Oman Healthcare IT Market Size, Share, Trends and Forecast by Product and Services, Component, Delivery Mode, End User, and Region, 2026-2034

Oman Healthcare IT Market Summary:

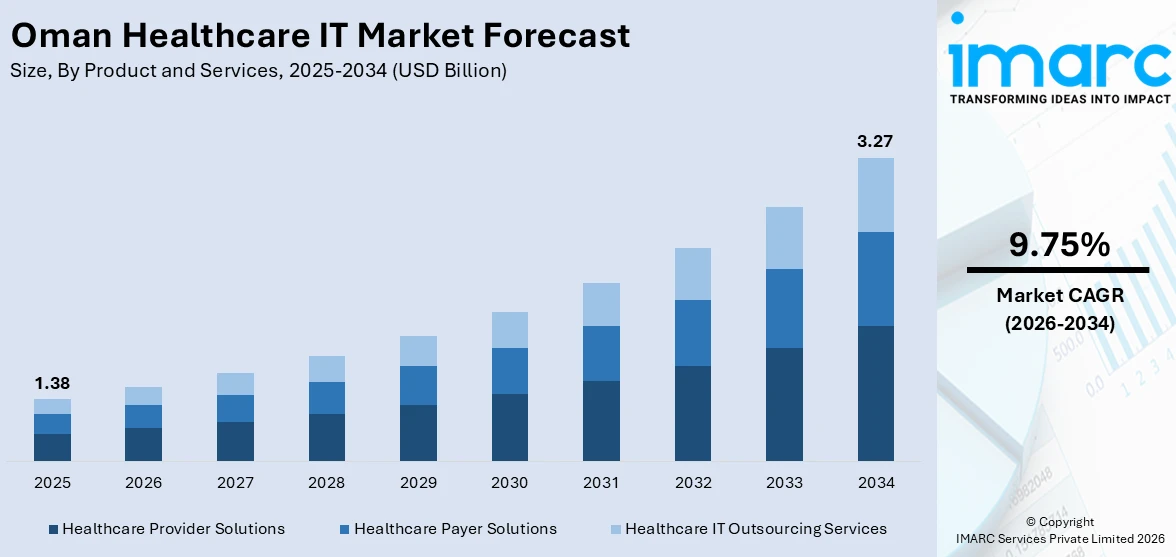

The Oman healthcare IT market size was valued at USD 1.38 Billion in 2025 and is projected to reach USD 3.27 Billion by 2034, growing at a compound annual growth rate of 9.75% from 2026-2034.

The Oman healthcare IT market is experiencing robust expansion driven by the government’s commitment to digital transformation under Oman Vision 2040, which prioritizes establishing a leading healthcare system with international standards. The National Digital Health Strategy (2024–2030) is accelerating the adoption of electronic health records, telemedicine platforms, and artificial intelligence-powered clinical tools across public and private healthcare facilities. Rising demand for cloud-based healthcare solutions, interoperable health information systems, and data-driven clinical decision-making is reshaping how healthcare services are delivered throughout the Sultanate. Oman’s digital health information system, which now supports over 85% of healthcare institutions, serves as the digital backbone enabling unified patient records and streamlined clinical workflows. Expanding hospital construction, growing private sector participation, and increasing healthcare insurance coverage through platforms like Dhamani are creating strong demand for integrated IT solutions. Furthermore, government investments in cybersecurity frameworks, workforce upskilling, and public-private partnerships are strengthening the foundation for sustainable healthcare digitization, positioning Oman as a regional hub for healthcare innovation and reinforcing the Oman healthcare IT market share.

Key Takeaways and Insights:

- By Product and Services: Healthcare provider solutions dominate the market with a share of 64.2% in 2025, driven by the expanding deployment of clinical information systems, electronic health records, and nonclinical administrative platforms across Oman’s public and private healthcare facilities.

- By Component: Software leads the market with a share of 49.6% in 2025, owing to rising investments in electronic health record platforms, clinical decision support systems, and health information exchange software that enhance operational efficiency and care coordination.

- By Delivery Mode: Cloud-based represents the largest segment with a market share of 56.3% in 2025, reflecting growing preference for scalable, cost-effective infrastructure that enables remote accessibility, seamless data integration, and rapid deployment across healthcare networks.

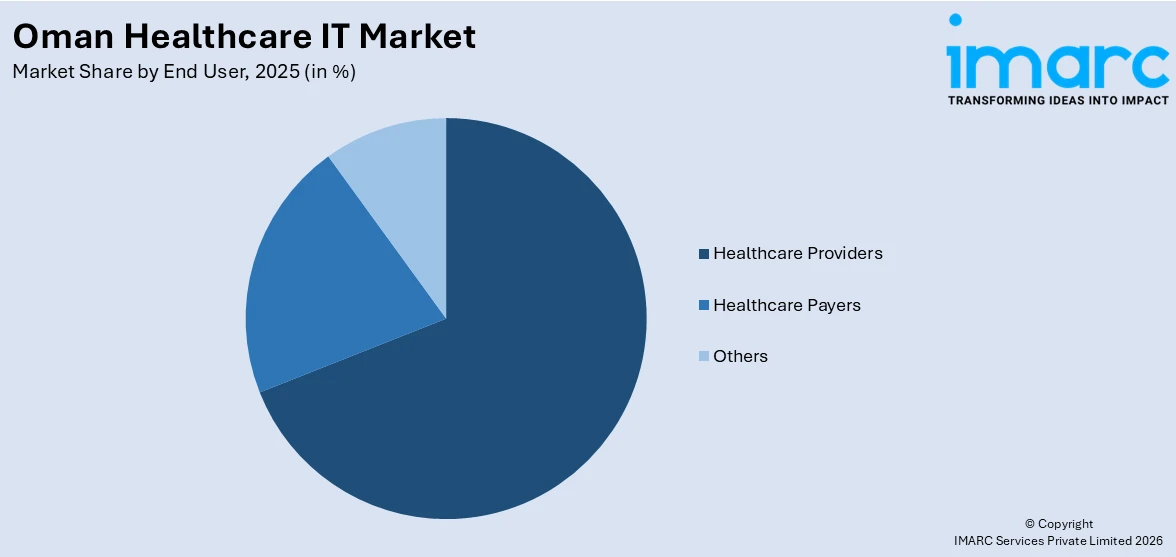

- By End User: Healthcare providers hold the biggest share at 68.8% in 2025, as hospitals, ambulatory care centers, and diagnostic facilities accelerate digital adoption to improve patient outcomes, streamline clinical workflows, and comply with regulatory mandates.

- By Region: Muscat is the largest region with 43.5% share in 2025, driven by its concentration of major hospitals, advanced healthcare infrastructure, technology companies, and government-backed digital health initiatives centered in the capital.

- Key Players: By enhancing cybersecurity capabilities, increasing cloud-based service offerings, investing in cutting-edge clinical software platforms, and establishing strategic alliances with healthcare organizations to speed up digital transformation and enhance care delivery, major players are influencing the Oman healthcare IT market.

To get more information on this market Request Sample

The Oman healthcare IT market is gaining strong momentum as the Sultanate pursues comprehensive healthcare modernization under its national development agenda. Increasing adoption of artificial intelligence in medical diagnostics, the expansion of telemedicine services to underserved governorates, and the growing integration of health information systems are collectively transforming the country's healthcare delivery landscape. Government-led initiatives promoting digital health platforms, cloud-based clinical solutions, and interoperable electronic records are strengthening care coordination across public and private institutions. Rising investments in cybersecurity frameworks and workforce upskilling are further reinforcing the foundation for sustainable healthcare digitization throughout the Sultanate. Public-private partnerships are enabling the digitization of insurance claims processing, with the Dhamani national health insurance platform processing nearly three Million transactions during the first quarter of 2025 after integrating with 33 private hospitals. Growing investments in cloud infrastructure, data analytics, and interoperable health record systems are enabling healthcare providers to deliver more efficient and personalized care. The convergence of regulatory support, technological innovation, and rising healthcare expenditure is strengthening the foundation for sustained market expansion across all segments of the Oman healthcare IT ecosystem.

Oman Healthcare IT Market Trends:

Accelerated Integration of Artificial Intelligence in Clinical Care

Artificial intelligence is rapidly transforming clinical workflows across Oman’s healthcare system, enabling more accurate diagnostics, personalized treatment planning, and efficient resource utilization. Healthcare providers are deploying AI-powered tools for medical imaging analysis, pathology interpretation, and predictive patient monitoring. The Ministry of Health is piloting AI-driven patient monitoring systems alongside digital health portals and mobile applications for appointment bookings and e-prescriptions, reflecting a systemic shift toward intelligent healthcare delivery that enhances both clinical outcomes and operational efficiency across the Sultanate’s healthcare institutions.

Expansion of Telemedicine and Virtual Care Platforms

Telemedicine adoption is accelerating as Oman seeks to overcome geographical barriers and improve healthcare accessibility in remote governorates. Virtual consultation platforms, remote patient monitoring, and structured home visit programs are expanding healthcare reach beyond urban centers. Healthcare institutions are increasingly leveraging AI-powered telehealth tools to enable real-time clinical assessments, streamline physician workflows, and reduce unnecessary hospital visits. The growing integration of telemedicine with electronic health records and cloud-based infrastructure is creating seamless care pathways that connect patients in underserved regions with specialist expertise, supporting the Oman healthcare IT market growth.

Digital Transformation of Health Insurance Ecosystems

Oman is witnessing a fundamental shift toward digital health insurance management through integrated technology platforms that connect healthcare providers, insurance companies, and regulators. These platforms streamline eligibility verification, preauthorization workflows, and claims processing while establishing unified electronic medical records across participating institutions. The transition from paper-based transactions to automated digital systems is enhancing transparency, reducing fraudulent claims, and accelerating settlement timelines. Growing regulatory emphasis on electronic integration within the insurance sector is driving widespread adoption of interoperable platforms that strengthen governance, improve service delivery quality, and promote broader insurance coverage across the Sultanate.

Market Outlook 2026-2034:

The Oman healthcare IT market is poised for sustained expansion as the country’s healthcare system undergoes comprehensive digital transformation aligned with Oman Vision 2040 objectives. Increasing government investments in smart hospital infrastructure, interoperable health information systems, and AI-enabled clinical platforms are expected to accelerate technology adoption across public and private healthcare networks. The market generated a revenue of USD 1.38 Billion in 2025 and is projected to reach a revenue of USD 3.27 Billion by 2034, growing at a compound annual growth rate of 9.75% from 2026-2034. The ongoing construction of nine new hospitals with over 1,660 beds will generate substantial demand for healthcare IT solutions, while the expansion of cloud computing, telehealth services, and digital insurance platforms will further propel market growth. Rising healthcare expenditure, growing private sector participation, and strengthening regulatory frameworks for health data governance are reinforcing long-term market opportunities across the Sultanate.

Oman Healthcare IT Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product and Services |

Healthcare Provider Solutions |

64.2% |

|

Component |

Software |

49.6% |

|

Delivery Mode |

Cloud-Based |

56.3% |

|

End User |

Healthcare Providers |

68.8% |

|

Region |

Muscat |

43.5% |

Product and Services Insights:

- Healthcare Provider Solutions

- Clinical Solutions

- Nonclinical Healthcare IT Solutions

- Healthcare Payer Solutions

- Pharmacy Audit and Analysis Systems

- Claims Management Solutions

- Analytics and Fraud Management Solutions

- Member Eligibility Management Solutions

- Provider Network Management Solutions

- Billing and Accounts (Payment) Management Solutions

- Customer Relationship Management Solutions

- Population Health Management Solutions

- Others

- Healthcare IT Outsourcing Services

- Provider HCIT Outsourcing Services Market

- Payer IT Outsourcing Services

- Operational IT Outsourcing Services

Healthcare provider solutions dominate with a market share of 64.2% of the total Oman healthcare IT market in 2025.

Healthcare provider solutions command the largest share of the Oman healthcare IT market, driven by the widespread deployment of clinical information systems, electronic health record platforms, and nonclinical administrative tools across the country's healthcare network. Public and private healthcare institutions are increasingly adopting integrated digital platforms that enable unified patient records, streamlined appointment scheduling, and coordinated laboratory services. The growing emphasis on interoperability and data-driven clinical workflows is accelerating the adoption of comprehensive provider-focused IT solutions throughout the Sultanate's expanding healthcare system.

The segment's dominance is further reinforced by the ongoing expansion of hospital infrastructure and the corresponding demand for advanced healthcare IT systems to support clinical operations. The government's national digital health strategy emphasizes leveraging emerging technologies, including virtual medicine, artificial intelligence, and big data analytics, to enhance diagnostic accuracy, improve care coordination, and optimize resource allocation. Rising investments in telemedicine capabilities and AI-powered patient monitoring systems are broadening the scope of provider solutions beyond traditional clinical settings into community and home-based care environments.

Component Insights:

- Software

- Hardware

- Services

Software leads with a share of 49.6% of the total Oman healthcare IT market in 2025.

Software solutions account for the largest share within the component segment, reflecting the healthcare sector's growing reliance on digital platforms for clinical management, data analytics, and administrative optimization. Electronic health record systems, clinical decision support tools, health information exchange platforms, and revenue cycle management software are being widely adopted by healthcare providers to enhance operational efficiency and patient care quality. The development of nationally integrated digital healthcare platforms offering services including medical reports, medication tracking, virtual appointments, and patient engagement features is further strengthening software demand across the Sultanate.

The software segment is further strengthened by the growing adoption of specialized applications for healthcare payer operations, population health management, and analytics-driven fraud detection. Oman's evolving regulatory environment is driving software adoption, with national health policies requiring healthcare facilities to implement standardized electronic health record systems across public and private hospitals, including compliance mandates for data interoperability and periodic institutional audits. These regulatory requirements are creating sustained demand for scalable, standards-compliant software solutions that support seamless information exchange across healthcare networks.

Delivery Mode Insights:

- On-Premise

- Cloud-Based

Cloud-based exhibits a clear dominance with a 56.3% share of the total Oman healthcare IT market in 2025.

Cloud-based delivery solutions hold the largest share within this segment, driven by healthcare providers' preference for scalable, flexible, and cost-effective IT infrastructure that supports real-time data access and remote collaboration. Cloud platforms enable seamless integration of electronic health records, telemedicine services, and analytics tools without requiring significant upfront capital investments in on-premise hardware. The national digital health strategy includes achieving full cloud transformation as a key strategic objective, reflecting the government's commitment to cloud-first healthcare IT deployment across the country's public and private healthcare institutions.

The growing cloud infrastructure ecosystem in Oman is further supporting adoption, with data center investments expanding to meet increasing demand across healthcare and other sectors. Strategic government partnerships with leading global cloud service providers are strengthening the foundation for cloud-based healthcare solutions and enabling faster deployment of digital health platforms. The hybrid cloud model, combining public cloud services with on-premise data centers, is increasingly being adopted by healthcare institutions to balance scalability requirements with data sovereignty, security compliance, and operational resilience across distributed healthcare networks.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Healthcare Providers

- Hospitals

- Ambulatory Care Centers

- Home Healthcare Agencies, Nursing Homes and Assisted Living Facilities

- Diagnostic and Imaging Centers

- Pharmacies

- Healthcare Payers

- Private Payers

- Public Payers

- Others

Healthcare providers represent the leading segment with a 68.8% share of the total Oman healthcare IT market in 2025.

Healthcare providers constitute the largest end-user segment, driven by hospitals, ambulatory care centers, and diagnostic facilities investing heavily in IT solutions to modernize clinical operations and improve patient outcomes. The government's ongoing expansion of hospital infrastructure across multiple governorates, including the construction of new facilities and the upgrading of existing primary healthcare institutions, is generating significant demand for integrated healthcare IT systems encompassing electronic health records, clinical decision support platforms, cloud-based data management, and telemedicine capabilities to equip modern, technology-enabled healthcare facilities.

Healthcare providers are increasingly deploying AI-assisted diagnostic systems, digital health portals, and mobile applications to streamline operations, reduce administrative burdens, and enhance patient engagement. The growing adoption of telemedicine platforms is enabling providers to extend care delivery to remote and underserved areas, improving healthcare accessibility and resource utilization. The segment's dominance is reinforced by regulatory mandates requiring digital health systems implementation across healthcare facilities, combined with rising healthcare expenditure, increasing private sector participation, and the ongoing development of a digitally skilled healthcare workforce throughout the Sultanate.

Regional Insights:

- Muscat

- Al Batinah

- Al-Sharqiyah

- Al-Dakhiliyah

- Dhofar

- Others

Muscat holds the largest share with 43.5% of the total Oman healthcare IT market in 2025.

Muscat dominates the regional landscape as the capital and primary hub for healthcare services, technology companies, and government digital health initiatives. The concentration of major public and private hospitals, research institutions, and international healthcare companies in Muscat creates a robust ecosystem for healthcare IT adoption. Leading tertiary care facilities and specialized medical centers headquartered in the capital drive demand for advanced clinical software, cloud infrastructure, telemedicine platforms, and AI-powered diagnostic solutions across the governorate.

The region's dominance is further reinforced by its role as the administrative center for national digital health strategy implementation, where key government bodies overseeing healthcare modernization and regulatory compliance are based. Muscat's advanced telecommunications infrastructure and connectivity networks provide the foundational support required for deploying cloud-based health information systems and real-time data exchange platforms. The presence of technology vendors, system integrators, and digital health startups in the capital fosters innovation and accelerates the commercialization of healthcare IT solutions. Growing public-private partnerships, rising healthcare insurance penetration, and expanding ambulatory care networks within Muscat are further strengthening demand for integrated digital health platforms that enhance care coordination, operational efficiency, and patient engagement across the governorate's healthcare institutions.

Market Dynamics:

Growth Drivers:

Why is the Oman Healthcare IT Market Growing?

Government-Led Digital Health Transformation Initiatives

The government's strategic commitment to healthcare digitization under Oman Vision 2040 serves as a primary catalyst for healthcare IT market growth. The national digital health strategy establishes a comprehensive framework for integrating artificial intelligence, telehealth, and data interoperability across the healthcare system, aligning with international best practices for sustainable health system digitization. This strategy emphasizes governance, IT infrastructure development, and workforce capacity building as foundational pillars for long-term digital health transformation. The Ministry of Health has been proactive in launching digital health portals, mobile applications for appointment bookings and e-prescriptions, and piloting AI-driven patient monitoring systems across public healthcare institutions. Strategic projects under this initiative include developing a visual and digital identity for health institutions, establishing entities that offer innovative digital health solutions, and advancing full cloud transformation across the public healthcare network. The regulatory environment is also evolving to support digital adoption, with national health policies mandating the implementation of standardized electronic health record systems and interoperability compliance across public and private healthcare facilities. These government-led efforts are creating a structured roadmap for technology adoption that drives sustained demand for healthcare IT solutions across the Sultanate.

Expansion of Healthcare Infrastructure and Hospital Construction

Oman's accelerating investments in healthcare infrastructure are generating substantial demand for integrated healthcare IT systems to equip new and expanded facilities. The Ministry of Health is currently overseeing the construction of multiple new hospitals across various governorates, alongside the expansion of referral hospitals and primary healthcare institutions to meet the needs of a growing population. These projects span diverse regions including Dhofar, Al Batinah, Al-Sharqiyah, Musandam, and Al-Dakhiliyah, ensuring healthcare development extends beyond the capital into underserved areas. Each new facility requires comprehensive healthcare IT infrastructure, including electronic health record systems, clinical decision support platforms, cloud-based data management systems, and telemedicine capabilities to enable modern, digitally connected care delivery. The upgrading of existing health centers into full-fledged hospitals further amplifies demand for scalable IT solutions that support expanded clinical operations, increased patient volumes, and enhanced specialty services. Additionally, the growing private sector participation in hospital development is contributing to rising demand for advanced health information systems, diagnostic imaging software, and integrated billing and administrative platforms. This sustained infrastructure expansion ensures consistent demand for healthcare IT solutions as the Sultanate builds technology-enabled healthcare facilities across all governorates.

Rising Adoption of AI-Powered Clinical Technologies

The increasing integration of artificial intelligence technologies into Oman's healthcare delivery system is significantly driving demand for advanced healthcare IT solutions. Healthcare providers are deploying AI-powered tools for medical imaging analysis, predictive diagnostics, and automated clinical workflows to enhance accuracy and reduce operational costs. The government has demonstrated strong commitment to leveraging AI for preventive healthcare at scale, with national initiatives focused on deploying AI-driven screening capabilities across healthcare institutions for early detection of chronic conditions including diabetic complications and cardiovascular diseases. These programs reflect a broader strategic vision to embed intelligent technologies within routine clinical practice across the Sultanate's public health network. The convergence of AI with electronic health records, telemedicine platforms, and population health management systems is creating integrated digital ecosystems that improve clinical decision-making, optimize resource allocation, and enable personalized patient care. Healthcare institutions are increasingly investing in AI-compatible IT infrastructure, data analytics platforms, and machine learning-enabled diagnostic tools that support evidence-based treatment planning and outcomes monitoring. The growing emphasis on precision medicine and proactive health management is further accelerating the adoption of intelligent healthcare solutions across the Sultanate.

Market Restraints:

What Challenges the Oman Healthcare IT Market is Facing?

Interoperability and System Integration Challenges

The lack of standardized interoperability frameworks across Oman’s healthcare IT ecosystem remains a significant barrier to seamless data exchange between public and private healthcare institutions. Different hospitals and health centers often operate on varying system versions, creating data silos that hinder comprehensive patient record sharing and care coordination. Over 40% of healthcare institutions lack formal digital health governance structures, complicating efforts to establish unified data standards and integration protocols that are essential for achieving a fully connected healthcare information network.

Cybersecurity and Data Privacy Vulnerabilities

Growing digital health adoption exposes healthcare institutions to escalating cybersecurity risks, with ransomware attacks targeting the healthcare sector surging significantly in recent years. More than half of Oman’s healthcare institutions have not fully implemented cybersecurity protocols, and approximately half lack patient data encryption. These vulnerabilities threaten patient data confidentiality, erode public trust in digital health systems, and create compliance risks that may slow technology adoption among healthcare providers and payers across the Sultanate.

Limited Digital Health Workforce and Skills Gap

The shortage of trained health informatics professionals and limited digital literacy among healthcare workers present persistent challenges to effective healthcare IT implementation. The transition from traditional workflows to digital systems requires substantial investment in training programs and change management initiatives. Resistance to technology adoption among healthcare staff, combined with insufficient specialized IT personnel to manage, maintain, and optimize complex health information systems, can delay implementation timelines and reduce the effectiveness of digital health solutions across healthcare institutions.

Competitive Landscape:

The Oman healthcare IT market is characterized by an evolving competitive landscape where both international technology providers and regional players compete to deliver integrated digital health solutions. Market participants are focusing on expanding product portfolios encompassing clinical software, cloud infrastructure, AI-powered diagnostics, and health information exchange platforms to meet the growing demands of healthcare modernization. Competition is intensified by increasing government requirements for interoperable health systems, data security compliance, and advanced analytics capabilities. Strategic partnerships between technology vendors and healthcare institutions are enabling faster deployment of innovative solutions, while investments in localized service delivery and workforce training are strengthening market positioning. Companies are also targeting emerging opportunities in telemedicine, health insurance digitization, and smart hospital technologies to capture market share.

Oman Healthcare IT Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Products and Services Covered |

|

|

Components Covered |

Software, Hardware, Services |

|

Delivery Modes Covered |

On-Premise, Cloud-Based |

|

End Users Covered |

|

|

Regions Covered |

Muscat, Al Batinah, Al-Sharqiyah, Al-Dakhiliyah, Dhofar, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Oman Healthcare IT Market Report

The Oman healthcare IT market size was valued at USD 1.38 Billion in 2025.

The Oman healthcare IT market is expected to grow at a compound annual growth rate of 9.75% from 2026-2034 to reach USD 3.27 Billion by 2034.

Healthcare provider solutions dominated the market with a share of 64.2%, driven by the widespread deployment of clinical information systems, electronic health records, and nonclinical administrative platforms across public and private healthcare facilities.

Key factors driving the Oman healthcare IT market include government-led digital health transformation under Vision 2040, expanding hospital infrastructure, rising AI adoption in clinical care, growing cloud computing investments, and increasing health insurance digitization.

Major challenges include interoperability and system integration barriers across healthcare institutions, cybersecurity vulnerabilities and incomplete data encryption protocols, limited digital health workforce, resistance to technology adoption, and the need for stronger governance frameworks.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)