Oman Petrochemicals Market Size, Share, Trends and Forecast by Type, Application, End-Use Industry, and Region, 2026-2034

Oman Petrochemicals Market Summary:

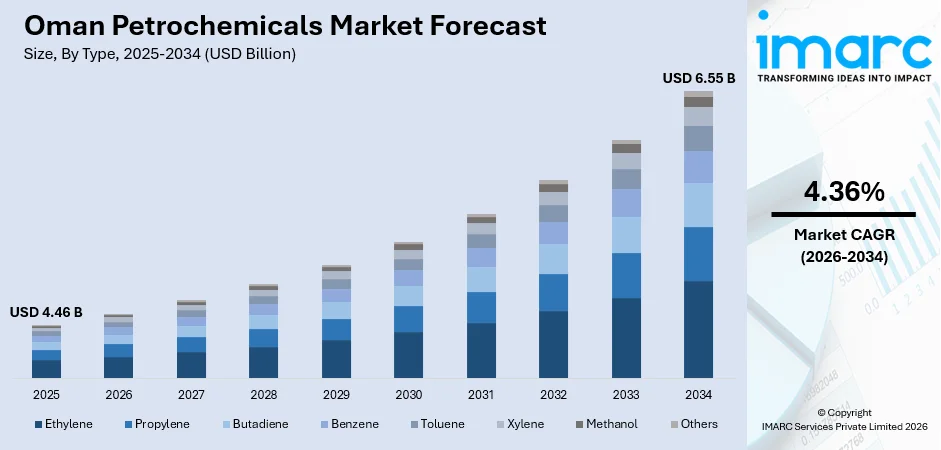

The Oman petrochemicals market size was valued at USD 4.46 Billion in 2025 and is projected to reach USD 6.55 Billion by 2034, growing at a compound annual growth rate of 4.36% from 2026-2034.

The market is advancing steadily as the Sultanate pursues value-added industrialization and downstream diversification under its national economic transformation strategy. Expanding refining and polymer production capacity, growing feedstock availability through new gas extraction projects, and rising demand from packaging, construction, and automotive sectors are strengthening the domestic petrochemical ecosystem. The integration of advanced manufacturing technologies and the development of dedicated industrial zones are further accelerating growth and expanding the Oman petrochemicals market share.

Key Takeaways and Insights:

- By Type: Ethylene dominates the market with a share of 26.8% in 2025, driven by its critical role as the primary building block for polyethylene production and widespread industrial applications across packaging and construction sectors.

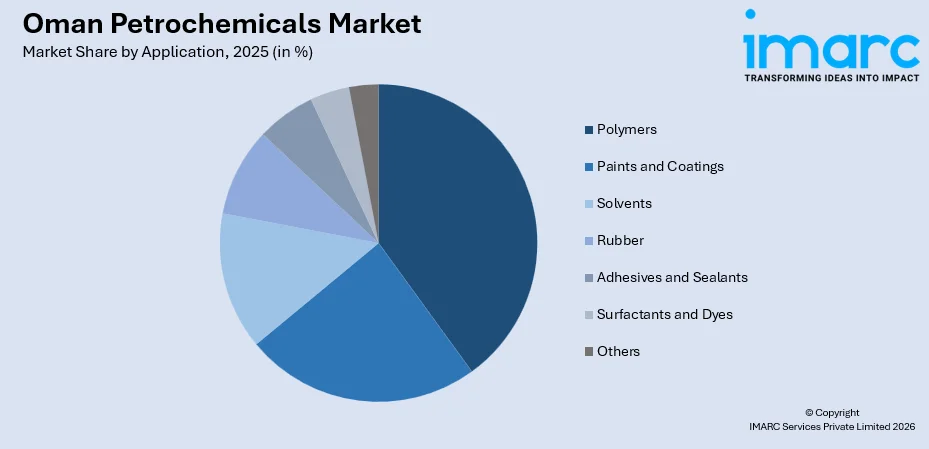

- By Application: Polymers lead the market with a share of 38.9% in 2025, reflecting strong demand for polyethylene and polypropylene resins used extensively in flexible and rigid packaging, consumer goods, and infrastructure development.

- By End-Use Industry: Packaging holds the largest share at 34.7% in 2025, owing to the rising consumption of polymer-based films, containers, and bottles across food and beverage, consumer goods, and e-commerce logistics sectors.

- By Region: Muscat represents the largest segment with a market share of 41.2% in 2025, supported by its position as the commercial capital housing major industrial operations, distribution networks, and consumer markets.

- Key Players: The Oman petrochemicals market features a concentrated competitive landscape with state-backed energy groups and integrated downstream operators driving capacity expansion, product diversification, and regional export competitiveness.

To get more information on this market Request Sample

Oman's petrochemicals market is picking up pace as the Sultanate accelerates its economic diversification strategy through downstream investments and industrial sector development. The petrochemicals sector in Oman is also witnessing an improvement in feedstock availability with the expansion in gas production operations and the development of new gas extraction plants. At the same time, the petrochemicals sector in Oman is also witnessing increased demand from end-use industries such as packaging materials, construction, automobiles, and healthcare. To illustrate this point, it was reported that OQ Group has initiated a front-end engineering design tender in February 2026 to build a natural gas liquids extraction plant at Saih Nihayda with a plant capacity to process up to 48 million cubic metres per day. Additionally, there would also be a fractionation plant at Duqm to separate one million tonnes of gas components annually.

Oman Petrochemicals Market Trends:

Expansion of Integrated Downstream Complexes

Oman is speeding up the development of integrated large-scale petrochemical facilities to realize the maximum potential of its hydrocarbon resources. OQ Group and Kuwait Petroleum International have agreed to sign a project development agreement on a jointly owned petrochemical complex in the Duqm Special Economic Zone in Oman. The move to increase downstream integration is adding to the product offerings, thus fueling the Oman petrochemicals market. The project development agreement has been signed by Ashraf Hamed Al Mamari, Group Chief Executive Officer of OQ, and Shafi Taleb Al Ajmi, Chief Executive Officer of KPI, at the Kuwait Oil & Gas Show (KOGS 2026), which shows the commitment of both parties to progressing the Oman Petrochemical Project. The move is a testament to the strategic importance of the project, which is deemed to be vital in enhancing cooperation in the region and in support of economic diversification initiatives in alignment with Oman Vision 2040.

Growing Adoption of Advanced Polymer Production

The Sultanate is seeking to improve its polymer production capabilities to meet the growing demand for polyethylene and polypropylene, both locally and externally. Sohar Port and Freezone in Oman has marked a major milestone in the country with the inauguration of a new polymer production plant, valued at RO 115.4 million (USD 300 million). The strategic move is a testament to Oman's advancement in terms of industrialization, thus enhancing its reputation on the global scene in terms of innovation and sustainable development. The new plant is expected to be set up on a 240,000 square-meter area in Sohar Port, where modern technology would be employed to produce polyacrylamide and monomers. The move is a testament to the country's determination to solidify its position in the global value chain.

Integration of Renewable Energy in Petrochemical Operations

The petrochemical industry in Oman is increasingly embracing different forms of renewable energy in its operations. This is in line with Oman’s strategy to achieve net-zero emissions. Solar and wind energy are being integrated with chemical production operations in newer plants in Duqm and Sohar. This is improving not only sustainability but also cutting operational costs in the petrochemical value chain. Worth noting are projects worth more than $3.3 billion (RO 1.275 billion) in various stages of development in the Salalah Free Zone in Oman. These projects are in industrial, petrochemical, green energy, food processing, and logistics sectors. By Q3 2025, the total investment value in the free zone was valued at RO 5.1 billion, driven mainly by foreign direct investments due to incentives like 100% foreign ownership and exemption from taxation.

Market Outlook 2026-2034:

Oman's petrochemicals market is positioned for sustained growth, driven by strategic industrial investments, expanding feedstock availability, and rising demand across key end-use sectors. The market generated a revenue of USD 4.46 Billion in 2025 and is projected to reach a revenue of USD 6.55 Billion by 2034, growing at a compound annual growth rate of 4.36% from 2026-2034. The continued development of integrated petrochemical complexes in Duqm and Sohar, coupled with supportive government policies under Oman Vision 2040, is expected to drive higher revenue streams and strengthen the Sultanate's competitive position as a regional downstream hub. Increasing polymer capacity, improved logistics infrastructure, and growing participation from international partners are anticipated to further broaden the market's growth trajectory.

Oman Petrochemicals Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Ethylene |

26.8% |

|

Application |

Polymers |

38.9% |

|

End-Use Industry |

Packaging |

34.7% |

|

Region |

Muscat |

41.2% |

Type Insights:

- Ethylene

- Propylene

- Butadiene

- Benzene

- Toluene

- Xylene

- Methanol

- Others

Ethylene leads the market with a revenue share of 26.8% of the total Oman petrochemicals market in 2025.

Ethylene forms the base of the Oman petrochemical market in terms of its largest share in product type due to its large number of downstream derivatives and strong global demand. It is primarily derived from the process of steam cracking hydrocarbon compounds like ethane and naphtha. It acts as a basic building block for a number of different petrochemical derivatives. Oman enjoys a cost advantage in ethylene production due to its abundant availability of natural gas.

Significantly, a large portion of the ethylene produced in Oman is used in the production of polyethylene, which has a wide range of applications in packaging, construction, and consumer products. Furthermore, it plays a vital role in the production of other important products, including ethylene glycol, styrene, and vinyl chloride, which are used in the textile, automobile, and construction industries. The geographical position of Oman, which is favorable in terms of international trade routes, also increases its potential in the export of its products, especially those derived from ethylene, to important countries in Asia, Europe, and Africa. The Government of Oman has been working towards enhancing the value of its products, especially those derived from ethylene, through integrated oil and petrochemical complexes. This has been a vital move in the economic diversification of the country, which has helped in reducing its dependence on crude oil exports.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Polymers

- Paints and Coatings

- Solvents

- Rubber

- Adhesives and Sealants

- Surfactants and Dyes

- Others

Polymers dominate with a share of approximately 38.9% in the Oman petrochemicals market in 2025.

Polymers represent the largest application segment in Oman's petrochemicals landscape, driven by the extensive use of polyethylene and polypropylene across packaging, consumer goods, and industrial applications. The Sultanate's integrated production facilities are capable of delivering high-volume polymer output that serves both local converters and international buyers. Rising demand for flexible and rigid packaging solutions, coupled with expanding construction activity, is sustaining robust polymer consumption growth across the economy.

The ongoing diversification of Oman's polymer product portfolio, including advanced grades of high-density polyethylene and linear low-density polyethylene, is enabling penetration into higher-value market segments. Investments in downstream plastic conversion industries and the establishment of specialized technology centers are further strengthening the local polymer ecosystem. These efforts are creating new opportunities for value addition and enhancing the competitiveness of Oman-produced polymers in regional and global markets.

End-Use Industry Insights:

- Packaging

- Automotive and Transportation

- Construction

- Electrical and Electronics

- Healthcare

- Others

Packaging is the largest segment, accounting for 34.7% of the Oman petrochemicals market in 2025.

The packaging sector serves as the primary consumer of petrochemical products in Oman, utilizing polyethylene, polypropylene, and specialty polymers for the production of films, containers, bottles, and industrial wrapping materials. Growing food and beverage processing activity, expanding retail distribution channels, and increasing e-commerce logistics are driving sustained demand for polymer-based packaging solutions. The sector benefits from proximity to domestic polymer production facilities, enabling efficient supply chain integration.

Evolving consumer preferences toward convenience, product safety, and extended shelf life are further bolstering demand for advanced packaging materials derived from petrochemical feedstocks. Regulatory emphasis on sustainable packaging practices and recyclability standards is encouraging innovation in packaging design and material formulations. These dynamics are creating a favorable environment for continued growth of petrochemical consumption within the packaging industry, reinforcing its position as the leading end-use segment in the market.

Regional Insights:

- Muscat

- Al Batinah

- Al-Sharqiyah

- Al-Dakhiliyah

- Dhofar

- Others

Muscat holds the largest share at approximately 41.2% of the Oman petrochemicals market in 2025.

Muscat serves as the commercial and administrative center of Oman's petrochemical ecosystem, housing major corporate headquarters, distribution networks, and consumer markets that collectively drive the largest share of market activity. The capital region benefits from well-developed transport infrastructure, access to ports, and proximity to key industrial operations. Growing urbanization, expanding retail and food processing sectors, and rising construction activity within the greater Muscat area are sustaining strong demand for petrochemical-derived products.

The concentration of manufacturing enterprises, packaging converters, and industrial consumers in Muscat further reinforces the region's dominance in the petrochemicals market. Government initiatives to develop specialized industrial clusters and improve logistics connectivity are enhancing the business environment for petrochemical downstream activities. The capital's strategic position as a hub for both domestic distribution and international trade is expected to maintain Muscat's leading market position throughout the forecast period.

Market Dynamics:

Growth Drivers:

Why is the Oman Petrochemicals Market Growing?

Strategic Downstream Industrialization and Economic Diversification

Oman is pursuing an ambitious economic diversification strategy that places petrochemical development at the center of its industrial transformation. The government's long-term vision prioritizes the creation of integrated downstream value chains that convert raw hydrocarbon resources into high-value finished products, reducing dependence on crude oil exports. Strategic industrial zones in key locations are being developed with specialized infrastructure, competitive incentives, and regulatory frameworks designed to attract both domestic and international investment into petrochemical manufacturing. This policy-driven approach is creating an enabling environment for sustained sectoral expansion, supporting the development of diverse product portfolios, and enhancing Oman's industrial self-sufficiency across critical petrochemical product categories. Future Fund Oman reported unprecedented activity in 2025, greenlighting 141 projects this year and raising total commitments to $1.2 billion as the fund propels Oman's economic diversification initiative. Created by the Oman Investment Authority, the fund has a capital commitment of $5.2 billion to be utilized over five years, making it one of the fastest-growing national investment vehicles in the region, with all funds focused on projects within Oman that align with the goals of Oman Vision 2040.

Expanding Feedstock Availability and Gas Infrastructure

The development of new natural gas extraction and processing facilities is significantly strengthening feedstock supply for Oman's petrochemical industry. Investments in upstream gas production, pipeline networks, and fractionation infrastructure are ensuring reliable and cost-competitive access to key feedstocks including ethane, propane, and naphtha. Long-term gas supply agreements are providing the supply certainty needed to support multi-decade industrial planning and capacity expansion. Enhanced feedstock availability is enabling existing petrochemical facilities to operate at higher utilization rates while also providing the foundation for new downstream projects. This expanding gas infrastructure ecosystem is positioning Oman as a competitive producer of petrochemical intermediates and finished products for domestic consumption and export markets.

Rising Demand from End-Use Industries

Robust growth across Oman's packaging, construction, automotive, and healthcare sectors is generating sustained demand for a diverse range of petrochemical products. The expanding food and beverage processing industry, coupled with growing e-commerce logistics, is driving increased consumption of polymer-based packaging materials. Infrastructure development programs, including large-scale urban planning projects and transportation networks, are supporting demand for construction chemicals, adhesives, coatings, and specialty polymers. The healthcare sector is also emerging as a significant consumer of petrochemical derivatives used in medical devices, pharmaceutical packaging, and disposable products. These converging demand trends are creating a broad and resilient consumption base that supports continuous growth of the petrochemicals sector. In 2026, OQ and Kuwait Petroleum International (KPI) have entered into a new project development agreement for their collaborative petrochemicals facility in the Special Economic Zone at Duqm (SEZAD). The pact, inked at the Kuwait Oil & Gas Show 2026, strengthens the dedication of both parties to the Oman Petrochemical Project. Technical teams are presently focused on optimized setups, while discussions are ongoing with potential partners to improve the project's international competitiveness.

Market Restraints:

What Challenges the Oman Petrochemicals Market is Facing?

Volatility in Global Crude Oil and Feedstock Prices

Fluctuations in global crude oil and natural gas prices directly impact the cost structure and profitability of petrochemical production in Oman. Price volatility affects input costs for feedstocks such as naphtha, ethane, and propane, creating uncertainty in production planning and margin management. Extended periods of depressed or elevated pricing can disrupt investment decisions and affect the competitiveness of Omani petrochemical products in international markets.

Environmental Regulatory Pressures and Sustainability Mandates

Increasingly stringent environmental regulations and sustainability requirements are imposing additional compliance costs on petrochemical manufacturers in Oman. New standards governing emissions, waste management, and recyclability demand significant capital investment in cleaner production technologies and process upgrades. These regulatory pressures, while beneficial for long-term sustainability, can increase operational costs and slow capacity expansion timelines in the near term.

Limited Domestic Skilled Workforce Availability

The petrochemical sector requires highly specialized technical and engineering talent, and Oman faces ongoing challenges in developing a sufficiently large domestic skilled workforce. Dependence on expatriate labor for critical operational and engineering roles adds to operational costs and creates workforce planning complexities. While national training initiatives are underway, the gap between industry requirements and available local talent continues to constrain operational efficiency and expansion capabilities.

Competitive Landscape:

The Oman petrochemicals market features a concentrated competitive landscape dominated by state-backed integrated energy groups that operate across the full hydrocarbon value chain from upstream extraction through downstream polymer production and marketing. These major players leverage significant capital resources, long-term feedstock access agreements, and advanced manufacturing technologies to maintain market leadership. Competition is also emerging from private sector participants developing specialized petrochemical parks and niche chemical production facilities. Strategic partnerships between domestic operators and international energy majors are facilitating technology transfer, capacity expansion, and market access. The emphasis on localization, value addition, and export competitiveness is driving continuous improvement in operational efficiency and product quality across the industry. Players are also increasingly integrating sustainability practices and circular economy principles into their production processes to align with evolving regulatory requirements and global market expectations.

Oman Petrochemicals Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Billion |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

Ethylene, Propylene, Butadiene, Benzene, Toluene, Xylene, Methanol, Others |

|

Applications Covered |

Polymers, Paints and Coatings, Solvents, Rubber, Adhesives and Sealants, Surfactants and Dyes, Others |

|

End-Use Industries Covered |

Packaging, Automotive and Transportation, Construction, Electrical and Electronics, Healthcare, Others |

|

Regions Covered |

Muscat, Al Batinah, Al-Sharqiyah, Al-Dakhiliyah, Dhofar, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Oman Petrochemicals Market Report

The Oman petrochemicals market size was valued at USD 4.46 Billion in 2025.

The market is expected to grow at a compound annual growth rate of 4.36% from 2026-2034 to reach USD 6.55 Billion by 2034.

Ethylene, holding the largest revenue share of 26.8%, remains pivotal for Oman's petrochemical sector, serving as the primary feedstock for polyethylene production and supporting diverse downstream applications across packaging, construction, and consumer goods industries.

Key factors driving the Oman petrochemicals market include strategic downstream industrialization under Oman Vision 2040, expanding feedstock availability through new gas infrastructure, rising demand from packaging and construction sectors, and growing international partnerships supporting capacity expansion.

Major challenges include global crude oil and feedstock price volatility, increasing environmental regulatory compliance costs, limited domestic skilled workforce availability, high capital intensity of new petrochemical projects, and competition from established regional petrochemical hubs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)