Coconut Oil Price Falls 7.0% in Sri Lanka, 5.5% in Indonesia — Q1 2026 Update

23-Jul-2025

Summary:

Copra supply adequacy defined Q1 2026. Across all five tracked origins, coconut oil prices posted QoQ declines ranging from 3.0% to 7.0%, as oleochemical processors, personal care manufacturers, and specialty fat buyers reduced spot purchases after exhausting Q4 procurement budgets, leaving sellers without pricing support at loading ports. Tightening the risk outlook further, the Israel–Iran–USA conflict pushed Brent crude prices above USD 100 per barrel as of March 15, 2026, a development that is threatening to escalate freight and processing input costs for coconut oil importers.

Coconut Oil Price Q1 2026:

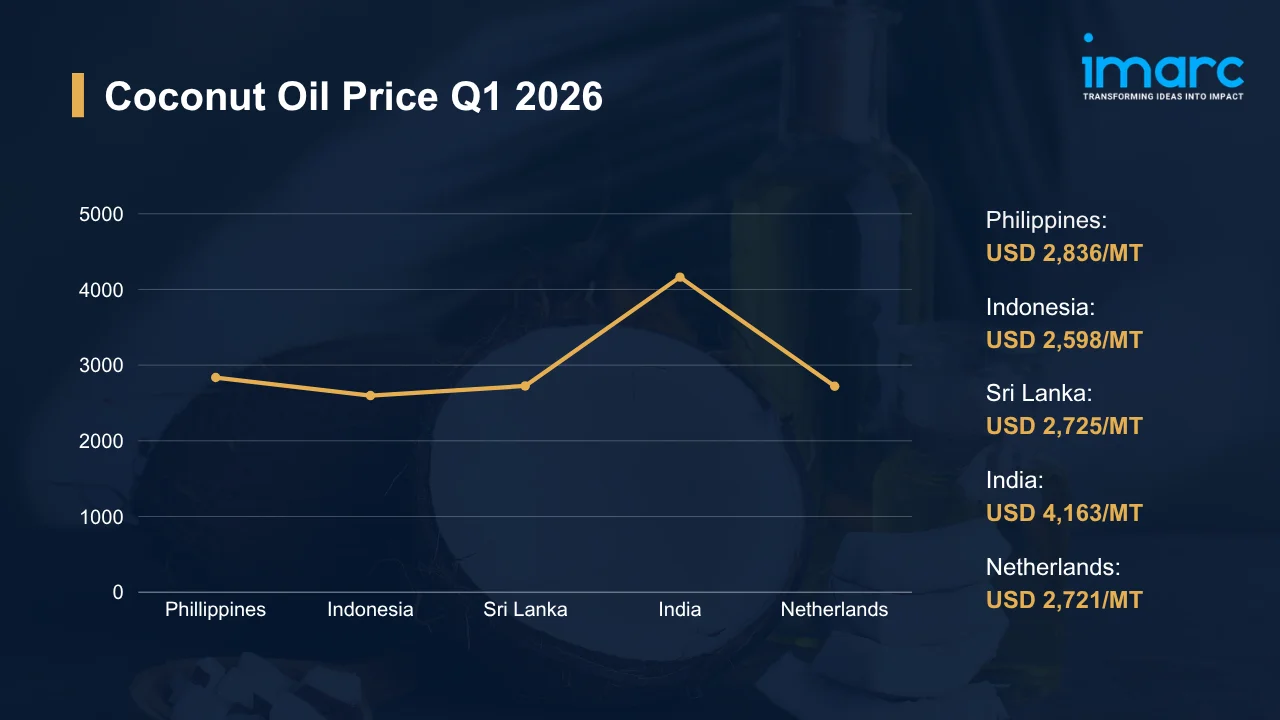

Regional prices (USD per MT) and QoQ changes Q1 vs Q4 2025:

| Region | Price (USD/MT) | QoQ Change | Direction |

|---|---|---|---|

| Philippines | 2,836 | -3.8% | ↓ Decline |

| Indonesia | 2,598 | -5.5% | ↓ Decline |

| Sri Lanka | 2,725 | -7.0% | ↓ Decline |

| India | 4,163 | -4.5% | ↓ Decline |

| Netherlands | 2,721 | -3.0% | ↓ Decline |

To access real-time prices Request Sample

Kindly note: IMARC’s pricing database tracks coconut oil price movements across major global markets.

What Moved Prices:

Philippines:

- At USD 2,836/MT in Q1 2026, Philippine coconut oil posted a 3.8% QoQ decline as export demand from food manufacturing and personal care converters contracted sharply following Q4’s active procurement cycle, dragging CIF offer levels downward across all major loading ports through March. The coconut oil price chart traced a consistent downward line as buyer appetite stalled.

- Competing CIF offers from Indonesian and Sri Lankan origins kept adequate spot tonnage visible throughout Q1, removing the pricing floor that Philippine exporters had relied on in prior quarters and compelling FMCG packagers and personal care formulators to adopt hand-to-mouth cover strategies rather than forward volume commitments. Short-cover positions persisted into March across all CIF destinations.

Indonesia:

- In Q1 2026, Indonesian coconut oil declined to USD 2,598/MT, a 5.5% QoQ contraction driven by muted restocking from European oleochemical processors and South Asian food manufacturers, both of which entered the quarter with inventory buffers accumulated during Q4 and saw little incentive to absorb additional spot supply. FOB loading volumes from Sulawesi and Sumatra ran below seasonal norms.

- Undercutting from Philippine origins eroded the pricing floor across Java’s crusher-led export segment throughout Q1, restricting Indonesian sellers to defensive offer levels that reflected tighter crushing margins rather than demand-led price discovery. Against this backdrop, buyers maintained short-cover CIF positions, deferring mid-year volume decisions as demand signals across Southeast Asian and European destinations remained ambiguous.

Sri Lanka:

- Sri Lanka registered the steepest QoQ loss among all five markets in Q1 2026, with prices at USD 2,725/MT reflecting a 7.0% decline as European edible oil processors and Asian personal care manufacturers reduced purchases against destination port inventory that had accumulated well above seasonal adequacy levels. Seller resistance collapsed under the weight of oversupplied CIF trade lanes.

- Throughout Q1, palm kernel oil parity at Rotterdam shifted decisively against Sri Lankan coconut oil, drawing European converters toward cheaper lauric alternatives and removing demand urgency that had supported Q4 offers. Running at elevated milling rates, Sri Lankan producers sustained high export availability through March, compressing FOB quotations and eliminating sellers’ ability to negotiate meaningful price floors across key destination markets.

India:

- At USD 4,163/MT in Q1 2026, Indian coconut oil recorded a 4.5% QoQ decline as improved South Indian copra harvests tightened the domestic supply gap that had boosted Q4 import urgency, reducing procurement motivation among personal care processors and household consumption-oriented food buyers across Kerala and Tamil Nadu. QoQ, the CIF import premium narrowed sharply.

- Higher copra arrivals across South Indian mandis depressed farm-gate prices and compressed refiner margins throughout Q1, removing the incentive to cover import volumes at prevailing spot offers and keeping refined coconut oil offer levels under persistent downward pressure. From palm kernel oil and palm-derived lauric substitutes, competitive pricing further constrained pricing headroom across pharmaceutical, cosmetic, and FMCG buying segments through the quarter.

Netherlands:

- At USD 2,721/MT in Q1 2026, Netherlands coconut oil eased 3.0% QoQ as post-Q4 restocking fatigue spread through European food manufacturing, cosmetics, and specialty fat converters, who collectively maintained conservative inventory positions and reduced competitive bid support during CIF Rotterdam price discovery sessions through the end of March. Buying interest ran below Q4 levels throughout.

- Sourcing under EU deforestation-free frameworks continued to channel European buying toward certified Philippine and Indonesian origins, sustaining a preference hierarchy that persisted despite tighter freight economics in Q1. Against this, Strait of Hormuz disruptions introduced latent uncertainty around import transit windows for Q2 cargoes, with logistics cost escalation emerging as a secondary but growing concern for European processors evaluating forward coverage.

Coconut Oil Price Outlook After the Israel–Iran–USA Conflict:

Rising Energy and Freight Costs for Coconut Oil Processing: High crude oil prices feed directly into copra crushing energy costs and coconut oil refinery fuel requirements, sharpening margin pressure across import-dependent processing hubs. Compounding this, On March 3, 2026, VLCC tanker rates reached a record USD 423,736 per day, climbing more than 94% from pre-conflict benchmarks as carrier availability tightened. Coconut oil CIF prices across deficit markets might absorb these elevated freight layers before offtake prices adjust upward.

Regional Price Uncertainty and Demand Disruption for Coconut Oil: Conflict-driven cost escalation has undermined the planning assumptions that European oleochemical converters and Asia-Pacific personal care manufacturers built into 2026 procurement budgets. Reliant on lauric feedstock at stable delivered costs, these buyers might delay volume commitments as freight rate uncertainty persists. Whether import demand recovers in the second half of 2026 will depend on how quickly conflict conditions stabilize and trade route economics normalize.

Immediate Market Reaction:

Procurement decisions across the coconut oil supply chain are under rapid reassessment. Conflict-driven freight escalation is reshaping cost assumptions for trade flows between Southeast Asian origins and European and Indian processors, placing the coconut oil price index under heightened scrutiny at each new booking cycle. Philippine, Indonesian, and Sri Lankan exporters might face indirect cost exposure if war-risk surcharges and vessel diversions raise the CIF premium without corresponding support from offtake pricing. For European converters on just-in-time replenishment schedules, CIF transmission risk is the most direct and immediate exposure.

Impact on Coconut Oil Prices:

The conflict might trigger several key changes in the coconut oil market:

- Energy Input Cost Escalation: High crude oil prices increase fuel and thermal energy costs across three consecutive processing stages, from copra drying through crushing and refining operations, creating a cost structure that cannot be readily absorbed without corresponding offtake price adjustments. Processors in import-dependent markets, such as India and the Netherlands, carry the sharpest exposure, as personal care and food sector clients typically resist rapid spot price pass-through, compressing refiner margins over the near term.

- Freight and Logistics Premium Widening: War-risk insurance surcharges and tanker shortage premiums are embedded in ocean freight costs across every coconut oil trade lane, adding cost layers at Philippine, Indonesian, and Sri Lankan loading ports that transmit directly into CIF quotations for European and Indian importers. Procurement teams holding fixed-price contracts with coconut oil suppliers might face forced spot market exposure at elevated premiums if vessels are diverted, delayed, or repriced as conflict conditions sustain tanker operator caution.

- Demand-Side Uncertainty in Downstream Sectors: For oleochemical manufacturers and personal care companies that depend on coconut oil as a primary lauric feedstock, conflict-driven energy and freight volatility make multi-quarter input budget forecasting unreliable, raising the risk of procurement undercommitment precisely when supply tightens. Demand signals from Europe, India, and Southeast Asia will remain ambiguous until conflict conditions stabilize, and buying activity across FMCG and specialty fat segments will not recover until freight cost trajectories become predictable again.

Taken together, these pressures will keep coconut oil pricing unsettled throughout the conflict period. Energy cost escalation might compress processor margins as freight premiums widen CIF import prices across all origin markets, while demand uncertainty in oleochemical and FMCG segments will dampen spot market liquidity. Price stabilization depends entirely on how quickly freight conditions normalize after the conflict recedes.

Supply Chain Disruptions:

Coconut oil export corridors linking the Philippines, Indonesia, and Sri Lanka to European and Indian importers traverse routes disrupted by conflict-driven carrier suspensions, war-risk surcharges, and vessel diversions that inflate CIF costs at every booking cycle. As of March 26, 2026, approximately 1,900 commercial ships were trapped in the Strait of Hormuz, mainly in the Persian Gulf, since the onset of US and Israeli strikes on Iran, a disruption that extends delivery timelines for coconut oil cargoes on Gulf-adjacent routes and removes the freight cost certainty that just-in-time import schedules require.

Cape of Good Hope rerouting has become the default fallback for coconut oil exporters as direct Hormuz transits remain suspended, adding roughly two weeks to voyage times and raising per-unit freight costs across Philippine, Indonesian, and Sri Lankan origin markets in the process. Logistics managers at key export origins are actively repositioning vessel schedules to reduce dependence on Gulf-adjacent routing corridors. Importers on tight replenishment cycles might require precautionary buffer inventory to sustain production continuity through Q2 2026, and cost escalation will persist for as long as conflict conditions restrict direct transit access.

Global Market Overview:

Globally, the coconut oil industry was valued at USD 7.0 Billion in 2025. Market projections indicate steady growth, with the industry expected to reach USD 11.9 Billion by 2034, with a compound annual growth rate (CAGR) of 5.96% during 2026-2034. Demand from food processing, oleochemical manufacturing, and personal care applications underpins this expansion as clean-label preferences and biofuel adoption widen the lauric feedstock base. The coconut oil price trend reflects durable demand from FMCG segments, reinforced by favorable cosmetics regulations and rising health-positioning across natural fat categories.

Recent Highlights & Strategic Developments:

Recent strategic moves within the industry further illustrate evolving dynamics:

- In March 2026, the Center for Sustainable Polymers at MSU-IIT in Iligan City, Philippines, developed Cocopolyol, a polyol derived from crude coconut oil, offering a renewable alternative to traditional petroleum-based polyurethane materials.

- In January 2025, ICAR-KVK CIARI Nicobar initiated a training program in Tapoiming Village to enable self-help groups to generate income through agriculture. The program aimed to enhance SHGs and FPOs to boost market access and pricing for small-scale farmers. Authorities emphasized the importance of adding value to coconuts, particularly through virgin coconut oil labeled under the NicoShe brand, as a significant opportunity to improve earnings and create sustainable livelihoods in the Nicobar district.

Coconut Oil Price Forecast (2026):

Conflict-driven energy and freight cost escalation will sustain direct upward input pressure on coconut oil import prices through mid-2026, keeping procurement caution elevated among European converters, Asian oleochemical buyers, and personal care manufacturers who cannot easily absorb rapid cost pass-through from origin markets. Any de-escalation might open a window for freight normalization.

If hostilities intensify, coconut oil prices will face renewed upward pressure as tanker freight costs climb further and crude oil-linked processing inputs compound across refinery operations in India and the Netherlands, markets most exposed to CIF cost transmission. A diplomatic resolution changes the trajectory entirely, as freight rates might retreat and copra supply corridors normalize, allowing coconut oil prices to trend toward pre-conflict levels by late 2026, which anchors the coconut oil price forecast for the year ahead.

Strategic Takeaways:

Looking ahead, the coconut oil market is expected to sustain its long-term growth trajectory as lauric feedstock demand from the personal care, oleochemical, and food processing sectors continues to expand across emerging and developed markets alike. Near-term geopolitical and freight volatility will require active risk management by all procurement, logistics, and trading stakeholders.

To navigate this complex landscape, stakeholders should:

- Monitor Regional Price Differentials: Track QoQ pricing variations across Philippine, Indonesian, and Sri Lankan origins to identify cost-saving procurement windows. Benchmarking landed CIF costs against prevailing contract rates at each quarterly update will expose differential opportunities before competitors capture them.

- Track Upstream Copra Market Conditions: Monitor copra harvest cycles, weather patterns, and farm-gate pricing trends across South Indian and Southeast Asian producing regions to anticipate supply-side cost movements. Early-warning visibility into copra price swings gives procurement teams lead time to adjust forward coverage before spot markets tighten.

- Monitor Geopolitical Risk Exposure: Track escalation dynamics in the current conflict and assess how shifts in hostility levels might affect coconut oil pricing, feedstock availability, and logistics costs across key trade corridors. Internal alert thresholds linked to freight rate benchmarks will trigger timely procurement or hedging action.

- Diversify Supply Chain Routes: Evaluate alternative sourcing geographies and shipping corridors to reduce concentration risk on conflict-exposed trade lanes. Secondary supplier agreements and contingency freight arrangements will provide critical resilience if primary routing corridors face disruption as geopolitical conditions evolve.

- Adjust Procurement Strategy for Conflict Conditions: Adopt flexible contract structures with price reopener clauses and force majeure provisions to protect against geopolitical price spikes in coconut oil procurement. Precautionary inventory buffers might reduce exposure to abrupt supply tightening if primary origin market disruptions intensify.

- Benchmark Against Regional FOB Indices: Track the coconut oil price per MT across Philippine, Indonesian, and Sri Lankan FOB benchmarks each quarter to identify cost-effective procurement windows and validate contract pricing. Consistent benchmarking helps procurement teams avoid elevated exposure during periods of active freight cost escalation.

Subscription Plans & Customization:

IMARC offers flexible subscription models to suit varying needs:

- Monthly Updates — 12 deliverables/year

- Quarterly Updates — 4 deliverables/year

- Biannual Updates — 2 deliverables/year

Each includes detailed datasets (Excel + PDF) and post-report analyst support.

.webp)

.webp)

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)