Next Generation Memory Market Report by Technology (Non-Volatile, Volatile), Wafer Size (200 mm, 300 mm, 450 mm), Storage Type (Mass Storage, Embedded Storage, and Others), Interface Type (PCIe and I2C, SATA, SAS, DDR), Application (BFSI, Consumer Electronics, Government, Telecommunications, Information Technology, and Others), Region and Competitive Landscape (Market Share, Business Overview, Products Offered, Business Strategies, SWOT Analysis and Major News and Events) 2026-2034

Next Generation Memory Market Size:

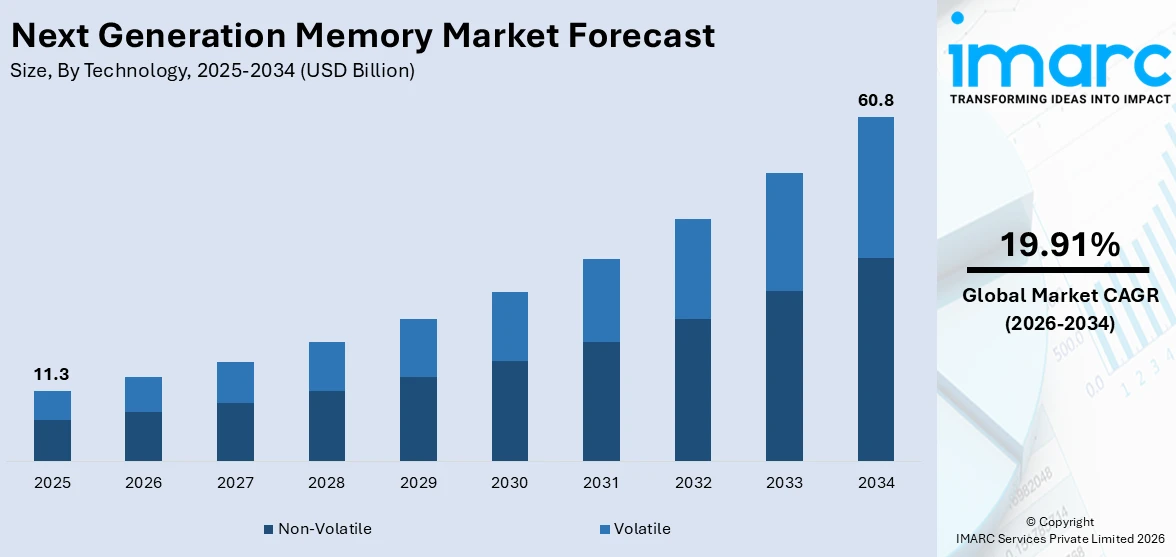

The next generation memory market size reached USD 11.3 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 60.8 Billion by 2034, exhibiting a growth rate (CAGR) of 19.91% during 2026-2034. The rising demand for non-volatile memory (NVM), emergence of the Internet of Things (IoT) devices and edge computing, and increasing number of data centers that generate high amounts of data are bolstering the growth of the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 11.3 Billion |

| Market Forecast in 2034 | USD 60.8 Billion |

| Market Growth Rate (2026-2034) | 19.91% |

Next Generation Memory Market Analysis:

- Major Market Drivers: The demand for non-volatile memory (NVM) is rising. This, along with the expanding data centers, is supporting the market growth.

- Key Market Trends: There is a rise in the need for high-capacity storage solutions for catering to the needs of various sectors.

- Geographical Trends: North America enjoys the leading position in the market share, which can be attributed to its highly developed (IT) infrastructure and the presence of key manufacturers. Besides this, favorable government initiatives in the Asia Pacific region are making it the fastest evolving market.

- Competitive Landscape: Some of the major market players in the next generation memory industry are Avalanche Technology, Crossbar Inc., Fujitsu Limited, Honeywell International Inc., Infineon Technologies AG, Intel Corporation, Micron Technology Inc., Nantero Inc., Samsung Electronics Co. Ltd., SK hynix Inc., Spin Memory Inc., Taiwan Semiconductor Manufacturing Co. Ltd., among many others.

- Challenges and Opportunities: The next generation memory market poses a risk, as next generation memory has a complex manufacturing process. Conversely, it offers various opportunities, such as expanding applications in the automotive and aerospace industries.

To get more information on this market Request Sample

Next Generation Memory Market Drivers:

Rising Demand for Non-Volatile Memory (NVM)

There is an increase in the need for high-performance, reliable, and scalable storage solutions due to expanding data centers. The rising utilization of smartphones, tablets, laptops, and wearables is catalyzing the demand for NVM. Besides this, NVM is widely employed in automotive applications for retaining crucial databases and information. Features like infotainment systems, navigation, driver assistance, and autonomous driving in vehicles require high-storage solutions for enhanced reliability and safety of passengers. People are increasingly adopting vehicles with superior functionalities due to their changing lifestyles. According to the International Organization of Motor Vehicle Manufacturers (OICA), there were about 92,724,668 vehicles sold in 2023 across the globe.

Emergence of the IoT and Edge Computing

The total number of cellular IoT connections was around 3 billion in 2023, as stated by Ericsson. The growing adoption of next generation memory due to the rising utilization of IoT devices and edge computing is offering a positive market outlook. Next generation memory provides high data storing capacity and low power consumption for numerous IoT devices. It also offers superior performance, reliability, and security, to ensure that data storage needs are not only met but also exceeded in the dynamic landscape of IoT devices.

Growing Data Center Market

The United States International Trade Commission claims that there were approximately 8,000 data centers around the world as of January 2021. The escalating demand for next generation memory solutions on account of the rising number of data centers across the globe is propelling the growth of the market. Data centers need high-performance and reliable memory solutions to handle the massive volumes of data generated by modern applications. Next-generation memory technologies provide faster access times and higher throughput than dynamic random access memory (DRAM) and NAND flash, which are traditional memory solutions. Furthermore, there is an increase in the need for scalable memory storage solutions to meet the requirements of data-intensive workloads in data centers.

Next Generation Memory Market Opportunities:

Expanding Applications in Automotive and Aerospace

There is a rise in the adoption of next generation memory within the automotive and aerospace sectors. In the automotive sector, these storage solutions are integrated due to the addition of infotainment and navigation systems. Similarly, these storage solutions are incorporated in aerospace systems, including satellites, aircraft, and spacecraft, for the purpose of storing and processing large quantities of data. The U.S. Air Force Research Laboratory Space Vehicles Directorate announced a US$ 35 million contract to Western Digital for the development of advanced next generation strategic radiation hardened memory (ANGSTRM) project on 14 November 2023. They are hard non-volatile memory chips that are engineered to endure the natural radiation found in space.

Rising Demand for High-Capacity Storage Solutions

There is an increase in the need for high-capacity storage solutions in various sectors, such as media and entertainment and healthcare. The rising demand for next generation memory solutions due to growing digital content, including movies, television shows, games, and virtual reality (VR) experiences. Besides this, high-capacity storage solutions play a crucial role in medical imaging and electronic health records (EHRs) for storing patient data accurately and efficiently. They also facilitate personalized treatment plans and contribute to improved patient satisfaction. Improving healthcare infrastructure necessitates high-capacity storage solutions. For instance, the United States was home to approximately 6,120 hospitals in 2022.

Key Technological Trends and Development:

Memristor-based Memories and Spin-Transfer Torque RAM (STT-RAM)

Memristor-based memories are engineered as a high-density crossbar architecture. Memristor devices are located at each intersection between two bars. Usually memristor-based memories do not use transistors for cell gating. Memristor-based memories have a retainable memory and a very high density as compared to other storage systems. On the other hand, spin transfer torque random access memory RAM (STT-RAM) is a new memory technology that combines the capacity and cost benefits of DRAM, the fast read and write performance of SRAM, and the non-volatility of flash memory with essentially unlimited endurance.

Micross Components, Inc., recently expanded its magnetoresistive random access memory (MRAM) product offering with the addition of a Ceramic Column Grid Array (CCGA) package. The portfolio includes 1Gb (32M x 32) & 4Gb (128M x 32) Parallel Spin-Torque MRAM product variants that are based on the technology partners 22nm Gen-3 pMTJ STT-MRAM process node topology.

Three-Dimensional (3D) Stacking

3D stacking, also known as 3D integration, is a semiconductor manufacturing technique that involves the vertical stacking of different chips or wafers together into a single package without changing the size of the original package. It allows for increased functionality, performance, and density in electronic devices. Moreover, the rising utilization of 3D stacking for microsystem integration is contributing to the market growth.

Next Generation Memory Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on technology, wafer size, storage type, interface type, and application.

Breakup by Technology:

- Non-Volatile

- Magneto-Resistive Random-Access Memory (MRAM)

- Ferroelectric RAM (FRAM)

- Resistive Random-Access Memory (ReRAM)

- 3D Xpoint

- Nano RAM

- Other Non-Volatile Technologies (Phase change RAM, STT-RAM, and SRAM)

- Volatile

- Hybrid Memory Cube (HMC)

- High-Bandwidth Memory (HBM)

Non-volatile accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the technology. This includes non-volatile [magneto-resistive random-access memory (MRAM), ferroelectric RAM (FRAM), resistive random-access memory (ReRAM), 3D Xpoint, nano RAM, and other non-volatile technologies (phase change RAM, STT-RAM, and SRAM)] and volatile [hybrid memory cube (HMC) and high-bandwidth memory (HBM)]. According to the report, non-volatile represented the largest segment.

Non-volatile is a semiconductor technology that does not need a continuous power supply to retain the data that is stored in a computing device. It preserves data integrity over extended periods without requiring a continuous power supply. It can hold the instructions first executed when the computer is turned on. It is widely utilized in the telecommunications, automotive, healthcare, and retail industries. On 25 August 2022, Samsung Electronics Co., Ltd. announced the 990 PRO, high-performance non-volatile memory (NVMe) SSD based on PCIe 4.0. It offers superior power efficiency in graphically demanding games and other intensive tasks, including three-dimensional (3D) rendering and 4K video editing.

Breakup by Wafer Size:

- 200 mm

- 300 mm

- 450 mm

300 mm holds the largest share of the industry

A detailed breakup and analysis of the market based on the wafer size have also been provided in the report. This includes 200 mm, 300 mm, and 450 mm. According to the report, 300 mm accounted for the largest market share.

300 mm wafer size provides about twice the usable die area as compared to 200mm wafers. It is manufactured from silicon and serves as the substrate on which multiple integrated circuits (ICs) are fabricated simultaneously. It has a lower cost per die and supports leading edge processes below 10nm. It assists in providing enhanced productivity and efficiency. Furthermore, key players in the market are increasingly producing these wafers by forming partnerships. For instance, Texas Instruments Incorporated (TI) signed an agreement to acquire the 300-mm semiconductor factory of Micron Technology in Lehi, Utah, for around US$ 900 million on 30 June 2021.

Breakup by Storage Type:

- Mass Storage

- Embedded Storage

- Others

Mass storage represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the storage type. This includes mass storage, embedded storage, and others. According to the report, mass storage represented the largest segment.

Mass storage is used to store a large amount of data and retains memory even when the computer is turned off, unlike main memory. It comprises solid-state drivers (SSD), hard drives, external hard drives, tape drives, universal serial bus (USB) storage, and flash memory cards. It is capable of handling terabytes (TB) and petabytes (PB) of data. It offers reliable and scalable storage solutions to meet the needs of organizations and individuals. On 16 September 2023, Seagate Technology announced its mass storage system ‘Exos CORVAULT 5U84’ at the International Broadcasting Convention (IBC) 2023. The product benefits media and entertainment organizations by reducing their carbon emissions and operating costs by keeping drives in service for a longer time.

Breakup by Interface Type:

- PCIe and I2C

- SATA

- SAS

- DDR

A detailed breakup and analysis of the market based on the interface type have also been provided in the report. This includes PCIe and I2C, SATA, SAS, and DDR.

Peripheral component interconnect express (PCIe) and I2C are interface types that are used in next generation memory devices. PCIe is a high-speed interface standard used for connecting various internal components in a computer system. It is essential for connecting expansion cards, such as graphics cards, network cards, and storage controllers, to the motherboard. In addition, I2C uses an open-drain or open-collector with an input buffer on the same line and allows a single data line to be used for bidirectional data flow.

SATA is a hard drive interface type that is used to read and write data to and from storage. It has a low voltage requirement and a high rate of data transfer. It is usually smaller in size and takes up less space inside a computer while increasing the airflow. It operates on 0.5V peak-to-peak signaling and helps a user promote much lower crosstalk and interference between the conductors.

SAS drives generally offer higher performance and faster data transfer rates as compared to SATA drives, which makes it a preferred choice for high-demand applications and environments that require quick access to data. SAS interfaces are backward compatible with SATA drives, meaning that SATA drives can be connected to SAS ports. They allow for greater flexibility and scalability, making them ideal for complex storage setups.

DDR is used in computers and other electronic devices to increase performance. It works by transferring data on both the rising and falling edges of the clock signal. This effectively doubles the data transfer rate as compared to earlier memory technologies that only transferred data on one edge of the clock signal. It has faster data transfer rates, improved system performance, and better multitasking capabilities.

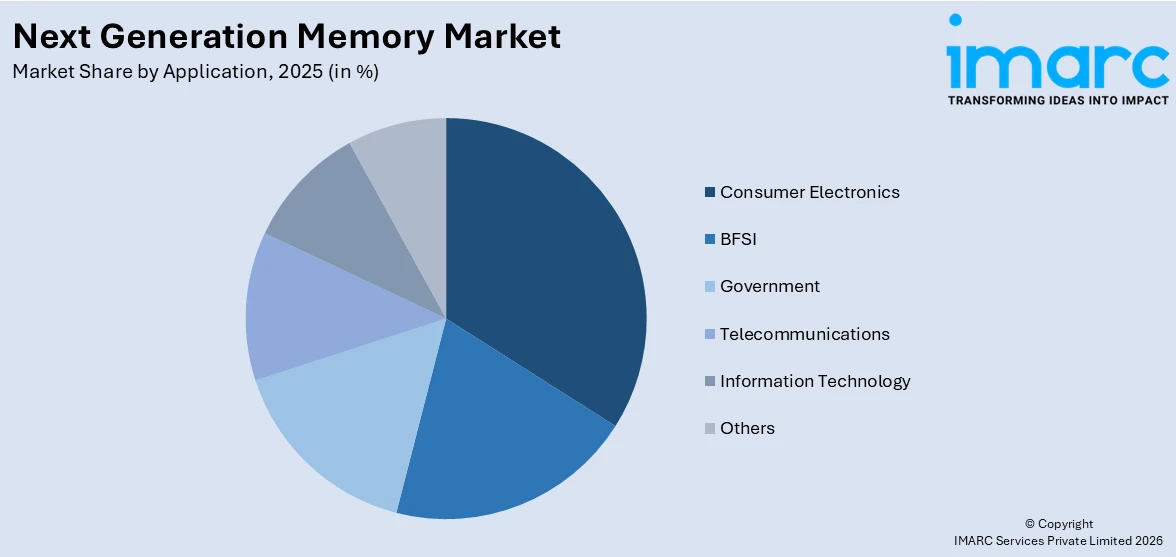

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- BFSI

- Consumer Electronics

- Government

- Telecommunications

- Information Technology

- Others

Consumer electronics dominate the market

The report has provided a detailed breakup and analysis of the market based on the application. This includes BFSI, consumer electronics, government, telecommunications, information technology, and others. According to the report, consumer electronics represented the largest segment.

The escalating demand for next generation memory due to the rising adoption of consumer electronics, such as smartphones, laptops, computers, gaming consoles, and wearables, is supporting the market growth. Consumer electronics require storage solutions to store diverse kinds of data and content. Besides this, there is a rise in the need for storage solutions in digital cameras. People are increasingly adopting these cameras due to their utilization in recording movies, events, and other celebrations. As per the research report of IMARC Group, the global digital camera market reached US$ 7.9 Billion in 2023.

Regional Insights:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East

- Africa

North America leads the market, accounting for the largest next generation memory market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); Middle East, and Africa. According to the report, North America represents the largest regional market for next generation memory.

North America has a highly developed (IT) infrastructure, along with the presence of key manufacturers. Moreover, the growing demand for next-generation memory due to the high data generation across diverse sectors in the region is positively influencing the market. Apart from this, key players in the region are investing in IT infrastructure to broaden their market presence. For example, Vantage Data Centers, a leading global provider of hyperscale data center campuses, announced the investment of an additional CAD$ 900 million to scale its Canadian operations on 17 March 2022.

Analysis Covered Across Each Country:

- Historical, current, and future market performance

- Historical, current, and future performance of the market based on technology, wafer size, storage type, interface type, and application.

- Competitive landscape

- Government regulations

Competitive Landscape:

- The market research report has provided a comprehensive analysis of the competitive landscape covering market structure, market share by key players, market player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant, among others. Detailed profiles of all major companies have also been provided. This includes business overview, product offerings, business strategies, SWOT analysis, financials, and major news and events. Some of the major market players in the next generation memory industry include Avalanche Technology, Crossbar Inc., Fujitsu Limited, Honeywell International Inc., Infineon Technologies AG, Intel Corporation, Micron Technology Inc., Nantero Inc., Samsung Electronics Co. Ltd., SK hynix Inc., Spin Memory Inc., and Taiwan Semiconductor Manufacturing Co. Ltd.

- Key manufacturers in the market are introducing high-performance storage solutions to cater to the needs of diverse industries and enhance user satisfaction. They are also expanding their manufacturing facilities to increase the production of next generation memory storage solutions. In line with this, major players are heavily investing in next generation memory solutions due to favorable government initiatives. On 18 May 2023, Micron Technology invested up to US$ 3.6 billion in Japan for next-generation memory chips with support from the Japanese government.

Analysis Covered for Each Player:

- Market Share

- Business Overview

- Products Offered

- Business Strategies

- SWOT Analysis

- Major News and Events

Next Generation Memory Market News:

- 9 May 2022: Western Digital Corp. introduced the Western Digital® PC SN740 non-volatile memory (NVMe) SSD to address the unique needs of the hybrid workforce and enhance the computing experience.

- 19 July 2023: Samsung Electronics completed the development of the industry’s first graphics double data rate 7 (GDDR7) DRAM. It is expected to be first installed in next-generation systems of key customers for verification this year.

- 22 August 2023: SK hynix developed the 5th generation DRAM product ‘HBM3E’, which is tailored for high-performance artificial intelligence (AI) applications. HBM is a high-value and high-performance chip that benefits in enhancing data processing speed by vertically connecting multiple DRAMs.

Next Generation Memory Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered |

|

| Wafer Sizes Covered | 200 mm, 300 mm, 450 mm |

| Storage Types Covered | Mass Storage, Embedded Storage, Others |

| Interface Types Covered | PCIe and I2C, SATA, SAS, DDR |

| Applications Covered | BFSI, Consumer Electronics, Government, Telecommunications, Information Technology, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East, and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Avalanche Technology, Crossbar Inc., Fujitsu Limited, Honeywell International Inc., Infineon Technologies AG, Intel Corporation, Micron Technology Inc., Nantero Inc., Samsung Electronics Co. Ltd., SK hynix Inc., Spin Memory Inc., Taiwan Semiconductor Manufacturing Co. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global next generation memory market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global next generation memory market?

- What is the impact of each driver, restraint, and opportunity on the global next generation memory market?

- What are the key regional markets?

- Which countries represent the most attractive next generation memory market?

- What is the breakup of the market based on the technology?

- Which is the most attractive technology in the next generation memory market?

- What is the breakup of the market based on the wafer size?

- Which is the most attractive wafer size in the next generation memory market?

- What is the breakup of the market based on the storage type?

- Which is the most attractive storage type in the next generation memory market?

- What is the breakup of the market based on the interface type?

- Which is the most attractive interface type in the next generation memory market?

- What is the breakup of the market based on the application?

- Which is the most attractive application in the next generation memory market?

- What is the competitive structure of the market?

- Who are the key players/companies in the global next generation memory market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the next generation memory market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global next generation memory market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the next generation memory industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)