Oman Retail Market Size, Share, Trends and Forecast by Product, Distribution Channel, and Region, 2026-2034

Oman Retail Market Summary:

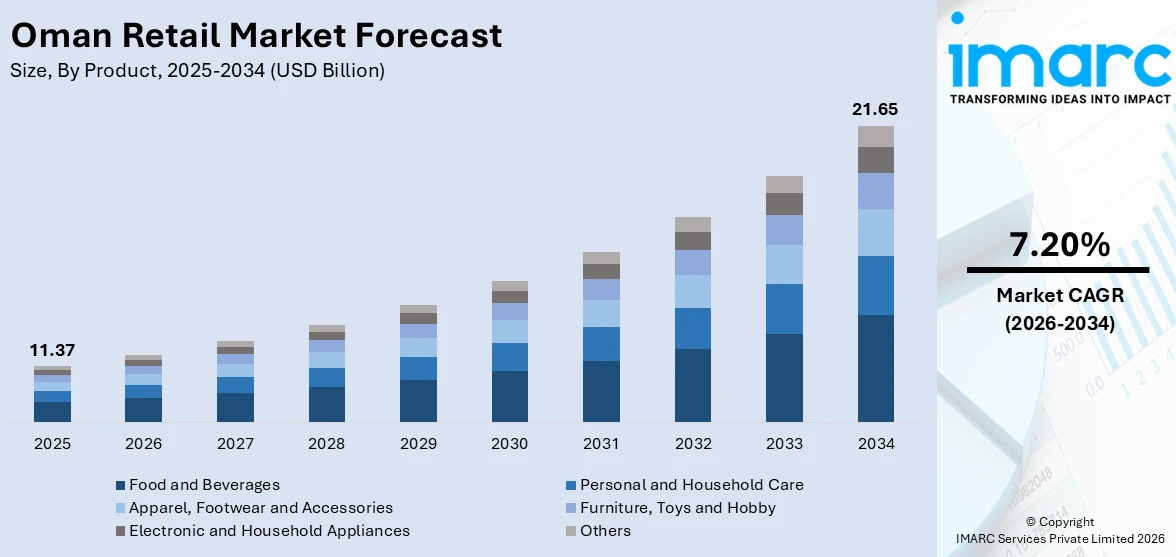

The Oman retail market size was valued at USD 11.37 Billion in 2025 and is projected to reach USD 21.65 Billion by 2034, growing at a compound annual growth rate of 7.20% from 2026-2034.

Rising consumer spending, more urbanization, and a younger demographic profile are driving the retail market's strong expansion in Oman. The retail industry is changing as a result of Vision 2040's economic diversification measures, with contemporary shopping forms becoming more popular alongside conventional outlets. Changing lifestyle choices, an increase in tourists, and the use of digital technology are changing consumer behavior and sustaining demand in the food, personal care, clothing, and electronics sectors across the retail market share of Oman.

Key Takeaways and Insights:

- By Product: Food and beverages dominate the market with a share of 41% in 2025, since the food expenditures are vital, the population is growing, the expat community is growing, and consumers' preferences for packaged and convenience foods are increasing across all retail channels.

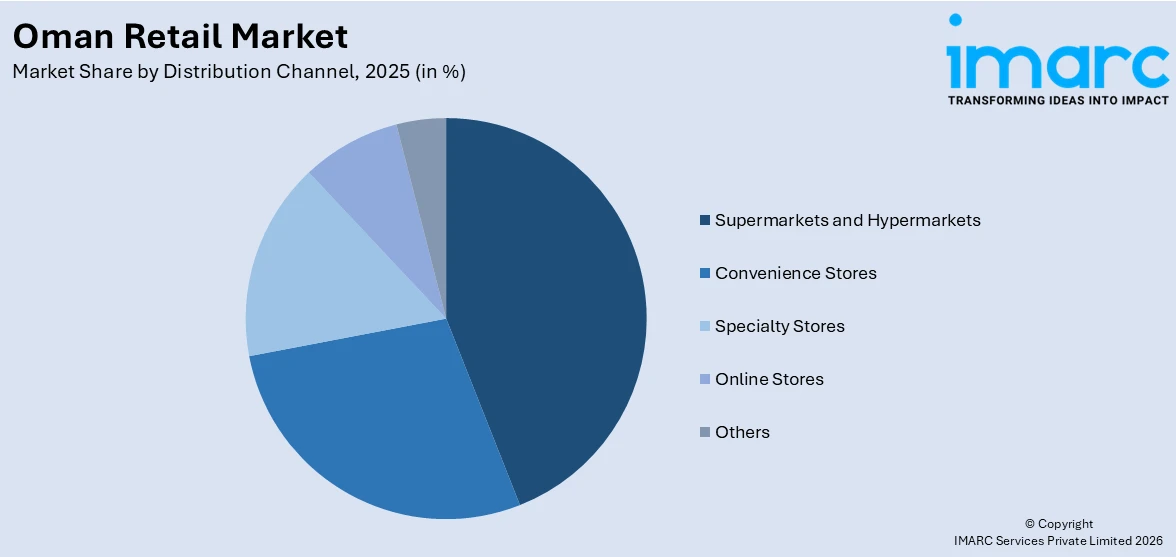

- By Distribution Channel: Supermarkets and hypermarkets lead the market with a share of 44% in 2025. Convenient one-stop shopping, aggressive pricing tactics, a wide range of products, and the continuous growth of contemporary retail formats throughout Oman's urban and semi-urban areas are the main drivers of this supremacy.

- By Region: Muscat is the largest region with 37% share in 2025, powered by a dense network of contemporary shopping malls, better disposable incomes, a large population concentrated in the capital governorate, and robust retail activity fueled by tourists.

- Key Players: By growing store networks, improving omnichannel capabilities, fortifying supply chains, and making investments in consumer engagement technologies, major competitors propel the retail business in Oman. Their strategic emphasis on regional products, low pricing, and product diversification speeds up market penetration and guarantees widespread consumer accessible.

To get more information on this market Request Sample

Under its Vision 2040 framework, Oman is pursuing a complete economic reform, and the retail industry is growing steadily. Rapid urbanization, a youthful populace, and rising disposable incomes are all driving consumer demand for a wide range of products. The growth of contemporary retail infrastructure, like as shopping centers, specialty shops, and large-format hypermarkets, is changing the way people shop and drawing both local and foreign merchants to the Omani market. The nation's expanding tourism industry, which keeps reinforcing retail purchasing trends in the food, clothing, and consumer electronics categories, is a key factor influencing this development. Convenience and consumer access are being further expanded through the integration of mobile payment solutions and digital commerce platforms. All governorates are experiencing continuous retail market expansion thanks to government measures encouraging private sector investment, enhanced logistics networks, and advantageous regulatory reforms.

Oman Retail Market Trends:

Rapid Expansion of E-Commerce and Digital Retail

Oman’s retail landscape is being reshaped by the accelerating adoption of e-commerce and digital payment platforms. The country’s youthful, mobile-first population is increasingly shifting spending toward online grocery, fashion, and quick-commerce applications. For instance, Apple Pay and Samsung Pay launched in Oman in 2024, expanding digital payment accessibility for consumers nationwide. Government-backed digital economy programs under Vision 2040, along with the nationwide rollout of mobile payment gateways, are strengthening the digital retail ecosystem and supporting the Oman retail market growth.

Growing Tourism-Driven Retail Spending

The tourism sector is emerging as a significant catalyst for retail consumption in Oman. Rising visitor arrivals are boosting demand for food and beverages, apparel, electronics, and lifestyle products across major retail destinations. For instance, Oman welcomed approximately 3.8 million visitors in 2024, with total visitor spending reaching OMR 989 Million according to the National Centre for Statistics and Information. Expanding hotel capacity, new cultural tourism sites, and improved air connectivity are drawing diverse international visitors, sustaining elevated retail footfall in malls and commercial districts.

Rise of Modern Organized Retail Formats

Traditional independent retail establishments are giving way to structured formats including shopping malls, hypermarkets, and integrated retail-entertainment venues in Oman. Consumer demands for ease, brand diversity, and immersive shopping experiences are driving this shift. Retailers and developers are investing in contemporary commercial buildings that house a variety of dining, entertainment, and lifestyle options in addition to a wide range of products. Organized retail is rapidly spreading throughout the sultanate's major cities and new suburban corridors due to consumers' increasing desire for carefully planned shopping experiences, access to luxury brands, and climate-controlled retail spaces.

Market Outlook 2026-2034:

The Oman retail market is positioned for sustained expansion over the forecast period, supported by economic diversification, population growth, rising tourism, and advancing digital infrastructure. The market generated a revenue of USD 11.37 Billion in 2025 and is projected to reach a revenue of USD 21.65 Billion by 2034, growing at a compound annual growth rate of 7.20% from 2026-2034. Favorable conditions for the growth of the retail sector are being created by government initiatives under Vision 2040, such as investments in commercial real estate, logistics corridors, and special economic zones. Higher income streams are anticipated as a result of the ongoing development of contemporary retail locations, the fortification of supply chain networks, and the growing adoption of omnichannel retail tactics. A competitive and dynamic retail environment will be fostered throughout the sultanate by a youthful consumer base, an increasing expatriate community, and greater connection through improved transportation infrastructure, which will further drive demand across the food, personal care, fashion, and electronics segments.

Oman Retail Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product |

Food and Beverages |

41% |

|

Distribution Channel |

Supermarkets and Hypermarkets |

44% |

|

Region |

Muscat |

37% |

Product Insights:

- Food and Beverages

- Personal and Household Care

- Apparel, Footwear and Accessories

- Furniture, Toys and Hobby

- Electronic and Household Appliances

- Others

Food and beverages dominate with a market share of 41% of the total Oman retail market in 2025.

Because grocery and packaged food purchases are necessary and recurrent, the food and beverage industry holds the highest share of Oman's retail market. Increased household formation, growing expatriate populations, and population growth are all contributing to the nation's high demand for packaged convenience goods, dairy products, drinks, and staple foods. Government initiatives to boost domestic food production, increase supply chain effectiveness, and lower post-harvest losses are contributing to the expansion of food-related retail activity, highlighting the sector's vital role in the larger retail ecosystem and in regular consumer purchasing patterns.

Oman's consumer preferences are shifting toward more upscale, convenient, and healthful food and drink options due to younger generations' shifting lifestyles and growing health consciousness. While international food products are becoming more popular through contemporary retail channels, traditional Omani cuisine is still a staple in households. In order to satisfy a growing number of picky consumers who are looking for convenience, quality, and nutrition, organized food retail formats, better cold chain logistics, and expanding ready-to-eat and organic product lines are all contributing to an increase in product variety and freshness in both urban and rural markets.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Stores

- Others

Supermarkets and hypermarkets lead with a share of 44% of the total Oman retail market in 2025.

Oman's retail business is dominated by supermarkets and hypermarkets, which provide customers with a convenient one-stop shop for groceries, electronics, personal care items, and household necessities. Competitive pricing, wide product selections, and well-organized shop spaces make these large-format stores appealing to both Omani citizens and foreigners. Growing consumer preference for contemporary retail formats that combine affordability, product diversity, and a comfortable shopping experience under a single climate-controlled environment throughout the sultanate is reflected in the hypermarket networks' steady expansion throughout urban and semi-urban areas.

Strategic investments in fresh produce logistics and supply chain infrastructure further boost the expansion of supermarkets and hypermarkets in Oman. Private label brands, loyalty plans, and integrated services like food courts, electronics departments, and pharmacies within stores are all ways that retailers are improving their products. These backend infrastructure investments are lowering operating costs, increasing product freshness, and facilitating more constant availability across a variety of retail locations around the nation. The competitive positioning of hypermarkets in the changing retail landscape is being further strengthened by the introduction of digital tools including click-and-collect services, mobile applications, and self-checkout systems.

Regional Insights:

- Muscat

- Al Batinah

- Al-Sharqiyah

- Al-Dakhiliyah

- Dhofar

- Others

Muscat holds the largest share at 37% of the total Oman retail market in 2025.

As the capital and main commercial center of Oman, Muscat has the biggest concentration of contemporary shopping malls, hypermarkets, specialized shops, and outlets for global brands, dominating the country's retail scene. Because of its economic prominence and demographic concentration, the governorate has the sultanate's largest customer base and draws substantial retail investment. Muscat is positioned as the center of organized retail activity due to the existence of premier retail destinations, which serve a variety of consumer segments such as wealthy locals, foreign visitors, and expatriates looking for high-end goods, branded merchandise, and immersive lifestyle shopping experiences across a range of retail formats.

Strong tourism-driven foot traffic, high disposable incomes, and ongoing infrastructural development that improves the shopping experience all contribute to Muscat's retail industry's success. With fresh store openings and retail partnerships strengthening its market leadership, the governorate is the main gateway for foreign retail brands looking to grow into Oman. Muscat's standing as the sultanate's top retail destination is further cemented by growing consumer desire for high-end goods, immersive retail formats, and internet shopping options. The capital's appeal as the go-to location for retail innovation and investment is strengthened by ongoing commercial real estate development, enhanced transportation connectivity, and government-backed urbanization initiatives.

Market Dynamics:

Growth Drivers:

Why is the Oman Retail Market Growing?

Economic Diversification and Rising Consumer Spending

Oman's strategic push toward economic diversification under Vision 2040 is strengthening the foundations of its retail market by promoting non-oil sector development, enhancing private sector participation, and improving the overall business environment. As the country reduces its reliance on hydrocarbon revenues, investments in tourism, logistics, manufacturing, and commercial real estate are generating new employment opportunities and raising household incomes across governorates. This economic transformation is boosting consumer purchasing power and stimulating retail demand across product categories. Growing disposable incomes are encouraging consumers to diversify their spending beyond essential items toward premium food products, branded apparel, electronics, and lifestyle goods. Government-backed investment programs are supporting private-sector expansion and job creation, which in turn elevates consumer confidence and retail spending. As new commercial developments and retail-oriented infrastructure projects materialize, the market is benefiting from a broader and more affluent consumer base that sustains demand across both essential and discretionary retail segments.

Expanding Tourism Sector and Visitor Spending

The robust growth of Oman's tourism industry is providing a significant boost to the retail market by increasing footfall across shopping destinations and driving demand for food, apparel, souvenirs, and consumer electronics. The government's commitment to positioning Oman as a premier tourism destination is supported by infrastructure investments in hotels, cultural sites, and transportation networks that facilitate increased visitor flows across the country. Rising visitor arrivals, extended average stays, and growing total tourism expenditure are translating directly into higher retail sales across commercial districts, shopping malls, and specialty markets in key governorates. The diversification of Oman's tourism base, encompassing cultural heritage, eco-tourism, adventure activities, and wellness experiences, is attracting a broader spectrum of international and regional visitors with varied spending patterns. Expanding hotel capacity, improved air connectivity, and visa facilitation measures continue to strengthen tourism-driven retail consumption throughout the sultanate.

Rapid Urbanization and Demographic Expansion

Oman's rapidly urbanizing population and youthful demographic composition are fundamental drivers of retail market growth. With a significant majority of the population residing in urban areas and a young median age, the country presents a dynamic consumer base with evolving preferences for modern retail formats, branded products, and convenience-oriented shopping experiences. The expanding expatriate community further diversifies consumer demand, introducing preferences for international food products, global fashion brands, and technology products. Urban population centers, particularly the capital governorate, are witnessing continuous residential development and infrastructure upgrades that support the establishment of new retail destinations. Large-scale urbanization initiatives, including mixed-use developments that integrate retail, hospitality, and entertainment components, are creating dense consumer clusters and expanding the addressable market for retailers operating across diverse product segments. These demographic and urban development trends are reinforcing sustained long-term retail growth across the sultanate.

Market Restraints:

What Challenges the Oman Retail Market is Facing?

High Import Dependency and Supply Chain Vulnerabilities

Oman’s retail market faces challenges related to its substantial dependence on imported goods, particularly in the food and beverages category where import dependency has historically remained high. Fluctuations in global commodity prices, shipping costs, and trade disruptions can elevate product prices and squeeze retail margins. Limited local manufacturing capacity for many consumer goods categories further exposes the market to supply chain interruptions and cost volatility, affecting affordability for price-sensitive consumers.

Intensifying Competition from E-Commerce Substitution

The rapid growth of online retail platforms presents a competitive challenge for traditional brick-and-mortar retailers in Oman. As consumers increasingly shift purchases to digital channels offering convenience, competitive pricing, and wider product selections, physical stores face declining footfall and margin pressures. Cross-border e-commerce from regional and international platforms is further intensifying price competition, requiring traditional retailers to invest significantly in omnichannel strategies and digital transformation to retain customer engagement and market relevance.

Economic Sensitivity to Oil Price Fluctuations

Despite ongoing diversification efforts, Oman’s economy remains partially linked to hydrocarbon revenues, which continue to influence government spending, employment levels, and consumer confidence. Periods of depressed global oil prices can constrain fiscal budgets, slow infrastructure investment, and reduce household spending power, directly affecting retail sector performance. This economic sensitivity introduces cyclical uncertainty into the retail market, as consumer discretionary spending on apparel, electronics, and lifestyle products tends to contract during periods of fiscal austerity and reduced government expenditure.

Competitive Landscape:

The Oman retail market features a competitive landscape characterized by the presence of established regional hypermarket chains, international brand operators, and a growing number of digital commerce platforms. Companies are differentiating through strategic store expansion, product portfolio diversification, investment in supply chain modernization, and adoption of omnichannel retailing approaches. Competition is further intensified by the entry of global fashion and lifestyle brands through partnership arrangements with local mall operators. Retailers are enhancing customer loyalty through rewards programs, digital engagement tools, and experiential retail concepts that combine shopping with dining and entertainment. As the market matures, strategic collaborations, franchise arrangements, and investment in technology-driven customer experiences are becoming key competitive levers shaping the industry’s evolution.

Oman Retail Market Report Coverage:

| Report Features | Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Products Covered |

Food and Beverages; Personal and Household Care; Apparel, Footwear and Accessories; Furniture, Toys and Hobby; Electronic and Household Appliances; Others |

|

Distribution Channels Covered |

Supermarkets and Hypermarkets; Convenience Stores; Specialty Stores; Online Stores; Others |

|

Regions Covered |

Muscat, Al Batinah, Al-Sharqiyah, Al-Dakhiliyah, Dhofar, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Oman Retail Market Report

The Oman retail market size was valued at USD 11.37 Billion in 2025.

The Oman retail market is expected to grow at a compound annual growth rate of 7.20% from 2026-2034 to reach USD 21.65 Billion by 2034.

Food and beverages dominated the market with a share of 41%, driven by essential consumer spending on groceries, packaged foods, and beverages, supported by a growing population and expanding organized food retail formats.

Key factors driving the Oman retail market include economic diversification under Vision 2040, rising consumer disposable incomes, expanding tourism activity, rapid urbanization, a youthful demographic profile, and growing adoption of modern retail formats.

Major challenges include high import dependency for consumer goods, intensifying competition from e-commerce platforms, economic sensitivity to oil price fluctuations, supply chain vulnerabilities, and the need for sustained investment in digital retail infrastructure.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)