Non-GMO Food Market Size, Share, Trends and Forecast by Product Type, Application, Distribution Channel, and Region, 2026-2034

Non-GMO Food Market Size and Share:

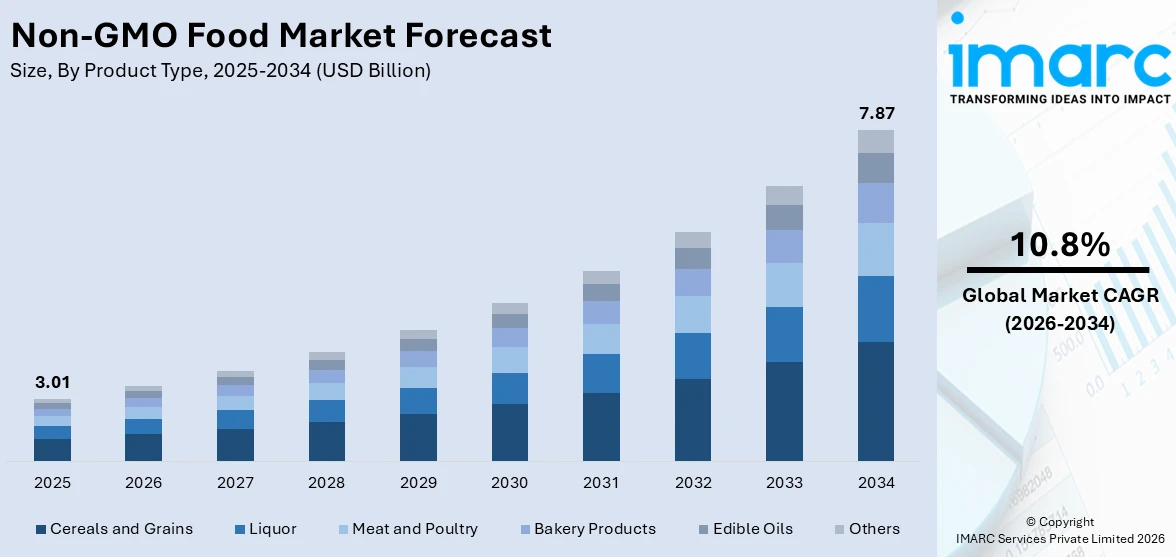

The global non-GMO food market size was valued at USD 3.01 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 7.87 Billion by 2034, exhibiting a CAGR of 10.8% from 2026-2034. North America currently dominates the market, holding a market share of 37.9% in 2025. The region benefits from advanced regulatory frameworks supporting bioengineered food disclosure, strong consumer preference for clean-label and transparent products, extensive retail distribution networks, and a well-established certification ecosystem led by the Non-GMO Project, all contributing to the non-GMO food market share.

Growing public awareness of the possible health dangers connected with genetically modified organisms has led to a major movement toward natural and organic food items, which in turn is driving the worldwide non-GMO food market. Customers are prioritizing products with cleaner and simpler ingredient lists due to the growing incidence of food allergies and sensitivities; non-GMO labeling is a reliable indicator of safety and transparency in this regard. Furthermore, consumers' demand for non-GMO food products is being strengthened by the increased focus on environmentally friendly and sustainable farming methods. The growth of health-conscious grocery stores and e-commerce platforms is making non-GMO products more accessible and available to a wider range of customer groups. Furthermore, the growing popularity of plant-based diets and the convergence of non-GMO certification with organic and clean-label characteristics are generating synergistic demand, which is boosting the expansion of the non-GMO food industry worldwide.

For a variety of reasons, the US has become a significant market for non-GMO foods. The demand for verified non-GMO food items is rising dramatically across retail and foodservice channels due to American consumers' increased health consciousness and growing mistrust of genetically modified organisms. The USDA's National Bioengineered Food Disclosure Standard, which went into full effect in June 2025 and mandates that importers and producers identify bioengineered ingredients, has increased consumer confidence and market openness. Nationwide, consumers now have more access to non-GMO products thanks to the growth of organic grocery chains, specialist natural food stores, and internet marketplaces. Furthermore, the non-GMO food market outlook in the US is being driven by growing disposable incomes and changing lifestyle preferences that favor clean-label, minimally processed, and chemical-free food options. This is supporting sustained demand across cereals, beverages, dairy substitutes, and packaged food categories.

To get more information on this market Request Sample

Non-GMO Food Market Trends:

Escalating Clean-Label Consumer Preferences

The global non-GMO food market is being driven by the growing customer preference for clean-label products. Transparency in food sourcing, production processes, and ingredient composition is becoming more and more important to consumers, which is forcing businesses to restructure their product lines to meet these demands. The clean-label movement encompasses larger characteristics including minimal processing, lack of artificial additives, and sustainable sourcing methods in addition to the absence of genetically modified components. In order to achieve a full clean-label positioning and help firms gain the trust and loyalty of consumers, non-GMO certification has become a crucial component. The number of certified product formulae available across retail channels is significantly increasing due to customer demand for verified non-GMO products, demonstrating the market's strong commitment to clear food labeling. The market's selection of confirmed non-GMO products is growing as a result of this consumer-driven shift, which is pushing food companies from all market categories to incorporate non-GMO sourcing into their product development plans. The momentum of clean-label adoption among various consumer demographics worldwide is being further reinforced by the convergence of non-GMO certification with broader wellness and sustainability values.

Growth of Plant-Based Non-GMO Products

The non-GMO food market forecast has significant development potential due to the growing acceptance of plant-based non-GMO proteins. In order to make the dual claims of being plant-based and non-GMO, manufacturers are increasingly concentrating on identity-preserved proteins made from soy, pea, and chickpea sources. This strategic positioning enables businesses to command premium price points and increase profit margins while appealing to health-conscious consumers. Regulatory advancements are further supporting this trend, as in June 2025 the United States Food and Drug Administration issued draft guidance on labeling standards for plant-based alternatives, reducing consumer confusion and fostering greater trust in these products. Plant-based nutrition, non-GMO certification, and allergen-free formulations are coming together to draw in a wider range of customers, including those with food sensitivities and dietary constraints. Additionally, the growing availability of non-GMO plant-based beverages, dairy alternatives, and protein-enriched snacks through mainstream retail channels is reinforcing the segment trajectory.

Strengthening Regulatory and Certification Frameworks

Consumer confidence is being bolstered and non-GMO food market trends are being driven by the global development of regulatory frameworks and certification programs. To improve the openness of the food supply chain, governments and regulatory agencies are enforcing obligatory disclosure laws and encouraging voluntary certification initiatives. A complete trust infrastructure that benefits both consumers and businesses is being created by the confluence of industry-led certification initiatives and government regulations. Ten European nations, including Germany, France, Austria, and Slovenia, have enacted clear non-GMO labeling laws, and voluntary initiatives result in billions of dollars' worth of yearly consumer expenditure on confirmed non-GMO goods. Additionally, in order to lower trade obstacles and consumer misunderstanding, harmonization initiatives are being carried out by groups like Donau Soja to unify non-GMO standards throughout European markets. In the end, these legal changes are increasing the availability and legitimacy of non-GMO food items worldwide by encouraging food producers to make investments in non-GMO sourcing, verification, and supply chain traceability.

Non-GMO Food Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global non-GMO food market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product type, application, and distribution channel.

Analysis by Product Type:

- Cereals and Grains

- Liquor

- Meat and Poultry

- Bakery Products

- Edible Oils

- Others

Cereals and grains hold 32.7% of the market share. Because of their adaptability to a variety of food uses, such as morning cereals, bakery goods, snacks, and animal feed formulations, cereals and grains form the basis of the non-GMO food sector. Because consumers prefer whole grain products as their main source of nutritional fiber, vital minerals, and complex carbs, there is a particularly significant demand for non-GMO cereals and grains. Verified non-GMO cereals are becoming more and more popular as customers around the world become more health conscious and aware of the possible dangers of genetically engineered grain kinds. A wider dietary movement toward transparent and naturally sourced grain-based products is seen in the persistent customer preference for snacks and food items branded as organic or non-GMO. Additionally, steady category expansion is being supported by the growing retail availability of non-GMO certified grain-based products through supermarkets, specialist health stores, and e-commerce platforms. The segment's standing within the overall market landscape is being further strengthened by food makers' increasing use of non-GMO grains for usage in reformulated product lines.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

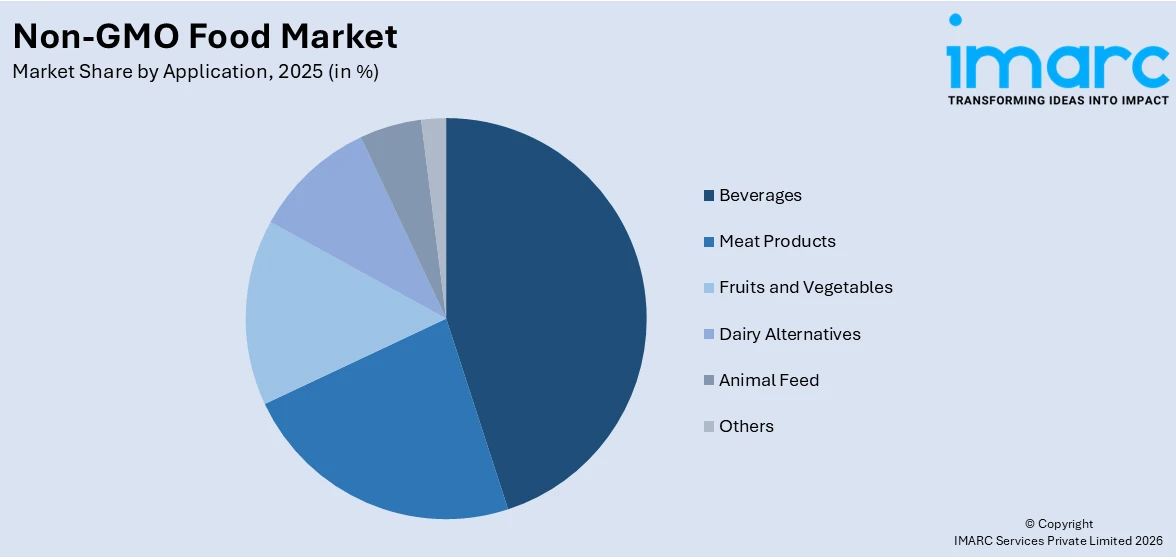

- Beverages

- Meat Products

- Fruits and Vegetables

- Dairy Alternatives

- Animal Feed

- Others

Beverages leads the market with a share of 45.5%. The beverages segment dominates the non-GMO food market, supported by the growing consumer demand for natural, clean-label, and health-enhancing drink products. Non-GMO labeling significantly enhances the perceived purity and health benefits of beverages including fruit juices, plant-based milks, functional drinks, and organic teas, driving strong consumer preference across retail and foodservice channels. The proliferation of non-GMO verified plant-based beverages, particularly oat milk, almond milk, and soy-based drinks, is expanding the application scope of non-GMO certification within this segment. For instance, in March 2025, SunOpta launched its Non-GMO Project Certified SOWN Oat Cold Foaming Cream, available at major retail outlets including Amazon and Sprouts Farmers Market stores across the United States. Globally, the non-GMO drinks application market is experiencing strong demand growth due to growing health consciousness, rising disposable incomes, and changing lifestyle tastes that favor functional and minimally processed beverages.

Analysis by Distribution Channel:

- Food Service

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Stores

- Others

Supermarkets and hypermarkets dominate the market, with a share of 48.6%. Due to their wide product selections, well-established customer trust, and easy shopping experiences, supermarkets and hypermarkets are the main distribution route for non-GMO food products. These retail formats are the main destination for health-conscious consumers looking for confirmed non-GMO solutions since they offer dedicated shelf space for organic, natural, and non-GMO certified items. This distribution channel is being strengthened by the big retail chains' increasing focus on growing their private-label non-GMO product catalogs. For instance, in November 2025, Natural Grocers, the largest family-operated organic and natural grocery retailer in the United States, launched three new Non-GMO Project Verified pickle and relish products crafted without artificial preservatives or synthetic colors. The strategic partnerships between non-GMO food manufacturers and large-format retailers, along with in-store promotional activities and consumer education initiatives, are reinforcing the dominance of supermarkets and hypermarkets.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 37.9% of the share, enjoys the leading position in the market. The region's dominance is attributed to the well-established regulatory infrastructure supporting food transparency, including mandatory bioengineered food disclosure requirements and widely recognized non-GMO verification programs. The heightened health consciousness among North American consumers, coupled with widespread access to verified non-GMO products through extensive retail networks, is sustaining strong market performance. The region benefits from a mature organic and natural food ecosystem, with major retailers dedicating significant shelf space to non-GMO certified product categories. The depth of consumer commitment to verified non-GMO products is evident in the widespread adoption of recognized certification seals across mainstream food and beverage retail channels throughout the region. Additionally, the growing convergence of non-GMO certification with organic, plant-based, and allergen-free product attributes is expanding the addressable consumer base and reinforcing North America's leading position in the global non-GMO food market. The continuous expansion of specialty natural food retailers and online grocery platforms is further broadening access to non-GMO offerings.

Key Regional Takeaways:

United States Non-GMO Food Market Analysis

The United States represents the largest and most dynamic market for non-GMO food products within North America, driven by a confluence of regulatory developments, consumer awareness, and retail expansion. The growing skepticism among American consumers regarding genetically modified organisms has catalyzed a significant shift toward verified non-GMO food products across all major retail and foodservice channels. The full enforcement of mandatory bioengineered food disclosure requirements has enhanced market transparency and empowered consumers to make more informed purchasing decisions. The United States market benefits from a robust certification ecosystem that enables consumers to identify and select verified non-GMO products with confidence. The expansion of natural food retailers, specialty grocery chains, and direct-to-consumer e-commerce platforms is broadening consumer access to non-GMO products across diverse geographic and demographic segments. Furthermore, the increasing corporate commitment to clean-label reformulation, with major food companies investing in non-GMO sourcing and product development, is accelerating the availability of verified non-GMO options across cereals, beverages, dairy alternatives, snacks, and packaged food categories. The rising consumer preference for sustainably produced, transparent, and minimally processed food products continues to underpin robust growth in the United States non-GMO food market.

Europe Non-GMO Food Market Analysis

The European non-GMO food market is expanding steadily, supported by stringent regulatory frameworks, strong consumer preference for food transparency, and well-established voluntary non-GMO labeling programs across multiple member states. The European Union's mandatory labeling requirements for food containing approved genetically modified organisms have created a regulatory environment that inherently supports non-GMO product positioning. Several European countries have established explicit non-GMO labeling regulations, with dedicated industry associations representing numerous member companies and a growing portfolio of labeled non-GMO products across the region. The traditional farming practices prevalent in many European countries, combined with consumer demand for ethically sourced and sustainably produced food items, are reinforcing market expansion. The harmonization of non-GMO standards through regional initiatives is reducing trade barriers and facilitating cross-border product distribution. The growing integration of non-GMO labeling with organic certification is further strengthening consumer trust and market credibility across the European non-GMO food landscape.

Asia-Pacific Non-GMO Food Market Analysis

The Asia-Pacific non-GMO food market is witnessing accelerated growth, driven by rising health consciousness, increasing disposable incomes, and the growing adoption of Western dietary preferences favoring natural and organic food products. The expanding middle-class population across countries including China, Japan, India, South Korea, and Australia is creating substantial demand for clean-label and non-GMO certified food items. The rising purchasing power across major economies in the region is enhancing consumer ability to afford premium non-GMO products. The increasing urbanization across the region, combined with the proliferation of modern retail formats and e-commerce platforms, is improving accessibility to non-GMO food products. Government initiatives promoting organic agriculture and sustainable farming practices are further supporting market development across the Asia-Pacific region.

Latin America Non-GMO Food Market Analysis

The Latin American non-GMO food market is gaining momentum, supported by the growing health awareness among urban populations and increasing consumer interest in sustainable and transparent food products. The region plays a significant role as a supplier of non-GMO raw materials, including cane sugar, tropical fruit concentrates, and soy products, to global manufacturers. The emergence of certified non-GMO supply chains across the region is marking important milestones for the regional infrastructure development. The expanding modern retail networks and growing e-commerce penetration are enhancing consumer access to non-GMO products across major markets including Brazil and Mexico.

Middle East and Africa Non-GMO Food Market Analysis

The Middle East and Africa non-GMO food market is experiencing emerging growth, driven by the increasing adoption of healthy eating trends and the expanding organic food sector across the region. The rising consumer awareness regarding food quality, nutritional value, and production transparency is encouraging demand for non-GMO certified products across both retail and foodservice channels. The growing urbanization and increasing disposable incomes are supporting consumer willingness to purchase premium non-GMO food items. The rising demand for natural, health-oriented, and sustainably sourced food products across key markets in the region is reinforcing consumption patterns. The expansion of international retail chains and specialty health food stores across major urban centers is further facilitating market development.

Competitive Landscape:

The competitive landscape of the non-GMO food market is characterized by the presence of both established multinational food conglomerates and specialized organic and natural food companies, each pursuing strategic initiatives to strengthen their market positioning. Key players are actively expanding their non-GMO product portfolios through new product development, reformulation of existing offerings, and the acquisition of non-GMO certifications to meet evolving consumer expectations. Strategic partnerships between manufacturers, certification bodies, and retail channels are facilitating broader market penetration and enhanced brand visibility. Companies are also investing in sustainable sourcing practices, supply chain traceability systems, and digital marketing campaigns to build consumer trust and differentiate their offerings in an increasingly competitive marketplace. The focus on clean-label innovation, allergen-free formulations, and plant-based non-GMO product lines is intensifying competition across segments.

The report provides a comprehensive analysis of the competitive landscape in the non-GMO food market with detailed profiles of all major companies, including:

- Amy's Kitchen Inc.

- Blue Diamond Growers

- Clif Bar & Company

- Chiquita Brands International Sarl

- The Hain Celestial Group Inc.

- Nature's Path Foods Inc.

- Now Health Group Inc.

- Organic Valley

- Pernod Ricard SA

- United Natural Foods Inc.

Latest News and Developments:

- In October 2025, Ciranda, a leading North American supplier of certified organic and non-GMO food ingredients, announced a new partnership with Incredo at SupplySide Global in Las Vegas. The collaboration enables Ciranda to offer clean-label sugar reduction solutions made from real cane sugar, providing non-GMO and gluten-free options for food and beverage manufacturers.

Non-GMO Food Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Cereals and Grains, Liquor, Meat and Poultry, Bakery Products, Edible Oils, Others |

| Applications Covered | Beverages, Meat Products, Fruits and Vegetables, Dairy Alternatives, Animal Feed, Others |

| Distribution Channels Covered | Food Service, Supermarkets and Hypermarkets, Convenience Stores, Online Stores, Others |

| Region Covered | North America, Asia Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Amy's Kitchen Inc., Blue Diamond Growers, Clif Bar & Company, Chiquita Brands International Sarl, The Hain Celestial Group Inc., Nature's Path Foods Inc., Now Health Group Inc., Organic Valley, Pernod Ricard SA, United Natural Foods Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the non-GMO food market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global non-GMO food market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the non-GMO food industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Non-GMO Food Market Report

The non-GMO food market was valued at USD 3.01 Billion in 2025.

The non-GMO food market is projected to exhibit a CAGR of 10.8% during 2026-2034, reaching a value of USD 7.87 Billion by 2034.

The key factors driving the non-GMO food market include the escalating consumer health consciousness, growing demand for clean-label and transparent food products, strengthening regulatory frameworks mandating bioengineered food disclosure, rising preference for sustainable and organic farming practices, expansion of plant-based non-GMO product categories, and increasing retail availability through supermarkets, specialty stores, and e-commerce platforms.

North America currently dominates the non-GMO food market, accounting for a share of 37.9%. The region benefits from advanced regulatory frameworks, widespread non-GMO certification adoption, strong consumer awareness, and extensive retail infrastructure supporting transparent food product distribution.

Some of the major players in the non-GMO food market include Amy's Kitchen Inc., Blue Diamond Growers, Clif Bar & Company, Chiquita Brands International Sarl, The Hain Celestial Group Inc., Nature's Path Foods Inc., Now Health Group Inc., Organic Valley, Pernod Ricard SA, United Natural Foods Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)