Offshore Decommissioning Market Report by Service (Project Management, Engineering and Planning, Permitting and Regulatory Compliance, Platform Preparation, Well Plugging and Abandonment, Conductor Depth, Mobilization and Demobilization of Derrick Barges, Platform Depth, Pipeline and Power Cable Decommissioning, Materials Disposal, Site Clearance), Removal (Leave in Place, Partial Depth, Complete Depth), Depth (Shallow Water, Deep Water), Structure (Topside, Substructure, Sub Infrastructure), and Region 2026-2034

Market Overview:

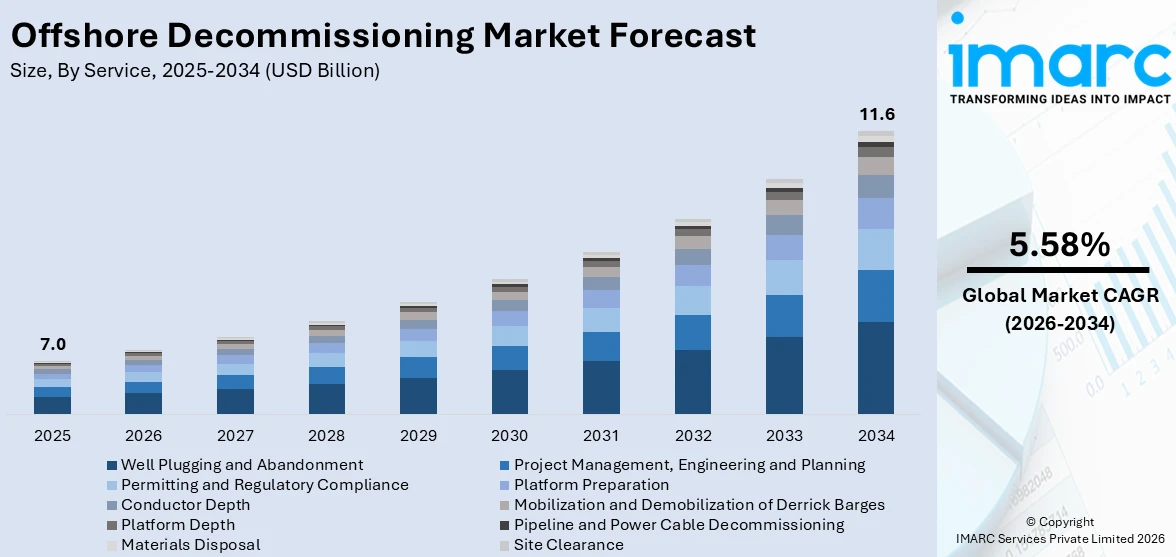

The global offshore decommissioning market size reached USD 7.0 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 11.6 Billion by 2034, exhibiting a growth rate (CAGR) of 5.58% during 2026-2034. The growing number of offshore oil and gas projects, increasing utilization of commercial drones, and rising implementation of stringent policies by governing agencies to preserve marine life, are some of the major factors propelling the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 7.0 Billion |

| Market Forecast in 2034 | USD 11.6 Billion |

| Market Growth Rate (2026-2034) | 5.58% |

Offshore Decommissioning Market Analysis:

- Market Growth and Size: The offshore decommissioning market is rapidly expanding, fueled by an increase in mature offshore oilfields and a global rise in energy demand. This sector is propelled by the continuous rise in oil and gas exploration activities and the pressing necessity to handle an escalating number of non-productive, mature oil wells.

- Major Market Drivers: Key drivers include the worldwide escalation in oil and gas exploration activities, which necessitates the decommissioning of inactive offshore infrastructure, complemented by stringent global environmental regulations. These regulations are designed to protect marine ecosystems and prevent pollution, ensuring the safe disposal or recycling of offshore structures.

- Key Market Trends: A significant trend in the market is the focus on well plugging and abandonment, representing the largest market share and aiming to avert environmental damage by securely sealing inactive underwater wells. Moreover, the sector is moving towards the adoption of sophisticated decommissioning methods and a shift towards more comprehensive removal of offshore structures.

- Geographical Trends: Europe dominates the market due to its widespread decommissioning in offshore and results from the profusion of mature offshore fields and the stricter EU legislation on environmental protection and the management of the offshore infrastructure. North America’s market is showing a significant growth which is being driven by increased environmental consciousness, regulation frameworks, and underlining the age of multiple offshore platforms for decommissioning, enabling the industry to tackle a range of market challenges.

- Competitive Landscape: The competition among the key market players has escalated with the players investing more in the eco-friendly decommissioning practices, innovative technologies, and sustainable strategies to remain ahead of the rest and to fulfil the ever-growing global demand. Companies are putting efforts into collaboration, technical innovations, and employee skill development for better decommissioning possibilities, consistent with environmental standards and the fast-growing market needs.

- Challenges and Opportunities: The sector is faced with challenges, such as the very high costs of decommissioning projects, technological complexities, and the need to balance economic and environmental aspects, therefore there is the necessity of creative solutions and good project management. There are market possibilities in the development of dismantling technologies, the chance for recycling and repurposing the discarded material, and the global continuing focus on environmental sustainability, showing new ways of market growth and development.

To get more information on this market Request Sample

Offshore decommissioning refers to the process of removing infrastructure from previous offshore sites that have been used to assist oil and gas extraction operations. The procedures encompass in offshore decommissioning, including project management, engineering, and planning, permitting and regulatory compliance, platform preparation, well plugging and abandonment, conductor removal, mobilization and demobilization of derrick barges, and pipeline and power cable decommissioning. It generally involves clearing and filling the well and removing all the infrastructure and platform. It also occurs during the final phase of an oil well’s life, as the bulk of the oil has been depleted.

Significant growth in offshore oil and gas projects is driving the global market. In addition, many counties government authorities have enforced strict regulations regarding marine life, which will benefit the industry by enabling companies to safely dispose of equipment used in offshore oil production. Also, several different decommissioning processes are available in most offshore areas, which is expected to increase market growth. Similarly, the growing demand for crude oil or fossil fuels to run vehicles and make other items, such as adhesives, solvents, plastics, and polyurethane will supplement the level of market growth. Additionally, the increase in the fluctuation of oil prices on a global scale will result in increased market growth.

Offshore Decommissioning Market Trends/Drivers:

Rising oil and gas exploration activities stimulating market growth

At present, the global demand for energy is prompting an increase in oil and gas exploration activities which is driving the offshore decommissioning market growth. This rise is also fueled by the widespread use of heavy machinery and electronic devices across various industries, as well as the increasing installation of air conditioning systems in both residential and commercial sectors, which lead to higher electricity consumption. Furthermore, the reliance of passenger cars and certain heavy-duty vehicles on oil-based fuels underscores the continuous need for oil. This growing demand for oil is paralleled by an increase in offshore decommissioning activities, which are essential for addressing mature oil wells that are no longer productive. As per the World Energy Outlook 2022 (WEO) report by IEA, global energy demand is anticipated to increase by 28% between 2021 and 2050, according to the International Energy Agency.

Increasing number of abandoned wells and mature offshore oilfields catalyzing demand for offshore decommissioning

Currently, the global rise in the number of abandoned wells and mature offshore oilfields is broadening the scope of the offshore decommissioning market report. Abandoned well and mature offshore oilfields refer to the oil wells which are no longer producing crude oil and are in the state of reaching the end of their productive lifecycle. These offshore oil fields require special management and cannot be left idle with the installed infrastructure in waterbodies. They are capable of releasing hydrocarbons into the water, which are responsible for destroying marine life and increasing the toxicity of natural water bodies. Hence, to prevent the destruction of marine life and water resources, employment of offshore decommissioning is necessary. According to NTSA, the total estimated cost of decommissioning UKCS upstream oil and gas infrastructure fell by £1.5bn (2%) to £44.5bn in 2021 – contributing to a total cut of £15bn (25%) since 2017, when the NSTA introduced a baseline estimate of £59.7bn and set a target of reducing costs by 35% to £39bn by end-2022.

Rising awareness about the restoration of marine life augmenting market growth

At present, there is a rise in environmental awareness among the masses due to the increasing incidence of global warming, climate change, and air and water pollution, which is leading to increase in offshore decommissioning market size. Apart from this, the production of various toxic wastes and hazardous wastewater from industries is degrading the conditions of marine life. In addition, various oil exploration activities, along with the rising cases of oil spills in oceans, are further hampering the conditions of water resources. Unused oil fields and mature oil wells, when left in offshore regions, often release toxic residues or hydrocarbons into the water bodies, which degrades marine life and increases toxicity. Hence, the adoption of offshore decommissioning and recycling of offshore infrastructures is important for restoring marine life and preventing the release of hazardous elements from mature wells, this is turn is escalating the offshore decommissioning market share. For instance, the International Tanker Owners Pollution Federation (ITOPF) recorded an average of 6.8 large oil spills (greater than 700 tonnes) per year between 2010 and 2019 from tankers, barges, and other sources.

Offshore Decommissioning Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global offshore decommissioning market report, along with forecasts at the global, regional, and country levels from 2026-2034. Our report has categorized the market based on service, removal, depth, and structure.

Breakup by Service:

- Project Management, Engineering and Planning

- Permitting and Regulatory Compliance

- Platform Preparation

- Well Plugging and Abandonment

- Conductor Depth

- Mobilization and Demobilization of Derrick Barges

- Platform Depth

- Pipeline and Power Cable Decommissioning

- Materials Disposal

- Site Clearance

Well plugging and abandonment represents the largest market share

The report has provided a detailed breakup and analysis of the offshore decommissioning market based on the service. This includes project management, engineering and planning, permitting and regulatory compliance, platform preparation, well plugging and abandonment, conductor depth, mobilization and demobilization of Derrick Barges, platform depth, pipeline and power cable decommissioning, materials disposal, and site clearance. According to the report, well plugging and abandonment represented the largest segment.

Well plugging and abandonment refers to the main element of the offshore decommissioning process and involves thoroughly cleaning the wellbore and carefully installing plugs in the well. This is an important step as it prevents any environmental issues caused by leaving the underwater well open.

Project management, engineering, and planning are initial steps managed by the facility owner to generate specific and sufficient information, including costs related to continuing operation for specific time periods, ceasing operation by a specific date, and determining the type of decommissioning to pursue.

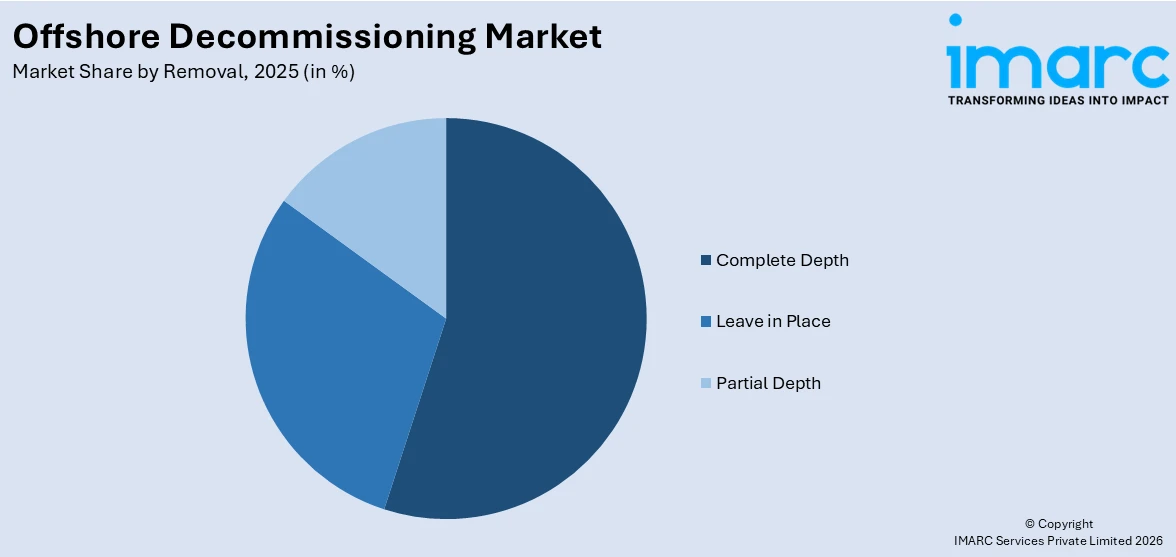

Breakup by Removal:

Access the comprehensive market breakdown Request Sample

- Leave in Place

- Partial Depth

- Complete Depth

Complete depth holds the leading market share

The report has provided a detailed breakup and analysis of the offshore decommissioning market based on the removal. This includes leave in place, partial depth, and complete depth. According to the report, complete depth represented the largest segment as it is essential to remove the complete offshore platform, restore marine life and seafloor to their pre-production conditions, and prevent the occurrence of environmental issues. It enables the ecosystem to return to its original state and minimizes pollution caused by oil and gas exploration activities.

Leave in place involves leaving structures, pipelines, and infrastructure in place without causing any environmental and physical disturbances. It is also capable of benefiting subtidal benthic invertebrates by providing habitat and shelter and encouraging the accumulation of natural sediments.

Breakup by Depth:

- Shallow Water

- Deep Water

Shallow water holds the largest market share

The report has provided a detailed breakup and analysis of the offshore decommissioning market based on the depth. This includes shallow water and deep water. According to the report, shallow water represents the largest segment. Shallow water refers to an area of water that measures only a short distance from the top of the surface. Offshore discharging activities in shallow water require lower operational expenses and a lesser amount of effort to disassemble the platform and infrastructure when it becomes non-operable.

Deep water refers to offshore regions that are nearer to the sea floor and wherein the depth of water is maximum. Additionally, oil and gas exploration activities are carried out in deep water and ultra-deep-water levels by creating holes in the sea floor and using a drilling rig. Moreover, offshore decommissioning activities in deep waters require a specialized workforce and equipment to reach a considerable depth and conduct the entire process without causing disturbances to marine life and other environmental complications.

Breakup by Structure:

- Topside

- Substructure

- Sub Infrastructure

Topside holds the biggest market share

The report has provided a detailed breakup and analysis of the offshore decommissioning market based on the structure. This includes the topside, substructure, and sub infrastructure. According to the report, topside represents the largest segment. Topside refers to parts of offshore drilling, which are present above the waterline and installed onto either a fixed or floating underwater structure. It comprises the drilling rig, living accommodation, and processing facilities. During the explanatory phase of the life of an offshore oil rig, the topside is often a bare structure sitting atop a submerged tower called a jacket.

Substructure of an offshore drilling platform is necessary to support the topside and maintain its position above the ocean-free surface. It is designed and fabricated separately and connected with the topside at the offshore site.

Breakup by Region:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Europe exhibits a clear dominance, accounting for the largest offshore decommissioning market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Europe accounted for the largest market share.

Europe held the biggest market share due to the rising offshore decommissioning activities taking place in the region. Besides this, the rising oil and gas exploration activities to fulfill the energy demands, along with the increasing number of abandoned wells and the presence of numerous offshore oilfields, are further propelling the growth of the market in the region.

North America is estimated to expand further in this domain, due to the growing environmental awareness and initiatives taken to preserve marine life. Besides this, the increasing number of offshore oil and gas platforms that are under evaluation for dismantlement in the bearish oil market is bolstering the growth of the market.

Competitive Landscape:

Several major players involved in the market are attracting considerable demand for offshore decommissioning. Due to rising oil and gas exploration to meet global energy demand and stringent regulations targeting marine life, they are concentrating on environmental-friendly procedures and recycling several offshore installations to reduce adverse environmental effects. Several top companies are implementing sustainable measures during engineering, procurement, construction, and integration of multiple types of offshore facilities. Moreover, they recruit a competent workforce and upgrade their skills to conduct the decommissioning procedures with the most advanced technology in the industry. Furthermore, they focus on collaboration and partnership with other organizations to enhance their foothold in the subsea services market. The leading companies are heavily investing to develop several advanced methods of offshore decommissioning, such as water injection, gas injection, chemical injection, thermal recovery, and hydraulic fracturing.

The report has provided a comprehensive analysis of the competitive landscape in the global offshore decommissioning market. Detailed profiles of all major companies have also been provided. Some of the key players in the global offshore decommissioning market include:

- AF Gruppen Asa

- Aker Solutions ASA

- Allseas Group S.A

- Claxton Engineering Services Ltd.

- DNV GL Group

- Heerema Marine Contractors

- John Wood Group PLC

- Mactech Offshore Machining & Cutting Solutions

- Petrofac Limited

- Saipem S.p.A.

- Subsea 7 S.A

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Recent Developments:

- In September 2023, AF Gruppen Asa received a contract from TotalEnergues EP Nederland B.V for the removal and recycling of platforms in the Dutch sector of the North Sea.

- In February 2023, Allseas Group S.A. announced its return to the East Mediterranean in the third quarter of 2024 to execute the installation scope for phase one of the Tamar expansion project.

- In June 2023, DNV GL Group signed a memorandum of understanding with the Institute of Energy and PTSC Mechanical and Construction to deliver one of the first offshore wind power assets in Vietnam.

Offshore Decommissioning Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Services Covered | Project Management, Engineering, and Planning, Permitting and Regulatory Compliance, Platform Preparation, Well Plugging and Abandonment, Conductor Depth, Mobilization and Demobilization of Derrick Barges, Platform Depth, Pipeline and Power Cable Decommissioning, Materials Disposal, Site Clearance |

| Removals Covered | Leave in Place, Partial Depth, Complete Depth |

| Depths Covered | Shallow Water, Deep Water |

| Structures Covered | Topside, Substructure, Sub Infrastructure |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | AF Gruppen Asa, Aker Solutions ASA, Allseas Group S.A, Claxton Engineering Services Ltd., DNV GL Group, Heerema Marine Contractors, John Wood Group PLC, Mactech Offshore Machining & Cutting Solutions, Petrofac Limited, Saipem S.p.A., Subsea 7 S.A, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global offshore decommissioning market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global offshore decommissioning market?

- What is the impact of each driver, restraint, and opportunity on the global offshore decommissioning market?

- What are the key regional markets?

- Which countries represent the most attractive offshore decommissioning market?

- What is the breakup of the market based on the service?

- Which is the most attractive service in the offshore decommissioning market?

- What is the breakup of the market based on the removal?

- Which is the most attractive removal in the offshore decommissioning market?

- What is the breakup of the market based on the depth?

- Which is the most attractive depth in the offshore decommissioning market?

- What is the breakup of the market based on the structure?

- Which is the most attractive structure in the offshore decommissioning market?

- What is the competitive structure of the global offshore decommissioning market?

- Who are the key players/companies in the global offshore decommissioning market?

Key Benefits for Stakeholders

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the offshore decommissioning market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global offshore decommissioning market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the offshore decommissioning industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)