Oman Gift Cards Market Size, Share, Trends and Forecast by Type, Card Type, Application, End User, and Region, 2026-2034

Oman Gift Cards Market Summary:

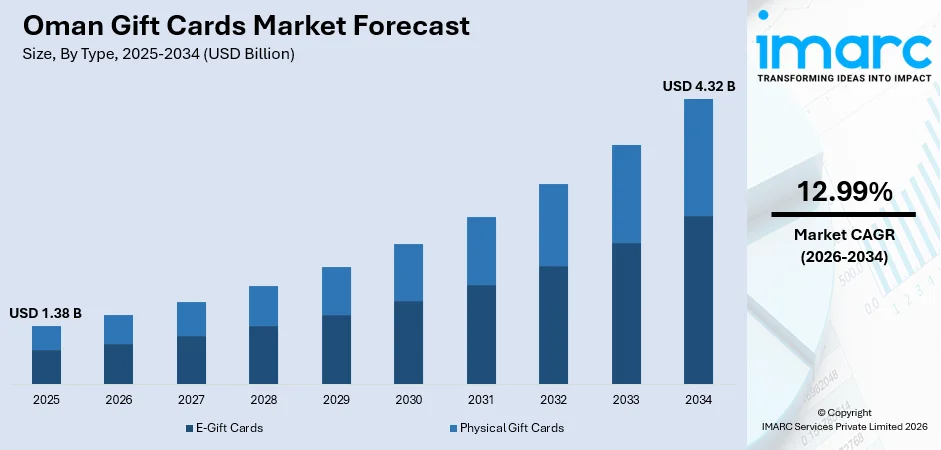

The Oman gift cards market size was valued at USD 1.38 Billion in 2025 and is projected to reach USD 4.32 Billion by 2034, growing at a compound annual growth rate of 12.99% from 2026-2034.

The Oman gift cards market is experiencing robust expansion driven by rapid digital payment adoption, evolving consumer gifting preferences, and increasing retail modernization across the sultanate. Government-led economic diversification initiatives under Oman Vision 2040, coupled with rising smartphone penetration and growing e-commerce activity, are strengthening digital gifting ecosystems. Enhanced merchant participation, expanding loyalty reward programs, and cultural gifting traditions are further propelling market momentum across diverse consumer and corporate segments.

Key Takeaways and Insights:

- By Type: E-gift cards dominate the market with a share of 65% in 2025, driven by rising smartphone adoption, expanding digital payment ecosystems, and consumer preference for instant, contactless gifting solutions across retail and corporate channels in Oman.

- By Card Type: Closed-loop card leads the market with a share of 58% in 2025, owing to strong retailer-specific loyalty programs, targeted promotional campaigns, and partnerships between merchants and payment providers that encourage repeat purchasing behavior.

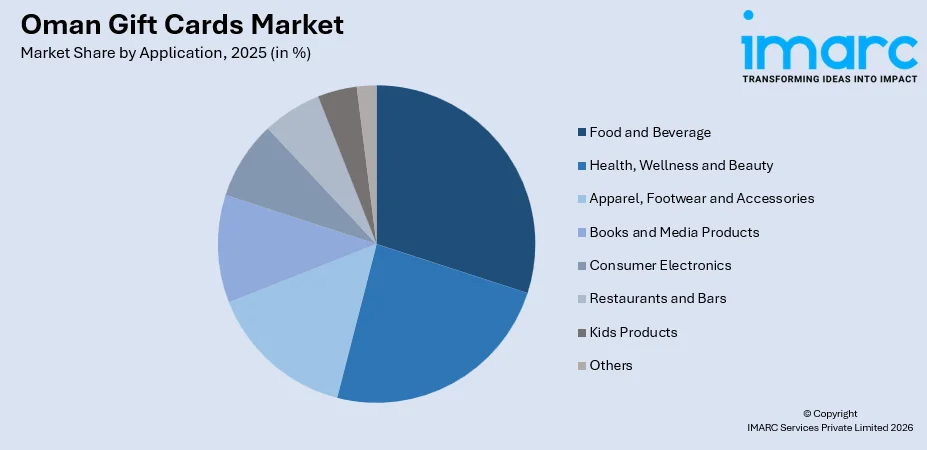

- By Application: Food and beverage holds the largest segment with a market share of 22% in 2025, reflecting Oman’s vibrant dining culture, growing quick-service restaurant presence, and increasing use of gift cards for corporate meal benefits and consumer gifting occasions.

- By End User: Retail exhibits a clear dominance in the market with a share of 70% in 2025, driven by expanding modern retail infrastructure, promotional campaigns by shopping malls, and growing consumer familiarity with gift card products across major urban centers in Oman.

- By Region: Muscat represents the largest region with 45% share in 2025, supported by the concentration of commercial establishments, higher disposable incomes, advanced digital payment infrastructure, and the presence of major shopping destinations in the capital governorate.

- Key Players: Key players drive the Oman gift cards market by expanding digital card platforms, enhancing redemption networks, investing in multi-brand gift card solutions, and forging strategic partnerships with retailers to boost consumer engagement, strengthen brand loyalty, and ensure consistent product availability across diverse distribution channels.

To get more information on this market Request Sample

The Oman gift cards market is advancing steadily as the sultanate embraces digital transformation and modern retail experiences. The government’s Oman Vision 2040 framework, which emphasizes economic diversification and digital innovation, is creating a supportive environment for cashless payment solutions, including gift cards. The growing presence of international and regional retail brands, expanding shopping mall ecosystems, and an increasingly tech-savvy young population are further accelerating demand. Corporate entities are also leveraging gift cards as employee incentives, promotional tools, and client engagement instruments, adding a significant demand layer beyond individual consumers. Cultural gifting traditions during Eid celebrations, National Day festivities, and other occasions continue to sustain strong seasonal demand. Enhanced payment infrastructure, merchant aggregation platforms, and evolving consumer expectations for convenience are collectively shaping the Oman gift cards market share.

Oman Gift Cards Market Trends:

Accelerating shift toward digital and mobile gifting solutions

Oman is witnessing a significant transition toward digital gifting platforms as mobile payment adoption accelerates across the sultanate. The Central Bank of Oman reported that mobile banking transactions increased substantially in 2024, reflecting broader consumer comfort with digital financial services. Retailers and fintech providers are capitalizing on this shift by integrating e-gift card options into mobile wallets and applications. This digital migration is enabling instant delivery, personalized messaging, and seamless redemption experiences, thereby enhancing the Oman gift cards market growth and expanding the addressable consumer base beyond traditional retail settings.

Expansion of loyalty and rewards-based gift card programs

Major retail operators and hospitality brands across Oman are increasingly integrating gift cards into structured loyalty and rewards programs to deepen customer engagement. Shopping destinations in Muscat, including Mall of Oman and Oman Avenues Mall, have expanded their multi-store gift card offerings to attract footfall and incentivize repeat visits. These programs allow consumers to earn and redeem rewards through gift card purchases, creating a cyclical engagement model that strengthens brand affinity and drives incremental spending across participating merchants and service providers.

Growing corporate adoption for employee incentives and client engagement

Corporate gift card utilization is gaining prominence in Oman as businesses seek efficient, scalable, and tax-advantaged methods for employee recognition and client relationship management. Organizations are replacing traditional gift items with branded and multi-brand gift cards that offer recipients greater choice and convenience. The Oman Chamber of Commerce and Industry has noted growing interest among member businesses in digital incentive solutions. This corporate demand channel is introducing bulk purchasing patterns and recurring order cycles that contribute to sustained market volume growth.

Market Outlook 2026-2034:

The Oman gift cards market is positioned for sustained growth as digital payment adoption deepens and retail ecosystems continue to modernize across the sultanate. Government initiatives under Oman Vision 2040 that prioritize financial inclusion and digital commerce are expected to further catalyze the transition from cash-based gifting to electronic gift card solutions. Increasing smartphone penetration, expanding e-commerce platforms, and growing corporate demand for digital incentive solutions are anticipated to drive higher transaction volumes. The proliferation of multi-brand gift card platforms, enhanced merchant acceptance networks, and evolving consumer preferences for convenient, personalized gifting experiences are expected to create a more competitive and dynamic market landscape, supporting robust revenue generation across both retail and corporate segments in the coming years. The market generated a revenue of USD 1.38 Billion in 2025 and is projected to reach a revenue of USD 4.32 Billion by 2034, growing at a compound annual growth rate of 12.99% from 2026-2034.

Oman Gift Cards Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

E-Gift Cards |

65% |

|

Card Type |

Closed-loop Card |

58% |

|

Application |

Food and Beverage |

22% |

|

End User |

Retail |

70% |

|

Region |

Muscat |

45% |

Type Insights:

- E-Gift Cards

- Physical Gift Cards

E-gift cards dominate with a market share of 65% of the total Oman gift cards market in 2025.

The rapid proliferation of smartphone usage and digital payment infrastructure across Oman is propelling e-gift card adoption among consumers and corporate buyers. The expansion of mobile broadband connectivity across the sultanate has created a robust digital ecosystem that supports instant gift card delivery and redemption through diverse online and mobile channels. E-gift cards offer distinct advantages including immediate delivery, personalization options, and integration with mobile wallet platforms, making them the preferred choice for tech-savvy consumers who prioritize convenience and contactless transactions in their gifting activities.

Retailers and hospitality providers are increasingly investing in dedicated e-gift card portals and application-based gifting features to capture the growing digital-first consumer segment. The Central Bank of Oman’s digital payment infrastructure enhancements, including the expansion of the national electronic clearing system in 2024, have streamlined online transactions and boosted consumer confidence in digital gifting. Corporate purchasers are also driving volume through bulk digital gift card orders for employee rewards and promotional campaigns, further reinforcing the segment’s commanding position within the broader Oman gift cards market.

Card Type Insights:

- Closed-loop Card

- Open-loop Card

Closed-loop card leads with a share of 58% of the total Oman gift cards market in 2025.

Closed-loop gift cards remain the dominant card type in Oman's market, driven by their widespread adoption among major retail chains, dining establishments, and entertainment venues that leverage branded cards to foster customer loyalty. The sultanate's retail sector continues to demonstrate strong economic contribution, reflecting a thriving commercial environment where retailer-specific gift cards serve as effective tools for customer retention, repeat purchases, and targeted promotional campaigns across established brand networks.

The preference for closed-loop cards is reinforced by merchants offering exclusive benefits such as bonus credit on purchases, seasonal discounts, and integration with store loyalty programs. Major shopping centers in Muscat and other urban areas have reported increased gift card activation volumes during festive periods including Eid al-Fitr and Eid al-Adha celebrations, which generated elevated retail footfall during 2024 festive seasons. These branded cards provide merchants with valuable consumer spending data while offering recipients a curated shopping experience within trusted retail environments.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Food and Beverage

- Health, Wellness and Beauty

- Apparel, Footwear and Accessories

- Books and Media Products

- Consumer Electronics

- Restaurants and Bars

- Kids Products

- Others

Food and beverage represents the largest segment with a market share of 22% of the total Oman gift cards market in 2025.

Oman's food and beverage sector has emerged as the leading application category for gift cards, reflecting the sultanate's dynamic culinary culture and expanding foodservice industry. The growing number of licensed food establishments across the country underpins a broad merchant base that supports gift card distribution and acceptance across diverse dining formats. Quick-service restaurants, specialty coffee chains, and fine-dining establishments increasingly offer gift card programs that serve both individual consumer gifting needs and corporate meal benefit requirements.

The food and beverage application is further bolstered by the integration of gift cards with food delivery platforms and aggregator applications that have witnessed significant growth in Oman. Consumer spending on dining out rose steadily, supported by Oman's tourism development initiatives that continue to attract a growing number of international visitors to the sultanate. This influx of tourists, combined with domestic demand, creates consistent utilization of food-related gift cards across diverse dining formats and price points throughout the year.

End User Insights:

- Retail

- Corporate

Retail holds the largest share at 70% of the total Oman gift cards market in 2025.

The retail end-user segment commands the dominant position in Oman's gift cards market, supported by the sultanate's expanding modern retail infrastructure and increasing consumer engagement with gift card products. Oman's retail sector has benefited from significant investment in shopping mall development, creating extensive organized retail space across major urban centers. Major retail destinations actively promote gift card programs through in-store displays, digital channels, and seasonal marketing campaigns that align with cultural celebrations and shopping festivals.

Consumer purchasing patterns in Oman indicate strong affinity for gift cards as versatile gifting solutions for personal occasions including birthdays, weddings, and religious festivals. Improving household consumption expenditure across the sultanate reflects enhanced consumer spending capacity that directly supports gift card purchasing activity. Retailers benefit from gift card sales through advance revenue recognition, reduced return rates, and incremental spending when card holders exceed the stored value during redemption transactions.

Regional Insights:

- Muscat

- Al Batinah

- Al-Sharqiyah

- Al-Dakhiliyah

- Dhofar

- Others

Muscat represents the largest region with a 45% share of the total Oman gift cards market in 2025.

Muscat serves as the commercial and economic hub of Oman, concentrating the majority of the sultanate's modern retail establishments, financial institutions, and corporate headquarters that drive gift card distribution and adoption. The governorate represents the largest consumer base in the country, supported by a densely populated urban landscape. Major shopping destinations actively maintain gift card programs that cater to diverse consumer preferences, offering extensive redemption options across retail, dining, and entertainment categories.

The capital's advanced digital infrastructure and higher disposable incomes compared to other governorates position Muscat as the primary market for both physical and electronic gift card products. Growing passenger traffic at Muscat International Airport generates additional demand through duty-free retail gift card offerings and tourist-oriented gifting solutions. The concentration of international brands, hospitality chains, and entertainment venues in Muscat creates a dense merchant acceptance network that reinforces the region's dominant market position.

Market Dynamics:

Growth Drivers:

Why is the Oman Gift Cards Market Growing?

Rapid digital payment adoption and financial technology advancement

Oman’s financial ecosystem is undergoing significant digital transformation as the Central Bank of Oman and commercial banking institutions invest heavily in modernizing payment infrastructure. The sultanate’s electronic payment transactions have witnessed substantial growth, with the Central Bank reporting that point-of-sale terminal transactions exceeded in value during 2024. This expanding digital payment landscape directly supports gift card adoption by ensuring seamless issuance, loading, and redemption experiences across physical and online retail channels. The emergence of fintech platforms and mobile wallet solutions is further accelerating the integration of gift cards into everyday consumer financial activities. Banks and payment service providers are partnering with retailers to embed gift card functionality within mobile banking applications, creating frictionless gifting experiences. These digital innovations are particularly resonant with Oman’s young demographic, as a significant proportion of the population falls below 30 years of age, representing a digitally native consumer cohort that favors electronic gifting solutions over traditional alternatives.

Expanding modern retail infrastructure and shopping culture

Oman’s retail landscape is evolving rapidly with substantial investments in shopping mall development, entertainment destinations, and mixed-use commercial projects that create extensive opportunities for gift card programs. This expanding retail footprint provides merchants with larger platforms to introduce and promote gift card products while offering consumers greater variety in redemption options. The growth of organized retail is complemented by changing consumer shopping habits that increasingly favor experiential and convenience-oriented purchasing approaches. Shopping festivals, seasonal promotions, and cultural celebrations drive peak demand periods for gift cards, with retailers strategically positioning gift card displays and digital promotional campaigns to capture gifting-related spending. The modernization of retail environments across secondary cities is also extending gift card availability beyond Muscat, gradually broadening the geographic reach of gift card programs throughout the sultanate.

Government economic diversification and Oman Vision 2040 initiatives

The Omani government's strategic commitment to economic diversification under the Oman Vision 2040 framework is creating a favorable environment for digital commerce and cashless payment solutions, including gift cards. The vision prioritizes financial inclusion, technology adoption, and private sector growth as key pillars of national development. The Ministry of Transport, Communications and Information Technology has actively promoted digital adoption initiatives, positioning Oman as one of the leading digital economies within the Gulf Cooperation Council region. These government-led initiatives are complemented by regulatory support for electronic payment systems and consumer protection frameworks that build confidence in digital financial products. Tourism development programs, which target increased visitor arrivals and tourism revenue contribution to national GDP, are also generating supplementary demand for gift card products through hospitality, entertainment, and retail channels. The synergy between government policy direction and private sector innovation is establishing a robust foundation for sustained growth in the gift cards market.

Market Restraints:

What Challenges the Oman Gift Cards Market is Facing?

Limited consumer awareness and adoption in non-urban areas

Despite growing momentum in major urban centers, gift card awareness and adoption remain relatively limited in Oman’s rural and semi-urban regions where cash-based transactions continue to prevail. Smaller towns and villages have fewer modern retail establishments capable of supporting gift card programs, resulting in limited merchant acceptance networks. This geographic disparity restricts market expansion potential and creates uneven penetration across governorates, particularly in areas where digital infrastructure development has not yet reached the levels achieved in Muscat and other primary urban centers.

Regulatory and compliance complexities for gift card issuers

Gift card issuers in Oman face evolving regulatory requirements related to stored-value instruments, anti-money laundering compliance, and consumer protection obligations that can increase operational costs and administrative burdens. The need to adhere to Central Bank of Oman guidelines on electronic payment instruments requires ongoing investment in compliance infrastructure, reporting systems, and know-your-customer verification processes. These regulatory complexities may deter smaller merchants and new market entrants from launching gift card programs, potentially limiting product diversity and competitive dynamism within the market.

Competition from alternative digital payment and gifting solutions

The gift cards market faces increasing competition from alternative digital payment methods including peer-to-peer transfer applications, direct mobile wallet credits, and cryptocurrency-based gifting platforms that offer recipients unrestricted spending flexibility. Social media platforms and messaging applications are also introducing embedded gifting features that bypass traditional gift card mechanisms. This competitive pressure from substitutes requires gift card providers to continuously innovate their value propositions, redemption experiences, and merchant networks to maintain relevance and consumer preference in an increasingly crowded digital payments landscape.

Competitive Landscape:

The Oman gift cards market features a competitive landscape characterized by a mix of established banking institutions, retail conglomerates, and specialized fintech providers. Market participants are differentiating through expanded merchant networks, multi-brand card offerings, and enhanced digital platforms that support instant issuance and redemption. Strategic partnerships between financial institutions and retail chains are intensifying as companies seek to capture larger shares of both consumer and corporate gifting segments. Investment in mobile-first solutions, personalized gifting experiences, and data-driven promotional strategies is reshaping competitive dynamics, with players focused on building scalable platforms that deliver seamless cross-channel functionality.

Oman Gift Cards Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Billion |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

E-Gift Cards, Physical Gift Cards |

|

Card Types Covered |

Closed-loop Card, Open-loop Card |

|

Applications Covered |

Food and Beverage, Health, Wellness and Beauty, Apparel, Footwear and Accessories, Books and Media Products, Consumer Electronics, Restaurants and Bars, Kids Products, Others |

|

End Users Covered |

Retail, Corporate |

|

Regions Covered |

Muscat, Al Batinah, Al-Sharqiyah, Al-Dakhiliyah, Dhofar, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Oman Gift Cards Market Report

The Oman gift cards market size was valued at USD 1.38 Billion in 2025.

The Oman gift cards market is expected to grow at a compound annual growth rate of 12.99% from 2026-2034 to reach USD 4.32 Billion by 2034.

E-gift cards dominated the market with a share of 65%, driven by rising smartphone adoption, expanding digital payment infrastructure, and growing consumer preference for instant, contactless gifting solutions across retail and corporate channels in Oman.

Key factors driving the Oman gift cards market include rapid digital payment adoption, expanding modern retail infrastructure, government economic diversification initiatives, growing corporate gifting demand, cultural celebration-driven purchasing patterns, and increasing fintech innovation.

Major challenges include limited consumer awareness in non-urban areas, regulatory and compliance complexities for gift card issuers, competition from alternative digital payment solutions, uneven merchant acceptance networks, and the need for continuous platform innovation to retain consumer engagement.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)