cost inflation outpaces contract renegotiation cycles.

Impact on Oxygen Prices:

The conflict might trigger several key changes in the oxygen market:

- Elevated Energy Input Costs for Air Separation Units: Electricity is the dominant variable cost in cryogenic oxygen production, representing a significant share of operating expense for ASU operators. As global power prices respond to higher crude oil and natural gas benchmarks driven by Strait of Hormuz disruption, ASU operators in energy-dependent markets will face a direct and immediate cost increase that is likely to be passed through to industrial and medical oxygen buyers, potentially reversing the downward trend observed in South America and widening the pricing premium already emerging in Europe.

- Supply Chain Disruption for Liquid Oxygen Transport: Liquid oxygen distribution depends critically on road tanker fleets and specialized cryogenic containers, both of which face escalating diesel fuel costs as the conflict keeps crude oil prices elevated. Freight rate increases for specialized cryogenic transport might compound ex-works price inflation for end users located far from production sites. Regions reliant on long-haul distribution networks, particularly inland industrial clusters in South America and Central Europe, will likely see delivered-cost premiums widening relative to plant-gate prices.

- Demand Volatility in Conflict-Exposed End-Use Sectors: Steel production, which represents one of the largest industrial oxygen demand categories globally, is particularly vulnerable to geopolitical-driven cost escalation in energy and raw material inputs. If steelmakers reduce blast furnace utilization in response to rising production costs or demand uncertainty, oxygen offtake might decline sharply in regions where steel industry procurement provides the base demand needed to support prevailing price levels. Healthcare oxygen demand, while comparatively inelastic, might also face procurement budget pressure in countries absorbing imported inflation.

Taken together, these three pressure channels, encompassing rising ASU energy costs, higher distribution expenses, and potential demand softening in key industrial segments, create a bifurcated market outlook. Oxygen prices in energy-import-dependent regions will likely trend higher, potentially extending Europe’s Q4 gains further. Markets where demand weakness was already the primary bearish factor, such as South America, might see only partial price recovery as cost inflation competes with structural oversupply.

Supply Chain Disruptions:

Industrial oxygen reaches end users through two primary supply chain pathways: pipeline supply at large integrated industrial sites and liquid oxygen distribution via cryogenic road tankers for smaller consumers. Both channels face direct conflict exposure. Pipeline-supplied steel mills and chemical complexes in the broader Middle East region are operating under severely constrained logistics environments, with port access at key Gulf terminals effectively halted. According to Kpler vessel tracking data, tanker transits through the Strait of Hormuz collapsed by approximately 92% in the week following the outbreak of hostilities on February 28. This disruption extends beyond crude oil flows, impacting the broader supply chain network that underpins industrial gas production costs in energy-import-dependent markets, and may persist for months if the conflict remains unresolved.

Oxygen supply chains are subject to secondary disruption due to the limited availability of specialist cryogenic transport assets, in addition to the direct energy cost channel. Road freight charges for liquid oxygen deliveries throughout Latin American and European distribution networks are rising due to the inflation of diesel fuel costs. In response, industrial gas providers may prioritize large accounts supplied by pipelines over long-distance tanker deliveries, resulting in localized supply constraints for hospital and mid-sized industrial customers. In order to protect themselves from prolonged utility price volatility, producers will probably expedite evaluations of alternative energy procurement options, such as power purchase agreements and on-site renewable generation.

Global Market Overview:

Globally, the oxygen industry was valued at USD 49.4 Billion in 2025. Market projections indicate steady growth, with the industry expected to reach USD 70.6 Billion by 2034, with a compound annual growth rate (CAGR) of 3.84% during 2026-2034. Growth is sustained by expanding healthcare infrastructure globally, surging demand for high-purity oxygen in semiconductor and electronics manufacturing, and growing consumption in steelmaking and chemical processing.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In July 2025, Hygenco Green Energies launched Maharashtra’s inaugural facility for producing green hydrogen and green oxygen in Chhatrapati Sambhaji Nagar, through a long-term supply contract with Sterlite Technologies (STL). This facility allowed STL’s optical fiber production process to utilize entirely green hydrogen and oxygen resources, consistent with its net zero objectives.

- In April 2025, Air Liquide unveiled plans to invest up to USD 850 Million in constructing a low-carbon oxygen industrial gas platform in Baytown, Texas, under a long-term clean industrial gas supply agreement. The project targeted reduced emissions intensity in oxygen production while reinforcing Air Liquide’s footprint in the US industrial gases market.

- In June 2025, the University of South Florida launched a USD 28 Million randomized clinical trial deploying hyperbaric oxygen therapy for US veterans and active-duty personnel with mild to moderate traumatic brain injury. The multi-year study involved over 30 researchers and aimed to validate whether HBOT could reduce inflammation, enhance neuroplasticity, and deliver measurable long-term benefit through rigorous placebo-controlled methodology.

Oxygen Price Forecast (2026):

Near-term oxygen prices will remain sensitive to the compounding effect of conflict-driven energy cost escalation and shifting industrial demand conditions in key consuming regions. European producers face the most acute upward pressure as power rates remain elevated, while North American market conditions will depend on whether domestic energy costs decouple from global benchmarks or track the broader price surge. Procurement hesitation from large industrial buyers might limit the speed of any price recovery in South America.

If geopolitical hostilities deepen and the Strait of Hormuz disruption persists beyond Q1 2026, oxygen prices will likely trend upward across all three tracked regions as ASU energy costs climb and logistics premiums widen, with Europe potentially revisiting multi-year price highs. A demand contraction in steel and chemical processing, triggered by broader macro softening, might partially offset cost-side pressures, keeping price gains contained rather than runaway. Conversely, a credible de-escalation that restores energy market stability might allow South American prices to stabilize at current levels while easing European cost inflation — outcomes that together will shape the oxygen price forecast throughout the year ahead.

Strategic Takeaways:

Looking ahead, the oxygen market is expected to maintain long-term growth momentum driven by expanding industrial gas demand across emerging markets. Energy cost dynamics and geopolitical risk will define near-term pricing trajectories, requiring agile procurement strategy planning from all stakeholders.

To navigate this complex landscape, stakeholders should:

- Track Regional Oxygen Price Differentials: Monitor quarterly pricing variations across Europe, South America, and North America to identify cost-saving procurement windows. Benchmark landed costs against contract rates to assess when spot buying offers material savings relative to term supply agreements. Tracking oxygen price per KG across key sourcing regions will help procurement teams capture value during regional price corrections.

- Monitor Geopolitical Risk Exposure: Track escalation dynamics in the current conflict and assess how shifts in hostility levels might affect oxygen pricing, feedstock availability, and logistics costs. Establish internal alert thresholds that trigger procurement or hedging action when energy cost benchmarks cross predefined levels tied to ASU operating economics.

- Diversify Supply Chain Routes: Evaluate alternative sourcing geographies and logistics corridors to reduce dependence on conflict-exposed supply chains. Secondary supplier agreements and contingency freight arrangements will provide critical resilience if primary distribution routes face disruption due to geopolitical escalation or regional infrastructure constraints.

- Monitor Healthcare and Steel Sector Demand Signals: Assess procurement activity levels from the two largest oxygen end use segments to anticipate demand-side price shifts before they appear in spot markets. Identify whether hospital infrastructure expansion and blast furnace utilization rates are trending in line with supply capacity growth to gauge future pricing equilibrium.

- Explore Long-Term Green Oxygen Supply Agreements: Evaluate emerging green hydrogen and green oxygen production platforms as potential lower-carbon supply alternatives for sustainability-focused operations. Early offtake agreements with green industrial gas producers, such as those being developed in India and the US, might lock in competitive pricing ahead of broader market adoption and premium pricing.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates — 12 deliverables/year

- Quarterly Updates — 4 deliverables/year

- Biannual Updates — 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)