North America Potato Starch Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Country, 2026-2034

North America Potato Starch Market Summary:

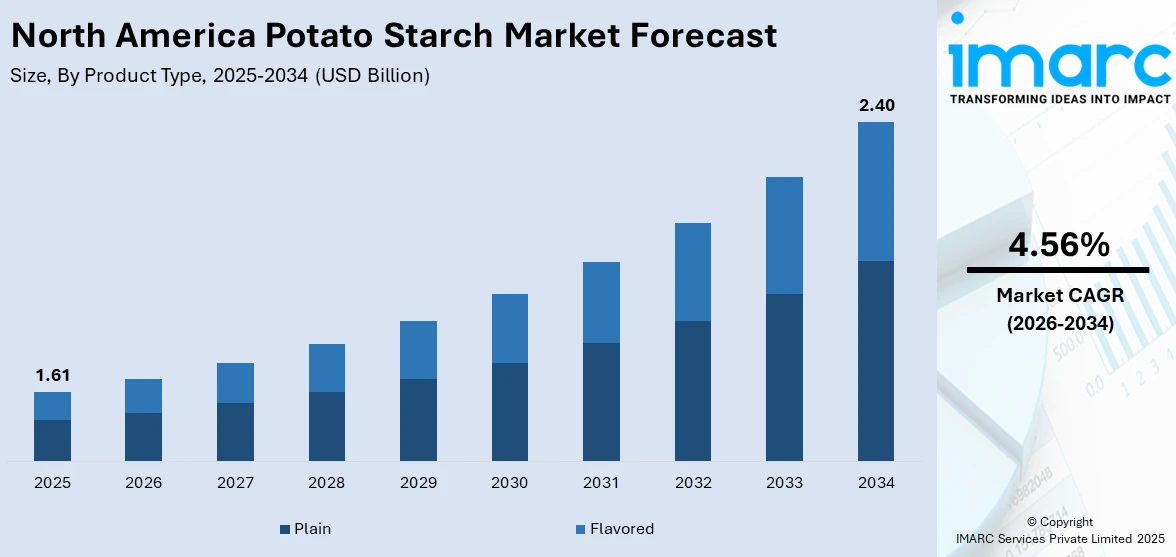

The North America potato starch market size was valued at USD 1.61 Billion in 2025 and is projected to reach USD 2.40 Billion by 2034, growing at a compound annual growth rate of 4.56% from 2026-2034.

The growth of the North America potato starch market is mainly influenced by the rising consumer preference for clean-label and gluten-free food items, the increasing use in processed and convenience foods, and the incorporation in plant-based food formulations. The alignment of health-focused consumer choices, sustainability efforts in packaging, and technological advancements in starch processing is fundamentally transforming the competitive environment and presenting significant opportunities for market players. The increasing use of potato starch as a natural thickening, binding, and stabilizing agent in food processing industries is contributing to the North America potato starch market share.

Key Takeaways and Insights:

- By Product Type: Plain leads the market with a share of 64% in 2025, propelled by its remarkable adaptability in food processing uses, neutral flavor profile allowing extensive application in baked goods, soups, sauces, and processed foods, along with enhanced thickening capabilities favored by producers.

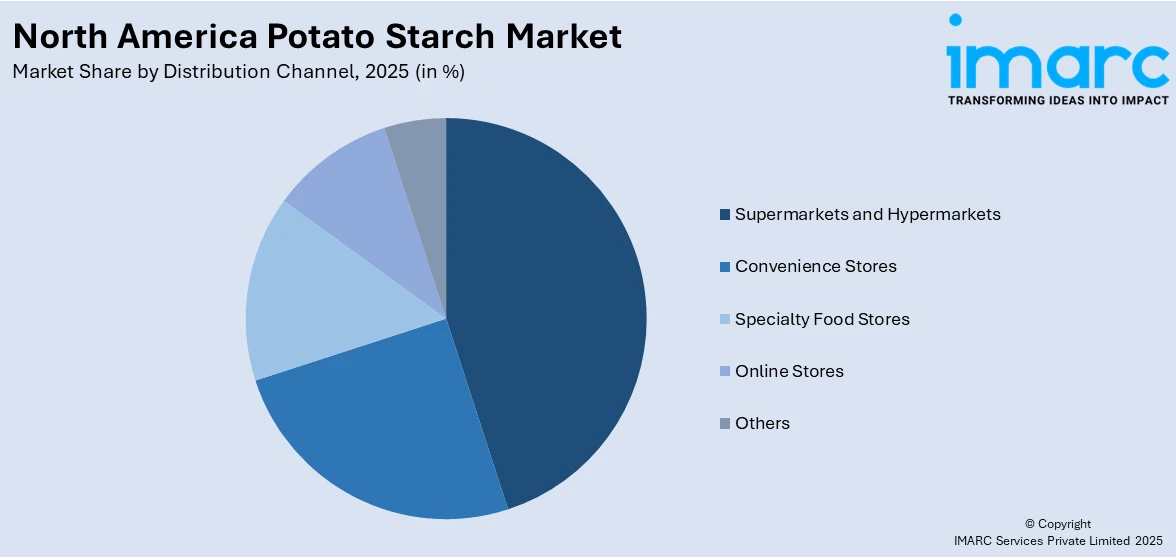

- By Distribution Channel: Supermarkets and hypermarkets represent the largest segment with a market share of 45% in 2025. This dominance is because of one-stop shopping convenience, extensive product assortment, competitive pricing strategies, and consumer preference for in-store purchasing experiences.

- By Country: United States dominates the market with a share of 73% in 2025, due to its robust manufacturing capabilities, broad retail infrastructure, high consumption of convenience foods, and well-established food processing industry.

- Key Players: The North America potato starch market exhibits moderate competitive intensity, with multinational ingredient corporations competing alongside regional manufacturers across product segments and distribution channels. Major players focus on product innovation, clean-label formulations, and strategic partnerships to strengthen market positioning.

To get more information on this market Request Sample

The North America potato starch market is seeing growth, supported by rising consumer interest in natural and minimally processed food components, along with the region's robust agricultural and food processing strengths. Potato starch is prized for its flexibility, acting as an essential component in numerous uses, such as baked goods, dairy substitutes, soups, sauces, and pre-packaged meals. It is particularly favored because of its gluten-free qualities, becoming a preferred option for those with dietary limitations. Moreover, its cost efficiency in relation to other starches is establishing it as a favored choice for food producers throughout various market segments, ranging from premium to budget offerings. The strong agricultural industry in North America meets the rising demand, with potato output for the United States and Canada projected to hit 538 million cwt in 2025, ensuring a steady supply of raw material to satisfy the expanding requirements of the potato starch sector.

North America Potato Starch Market Trends:

Increasing Demand for Processed Food Products

The growing consumer demand for convenient, ready-to-eat (RTE) food options is a key factor influencing the North American potato starch market, as processed foods like snacks, sauces, and baked goods increasingly rely on potato starch for stabilizing, thickening, and enhancing texture. As the preference for quick meal solutions rises, manufacturers increasingly depend on potato starch to meet these consumer expectations. In 2024, government data revealed that the food and beverage processing industry was Canada’s largest manufacturing sector, with sales of goods manufactured valued at $173.4 billion, underscoring the significant role of processed food in the economy.

Strengthened Supply Chain for Potato Farming

The stability and resilience of the potato supply chain in North America is a crucial factor impelling the growth of the potato starch market. Improvements in farming techniques, storage facilities, and transportation networks ensure a reliable supply of high-quality potatoes for starch production. This consistency benefits manufacturers by providing a steady, cost-effective source of raw material, which helps maintain competitive production costs. Additionally, in 2024, Ahold Delhaize USA and Campbell's launched a pilot initiative to reduce Scope 3 emissions in potato farming. Over three years, the project aimed to support regenerative farming practices on 1,000 acres across North Carolina, New York, and Michigan, further enhancing sustainability in the supply chain.

Development in Personalized Nutrition and Functional Foods

The rise in personalized nutrition, where consumers seek tailored diets based on individual health needs, is creating new opportunities for potato starch, particularly in functional foods and supplements. Potato starch, especially resistant starch, is valued for its prebiotic properties and is increasingly used in products aimed at improving gut health, blood sugar control, and overall well-being. This trend is especially prominent among the geriatric population, as the number of older adults with specific health concerns, such as digestive issues and blood sugar imbalances, continues to rise. The number of Americans ages 65 and older is projected to increase from 58 million in 2022 to 82 million by 2050 (a 42% increase), and the 65-and-older age group’s share of the total population is projected to rise from 17% to 23%, thus catalyzing the demand for health-focused food products.

Market Outlook 2026-2034:

The North America potato starch market shows growth potential throughout the forecast period, driven by rising demand for clean-label products and evolving food manufacturing practices. The market generated a revenue of USD 1.61 Billion in 2025 and is projected to reach a revenue of USD 2.40 Billion by 2034, growing at a compound annual growth rate of 4.56% from 2026-2034. This growth is influenced by consumer preferences for natural ingredients and healthier food options, along with the increasing use of potato starch as a versatile ingredient in various industries, particularly food and beverages.

North America Potato Starch Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Plain |

64% |

|

Distribution Channel |

Supermarkets and Hypermarkets |

45% |

|

Country |

United States |

73% |

Product Type Insights:

- Plain

- Flavored

Plain dominates with a market share of 64% of the total North America potato starch market in 2025.

Plain potato starch serves as a fundamental ingredient across diverse food processing applications due to its neutral taste profile, exceptional thickening capabilities, and versatile functionality. The segment dominates the market because plain potato starch offers unmatched adaptability for manufacturers seeking clean-label thickening and binding solutions without altering product flavor characteristics. Food processors utilize plain potato starch extensively in soups, sauces, gravies, and bakery products where maintaining original taste profiles remains essential for consumer acceptance.

The segment also benefits from the growing demand in gluten-free food formulations, where plain potato starch provides superior texture and consistency compared to alternative starches. The cost-effectiveness of plain potato starch compared to modified variants further strengthens its market leadership, particularly among price-sensitive manufacturers in processed food and industrial applications. Moreover, plain potato starch maintains a commanding market position primarily serving traditional food applications where natural labeling and clean ingredient declarations are essential.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Convenience Stores

- Specialty Food Stores

- Online Stores

- Others

Supermarkets and hypermarkets lead with a market share of 45% of the total North America potato starch market in 2025.

Supermarkets and hypermarkets hold the biggest market share owing to their broad reach, diverse product offerings, and consumer preference for convenient, one-stop shopping. These retailers attract price-sensitive shoppers with competitive pricing strategies, making them highly appealing to budget-conscious consumers. Supported by robust supply chain networks, they maintain consistent product availability in both metropolitan and suburban areas. For example, in 2025, U.S. retail and food service sales were estimated at $735.9 billion, highlighting the significant role of these retail formats in meeting diverse consumer needs.

The dominance of supermarkets and hypermarkets is further strengthened by their ability to stock a wide variety of potato starch brands and product types, catering to different consumer preferences, including organic, conventional, and specialty formulations. These retail stores enhance in-store visibility by setting up dedicated sections for baking and cooking ingredients, driving impulse purchases. Additionally, the integration of loyalty programs, digital marketing campaigns, and targeted promotions bolsters client engagement, encouraging repeat purchases and long-term brand loyalty among shoppers.

Country Insights:

- United States

- Canada

United States exhibits a clear dominance with a 73% share of the total North America potato starch market in 2025.

United States represents the largest segment, driven by a well-established food processing industry and the growing demand for clean-label, natural ingredients. The country’s large-scale food manufacturers are increasingly adopting potato starch as a versatile ingredient due to its superior texture, stability, and natural composition. Additionally, the rising consumer awareness around health and sustainability is catalyzing the demand for potato starch in processed foods, snacks, and beverages, contributing to the market growth.

The Philippines benefits from advanced agricultural practices, ensuring a steady supply of high-quality potatoes for starch production. This consistent availability, coupled with innovations in extraction technology, improves both efficiency and sustainability within the industry. A key example of this progress is the USDA's 2025 launch of the $700 million Regenerative Pilot Program. This initiative supports farmers transitioning to regenerative practices, reducing production costs while enhancing soil health and water quality. The program offers streamlined applications and funds key conservation initiatives, driving long-term agricultural sustainability.

Market Dynamics:

Growth Drivers:

Why is the North America Potato Starch Market Growing?

Technological Advancements in Potato Starch Processing

Advancements in starch extraction and processing technologies are significantly improving the efficiency and quality of potato starch production. Modern techniques, such as enzymatic modifications and state-of-the-art filtration systems, are enhancing the functional properties of potato starch, including its viscosity, solubility, and stability under varying conditions. These technological innovations make potato starch more versatile and suitable for a broader range of applications like food, pharmaceuticals, cosmetics, and industrial uses. The ability to produce customized starches with specific characteristics is further expanding its market potential, driving the demand across various industries that require specialized ingredients for product formulations and enhanced performance.

Increasing Preference for Organic Products

The rising demand for organic food products is significantly contributing to the growth of the potato starch market, as consumers increasingly seek organic ingredients for their health and sustainability benefits. Potato starch sourced from organically grown potatoes is becoming a preferred choice for food and beverage manufacturers aiming to meet this demand. This shift aligns with the broader movement toward organic and sustainable agriculture. According to the IMARC Group, the Canada organic food market is projected to reach USD 13.05 billion by 2033, underscoring the growing consumer preference for organic products and driving the adoption of organic potato starch within the industry.

Rising Demand in Food and Beverage Sector

The robust expansion of the North American food and beverage sector has significantly increased the demand for potato starch, which plays a crucial role in addressing the evolving preferences of consumers. As the population continues to grow, with Statistics Canada reporting an increase of 20,107 people between January 1 and April 1, 2025, bringing the total population to 41,548,787 the demand for more diverse and specialized food products intensifies. Potato starch’s versatility, used in beverages, dressings, processed meats, and more, enables food manufacturers to meet these consumer needs. Its functional properties support the growing demand across multiple food production channels, further expanding its market presence.

Market Restraints:

What Challenges the North America Potato Starch Market is Facing?

Intense Competition from Substitute Starches

The market encounters substantial difficulties from alternative starches, such as corn starch, wheat flour, arrowroot powder, rice flour, and tapioca starch. These alternatives are frequently utilized in culinary applications, like thickening, baking, and frying, decreasing dependence on potato starch. Alternatives frequently provide advantages such as improved heat resistance and competitive costs, restricting the growth of the potato starch market in specific uses.

Raw Material Price Volatility and Supply Chain Disruptions

Potato cultivation is very responsive to environmental factors, resulting in supply weaknesses for starch producers. Weather phenomena like droughts, floods, and temperature extremes can greatly influence potato yields and quality, resulting in price variations and supply deficits. This fluctuation impacts the whole supply chain from processors to final users, compelling producers to handle procurement risks via varied sourcing strategies.

Limited Shelf Life and Storage Requirements

Native potato starch typically has a limited shelf life of twelve to eighteen months and can be susceptible to microbial growth if not kept in ideal humidity and temperature conditions. These storage needs raise operational expenses for producers and suppliers while restricting market entry in areas without sufficient cold-chain systems and regulated storage options.

Competitive Landscape:

The North America potato starch market exhibits moderate competitive intensity characterized by the presence of multinational ingredient corporations alongside regional manufacturers competing across product segments and distribution channels. Market dynamics reflect strategic positioning, ranging from premium, innovation-driven offerings emphasizing advanced functionality and clean-label formulations to value-oriented products targeting cost-conscious food manufacturers. The competitive landscape is increasingly shaped by sustainability initiatives, product innovation capabilities, and strategic partnerships enabling companies to strengthen market positioning. Key players focus on expanding production capacity, developing specialized starches for emerging applications, and enhancing distribution networks to capture the growing demand across food processing, pharmaceutical, and packaging industries.

Recent Developments:

- July 2025: Brenntag and Royal Avebe expanded their partnership to North America, marking the first time Royal Avebe’s potato starch and derivatives will be supplied to the US food and nutrition market. The collaboration aimed to meet rising consumer demand for sustainable, plant-based ingredients.

North America Potato Starch Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | ‘000 Tons, Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Plain, Flavored |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Specialty Food Stores, Online Stores, Others |

| Countries Covered | United States, Canada |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the North America Potato Starch Market Report

The North America potato starch market size was valued at USD 1.61 Billion in 2025.

The North America potato starch market is expected to grow at a compound annual growth rate of 4.56% from 2026-2034 to reach USD 2.40 Billion by 2034.

Plain holds the largest revenue share of 64% in 2025 due to its versatility, neutral taste profile, and widespread applications across food processing, pharmaceutical, and cosmetic industries as a natural thickening and binding agent.

Key factors driving the North America potato starch market include the stability and resilience of the potato supply chain, supported by advancements in farming techniques, storage, and transportation. For instance, in 2024, Ahold Delhaize USA and Campbell's launched an initiative to support regenerative farming on 1,000 acres, enhancing sustainability and ensuring a reliable, cost-effective supply of potatoes for starch production.

Major challenges include intense competition from substitute starches, such as corn and tapioca, raw material price volatility due to weather-related supply disruptions, limited shelf life requiring controlled storage conditions, and supply chain constraints affecting procurement stability.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)