RBD Soybean Oil Price Falls 3.5% in USA, Increases 1.3% in India — Q1 2026 Update

06-Apr-2026

Summary:

Q1 2026 brought a fractured pricing picture for the RBD soybean oil market, with North American demand softening against a backdrop of firming consumption across Asia and Europe. RBD soybean oil prices swung between a 3.5% decline and a 1.3% gain quarter-on-quarter, as feedstock availability, currency shifts, and logistics cost pressures pulled markets in opposing directions. Layered on top, the Israel–Iran–USA conflict introduced an energy cost shock with direct consequences for refining and freight. The war has halted most shipments via the Strait of Hormuz, through which 20% of global oil and gas supplies pass, causing a disruption currently transmitting directly through edible oil production costs and shipping rates alike.

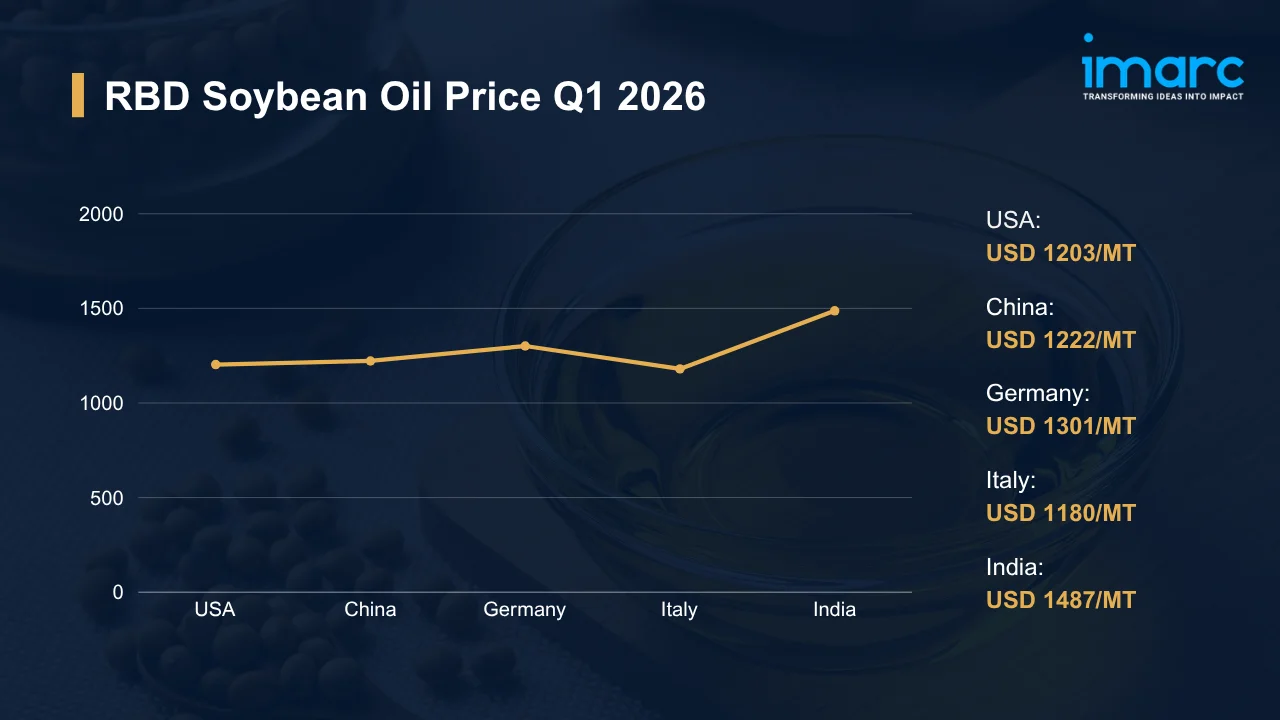

RBD Soybean Oil Price Q1 2026:

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| USA | 1203 | -3.5% | ↓ Decline |

| China | 1222 | +1.2% | ↑ Growth |

| Germany | 1301 | +1.0% | ↑ Growth |

| Italy | 1180 | +1.2% | ↑ Growth |

| India | 1487 | +1.3% | ↑ Growth |

To access real-time prices Request Sample

Kindly note: IMARC's pricing database tracks RBD soybean oil price movements across major global markets.

What Moved Prices:

USA:

- In Q1 2026, USD 1203/MT cleared for RBD soybean oil in the USA, down 3.5% from the USD 1246/MT logged in Q4 2025, as food-sector demand softened and biofuel blenders paused discretionary purchasing amid margin uncertainty. Post-holiday inventory drawdowns by food processors reduced restocking urgency through January and February, while biodiesel economics temporarily turned less compelling as renewable fuel credit prices lagged the initial crude oil surge triggered by the Israel–Iran–USA conflict. The RBD soybean oil price chart showed the quarter settling below Q4 2025 levels as crushers held back on forward sales, reluctant to commit supply into a market where both food and biofuel demand signals were momentarily mixed.

- Gulf Coast export logistics created additional downward price pressure in Q1, as Latin American buyers deferred contract execution in response to conflict-driven freight cost uncertainty. Midwest distribution costs edged higher due to diesel-related inland transport inflation, but these did not offset the broader demand softening that pulled spot prices below Q4 2025 levels. Dollar strength against several commodity-currency counterparts kept CIF import offers from competing origins competitive enough to suppress any meaningful price recovery through the end of March.

China:

- In Q1 2026, USD 1222/MT cleared for RBD soybean oil in China, a 1.2% gain over the USD 1207/MT recorded in Q4 2025, driven by firm demand from packaged food manufacturers ahead of the Lunar New Year consumption cycle. Pre-festival inventory builds across edible oil blending lines and institutional catering channels sustained a steady offtake pace through January, with buyers absorbing modest CIF cost increases without meaningful volume pullback. South American soybean arrivals were steady through Qingdao and Tianjin, keeping crush margins manageable, though freight surcharges triggered by the Middle East conflict introduced an upward bias to imported feedstock costs from February onward.

- The Israel–Iran–USA conflict added complexity to China’s procurement calculus from February onward, as Cape of Good Hope rerouting inflated freight bills on South America–Asia lanes and war-risk insurance premiums widened CIF spreads. Beijing’s reserve procurement policy continued to anchor structured contract buying, preventing the kind of spot-market volatility seen in less regulated import markets. RMB-USD cross rates held relatively stable through Q1, limiting additional currency-driven cost escalation and keeping landed price increases contained to conflict-related freight factors rather than any deterioration in underlying soybean supply availability.

Germany:

- In Q1 2026, USD 1301/MT was the reported price for RBD soybean oil in Germany, up 1.0% from USD 1288/MT in Q4 2025, as biodiesel blending mandates under Germany’s renewable fuel framework sustained industrial demand and Middle East conflict-driven freight inflation lifted CIF import costs at Hamburg and Rotterdam. High crude oil prices made blending economics attractive for energy-sector buyers, whose increased offtake tightened available supply for food processors in the short term. EU-level traceability and deforestation regulation compliance requirements continued to add a certified-origin premium layer that favored established suppliers and kept offer prices firm even as food-sector volumes held flat.

- Food processing demand across bakery, margarine, and industrial fat applications remained steady through Q1 but could not fully offset cost pressures created by freight inflation and energy-sector competition for feedstock. War-risk insurance surcharges on inbound South American cargoes were passed through directly to CIF offers, narrowing the margin advantage that German importers had previously relied on from competitively priced origin supplies. Buyers locked into annual contracts absorbed the quarterly increase passively, while spot-market participants faced a more expensive and thinly offered book through February and March as conflict-related logistics costs embedded themselves in carrier tariff sheets.

Italy:

- In Q1 2026, USD 1180/MT cleared for RBD soybean oil in Italy, up 1.2% from the USD 1166/MT recorded in Q4 2025, as HoReCa operators and food manufacturers accepted modestly higher prices driven by freight cost pass-through from Middle East conflict disruptions. Restaurant chains, catering groups, and pasta sauce manufacturers maintained steady procurement volumes through Q1, absorbing the incremental cost increase rather than reducing orders, as the price differential against alternative vegetable oils remained manageable. Italy retained its price-sensitive character, with buyers continuing to rotate among South American and Central European origin suppliers to protect margins, but conflict-driven freight inflation narrowed the spread between competing offers.

- Northern Italian food processors running rolling 4–6 week procurement cycles faced higher CIF offers on South American-origin cargoes as Cape rerouting added freight cost layers that suppliers passed forward promptly. Sustainability and traceability documentation requirements compressed the pool of lowest-cost eligible suppliers, reducing the downward pricing pressure that multi-origin competition had previously generated. Despite the 1.2% quarterly increase, Italy maintained the lowest price level among the five tracked markets, reflecting the structural advantage of its access to multiple competitively priced origin corridors that absorbed, but did not fully offset, the impact of elevated logistics costs.

India:

- In Q1 2026, USD 1487/MT was the market price for RBD soybean oil in India, up 1.3% from the USD 1468/MT recorded in Q4 2025 and the highest among all five tracked markets, as rupee depreciation against the US dollar continued to inflate the local-currency cost of dollar-denominated imports. Post-Diwali inventory normalization had reduced restocking urgency early in the quarter, but distribution requirements ahead of the rabi harvest cycle kept procurement volumes flowing through Kandla and Mundra ports.

- The Israel–Iran–USA conflict amplified India’s structural vulnerability as a large net importer of edible oils: Cape of Good Hope rerouting added 10–14 days to South American soybean oil voyages, tying up vessel capacity and raising bunker costs that carriers passed through directly to CIF offers. Government import duty policy remained under active review through the quarter, keeping buyers cautious about over-committing forward volumes and limiting procurement planning horizons at solvent extraction plants to four to six weeks.

RBD Soybean Oil Price Outlook After the Israel–Iran–USA Conflict:

Rising Energy Costs and Feedstock Price Pressure for RBD Soybean Oil: Natural gas and electricity are consumed at every stage of RBD soybean oil refining: crude degumming, bleaching, and high-temperature deodorization all draw on energy inputs that move closely with crude oil. High Brent crude oil prices are already pushing utility and bunker fuel bills sharply higher at processing plants in Brazil, Argentina, and Asia—the three origin regions that collectively supply the bulk of globally traded volumes. The conflict has effectively halted a significant portion of global crude and natural gas supply, eliminating the pricing cushion refiners previously relied upon to absorb input cost spikes. Margins might compress to the point where crushers and refiners delay or reduce output rather than sell below cost, tightening effective supply even in origin regions that face no direct conflict exposure.

Regional Price Volatility and Demand Uncertainty for RBD Soybean Oil: Price discovery across RBD soybean oil markets has deteriorated sharply since hostilities began, with buyers in import-reliant markets unwilling to commit to forward volumes when freight costs, currency values, and end-market demand are all moving simultaneously. 3–6 month procurement planning cycles are functionally broken for many buyers. Packaged food manufacturers might reduce contract commitment lengths to four to six weeks to preserve flexibility, while institutional catering operators could trim menu-dependent oil volumes as operating cost pressures compress their own margins. This demand-side hesitation, layered on top of the supply-side cost shock, will likely widen the price gap between spot and forward market RBD soybean oil offers well into Q3 2026.

Immediate Market Reaction:

Trade flows that previously moved through Gulf transit points are being rerouted, lengthened, and re-priced at speed—and the RBD soybean oil market is not immune. South American exports heading to the Middle East and South Asia face Cape of Good Hope detours adding 10 to 14 days and several hundred dollars per MT in extra fuel and carrier costs. The RBD soybean oil price index will likely diverge between origin FOB benchmarks and destination CIF levels as this freight premium embeds itself in offer sheets. As of March 2, 2026, war-risk insurance surcharges of USD 1,500–4,000 per container were already being applied by major carriers, a cost that falls directly on CIF-basis buyers. Producing regions in Brazil, Argentina, and the US Midwest face no direct operational disruption, though their export pricing will adjust upward as freight demand tightens available carrier capacity on the currently busier Cape route.

Impact on RBD Soybean Oil Prices:

The conflict might trigger several key changes in the RBD soybean oil market:

- Energy-Driven Processing Cost Escalation: Deodorization alone consumes a major portion of the total thermal energy used in RBD soybean oil refining, making natural gas price movements a direct driver of per-MT production cost. With Brent crude oil prices increasing, gas tariffs at processing plants in Brazil, Argentina, and Southeast Asia will push operating costs well above Q4 2025 levels. Refiners facing this margin squeeze will pass costs forward. FOB export offers will rise, and buyers on CIF contracts may face additional processing-cost inflation even before freight surcharges are added.

- Biodiesel Demand and Feedstock Competition: Rising crude oil prices flip the biodiesel economics from marginal to highly attractive, and US and EU blenders will accelerate soybean oil offtake to capitalize on blending economics. This pull from the energy sector directly competes with food industry demand, historically the dominant buyer of RBD soybean oil. The price floor will rise across both use channels as a result: food manufacturers cannot simply step back and wait while biofuel producers bid aggressively, so the competition will keep prices elevated even if physical soybean supply remains uninterrupted.

- Currency and Financing Cost Volatility: India’s rupee, the Indonesian rupiah, and several Middle Eastern import-market currencies have weakened against the US dollar since the conflict began, automatically raising the local-currency cost of every dollar-denominated RBD soybean oil cargo. Currency depreciation is increasing domestic procurement costs even without any change in global offer levels. Tighter trade finance conditions, with banks incorporating higher risk premiums into commodity credit lines, are adding pressure and prompting some smaller buyers to shorten coverage windows or scale back contracted volumes.

Three reinforcing pressures, including rising refinery input costs, intensified biodiesel feedstock competition, and import-market currency weakness, will keep RBD soybean oil prices under upward stress through at least Q2 2026. None of these forces is self-correcting in the near term. Energy costs will not fall until the conflict recedes, blending economics will stay favorable as long as crude prices stay elevated, and currency recovery takes quarters, not weeks. Procurement teams that lock in forward contracts now will likely secure pricing below where offers stand by mid-year; those that wait for clarity might find the market has moved sharply past their budget assumptions.

Supply Chain Disruptions:

Maersk, MSC, Hapag-Lloyd, and CMA CGM have all suspended Strait of Hormuz transits and rerouted fleets via the Cape of Good Hope, adding 10 to 14 days and substantial bunker costs to every South America–Asia and South America–Middle East soybean oil voyage. For bulk liquid cargoes moving in flexi-tanks or ISO containers, these added voyage days translate directly into per-MT freight cost increases that carriers are passing through immediately. During March 2026, spot container rates on major global routes rose approximately 150% since the conflict began. RBD soybean oil buyers in India, Egypt, and the UAE who relied on CIF pricing are currently absorbing elevated freight premiums compared to pre-conflict levels on affected routes.

The extended transit times and higher freight costs are disrupting inventory planning and delivery schedules in the RBD soybean oil market. Import-dependent buyers will face reduced visibility on shipment timelines, increasing the risk of stockouts or the need to hold higher safety inventories. In response, some participants might diversify sourcing routes or shift toward FOB contracts to gain greater control over logistics, while others might renegotiate delivery terms to better manage cost volatility and supply uncertainty.

Global Market Overview:

Globally, the RBD soybean oil industry reached a volume of 56.8 Million Tons in 2025. Market projections indicate steady growth, with the industry expected to reach 64.1 Million Tons by 2034, with a compound annual growth rate (CAGR) of 1.33% during 2026–2034. Food industry expansion in South and Southeast Asia is generating the most durable volume growth, as rising household incomes shift cooking practices toward packaged and refined oils. Oleochemical manufacturers in Malaysia and Indonesia are absorbing increasing volumes for personal care and industrial applications, diversifying demand beyond traditional food channels.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In November 2025, a study was published by researchers demonstrating that specific natural antioxidant compounds could notably enhance the oxidative stability of RBD soybean oil when subjected to accelerated storage and frying conditions. The research indicated that phenolic extracts are capable of chelating trace metals in RBD soybean oil, thus postponing the development of lipid oxidation products, such as hydroperoxides and malondialdehyde. The study emphasized actionable insights for edible oil manufacturers seeking to improve the shelf life and quality of RBD soybean oil by using natural antioxidants instead of synthetic additives.

RBD Soybean Oil Price Forecast (2026):

Freight cost inflation from the Hormuz closure is already embedded in Q1 2026 landed price offers, and that pressure will not lift quickly. Cape of Good Hope rerouting adds 10 to 14 days per voyage, tying up vessel capacity and raising bunker costs across every South America–Asia and South America–Europe lane used by soybean oil traders. Biodiesel blending economics will sustain an aggressive energy-sector bid for soybean oil feedstock through at least H1. Origin supply from Brazil and Argentina remains physically adequate, but the cost of moving that supply to consuming markets will keep FOB-to-CIF spreads wide, sustaining elevated delivered prices even as origin benchmarks hold relatively steady.

Two scenarios will define H2 2026 pricing. Under an escalation scenario, with Hormuz closures extending through Q2, sustained crude above USD 110, and no credible ceasefire, landed RBD soybean oil prices in key import markets may rise significantly above Q1 2026 levels as freight, insurance, and processing costs compound. Procurement teams locked into fixed-price contracts will face margin pressure while spot buyers might scramble. Under a stabilization scenario, a ceasefire and gradual freight normalization will bring container rates down, and with South American supply ample, prices might retrace from conflict-inflated highs as CIF spreads compress. Monitoring both scenarios with real-time data inputs is the only way to time sourcing decisions correctly, making a structured approach to the RBD soybean oil price forecast indispensable for procurement planning through the remainder of 2026.

Strategic Takeaways:

Looking ahead, the RBD soybean oil market is expected to face a multi-front cost pressure cycle driven by freight disruption, biodiesel feedstock competition, and geopolitical energy shocks that will take at least two quarters to resolve. Buyers and producers alike will need scenario-aware procurement strategies, not the static annual contracts that worked well in calmer markets.

To navigate this complex landscape, stakeholders should:

- Monitor Geopolitical Risk Exposure: Watch Hormuz transit data, Brent price movements, and ceasefire negotiation signals simultaneously, since all three feed directly into the cost of sourcing RBD soybean oil. Internal price alert thresholds tied to elevated crude levels and higher container rates will give procurement teams clear trigger points to shift from passive contract coverage to active hedging or emergency spot buying before costs rise further.

- Diversify Supply Chain Routes: Qualify suppliers in both Brazil and Argentina, before freight normalization makes the urgency feel less acute, since origin diversification across South Atlantic ports reduces dependence on any single routing corridor. Contingency freight agreements pre-negotiated with carriers operating Cape routes will matter more than spot market scrambling if the Hormuz closure extends into Q3; secondary logistics arrangements cost far less to set up in advance than to execute under pressure.

- Track Biodiesel Policy and Feedstock Demand: US Renewable Fuel Standard volumes, EU blending mandate reviews, and India’s biodiesel policy calendar each have the power to move soybean oil demand by millions of metric tons per year, making them procurement planning inputs rather than background reading. Rising crude oil prices make renewable diesel (RD) and biodiesel margins attractive enough to crowd food buyers out of the spot market at critical restocking moments. Tracking the RBD soybean oil price per MT alongside biofuel credit prices will flag when that crowding-out risk is building before it hits offer sheets.

- Strengthen Supplier Qualification and Contingency Planning: Run a formal supplier qualification exercise across at least two secondary origins. Paraguay and Ukraine are viable RBD soybean oil sources that sit outside the current conflict disruption zone and remain accessible via non-Hormuz routing. Documentation packages, quality certification alignments, and logistics connectivity assessments take four to eight weeks to complete. Teams that start early will have workable backup options in place before Q3 price pressure peaks, while those who wait for an emergency will be qualifying suppliers under time pressure that invariably raises cost and risk.

- Engage in RBD Soybean Oil Price Trend Analysis: Tracking the RBD soybean oil price trend across all five tracked markets simultaneously will expose the price divergence that is currently opening between conflict-exposed import regions and insulated producing regions, leading to a divergence that creates real arbitrage and timing opportunities for well-positioned buyers. Quarterly trend analysis that maps origin FOB movements against destination CIF changes will also flag when freight normalization is beginning to compress the spread, giving procurement teams a data-driven signal to shift back toward longer-horizon contracts.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates — 12 deliverables/year

- Quarterly Updates — 4 deliverables/year

- Biannual Updates — 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

.webp)

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)