Oman Packaging Market Size, Share, Trends and Forecast by Material, Product Type, Packaging Type, End-Use Industry, and Region, 2026-2034

Oman Packaging Market Summary:

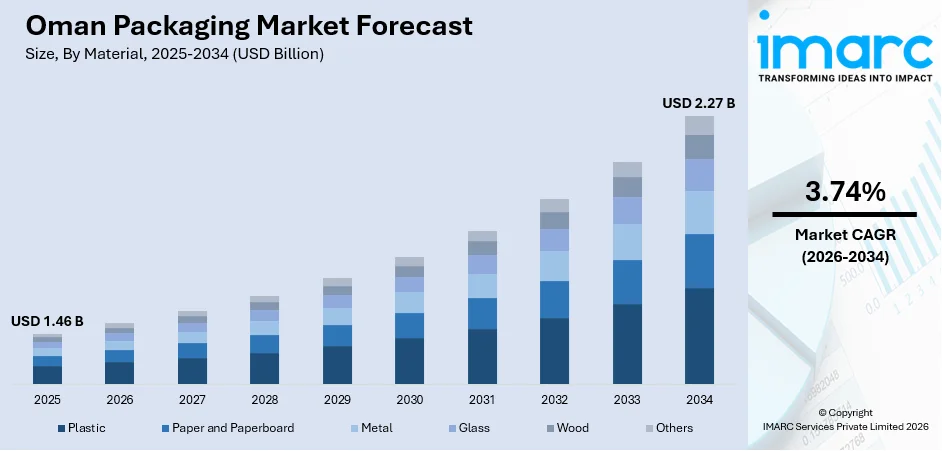

The Oman packaging market size was valued at USD 1.46 Billion in 2025 and is projected to reach USD 2.27 Billion by 2034, growing at a compound annual growth rate of 3.74% from 2026-2034.

The market is advancing steadily as the country accelerates its economic diversification efforts and expands its manufacturing and food processing sectors. Rising consumer demand for packaged goods, growing retail and e-commerce activities, and increased government focus on sustainable packaging practices are strengthening demand across all material and product segments. The ongoing development of industrial free zones, downstream polymer manufacturing capabilities, and upgraded port and logistics infrastructure is reshaping the supply landscape, positioning the Sultanate as a competitive packaging hub within the broader GCC region, thereby expanding the Oman packaging market share.

Key Takeaways and Insights:

- By Material: Plastic dominates the market with a share of 41.6% in 2025, driven by its versatility, cost-effectiveness, and widespread application across food, beverage, pharmaceutical, and consumer product packaging throughout the Sultanate.

- By Product Type: Rigid packaging leads the market with a 55.2% share in 2025, supported by strong demand for durable containers, bottles, jars, and trays used extensively in food preservation, industrial storage, and pharmaceutical distribution.

- By Packaging Type: Primary packaging holds the largest share at 49.8% in 2025, reflecting its essential role in direct product contact, protection, and consumer-facing presentation across all major end use industries in Oman.

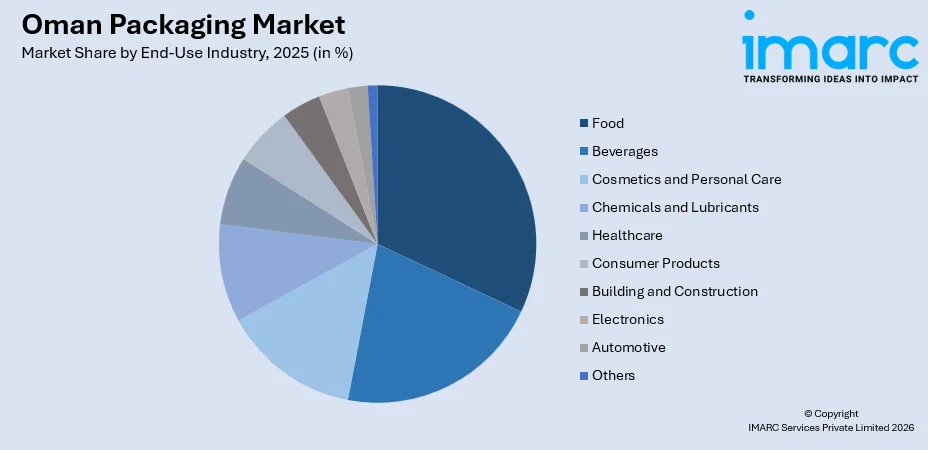

- By End-Use Industry: Food accounts for the highest revenue share of 32.9% in 2025, underpinned by growing consumer spending, rising population, and increasing emphasis on food safety and shelf-life extension across the country.

- By Region: Muscat is the largest regional market with a 40.5% share in 2025, owing to its position as the commercial, industrial, and logistics hub of Oman with the highest concentration of manufacturing and distribution activities.

- Key Players: The Oman packaging market features a competitive mix of domestic manufacturers and international suppliers, with companies focusing on product diversification, sustainable material innovation, and capacity expansion to capture growing demand across industrial and consumer segments.

To get more information on this market Request Sample

Oman packaging market is witnessing a steady growth rate due to the economic diversification initiatives undertaken by the government in Oman, development in manufacturing activities, and increasing demand for packaged products in food, beverages, pharmaceuticals, and personal care. The Oman government is focusing on investing in non-petrochemical sectors, such as food processing and downstream petrochemical manufacturing, as part of their Oman Vision 2040 plan. These sectors are directly adding to the demand for packaging. In addition, development in industrial infrastructure is adding to Oman’s manufacturing capabilities. For example, a total of USD 220 million in investments has been committed to the Ladayn Polymer Park in Sohar Industrial City, Oman, out of 26 total commitments as of October 2025. The industrial park is involved in the development of advanced packaging materials, healthcare products, and specialty polymers. All these factors are adding to a positive outlook for Oman packaging market growth.

Oman Packaging Market Trends:

Rising Adoption of Sustainable and Eco-Friendly Packaging

Oman is at a critical juncture in its journey to sustainable packaging solutions, where regulatory and consumer trends are increasingly in sync with sustainable and environmentally friendly options. The country’s regulatory environment is pushing forward sustainable packaging options through Ministerial Decision No. 8/2024, which outlines a phased ban on single-use plastic shopping bags, starting from July 2024 in the healthcare sector, followed by the retail and textile industries in January 2025, and then food retail and bakeries in July 2025, with a total ban by 2027.

Growth of E-Commerce and Last-Mile Delivery Packaging

The rapid growth in e-commerce and online food delivery services in Oman is creating significant demand for secondary and tertiary packaging solutions. The shift to home delivery is changing packaging demand, with corrugated boxes, cushioning materials, and temperature-controlled packaging increasingly being used. In the wider GCC, last-mile corrugated packaging was catapulted to become one of the major percentages of box production in each country in 2025, up, as the shift in packaging demand accelerates in response to digital commerce and modernized logistics services.

Expansion of Downstream Polymer and Plastics Manufacturing

Oman is in the process of rapidly developing its domestic conversion capacity in the field of plastics through the launch of industrial initiatives in the country. The Ladayn Polymer Park, a joint venture between the OQ Group and Madayn in the Sohar Industrial City, has received 26 investment commitments totaling 220 million dollars as of October 2025, out of which 10 agreements have been signed in 2025 itself. The Ladayn Polymer Park is attracting international investors from Germany, Italy, India, China, Turkey, and Egypt in the field of packaging, healthcare, and automotive applications of polymers.

Market Outlook 2026-2034:

The Oman packaging market is poised for steady expansion over the forecast period, supported by ongoing economic diversification, growing industrial output, and rising consumer demand for packaged goods. The country’s strategic investments in polymer manufacturing infrastructure, expanding food and beverage sector, and strengthening logistics networks are expected to drive sustained demand across all packaging segments. The market generated a revenue of USD 1.46 Billion in 2025 and is projected to reach a revenue of USD 2.27 Billion by 2034, growing at a compound annual growth rate of 3.74% from 2026-2034. Regulatory initiatives promoting sustainable packaging practices and the phased elimination of single-use plastics will continue to accelerate innovation in biodegradable and recyclable materials, creating new growth opportunities.

Oman Packaging Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Material |

Plastic |

41.6% |

|

Product Type |

Rigid Packaging |

55.2% |

|

Packaging Type |

Primary Packaging |

49.8% |

|

End-Use Industry |

Food |

32.9% |

|

Region |

Muscat |

40.5% |

Material Insights:

- Plastic

- Paper and Paperboard

- Metal

- Glass

- Wood

- Others

Plastic leads the Oman packaging market with a 41.6% share of the total market in 2025.

Plastic packaging maintains its dominant position in Oman owing to its adaptability across a wide spectrum of applications, ranging from food and beverage containers to pharmaceutical blister packs and industrial wrapping. The material’s lightweight properties, barrier performance, and cost efficiency make it the preferred choice for manufacturers seeking to balance product protection with logistics optimization. The country’s expanding downstream petrochemical sector is further strengthening plastic packaging supply, with the Ladayn Polymer Park in Sohar attracting global investment to localize advanced plastic conversion capabilities.

Oman’s integrated petrochemical infrastructure provides domestic converters with competitive access to polymer resins produced at OQ’s Liwa Plastics Industry Complex. The Madayn Plastic Company (MAPCO), the first Omani manufacturer of Form Fill Seal bags, commenced production at the Ladayn Polymer Park in Q1 2025 with an investment of USD 8 million, signaling a shift toward local self-sufficiency in specialty plastic packaging. This growing domestic manufacturing base, combined with consistent demand from food processing and consumer goods sectors, ensures that plastic remains the cornerstone of the Oman packaging market.

Product Type Insights:

- Rigid Packaging

- Boxes and Containers

- Bottles and Jars

- Pails and Cans

- Trays and Pallets

- Caps and Closures

- Tubes

- Others

- Flexible Packaging

- Bags and Sacks

- Films and Wraps

- Labels

- Sachets and Pouches

- Tapes

- Others

Rigid packaging dominates the Oman packaging market with a 55.2% share of the total market in 2025.

Rigid packaging holds the largest position within Oman’s packaging landscape, driven by strong demand from food and beverage, pharmaceutical, and industrial sectors that prioritize structural integrity and product safety. Containers, bottles, jars, trays, and cans remain indispensable for preserving perishable goods, meeting regulatory compliance, and ensuring safe storage and transportation. The format’s superior barrier properties and tamper-evident capabilities make it particularly well-suited for Oman’s growing processed food and healthcare industries.

The continued expansion of industrial infrastructure across Oman is reinforcing rigid packaging demand. Manufacturing output grew in 2024, with food processing, chemicals, and construction materials driving significant packaging requirements. The development of economic zones, including Sohar, Duqm, and Salalah, has enabled the establishment of specialized production facilities that require high-performance rigid packaging for both domestic distribution and export markets, sustaining the segment’s dominant share.

Packaging Type Insights:

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

Primary packaging accounts for the highest revenue with a 49.8% share of the total Oman packaging market in 2025.

Primary packaging commands the largest segment share in Oman, reflecting its critical role as the first layer of protection that directly contacts and preserves the product. In the food and beverage sector, which represents the largest end use industry, primary packaging ensures freshness, extends shelf life, and complies with health and safety regulations. Consumer goods, pharmaceutical products, and personal care items similarly depend on primary packaging for product integrity and brand presentation.

The growing emphasis on food safety standards and heightened consumer awareness of hygiene following global health trends have intensified demand for tamper-evident, antimicrobial, and barrier-enhanced primary packaging solutions. Additionally, Oman’s expanding retail landscape, coupled with rising household consumption and urbanization, is driving manufacturers to invest in innovative primary packaging formats that combine functionality with visual appeal and sustainability.

End-Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Food

- Dairy Products

- Meat, Poultry, and Seafood

- Agricultural Produce

- Others

- Beverages

- Alcoholic Beverages

- Non-alcoholic Beverages

- Cosmetics and Personal Care

- Skin Care

- Hair Care

- Others

- Chemicals and Lubricants

- Healthcare

- Pharmaceuticals

- Medical Devices

- Others

- Consumer Products

- Building and Construction

- Electronics

- Automotive

- Others

Food is the largest end use segment, holding a 32.9% share of the total Oman packaging market in 2025.

The food industry represents the primary demand driver for packaging in Oman, driven by a growing population, rising consumer spending on processed and packaged foods, and increasing attention to food safety and quality preservation. The expanding domestic food processing sector, supported by government initiatives to enhance food security under Oman Vision 2040, is generating sustained demand for both rigid and flexible packaging formats across dairy, meat, seafood, and agricultural produce categories.

Oman’s food security initiatives include projects such as the Safailah Farming Project in Mirbat with a capacity of 600 tonnes annually, natural shrimp farming projects producing 4,000 tonnes per year, and wheat production from Najd farms with a capacity of 10,000 tonnes. These expanding agricultural and aquaculture operations are creating substantial demand for packaging solutions that ensure product freshness, safe transportation, and extended shelf life across domestic and export markets.

Regional Insights:

- Muscat

- Al Batinah

- Al-Sharqiyah

- Al-Dakhiliyah

- Dhofar

- Others

Muscat holds the largest regional share at 40.5% of the total Oman packaging market in 2025.

Muscat dominates the Oman packaging market owing to its position as the country’s economic, administrative, and commercial capital with the highest concentration of manufacturing facilities, distribution networks, and consumer markets. The governorate hosts major packaging manufacturers, including Omani Packaging Company SAOG in Rusayl Industrial Estate, and serves as the primary hub for food processing, retail, and logistics operations that drive packaging consumption across all material types and product categories.

The capital region benefits from its proximity to Muscat International Airport and well-developed road infrastructure connecting it to major industrial cities and ports. Ongoing urban development projects, including the Al Khuwair Downtown development spanning approximately 3.6 million square meters, are further expanding commercial and retail activity, intensifying demand for consumer and industrial packaging solutions and reinforcing Muscat’s leading position in the national packaging market.

Market Dynamics:

Growth Drivers:

Why is the Oman Packaging Market Growing?

Economic Diversification and Industrial Expansion Under Oman Vision 2040

Oman’s strategic push to diversify its economy away from oil dependence is generating substantial growth in the packaging market. The Oman Vision 2040 framework prioritizes manufacturing, food processing, logistics, and petrochemical industries as key pillars of economic transformation, each of which directly increases packaging demand. The non-oil sector has demonstrated consistent expansion, with construction, manufacturing, and services sectors leading the growth trajectory. The development of dedicated economic zones, industrial parks, and free trade corridors is attracting both domestic and foreign investment into packaging-intensive sectors, creating a multiplier effect on the overall packaging ecosystem. In 2025, The Public Authority for Special Economic Zones and Free Zones (OPAZ) initiated the development of new industrial cities to enhance the number of industrial facilities, localise investments within the industrial sector, elevate the sector's contribution to the gross domestic product, and generate additional job opportunities for Omani youth. The industrial zones presently under development by the Authority, in partnership with the Public Establishment for Industrial Estates (Madayn), encompass Mahas Industrial City in the Wilayat of Khasab, Musandam Governorate, where a contract for road and infrastructure enhancement was inked in October of the previous year.

Growing Food and Beverage Consumption

The food and beverage sector remains a fundamental driver of packaging demand in Oman, fueled by a rising population, increasing urbanization, and growing consumer spending on processed and packaged food products. Government-led food security initiatives are expanding domestic agricultural output and food processing capabilities, generating consistent demand for packaging materials that ensure product safety, hygiene, and extended shelf life. The retail landscape is also evolving, with modern supermarkets, hypermarkets, and convenience stores replacing traditional channels, each demanding sophisticated packaging solutions that combine functionality with brand differentiation. IMARC Group predicts that the Oman foodservice market reached USD 3.68 Billion by 2034.

Strategic Development of Polymer Manufacturing Infrastructure

Oman is investing strategically in building a comprehensive domestic polymer conversion industry that directly strengthens packaging manufacturing capacity. The establishment of dedicated industrial parks with integrated raw material supply, infrastructure, and logistics connectivity is reducing import dependency and positioning the Sultanate as a competitive regional packaging production hub. Access to competitively priced polymer resins from domestic petrochemical complexes provides manufacturers with a structural cost advantage, enabling the production of plastic packaging products for both local consumption and export to GCC and international markets. The development of specialized industrial clusters is fostering collaboration among converters, attracting foreign technology and investment, and creating a self-reinforcing ecosystem that supports continuous innovation and capacity growth in the packaging sector.

Market Restraints:

What Challenges the Oman Packaging Market is Facing?

Limited Domestic Recycling Infrastructure

Despite growing regulatory emphasis on sustainability, Oman’s recycling infrastructure remains underdeveloped, with a limited number of processing facilities and insufficient waste segregation systems. This gap hampers the effective recovery and reuse of packaging materials, increasing landfill dependency and raising the cost of compliance with evolving environmental regulations for packaging manufacturers and converters.

High Cost of Sustainable Packaging Materials

The transition from conventional to biodegradable, compostable, and recyclable packaging materials involves significantly higher production costs, creating a price barrier for manufacturers. This cost differential is particularly challenging for small and medium-sized enterprises that constitute a substantial share of the packaging supply chain, potentially slowing the adoption of sustainable packaging solutions despite strong regulatory and consumer pressure.

Raw Material Price Volatility and Supply Chain Disruptions

The Oman packaging market remains vulnerable to fluctuations in global raw material prices, particularly for key polymers such as polyethylene and polypropylene, as well as paper and metal inputs. Geopolitical tensions, international supply chain disruptions, and shifting commodity dynamics can increase production costs unpredictably, compressing margins for converters and potentially limiting investment in capacity expansion.

Competitive Landscape:

The Oman packaging market is characterized by a competitive mix of established domestic manufacturers and international suppliers serving diverse end use industries. Key players are focusing on expanding production capacity, upgrading manufacturing technologies, and investing in sustainable material innovation to meet evolving regulatory requirements and consumer preferences. Competition is intensifying as the government’s industrialization strategy attracts new entrants through economic zone incentives, polymer park investments, and streamlined licensing procedures. Strategic partnerships between local converters and international technology providers are fostering knowledge transfer and enhancing product quality, while the proximity to competitively priced raw materials provides domestic manufacturers with a cost advantage in regional and export markets.

Oman Packaging Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Billion |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Materials Covered |

Plastic, Paper and Paperboard, Metal, Glass, Wood, Others |

|

Product Types Covered |

|

|

Packaging Types Covered |

Primary Packaging, Secondary Packaging, Tertiary Packaging |

|

End-Use Industries Covered |

|

|

Regions Covered |

Muscat, Al Batinah, Al-Sharqiyah, Al-Dakhiliyah, Dhofar, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Oman Packaging Market Report

The Oman packaging market size was valued at USD 1.46 Billion in 2025.

The market is expected to grow at a compound annual growth rate of 3.74% from 2026-2034 to reach USD 2.27 Billion by 2034.

Plastic, holding the largest revenue share of 41.6%, remains the dominant material in the Oman packaging market, driven by its versatility, cost-effectiveness, and extensive use across food, beverage, pharmaceutical, and consumer product packaging applications.

Key factors driving the Oman packaging market include economic diversification under Oman Vision 2040, expanding food and beverage consumption, strategic polymer manufacturing infrastructure development, growing e-commerce activity, and increasing demand for sustainable packaging solutions.

Major challenges include limited domestic recycling infrastructure, high costs associated with sustainable packaging materials, raw material price volatility, supply chain disruptions, and the need for greater investment in advanced packaging technologies and skilled workforce development.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)