Sodium Citrate Price Increases 7.2% in China, 4.3% in Argentina — Q1 2026 Update

29-Apr-2026

Summary:

Q1 2026 closed firmer for sodium citrate. Across all five tracked markets, sodium citrate prices advanced as pharmaceutical formulators, packaged-food converters, and beverage producers pulled steadily, with tightening export windows and disciplined producer offers reinforcing the upward bias through March. Movements ranged between a 2.4% rise and a 7.3% gain on a QoQ basis. Brent crude prices topped USD 106 per barrel in late April 2026, as Strait of Hormuz tensions deepened, layering fresh upstream cost pressure onto petrochemical input markets.

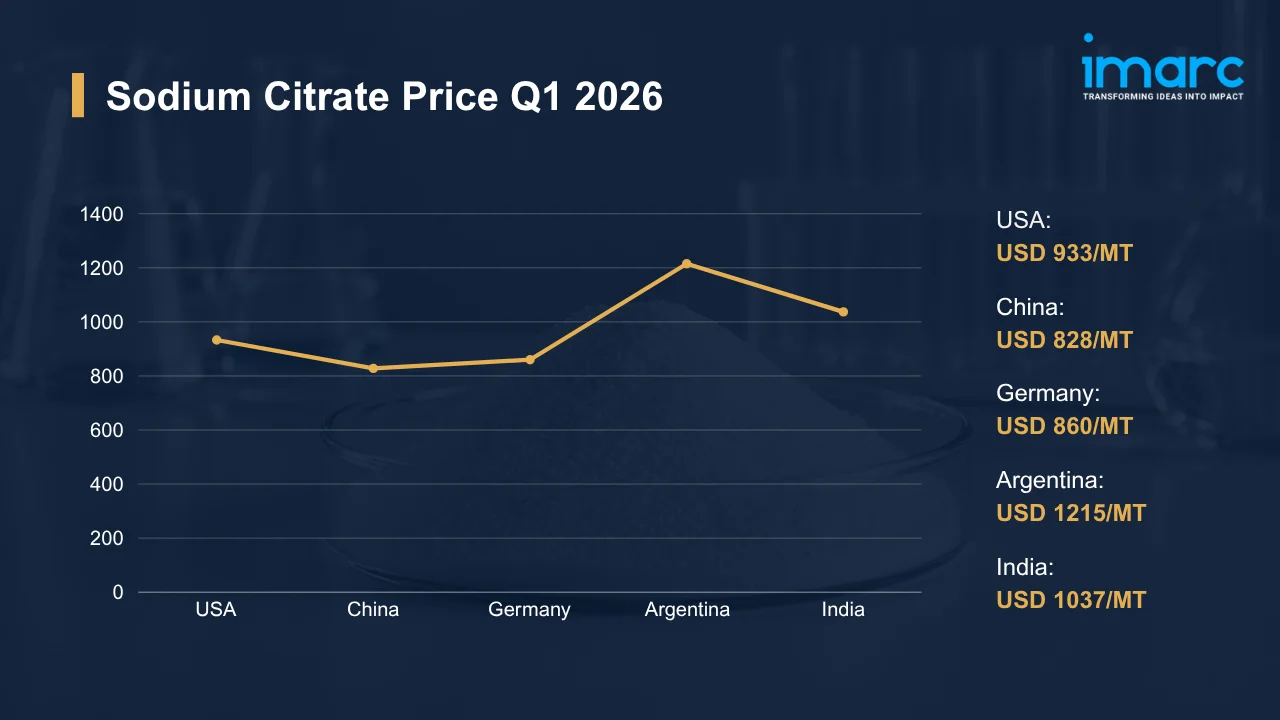

Sodium Citrate Price Q1 2026:

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| USA | 933 | +3.5% | ↑ Growth |

| China | 828 | +7.2% | ↑ Growth |

| Germany | 860 | +2.3% | ↑ Growth |

| Argentina | 1215 | +4.3% | ↑ Growth |

| India | 1037 | +3.6% | ↑ Growth |

To access real-time prices Request Sample

Kindly note: IMARC’s pricing database tracks sodium citrate price movements across major global markets.

What Moved Prices:

USA:

- In Q1 2026, sodium citrate prices in the USA reached USD 933/MT on firm food-processing and pharmaceutical pull. Beverage demand held steady through the quarter. Buoyed by controlled domestic output and limited import variability, supply stayed balanced, with raw-material cost pass-through from upstream citric acid producers nudging March settlements above year-end benchmarks across most contracts.

- Asian import availability tightened through Q1. Reflecting steady gains alongside firm Gulf Coast logistics costs and stable inland freight conditions, the latest sodium citrate price chart held its upward path through March, with pharmaceutical and personal-care channels absorbing shipments at firm offers and converters pulling back from large-volume restocking. Procurement teams secured measured volumes only to safeguard Q2 production schedules.

China:

- In Q1 2026, sodium citrate prices in China rose to USD 828/MT, marking the steepest gain across tracked markets. Spot availability tightened across the quarter. Combined with firm export interest, demand from food additives and industrial applications drove producer pricing power higher, while stable production rates and consistent processing expenses prevented any margin slippage even as utility costs ticked upward at certain coastal facilities.

- Domestic FMCG absorption stayed resilient through March. Across major Guangzhou and Yiwu trading hubs, citric acid feedstock costs held firm on raw-material tightness, lifting offer levels and giving exporters added negotiating leverage as CNY exchange rate dynamics turned mildly favorable on the export side. Buyers across food-grade and industrial channels accepted higher contracts to secure assured volumes through Q2.

Germany:

- In Q1 2026, sodium citrate prices in Germany advanced to USD 860/MT on stable food-preservation and pharmaceutical demand. Regional supply held consistent through March. Backed by balanced import availability paired with controlled domestic output, stable operational and transportation costs supported firm pricing through the quarter, while EU compliance overheads continued weighing on net offer levels reaching converters.

- Mittelstand purchasing patterns held measured throughout March. Across the Rhine corridor, logistics functioned smoothly even as freight surcharges and elevated electricity tariffs continued influencing supplier offers, with EU compliance overheads lifting effective landed prices for downstream beverage and pharmaceutical buyers. Beverage manufacturers absorbed incremental price adjustments to safeguard production schedules through the quarter.

Argentina:

- In Q1 2026, sodium citrate prices in Argentina reached USD 1215/MT, the highest absolute level across all tracked markets. Across the quarter, stable consumption patterns reinforced supplier power. Firm pull from food-processing and beverage industries, combined with relatively controlled domestic production and limited import availability, supported the upward trajectory through the quarter despite peso volatility chipping at converter purchasing budgets.

- Argentina runs heavily import-dependent through the year. Across Buenos Aires packaging hubs, peso volatility raised landed costs for processors and pushed beverage manufacturers to absorb higher contract revisions, even as domestic offtake stayed firm on steady food-processing demand. Higher port handling fees fed directly into supplier negotiations, while distributors held cautious inventory strategies through the quarter.

India:

- During Q1 2026, sodium citrate prices in India rose to USD 1037/MT on sustained packaged-food, dairy-processing, and pharmaceutical demand. Spot supply stayed tight through March. Backed by stable domestic production paired with steady export inquiries from regional Asian markets, firm raw-material and energy costs reinforced the upward pricing direction across major trading hubs spanning Mumbai, Ahmedabad, and Hyderabad converters.

- Post-monsoon FMCG restocking sustained converter demand. On the export side, inquiries from Middle East and Southeast Asian buyers tightened domestic availability through Q1, with logistics costs at western ports holding firm and supporting elevated landed prices into March settlements. Pharmaceutical-grade buyers accepted incremental contract revisions to secure feedstock continuity.

Sodium Citrate Price Outlook After the Israel–Iran–USA Conflict:

Energy Cost Pressure and Petrochemical Feedstock Strain on Sodium Citrate: The primary input is citric acid. Although sodium citrate derives from citric acid rather than crude petrochemicals, the conflict tightens ancillary input costs for chemical producers globally as petrochemical-linked utilities and freight benchmarks climb sharply through Q2.

Regional Price Volatility and Demand Uncertainty for Sodium Citrate: Procurement teams move cautiously across the board. Across the segment, macro-level uncertainty weighs on sentiment among food, beverage, and pharmaceutical buyers globally, while currency volatility in oil-import-dependent economies reshapes effective landed costs for sodium citrate week to week. End use buyers might delay forward contracts, while Asian and European exporters could renegotiate volumes if downstream demand softens unevenly.

Immediate Market Reaction:

The market reacts in real time. As the conflict escalates and shipping disruptions ripple through the Persian Gulf, the sodium citrate market faces secondary exposure through energy-linked production costs and freight rate volatility, with producers in Asia and the Middle East delaying shipments as port access tightens. Across other regions, distributors reposition inventory toward safer trade corridors. The sodium citrate price index might respond unevenly across regions as procurement teams hedge against further escalation, with buyers concentrating purchases in shorter-cycle contracts to limit exposure. Across export markets, exporters watch for cues from feedstock and logistics benchmarks before committing forward volumes.

Impact on Sodium Citrate Prices:

The conflict might trigger several key changes in the sodium citrate market:

- Elevated Energy and Feedstock Costs: The cost chain runs upstream from crude through citric acid. Once oil price escalation lifts production costs at energy-intensive plants in Asia and Europe, where naphtha and gas inputs remain exposed to Strait of Hormuz disruption, sodium citrate manufacturers will absorb pressure through Q2 and Q3. Producers might pass costs onto buyers via contract revisions, while plants short on natural gas could throttle utilization and tighten regional availability.

- Freight Rate Inflation Across Trade Routes: Freight pressure follows oil pressure quickly. Across Middle East-adjacent shipping corridors, container and bulk freight rates will climb on rerouting and war-risk insurance premiums, lifting CIF prices for sodium citrate consignments bound for European, African, and Asian end use markets. Buyers across Latin America, Africa, and parts of Asia, where import dependency runs structurally high, might face widened landed-cost differentials versus FOB benchmarks, prompting tighter procurement scheduling and selective forward cover.

- Disrupted Production and Export Flows: Production geography compounds both pressures meaningfully. Once hostilities affect plant access or export logistics, Iranian and adjacent Gulf-region chemical operations face direct exposure that narrows global citric acid availability and feeds into sodium citrate offer levels worldwide. Asian and European producers will capture displaced demand, but operating-rate adjustments and inventory rebalancing might lengthen lead times for just-in-time buyers in Latin America and Africa.

These three pressures interlock through 2026. Combined, they will shape sodium citrate price trajectories with magnitude tied to conflict duration and energy-market volatility, while buyers might secure forward cover where contractual flexibility allows and producers will tighten allocation discipline. Volatility across petrochemical-linked input markets will keep procurement teams vigilant on feedstock and freight benchmarks.

Supply Chain Disruptions:

Persian Gulf chokepoints face direct exposure. Across the conflict zone, sodium citrate flows traverse Middle East-adjacent shipping corridors, Asian export routes, and European port access points, all under strain from ongoing hostilities, while Persian Gulf chemical hubs run at curtailed export capacity. Per CNBC reporting in late April, cumulative supply losses tied to the near two-month Strait of Hormuz closure had already exceeded half a billion barrels of crude, condensates, and natural gas liquids, signaling acute downstream cost transmission across import-dependent end-use industries.

Substitution paths begin to take shape. Across feedstock chains, Asian and European producers will likely emerge as primary alternatives as Gulf-region availability narrows. On the buyer side, procurement teams might shift to overland or trans-Pacific routing for time-sensitive consignments, while higher freight surcharges will lift landed prices through 2026 and distributors widen inventory buffers. Carrying-cost discipline limits aggressive accumulation, leaving forward contracts with price reopener and force majeure provisions as the most resilient procurement path.

Global Market Overview:

Globally, the sodium citrate industry was valued at USD 954.6 Million in 2025. Market projections indicate steady growth, with the industry expected to reach USD 1,375.1 Million by 2034, with a compound annual growth rate (CAGR) of 4.01% during 2026-2034. Across food and beverage (F&B) processing, demand remains structurally anchored. Pharmaceutical, personal-care, and industrial cleaning applications add incremental volume globally, while regulatory shifts toward cleaner-label additives and emphasis on functional ingredient certifications reinforce the sodium citrate price trend through 2034.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In June 2025, India’s Directorate General of Foreign Trade (DGFT) announced a revised Standard Input Output Norm under the Chemical and Allied Product category, permitting 0.740 kg of citric acid monohydrate as the input allowance per kilogram of sodium citrate exported under the Advance Authorisation Scheme.

Sodium Citrate Price Forecast (2026):

Near-term direction stays firm through mid-2026. Across the major markets, sodium citrate prices will hold supported by sustained pull from food, beverage, and pharmaceutical end users, while procurement caution might rise if conflict-driven freight rates climb further into Q2 and Q3. Stable feedstock availability outside conflict-exposed regions should temper sharper price escalation.

Two scenarios bracket the year ahead. If geopolitical hostilities intensify, sodium citrate prices will face renewed upward pressure as energy and freight costs climb, lifting landed prices for import-dependent buyers and pushing producers in conflict-adjacent regions to curtail output. Conversely, a diplomatic resolution might ease shipping rates and restore feedstock flows, allowing prices to drift back toward pre-escalation levels by late 2026 and shaping the sodium citrate price forecast through the year ahead.

Strategic Takeaways:

Looking ahead, the sodium citrate market is expected to remain firm. Producers and procurement teams will balance feedstock cost exposure with downstream demand resilience as geopolitical tensions, regional freight variability, and end-use sector dynamics across food, beverage, and pharmaceutical channels continue evolving over the coming quarters into late 2026.

To navigate this complex landscape, stakeholders should:

- Monitor Regional Price Differentials: Track quarterly price variations across the USA, China, Germany, Argentina, and India to identify cost-saving procurement windows. Benchmark landed costs against contract rates and historical baselines, then optimize regional sourcing decisions throughout the rest of 2026.

- Monitor Geopolitical Risk Exposure: Track escalation dynamics in the conflict and assess how shifts in hostility levels might affect sodium citrate pricing, feedstock availability, and logistics costs. Establish internal alert thresholds that trigger procurement or hedging action when warranted.

- Diversify Supply Chain Routes: Evaluate alternative sourcing geographies and shipping corridors to reduce dependence on conflict-exposed trade lanes. Secondary supplier agreements and contingency freight arrangements will provide critical operational resilience if primary routes face disruption or extended port congestion.

- Adjust Procurement Strategy for Conflict Conditions: Adopt flexible contract structures with price reopener clauses and force majeure provisions to protect against geopolitical price spikes. Precautionary inventory buffers might reduce exposure if supply tightens abruptly across critical sourcing corridors and freight routes.

- Track Citric Acid Feedstock Costs: Monitor citric acid contract rates and spot market trends across major global producing regions. Energy-intensive citric acid production directly influences sodium citrate manufacturing costs, making upstream visibility essential for procurement teams negotiating supply commitments.

- Evaluate Currency and Trade Policy Shifts: Monitor ARS, INR, EUR, and CNY movements against the USD on a sustained basis. Import tariff and export-incentive shifts reshape effective sodium citrate price per MT calculations and supplier negotiation positions across major sourcing geographies.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates — 12 deliverables/year

- Quarterly Updates — 4 deliverables/year

- Biannual Updates — 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)