North America Flexible Packaging Market Size, Share, Trends and Forecast by Product Type, Raw Material, Printing Technology, Application, and Country, 2026-2034

North America Flexible Packaging Market Size, Share, Trends & Forecast (2026-2034)

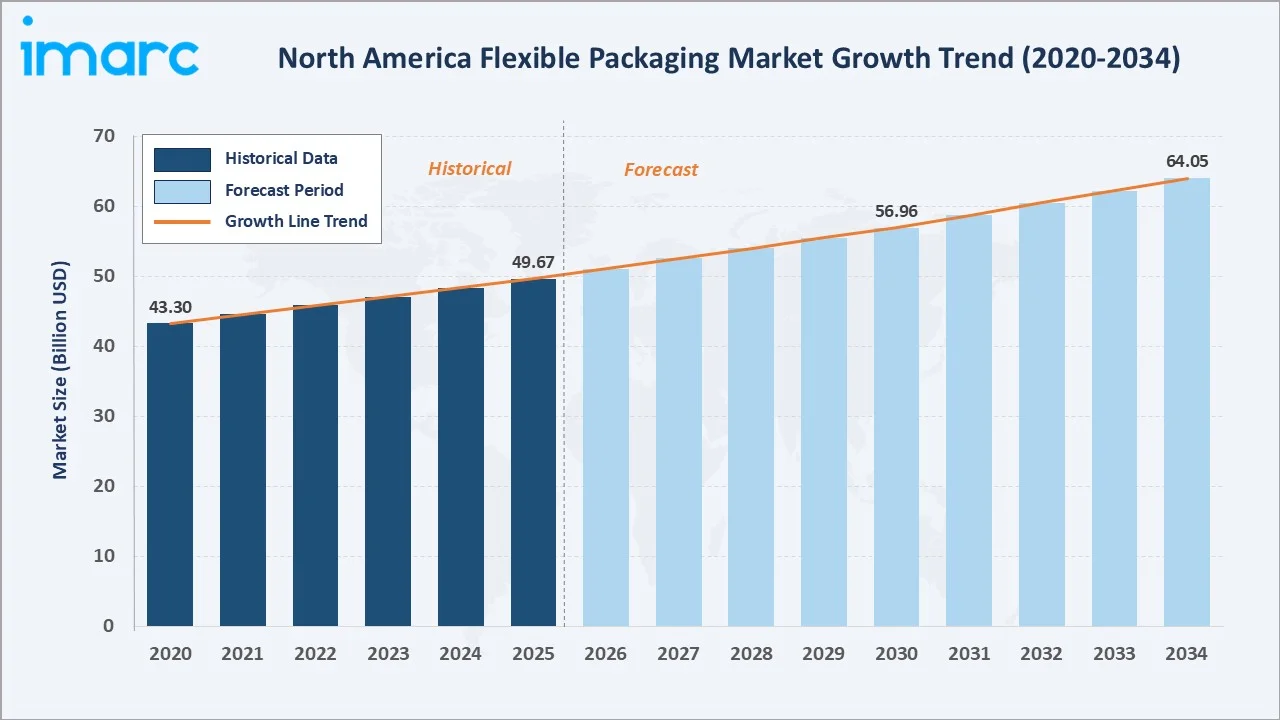

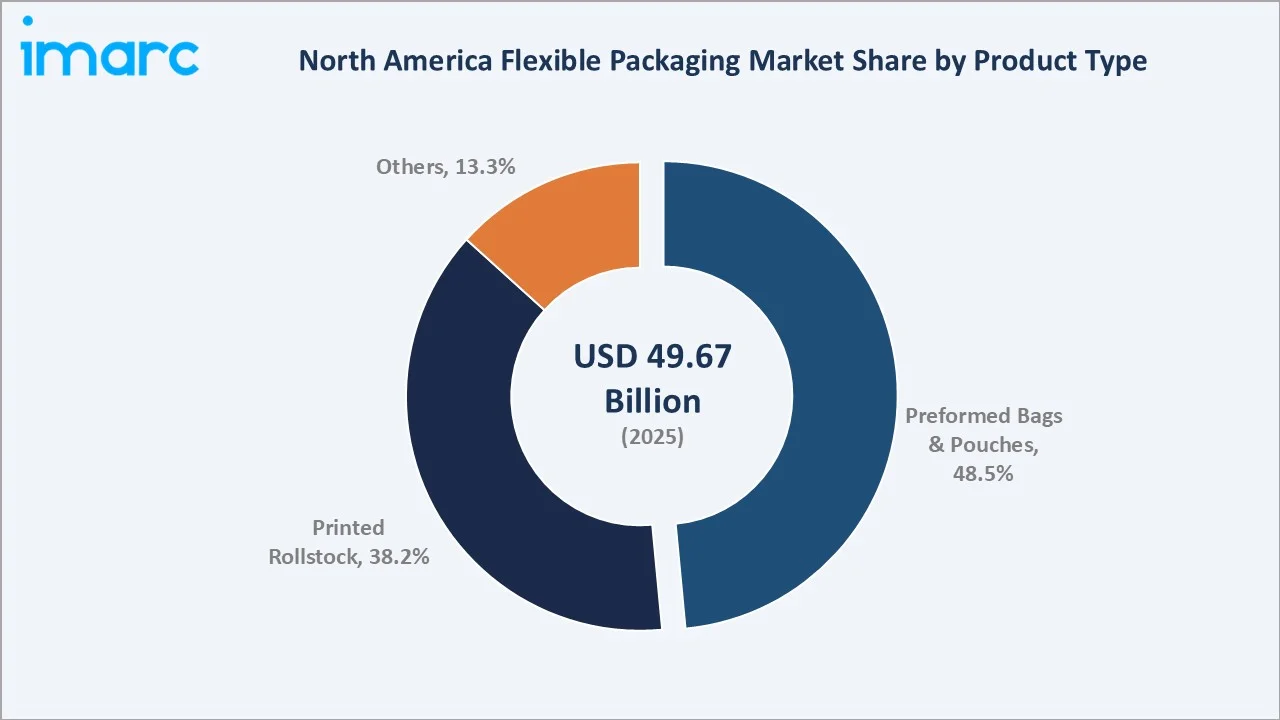

The North America flexible packaging market size reached USD 49.67 Billion in 2025 and is projected to reach USD 64.05 Billion by 2034, exhibiting a CAGR of 2.78% during 2026-2034. Rising consumer preference for lightweight, sustainable packaging, expanding e-commerce, and robust food and beverage sector demand are the primary forces driving market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 49.67 Billion |

|

Forecast Market Size (2034) |

USD 64.05 Billion |

|

CAGR (2026-2034) |

2.78% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Country |

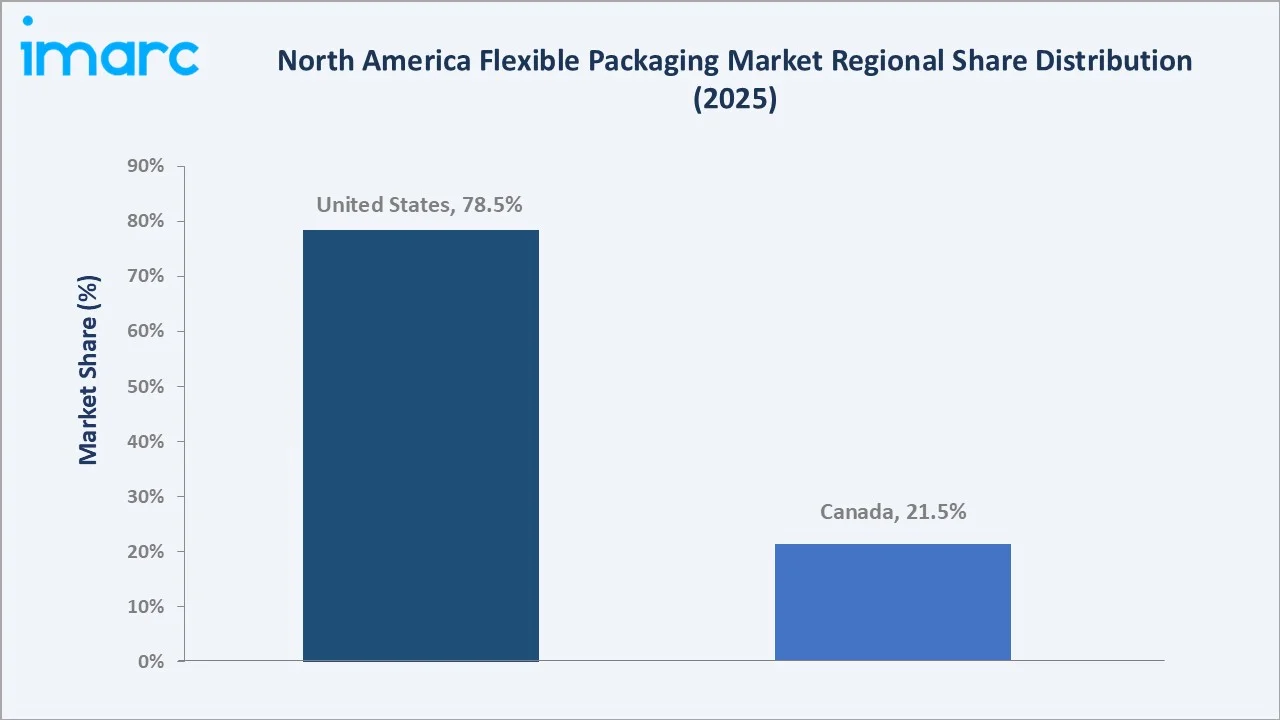

United States (78.5% share, 2025) |

|

Second Country |

Canada (21.5% share, 2025) |

|

Leading Application |

Food and Beverages (52.4%, 2025) |

|

Leading Product Type |

Preformed Bags and Pouches (48.5%, 2025) |

The North America flexible packaging market growth trajectory from 2020 through 2034, with historical expansion to USD 49.67 Billion in 2025, reflects consistent food-safety and convenience-driven demand, while the forecast to USD 64.05 Billion captures accelerating sustainable packaging transitions and pharmaceutical sector expansion.

To get more information on this market, Request Sample

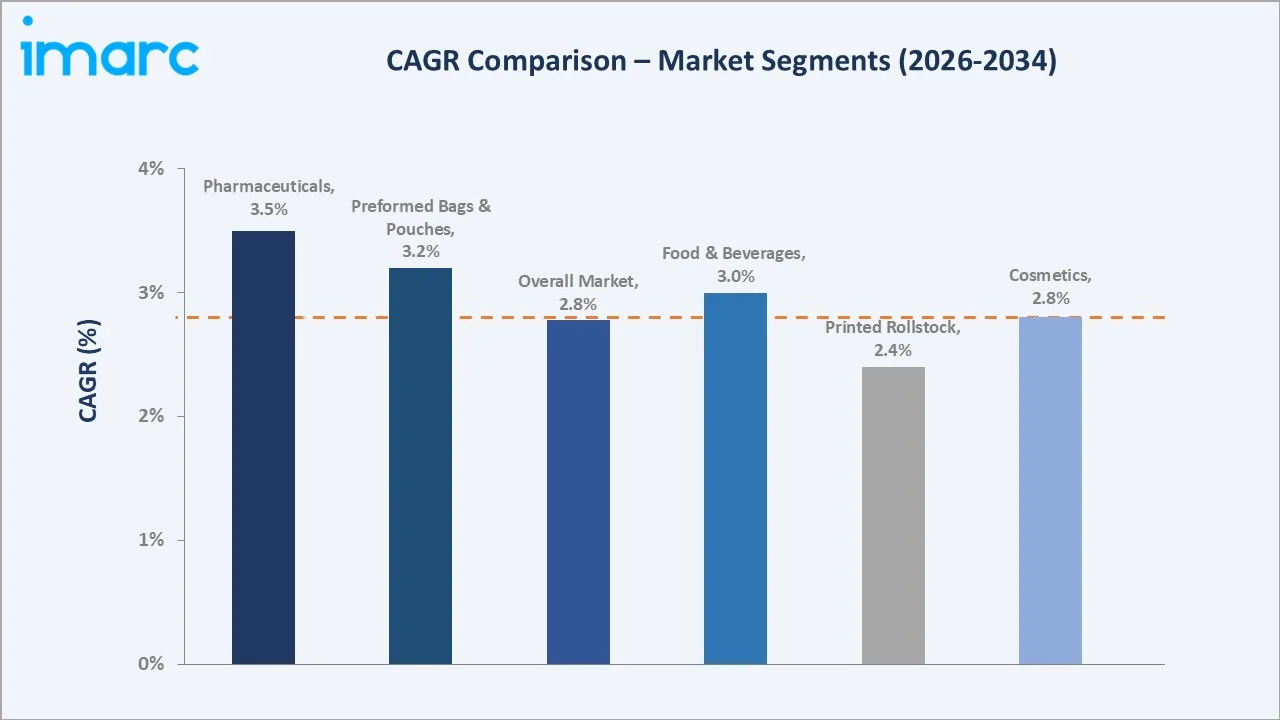

The CAGR trajectories across key application and product segments, with Pharmaceuticals at ~3.5% CAGR and Preformed Bags & Pouches at ~3.2% CAGR, are the fastest-growing sub-categories within the North America flexible packaging industry analysis through 2034.

Executive Summary

The North America flexible packaging market is on a sustained growth trajectory from USD 49.67 Billion in 2025 to USD 64.05 Billion by 2034. Flexible packaging is an essential component across food, beverage, pharmaceutical, and cosmetic categories, benefiting from non-discretionary and recurring procurement demand across retail, foodservice, and e-commerce channels.

Food and Beverages dominate application at 52.4% in 2025, owing to the wide adoption of flexible formats for snacks, beverages, frozen meals, and dairy. Pharmaceuticals (22.6%) commands premium pricing due to regulatory compliance requirements for barrier integrity and sterility, growing at the fastest CAGR of ~3.5% through 2034.

Preformed Bags and Pouches lead product type at 48.5% in 2025, reflecting growing consumer preference for stand-up pouches, spouted pouches, and resealable formats. Printed Rollstock (38.2%) serves high-volume production environments running VFFS and HFFS automated packaging lines in food manufacturing.

The United States commands 78.5% of the North America market in 2025, underpinned by the world's largest packaged food sector, major pharmaceutical manufacturing, and advanced retail infrastructure. Canada (21.5%) demonstrates consistent demand from food processing, health products, and cosmetic packaging.

Key Market Insights

|

Insight |

Data |

|

Largest Application |

Food and Beverages – 52.4% share (2025) |

|

Leading Product Type |

Preformed Bags and Pouches – 48.5% share (2025) |

|

Leading Country |

United States – 78.5% revenue share (2025) |

|

Second Country |

Canada – 21.5% revenue share (2025) |

|

Top Companies |

Amcor plc, Sealed Air, Mondi, Novolex, ProAmpac, American Packaging Corporation |

Key Analytical Observations Expanding On The Above Data:

- Food and Beverages, with 52.4% in 2025, dominates because flexible packaging extends shelf life, reduces food waste, and meets retail display requirements at significantly lower weight and cost than rigid alternatives, making it the default specification across snacks, beverages, frozen meals, and dairy categories.

- Preformed Bags and Pouches, with 48.5% in 2025, leads product type because stand-up pouches offer superior shelf presence, consumer convenience features (resealable zippers, spouts), and efficient transportation economics satisfying the broadest range of retail, food service, and e-commerce packaging requirements.

- United States' 78.5% dominance reflects its position as the largest packaged consumer goods market globally. Leading US food and beverage brands, pharmaceutical manufacturers, and personal care companies generate unparalleled flexible packaging procurement volumes across domestic converters.

- Canada, with 21.5% in 2025, benefits from a well-developed food processing sector including major processors in grains, dairy, and meat products, combined with a growing pharmaceutical and natural health product manufacturing base requiring certified barrier packaging solutions.

North America Flexible Packaging Market Overview

Flexible packaging refers to non-rigid packaging formats made from plastic films, paper, aluminum foil, and laminates thereof, configured into pouches, bags, wraps, films, and rollstock for primary and secondary product packaging. Performance attributes include barrier protection against moisture, oxygen, UV light, and contaminants across diverse end-use applications.

The North America ecosystem integrates petrochemical resin producers, film extrusion and lamination manufacturers, packaging converters and printers, brand owners and contract manufacturers, retail and food service distributors, and end-use industries spanning food, beverage, healthcare, personal care, and industrial products.

Market Dynamics

To evaluate market opportunities, Request Sample

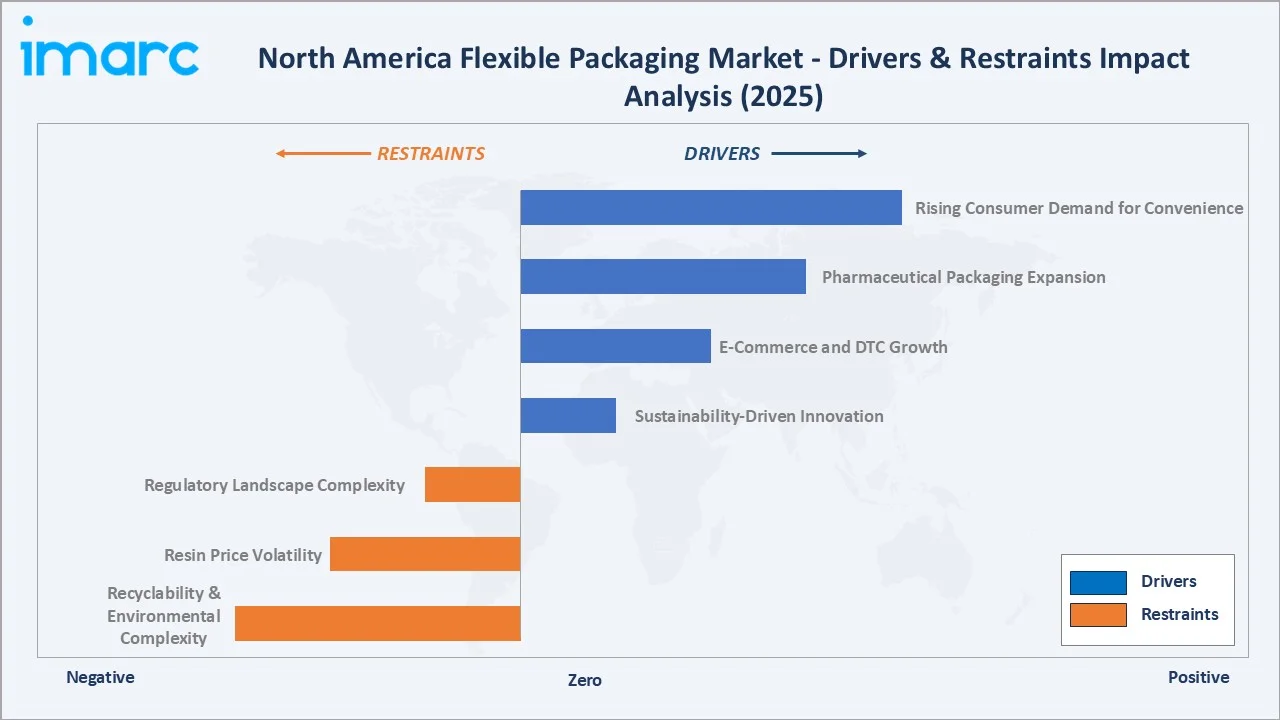

Market Drivers

- Rising Consumer Demand for Convenience: North American consumers' increasing preference for single-serve, on-the-go, and ready-to-eat food formats drives flexible pouch and stand-up bag adoption. Flexible formats offer resealable, easy-open, and portion-control features that align with modern consumption patterns and reduce household food waste.

- E-Commerce and Direct-to-Consumer Growth: Online grocery and direct-to-consumer shipment volumes in North America require lightweight, damage-resistant packaging that maintains product integrity through multi-node logistics chains. The United States counts 288 million active online shoppers, representing approximately 86% of the total population, thereby increasing the demand of packaging materials in the market. Flexible packaging's superior strength-to-weight ratio reduces shipping costs and dimensional weight charges versus rigid alternatives.

- Pharmaceutical and Healthcare Packaging Expansion: Rising demand for unit-dose packaging, blister films, and high-barrier pharmaceutical pouches, driven by increasing generic drug production and the growth of specialty pharmaceuticals, is supporting sustained, high-margin demand within the healthcare segment. Between 2011 to 2020, pharmaceutical imports into Canada increased by 58%. In the same period, Canadian pharmaceutical exports increased by 143%. United States accounted for 64% of exports and 29% of imports in 2020. The expansion of imports and exports highlights a robust and integrated supply chain, driving consistent demand for advanced, compliant, and protective flexible packaging solutions.

Market Restraints

- Recyclability and Environmental Complexity: Multi-layer flexible packaging structures combining incompatible polymer layers present significant technical and infrastructure barriers to mechanical recycling. Consumer pressure and brand sustainability commitments create reformulation cost pressures for converters and brand owners.

- Resin Price Volatility and Supply Chain Exposure: Flexible packaging raw material costs are directly linked to petrochemical feedstock pricing, which remains volatile due to crude oil price fluctuations, refinery disruptions, and natural gas market events, limiting converter margin protection capacity.

Market Opportunities

- Sustainable Mono-Material and Recyclable Film Development: Growing retailer sustainability mandates and brand packaging commitments are creating immediate demand for recyclable mono-material PE and PP flexible formats that replace complex multi-layer structures across food and personal care categories. In January 2024, Walki introduced fully recyclable mono-material packaging solutions for the food industry, aimed at supporting the transition toward a circular economy and reducing overall environmental impact. The company developed mono-material laminates that maintain strong barrier properties required for products such as meat, cheese, and other perishable foods, ensuring extended shelf life while minimizing food waste.

- Pharmaceutical Cold-Chain and Specialty Packaging: Expansion of biologics, gene therapies, and temperature-sensitive pharmaceutical products requiring ultra-high barrier, cold-chain-compatible flexible packaging formats creates a premium-priced growth segment less exposed to commodity price competition.

Market Challenges

- Regulatory Landscape and Food Contact Compliance: Evolving FDA food contact regulations, state-level chemical restriction legislation (California SB 54), and PFAS restrictions in food contact materials require continuous reformulation investment and create technical compliance complexity for multi-application converters.

- Consumer Perception and Greenwashing Scrutiny: Growing regulatory scrutiny of environmental claims for flexible packaging, including FTC Green Guides compliance for recyclability and compostability claims, imposes increasing risk management burdens on brand owners and their packaging suppliers.

Emerging Market Trends

1. Shift Towards Sustainable and Recyclable Packaging Solutions

Sustainable packaging adoption is the defining structural trend reshaping the North America flexible packaging market. Retailer mandates, brand pledges, and state-level packaging legislation are driving accelerated investment in mono-material recyclable films, bio-based polymers, and certified compostable formats as alternatives to conventional multi-layer structures.

2. Integration of Smart Packaging Technologies

QR codes, NFC tags, RFID integration, and time-temperature indicators embedded in flexible packaging formats are gaining adoption across pharmaceutical, premium food, and e-commerce applications. Smart packaging enables product authentication, consumer engagement, supply chain visibility, and serialization compliance.

3. Stand-Up Pouch and Spouted Pouch Format Expansion

Consumer preference for upright, resealable, and easy-pour packaging formats drives continued conversion from rigid containers to stand-up pouches and spouted variants across liquid, semi-liquid, powder, and solid food categories. Pouch formats reduce material consumption by 30–40% versus rigid equivalents.

4. Digital Printing and Short-Run Personalization

Advanced digital printing technology adoption by flexible packaging converters enables cost-effective short-run and personalized packaging production, supporting brand innovation cycles, seasonal campaigns, regional SKU variations, and direct-to-consumer packaging designs previously unfeasible with conventional flexographic setups.

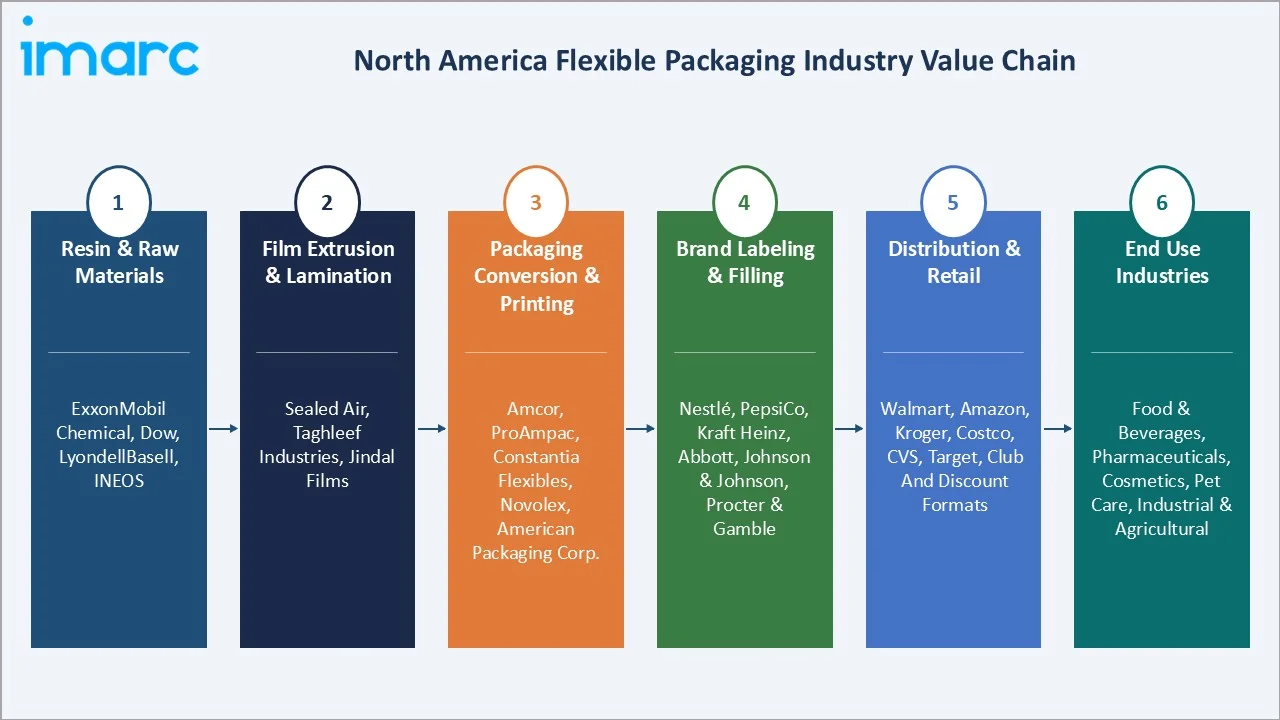

Industry Value Chain Analysis

The flexible packaging value chain spans six stages from raw material sourcing through end-use consumption. Film conversion and printing capture the highest value-add margins, while distribution logistics and multi-layer lamination generate significant technical differentiation that favors well-invested converters with broad material science capabilities.

|

Stage |

Key Players / Examples |

|

Resin & Raw Materials |

ExxonMobil Chemical, Dow, LyondellBasell, INEOS |

|

Film Extrusion & Lamination |

Sealed Air, Taghleef Industries, Jindal Films |

|

Packaging Conversion & Printing |

Amcor, ProAmpac, Constantia Flexibles, Novolex, American Packaging Corp. |

|

Brand Labeling & Filling |

Nestlé, PepsiCo, Kraft Heinz, Abbott, Johnson & Johnson, Procter & Gamble |

|

Distribution & Retail |

Walmart, Amazon, Kroger, Costco, CVS, Walgreens, Target, club and discount formats |

|

End Use Industries |

Food & Beverages, Pharmaceuticals, Cosmetics, Pet Care, Industrial & Agricultural |

Integrated converters with captive film extrusion, in-house printing, and proprietary lamination, such as Amcor's integrated flexible packaging model, achieve lower material cost structures and faster new product development cycles than processors relying on external film procurement.

Technology Landscape in the North America Flexible Packaging Industry

Film Extrusion and Multi-Layer Coextrusion Technology

The dominant film production technology is blown and cast film extrusion, where modern multilayer coextrusion lines produce up to 11-layer structures in a single pass, enabling precise barrier and mechanical property engineering. Coextruded films with EVOH, PVDC, and metallocene PE layers achieve oxygen transmission rates below 1 cc/m²/day for sensitive food and pharmaceutical applications.

Sustainable Material Innovation: Mono-Material and Bio-Based Films

High-barrier mono-material PE films incorporating ultra-thin EVOH barrier layers coextruded within all-polyethylene structures are enabling recyclable packaging transitions without sacrificing barrier performance. Bio-based PLA and PBAT compostable films are gaining certification traction for fresh produce, bakery, and food service flexible formats across North America.

Advanced Sealing and Barrier Coating Technologies

High-speed heat-sealing systems achieving hermetic seals at 400–600 packages per minute, combined with ultrasonic sealing for difficult-to-seal substrates, enable throughput expansion at brand owner filling lines. Plasma-deposited SiOx and AlOx transparent barrier coatings on flexible films displace traditional metallization in applications requiring optical transparency and microwave compatibility.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Preformed Bags and Pouches |

48.5% |

2025 |

|

Raw Material |

Plastic |

🔒 |

2025 |

|

Printing Technology |

Flexography |

🔒 |

2025 |

|

Application |

Food and Beverages |

52.4% |

2025 |

|

Country |

United States |

78.5% |

2025 |

By Application

Food and beverages command a 52.4% majority share in 2025 owing to its fundamental reliance on flexible packaging for product preservation, shelf-life extension, and retail display. Flexible formats have become the default specification across snack foods, beverages, dairy, frozen meals, and confectionery, owing to cost efficiency, format versatility, and superior barrier performance.

To access detailed market analysis, Request Sample

Pharmaceuticals at 22.6% in 2025, growing fastest at ~3.5% CAGR, is irreplaceable in environments requiring child-resistant, tamper-evident, moisture-barrier, and blister packaging certified to USP, FDA, and Health Canada standards.

Cosmetics (14.8%) serves premium personal care brands adopting stand-up pouches, sachets, and flexible tubes for travel-size and sustainable format innovation.

By Product Type

Preformed bags and pouches dominate the product segment at 48.5% in 2025, representing the highest-growth, most consumer-visible flexible packaging format. Stand-up pouches, quad-seal bags, flat-bottom pouches, and spouted formats dominate shelf space across baby food, pet food, beverages, sauces, and personal care, offering superior convenience and retail display economics.

Printed rollstock, with 38.2% in 2025, is the workhorse of high-volume food and consumer goods manufacturing, enabling VFFS and HFFS automated packaging lines at 200–400 packages per minute. Others (13.3%) includes specialty formats such as lidding films, shrink wrap, stretch wrap, and industrial flexible packaging.

Regional Market Insights

|

Country |

Share (2025) |

Key Growth Drivers |

|

United States |

78.5% |

World's largest packaged food sector; pharmaceutical manufacturing; personal care innovation; e-commerce growth |

|

Canada |

21.5% |

Food processing exports; natural health product manufacturing; sustainable packaging mandates; cross-border supply chain integration |

United States' 78.5% market dominance in 2025 is driven by the most structurally concentrated combination of packaged consumer goods production, food manufacturing scale, pharmaceutical output, and retail infrastructure in North America, generating unparalleled flexible packaging procurement volumes from domestic converters and co-manufacturers.

Canada, with 21.5% in 2025, demonstrates consistent demand anchored by robust food processing and agricultural product packaging. Major Canadian food processors in grain products, dairy, meat, and beverages generate significant domestic flexible packaging demand, supplemented by a growing pharmaceutical and natural health product sector requiring certified barrier packaging.

Competitive Landscape

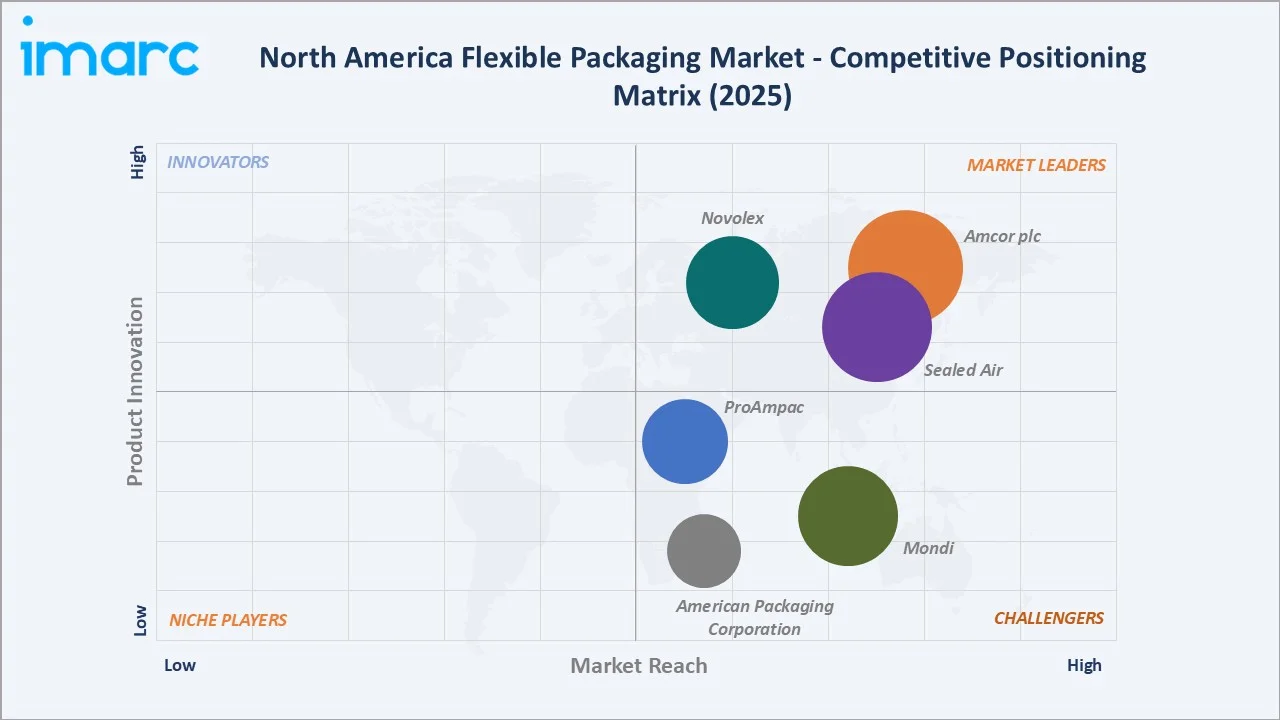

The North America flexible packaging market is moderately consolidated, with large global packaging conglomerates holding dominant positions supplemented by regional specialists. The US market is led by Amcor, Berry Global, Sealed Air, and Sonoco, while Canadian markets feature both global players and local converters.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

Amcor plc |

Flexibles, pouches, rollstock, medical packaging |

Leader |

Global scale post-Berry merger; sustainability; medical flex |

|

Sealed Air |

Cryovac food packaging, protective packaging |

Leader |

Food safety; e-commerce protective flex |

|

Mondi |

Consumer flexibles, industrial bags |

Challenger |

Sustainable materials; active North America manufacturing |

|

Novolex |

Bags, pouches, food service packaging |

Leader |

Food service; retail bags; US distribution |

|

ProAmpac |

Flexible pouches, rollstock, laminates |

Challenger |

PE-based sustainable flexible packaging |

|

American Packaging Corporation |

Printed flexible packaging, rollstock |

Challenger |

US regional; food and consumer goods |

Key players include Amcor plc, Sealed Air, Mondi, Novolex, ProAmpac, American Packaging Corporation, and others.

Key Company Profiles

Amcor plc

Amcor plc is one of world's largest flexible packaging companies, with operations across North America, Europe, Asia-Pacific, and Latin America. Amcor's portfolio encompasses flexible packaging, rigid packaging, and specialty cartons serving food, beverage, pharmaceutical, and personal care end markets.

- Product Portfolio: Offers consumer flexible packaging including stand-up pouches, rollstock, laminates, specialty pharmaceutical blister films, retort pouches, and high-barrier medical device packaging certified to ISO 11607.

- Recent Developments: In April 2019, Amcor announced the launch of its AmLite Ultra Recyclable packaging solution, a high-barrier flexible packaging designed to be fully recyclable while maintaining strong product protection. The company stated that the innovation utilized advanced polyolefin-based film technology, enabling packaging to be recycled within existing streams while delivering performance comparable to conventional multi-layer structures.

- Strategic Focus: Amcor's strategy leverages global scale and integrated manufacturing to compete on total cost, technical service, and innovation speed in North America's food and pharmaceutical flexible packaging markets, advancing sustainable packaging transitions.

Mondi

Mondi is a global leader in sustainable packaging and paper, with active North America operations through its Consumer Flexibles division headquartered in Jackson, Missouri. Mondi Consumer Flexibles in North America is a fully integrated flexible plastic packaging manufacturer providing a selection of value-added packaging solutions to various industries.

- Product Portfolio: The company offers stand-up pouches, pre-made bags, printed rollstock, high-barrier laminates, and industrial bags for food, pet food, personal care, and consumer goods packaging.

- Recent Developments: In August 2025, Mondi announced the launch of its Ad/Vantage Smooth Brown Semi Extensible kraft paper, designed to deliver high performance for both industrial and consumer packaging applications. The new paper combined strength, extensibility, and puncture resistance with a smooth surface, enabling efficient converting while supporting superior printing and coating performance.

- Strategic Focus: Mondi's North America strategy differentiates on deep consumer research capabilities, material-neutral design across plastic and paper substrates, and How2Recycle-certified recycle-ready formats targeting the pet food, personal care, and consumer goods segments.

Sealed Air

Sealed Air is a leading global packaging company known for its Cryovac brand of flexible food packaging and Bubble Wrap protective packaging solutions. Sealed Air's flexible packaging operations focus on food safety, protein packaging, and e-commerce protective packaging applications in North America.

- Product Portfolio: The company offers Cryovac shrink films, barrier bags, vacuum pouches, and modified atmosphere packaging (MAP) solutions for fresh meat, poultry, seafood, cheese, and processed food, along with e-commerce mailers and protective packaging.

- Recent Developments: In September 2025, Sealed Air announced the launch of its AUTOBAG 850HB Hybrid Bagging Machine, expanding its automated packaging portfolio to support both paper and poly mailers within a single system. The company stated that the new machine was designed to enhance fulfillment efficiency by enabling quick transitions between packaging materials, allowing operations to adapt to varying sustainability and performance requirements without disrupting throughput.

- Strategic Focus: Sealed Air's strategy focuses on technology leadership in food protection flexible packaging, leveraging Cryovac brand premium positioning to command value-over-volume market strategies in protein and perishable food categories.

Market Concentration Analysis

The North America flexible packaging market is moderately consolidated, with large global packaging conglomerates led by Amcor, Berry Global, and Sealed Air holding strong positions in high-volume commodity flexible segments, while regional converters and specialty operators maintain significant share in niche application markets.

The top four flexible packaging suppliers in North America collectively account for approximately 45–55% of regional revenue, reflecting concentration higher than the global market average but still leaving substantial share for mid-tier regional converters, specialty pharmaceutical packagers, and private-label flexible suppliers.

Consolidation through M&A is active in North America, driven by PE-backed platform roll-up strategies targeting regional converters, large packaging groups divesting non-core flexible assets, and brand owner supplier rationalization programs rewarding converters capable of serving multiple facilities across product categories.

Investment & Growth Opportunities

Fastest-Growing Segments

Pharmaceuticals flexible packaging at ~3.5% CAGR through 2034 is the highest-growth application segment, driven by biologics growth, specialty drug proliferation, unit-dose blister packaging expansion, and cold-chain pharmaceutical supply chain investment. Preformed Bags and Pouches growing at ~3.2% CAGR represents the broadest-based growth opportunity across food, personal care, and pet care.

Emerging Investment Themes

Sustainable packaging technology investment, including mono-material recyclable film development, bio-based resin alternatives, and certified compostable flexible structures, is attracting substantial capital from both strategic packaging companies and infrastructure-oriented PE investors aligned with North American retailer EPR mandates.

Venture & Investment Trends

Private equity interest in consolidating fragmented North America flexible packaging converter markets is growing, driven by fragmentation among mid-tier converters, recurring food and consumer goods demand supporting cash flow visibility, and strategic value from serving large-brand customers demanding flexible packaging innovation and sustainability credentials.

Future Market Outlook (2026-2034)

The North America flexible packaging market is forecast to expand from USD 49.67 Billion in 2025 to USD 64.05 Billion by 2034 at a CAGR of 2.78%, adding USD 14.38 Billion in incremental annual market value over the forecast period. This consistent, sustained growth reflects the market's food, pharmaceutical, and consumer goods demand characteristics.

Three structural forces will shape the North America flexible packaging landscape through 2034. Sustainable packaging transition, with major retailer EPR compliance deadlines and state-level plastic packaging legislation, will drive multi-billion-dollar converter investment in recyclable film infrastructure, reshaping material specifications across the flexible packaging market.

Pharmaceutical flexible packaging growth, accelerated by the biologic drug pipeline's cold-chain packaging requirements and OTC drug market unit-dose adoption, will become an increasingly important growth driver as food flexible packaging growth moderates. Digital and smart packaging integration will differentiate premium products from commodity alternatives.

Research Methodology

Primary Research

Primary research encompassed over 40 structured interviews with North America flexible packaging industry stakeholders, including senior commercial managers at major converters, procurement specialists at brand owner companies, sustainability directors at retail groups, and technical directors at film and resin manufacturers.

Secondary Research

Key secondary sources include Flexible Packaging Association (FPA) industry data, American Chemistry Council resin production statistics, US Census Bureau packaging shipments data, FDA pharmaceutical packaging guidance, Health Canada packaging regulations, Packaging Digest, Flexible Packaging Magazine, and Converting Magazine.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, consumer expenditure data, packaged food market growth, pharmaceutical sector expansion, and historical market evolution patterns with scenario analysis for uncertainty.

North America Flexible Packaging Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Printed Rollstock, Preformed Bags and Pouches, Others |

| Raw Materials Covered | Plastic, Paper, Others |

| Printing Technologies Covered | Flexography, Rotogravure, Digital, Others |

| Applications Covered | Food and Beverages, Pharmaceuticals, Cosmetics, Others |

| Countries Covered | United States, Canada |

| Companies Covered | Amcor plc, Sealed Air, Mondi, Novolex, ProAmpac, American Packaging Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the North America flexible packaging market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the North America flexible packaging market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the North America flexible packaging industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the North America Flexible Packaging Market Report

The North America flexible packaging market reached USD 49.67 Billion in 2025, reflecting consistent demand from the food, beverage, pharmaceutical, and personal care industries across the United States and Canada.

The market is projected to reach USD 64.05 Billion by 2034, growing at a CAGR of 2.78% during 2026-2034, driven by e-commerce expansion, pharmaceutical sector growth, and sustainable packaging format adoption.

Food and beverages lead with a 52.4% application share in 2025, owing to the broad adoption of flexible formats across snacks, beverages, dairy, frozen meals, and confectionery for shelf life, cost, and format versatility advantages.

Preformed bags and pouches lead at 48.5% in 2025, driven by stand-up pouches and spouted formats gaining penetration across food, personal care, and pet food categories with superior convenience and retail display features.

United States commands a dominant 78.5% market share in 2025, driven by the world's largest packaged food sector, major pharmaceutical manufacturing, personal care brand innovation, and advanced retail and e-commerce infrastructure.

Pharmaceuticals is the fastest-growing application at ~3.5% CAGR through 2034, driven by biologics, unit-dose blister packaging, specialty drug flexible requirements, and OTC product packaging innovation.

Leading companies include Amcor plc, Sealed Air, Mondi, Novolex, ProAmpac, American Packaging Corporation, and others.

Key applications include food snack packaging, beverage pouches, pharmaceutical blister films, cosmetic sachets, pet food bags, fresh produce films, frozen meal packaging, and personal care product flexible formats across retail, food service, and e-commerce channels.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade