Steel Price Falls 3.3% in Malaysia, 0.9% in Germany — Q1 2026 Update

02-Apr-2026

Summary:

Q1 2026 delivered uniform price declines across all five tracked steel markets, with construction restraint, moderate industrial output, and competitive import availability all weighing on demand. Steel prices fell between 0.1% and 3.3% QoQ. With feedstock costs holding firm through most of the quarter, producer cost structures stayed largely stable. The Israel–Iran–USA conflict has since shattered that stability, with merchant vessel traffic through the Strait of Hormuz collapsing more than 85% as of March 6, 2026, threatening to disrupt energy and raw material flows critical to the global steelmaking supply chain.

Steel Price Q1 2026:

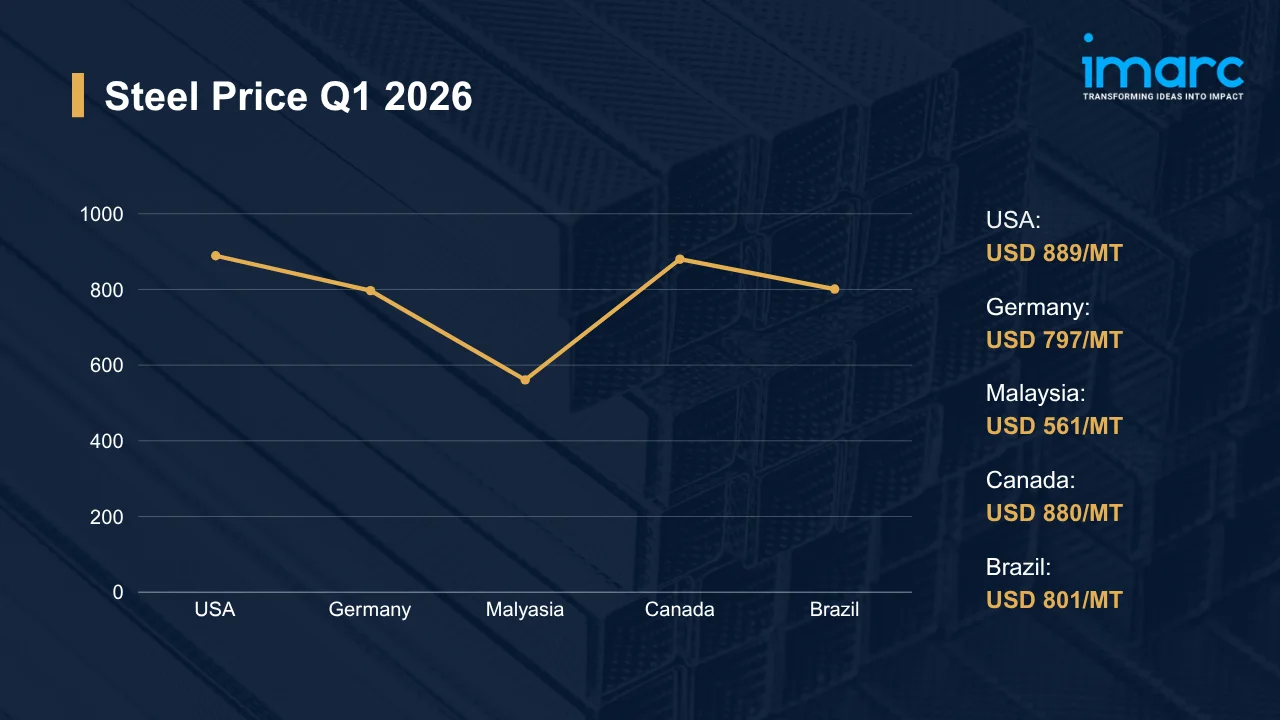

Regional prices (USD per MT) and QoQ changes Q1 2026 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| USA | 889 | -0.2% | ↓ Decline |

| Germany | 797 | -0.9% | ↓ Decline |

| Malaysia | 561 | -3.3% | ↓ Decline |

| Canada | 880 | -0.1% | ↓ Decline |

| Brazil | 801 | -0.5% | ↓ Decline |

To access real-time prices Request Sample

Kindly note: IMARC’s pricing database tracks steel price movements across major global markets.

What Moved Prices:

USA:

- In Q1 2026, USA steel prices reached USD 889/MT, a 0.2% QoQ decline. Service centers prioritized drawing down Q4-accumulated inventory rather than entering the spot market, a posture that kept offer levels under consistent downward pressure as balanced domestic mill output and moderated construction demand gave buyers no urgency to accelerate procurement.

- Across US distribution channels, import competition from Asian mills limited domestic seller pricing power through Q1. The steel price chart confirmed a consistent downward drift, with Gulf Coast service center procurement staying short-cycle as buyers sourced against confirmed fabrication orders rather than building speculative inventory positions.

Germany:

- In Q1 2026, German steel prices retreated to USD 797/MT, a 0.9% QoQ decline. Subdued automotive assembly procurement and constrained machinery sector demand drove the pullback, compounded by energy cost normalization that simultaneously reduced the producer cost floor and removed the pricing justification for sellers to maintain Q4 offer levels through the new period.

- Competing import volumes from neighboring European and Asian origins kept domestic mill pricing power limited throughout the quarter. Across the Mittelstand converter base, buyers followed the steel price trend lower through Q1, maintaining short-cycle purchasing as limited automotive recovery visibility and constrained industrial order books discouraged any meaningful forward volume commitment.

Malaysia:

- In Q1 2026, Malaysia recorded the steepest tracked decline, with steel prices settling at USD 561/MT for a 3.3% QoQ drop. Weak construction activity and slower infrastructure disbursements left producers with insufficient order coverage to hold Q4 offer levels, while limited regional export demand removed the supply absorption channel that could have cushioned the decline.

- Elevated regional supply from consistent Southeast Asian mill output kept buyers in a position of strong spot-market leverage through Q1. Pricing negotiations on flat and long steel categories trended lower as extended lead times and low order urgency allowed buyers to push offers down across successive purchasing cycles.

Canada:

- In Q1 2026, Canadian steel prices edged to USD 880/MT. Cross-border supply from the USA and efficient domestic service center operations kept competitive pressure present throughout the quarter, limiting sellers’ ability to stabilize pricing as construction and manufacturing activity remained steady but generated no meaningful incremental demand that could shift the market’s directional balance upward.

- Throughout Q1, supply chain operations ran efficiently, with service centers holding inventory closely aligned to confirmed order books. Domestic mill output tracked visible demand without surplus accumulation, eliminating the scarcity rationale that sellers might otherwise have used to resist buyers consistently pushing for lower contracted rates on construction and industrial steel grades.

Brazil:

- In Q1 2026, steel prices in Brazil fell to USD 801/MT, posting a 0.5% QoQ decline as slower infrastructure disbursements and measured industrial output together removed the demand foundation that had supported Q4 offer levels, leaving sellers exposed to persistent buyer resistance across both spot and contract channels throughout the quarter. Export channels offered no relief.

- Holding steady through Q1, domestic steel production maintained adequate supply without accumulating the surplus tonnage that might otherwise have added sharper downward pressure to already weakened offer levels. Market sentiment stayed cautious. Buyers avoided large-volume forward commitments, with limited project pipeline visibility constraining confidence in demand recovery.

Steel Price Outlook After the Israel–Iran–USA Conflict:

Rising Energy and Feedstock Costs for Steel: Steelmaking feedstock costs are responding sharply to the conflict’s energy transmission channel. Coking coal and coke prices moved higher in the immediate aftermath, as elevated oil prices fed directly into input costs. Producers relying on open-market sourcing may see raw material expenses increase faster than steel selling prices, putting pressure on margins.

Regional Price Volatility and Demand Uncertainty for Steel: Conflict-driven macro uncertainty is reshaping procurement expectations for steel. Across construction and industrial segments, buyers might defer volume commitments as project budget reassessments accumulate, a shift that could push the soft demand trajectory beyond what Q1 seasonal patterns alone would predict. Geopolitical risk premiums are rising faster than underlying cost structures.

Immediate Market Reaction:

Steel market participants have turned cautious on procurement and logistics planning as conflict dynamics unfold across the Persian Gulf. Through key trade corridors, billets, DRI pellets, and iron ore face Strait of Hormuz exposure, with Hormuz-adjacent terminal operations running well below pre-conflict throughput. These pressures have created export-channel uncertainty and tightened shipping conditions. Against this backdrop, the steel price index reflects a convergence of rising energy input costs, logistical constraint, and pervasive buyer caution, a combination that procurement teams are finding difficult to model.

Impact on Steel Prices:

The conflict might trigger several key changes in the steel market:

- Rising Energy Costs and Production Margin Compression: Surging crude oil prices are feeding into electricity costs for EAF operators and processing costs at integrated mills. Heading into the conflict, margins were already narrow. Should energy prices remain elevated through mid-2026, producers will face a direct choice between absorbing cost escalation or raising offer levels into a market where demand conditions are too weak to sustain higher pricing.

- Feedstock Supply Disruption and Raw Material Cost Escalation: Coking coal and iron ore routed through Persian Gulf corridors now face elevated war risk premiums and port throughput constraints at Hormuz-adjacent terminals. Rerouting around the Cape of Good Hope adds 10–14 days to voyage times. Where alternative feedstock origins exist, procurement teams will pivot, but premium spot pricing in non-Gulf origin markets might narrow mill margins for producers dependent on open-market purchasing rather than pre-contracted supply at fixed rates.

- Trade Route Disruption and Market Access Constraints: Routing steel export volumes through Middle Eastern distribution hubs toward South Asia and East Africa, producers face timing and volume uncertainty as Hormuz-adjacent port throughput falls. Buyers in affected markets might pivot quickly. Redirecting procurement toward Chinese and European origins will push cargo onto Cape of Good Hope corridors at significantly higher CIF landed costs, elevating delivered price levels even where underlying demand stays subdued.

These combined pressures create a complex pricing environment for steel through 2026, where soft demand will pull prices lower while conflict-driven input and logistics costs might simultaneously offset that downward momentum. From a forecasting standpoint, neither signal is straightforward. Producers and buyers must monitor both fronts actively.

Supply Chain Disruptions:

Steel’s supply chain is under active disruption. Routed through Gulf corridors, coking coal, iron ore, and DRI pellets are facing elevated war risk premiums and constrained port throughput at Hormuz-adjacent terminals, with producers unable to maintain pre-conflict delivery schedules. On March 1, 2026, major carriers, including Maersk and Hapag-Lloyd suspended Strait transits and rerouted around Africa, adding several extra days to voyage times, stretching raw material delivery windows and lifting landed procurement costs for steel producers across Europe and Asia.

Forced onto Cape of Good Hope routes, steel raw material shippers face higher bunker fuel costs and tightening vessel capacity as bulk demand for the Africa diversion surges. Domestic producers will likely build near-term inventory buffers. That procurement posture tightens available raw material tonnage in non-Gulf origins, while buyers locked into pre-conflict CIF pricing terms might find landed cost structures no longer competitive against domestically sourced alternatives, compressing import economics across multiple consuming regions.

Global Market Overview:

Globally, the steel industry reached a volume of 1,746 Million Tons in 2025. Market projections indicate steady growth, with the industry expected to reach 2,094 Million Tons by 2034, at a compound annual growth rate (CAGR) of 2.10% during 2026–2034. Construction expansion across Asia and Africa, rising automotive output, and sustained infrastructure investment are underpinning long-term demand growth. Regulatory pressure toward low-carbon steelmaking and the accelerating adoption of electric arc furnace technology is reshaping the global production cost structure.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In March 2026, the United Kingdom announced plans to significantly increase tariffs on imported steel, particularly from China, including sharp reductions in import quotas and higher out-of-quota duties aimed at protecting domestic producers and expanding production capacity, with a focus on building output in Wales.

- In June 2025, Nippon Steel finalized its USD 14.9 Billion acquisition of U.S. Steel, committing USD 11 Billion in investments through 2028, including USD 1 Billion for a new domestic US facility and USD 3 Billion for future expansion, positioning the entity to capitalize on US infrastructure growth.

- In January 2025, JFE Steel launched commercial sales of its JGreeX low-carbon steel through distributor JFE Shoji Pipe & Fitting Corporation, marking the product’s entry into the steel pipe sector and expanding the reach of green steel offerings to a broader base of industrial customers in Japan. JFE Steel and JKK intended to create a flexible sales system through this collaboration, emphasizing small lot shipments and rapid delivery.

Steel Price Forecast (2026):

Steel prices will stay under pressure. Through the first half of 2026, conflict-driven energy and logistics cost escalation is likely to prevent the demand-driven declines that soft construction and industrial activity would otherwise produce, keeping buyers and sellers locked in a narrow and unstable pricing band. Procurement caution might ease only if a clear directional signal emerges from either front.

Should hostilities intensify, steel prices will face renewed upward pressure as energy costs climb, freight rates widen, and war risk premiums extend across seaborne raw material trade routes. Scenario divergence is sharp. Conversely, if a diplomatic resolution restores Hormuz transit and lowers supply chain costs, demand-driven price weakness might gradually reassert itself, pulling prices back toward pre-conflict levels and shaping the steel price forecast across tracked markets through year-end.

Strategic Takeaways:

Looking ahead, the steel market is expected to sustain moderate growth, driven by infrastructure development, construction activity, and rising automotive production across emerging and developed economies. Conflict-driven input cost volatility and supply chain disruption will require procurement teams to adopt more adaptive and resilient sourcing approaches.

To navigate this complex landscape, stakeholders should:

- Monitor Geopolitical Risk Exposure: Track escalation dynamics in the conflict and assess how hostility shifts might affect steel pricing, feedstock availability, and logistics costs. Establish alert thresholds that trigger procurement or hedging action when key indicators move.

- Adjust Procurement Strategy for Conflict Conditions: Adopt flexible contract structures with price reopener clauses and force majeure provisions to protect against geopolitical price spikes. Precautionary steel inventory buffers might reduce exposure if conflict-driven supply tightening occurs abruptly along key procurement corridors.

- Track Regional Price Movements: Monitor price movements across all tracked regions to identify procurement windows and benchmarking opportunities. Tracking the steel price per MT across key markets enables buyers to optimize contract timing and limit exposure.

- Assess Upstream Feedstock and Energy Cost Exposure: Evaluate energy and raw material cost inputs feeding into steel pricing across key sourcing markets. Benchmarking feedstock costs against historical ranges helps procurement teams anticipate margin-driven adjustments before they transmit fully to spot market offer levels.

- Monitor Downstream Sector Health: Track demand indicators across construction, automotive, and industrial manufacturing segments to anticipate shifts in steel consumption volumes. Understanding which end-use sectors are expanding or contracting will enable earlier procurement positioning and reduce inventory misalignment risk.

- Evaluate Long-Term Supply Contracts: Assess the current balance between spot and contracted steel purchasing to determine whether forward agreements offer cost certainty during elevated volatility. Locking in supply pricing with trusted producers will reduce exposure to conflict-driven market disruptions and logistics cost escalation.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates — 12 deliverables/year

- Quarterly Updates — 4 deliverables/year

- Biannual Updates — 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

.webp)

.webp)

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)