Operating Room Equipment Market Report by Type (Anesthesia Devices, Endoscopes, Operating Room Tables and Lights, Electrosurgical Devices, Surgical Imaging Devices, Patient Monitors, and Others), End User (Hospitals & Clinics, Ambulatory Surgical Centres, and Others), Region and Competitive Landscape (Market Share, Business Overview, Products Offered, Business Strategies, SWOT Analysis and Major News and Events) 2026-2034

Operating Room Equipment Market Size:

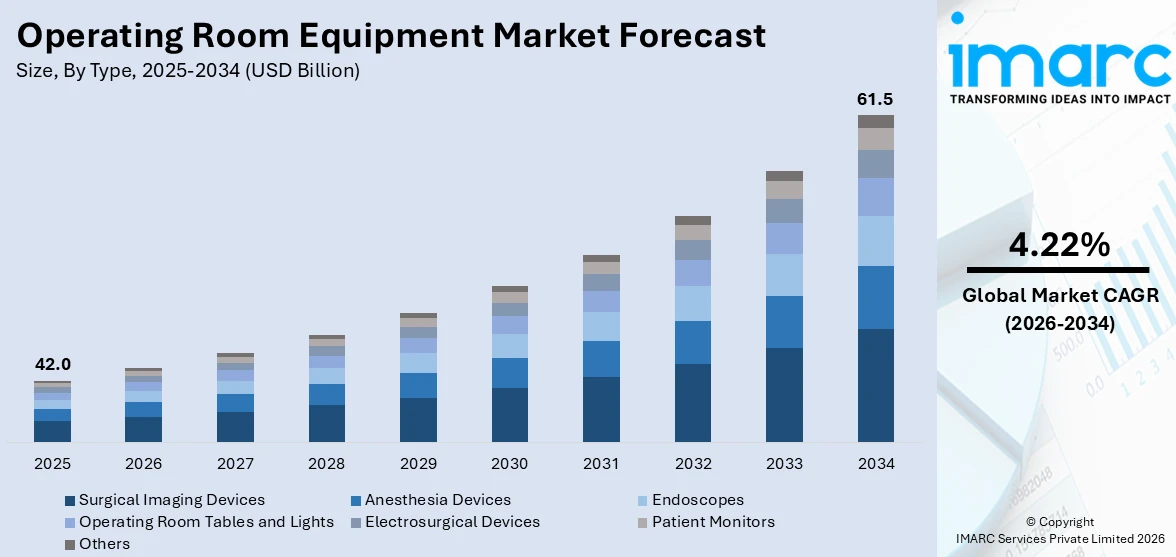

The operating room equipment market size reached USD 42.0 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 61.5 Billion by 2034, exhibiting a growth rate (CAGR) of 4.22% during 2026-2034. There are various factors that are driving the global market, which include improving healthcare infrastructure, rising number of hospitals and ambulatory surgery centers, and increasing concerns about enhancing safety while minimizing infection among patients.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 42.0 Billion |

| Market Forecast in 2034 | USD 61.5 Billion |

| Market Growth Rate (2026-2034) | 4.22% |

Operating Room Equipment Market Analysis:

- Major Market Drivers: One of the key market drivers is improved healthcare infrastructure. Moreover, the increasing number of hospitals and ambulatory surgery centers is acting as a growth-inducing factor.

- Key Market Trends: The market demand is impelled owing to numerous primary trends, which include the rising demand for hybrid operating rooms.

- Geographical Trends: According to the report, North America exhibits a clear dominance, accounting for the largest market share due to various partnerships among industry players.

- Competitive Landscape: Operating room equipment industry players in the market are Dragerwerk AG & Co. KGaA, General Electric Company, Getinge AB, Hill-Rom Holdings Inc. (Baxter International Inc.), Karl Storz SE & Co. KG, Koninklijke Philips N.V., Medtronic plc., MIZUHO Corporation., Siemens Healthineers AG (Siemens AG), Skytron LL., among many others.

- Challenges and Opportunities: One of the key challenges hindering the market growth is high maintenance and service costs. Nonetheless, the adoption of robotic equipment and investment in healthcare represent some recent opportunities.

To get more information on this market Request Sample

Operating Room Equipment Market Drivers:

Improved Healthcare Infrastructure

On 28 November 2021, GE Healthcare launched around 60 new technology solutions across various areas of healthcare such as patient screening, diagnostics, therapy planning, guidance, and monitoring. The company speeds up advancements supported by artificial intelligence (AI) and digital solutions to revolutionize healthcare delivery, improving convenience and efficiency for clinicians and health systems, and offering more personalized and accurate care for patients. Furthermore, the increasing emphasis on enhanced healthcare facilities is stimulating the need for surgical room equipment. Healthcare facilities are prioritizing the delivery of improved services to patients by investing in enhancing hospital infrastructure.

Rising Number of Hospitals and Ambulatory Surgery Centers

The prevalence of chronic diseases among people is leading to an increase in the number of healthcare facilities. Furthermore, governing authorities around the world are concentrating on expanding healthcare facilities, which involve operating rooms. For example, the Alberta government invested US$ 63.5 Million on 25 February 2022, to build 11 new surgery rooms at the Foothills hospital in Calgary. Up to 7,000 more procedures will be possible annually at the Northwest Calgary hospital as 11 extra operating rooms are added to the 32 already-existing ones.

Concerns Regarding Patient Safety and Infection

Rising concerns about patient safety and infection are catalyzing the demand for efficient operating room equipment. Furthermore, healthcare facilities are adopting advanced tools that benefit in maintaining improved patient safety and minimizes the risk of infection. For example, on 26 January 2023, Autonomi company in cooperation with Sarel, Israel’s Group Purchasing Organization (GPO) for government hospitals, opened first smart operating room that manages inventory. The new operating room tracks and manages inventory, reduces waste, conducts patient-safety recalls, and issues expiration warnings.

Operating Room Equipment Market Opportunities:

Innovation in Technologies

Key players in the industry are focusing on introducing advanced technologies in operating room equipment to provide enhanced care to patients while saving time and money. They are unveiling tools that offer enhanced convenience to healthcare professionals as well as patients. For instance, on March 2021, General Electric unveiled its new wireless, hand-held ultrasound device ‘Vscan Air’. It is the latest foray of the company into the point-of-care (POC) ultrasound market. It easily connects to a smartphone app to read the ultrasound and the images can be securely shared with patients. It can also be used by trained health-care providers to quickly evaluate blood flow and gallbladder disease.

Investment in Healthcare

There is an increase in investments in healthcare facilities by governing authorities and major players. Governing agencies are offering funding for research and development (R&D) activities in the healthcare systems. Moreover, top industry players are engaging in collaboration with other industry stakeholders to provide enhanced patient care. For instance, on 13 December 2021, Baxter International Inc. announced the completion of its acquisition with Hillrom. It accelerated the company's vision for transforming healthcare and advancing patient care worldwide. It created opportunities for innovation that increase efficiencies across care settings and help improve care outcomes.

Adoption of Robotic Equipment

On 22 February 2024, Zimmer Biomet Holdings, Inc. got U.S. Food and Drug Administration (FDA) 510(k) clearance of the ROSA® shoulder system for robotic-assisted shoulder replacement surgery. ROSA shoulder is the world's first robotic surgery system for shoulder replacement, and the fourth application for the Company's comprehensive ROSA® Robotics portfolio, which has the ROSA® Knee System for total knee arthroplasty and ROSA® Hip System for total hip replacement. Moreover, robotic systems offer high precision and control during surgeries that lead to better surgical outcomes and lower risk of complications.

Key Technological Trends & Development:

Telepresence for Operating Room

On 1 December 2023, Proximie unveiled its software development kit (SDK), with an emphasis on operating and diagnostic room digitization. To facilitate the sharing of knowledge and skills across hospitals, surgeons, and device manufacturers, SDK integrates telepresence, content management, and data insights. The company debuted SDK at Slush 2023, a conference held in Helsinki, Finland, where Proximie showcased the platform's capabilities using a robot called PxMosay. Furthermore, regardless of geographical distance, telepresence allows experienced surgeons to mentor less experienced doctors in real time throughout intricate surgeries. This can enhance surgical results by integrating global expertise.

Robotic Surgeries

Robotic systems offer high-precision tools and enhanced flexibility that exceed the natural capabilities of the human hand. They allow surgeons to perform complex procedures more accurately and lower the risk of infection. In addition, key players are focusing on expanding their product offerings. As on 18 January 2024, Augusta Health expanded robotic-assisted surgery capabilities to include total joint replacement. This cutting-edge robotic tool is used to benefit surgeons in creating an ideal individualized surgical plan with precision. The tool has clinical evidence that demonstrates reduced postoperative pain, decreased length of stay, and better physical function.

Image-Guided Vascular Access Technologies

On 17 October 2023, Abbott launched its new vascular imaging platform powered by Ultreon 1.0 Software in India. The intra-vascular imaging software combines optical coherence tomography (OCT) with the power of AI, providing physicians a comprehensive view of blood flow and blockages within coronary arteries. The innovative imaging software can automatically differentiate between a calcified and non-calcified blockage, detect the severity of calcium-based blockages, and measure vessel diameter. In addition, image-guided vascular access technologies are beneficial in enhancing the accuracy and safety of accessing blood vessels during various medical procedures. They utilize imaging methods such as ultrasound, fluoroscopy, or computed tomography (CT) to guide the insertion of catheters, needles, and other instruments into veins and arteries.

Operating Room Equipment Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on type and end user.

Breakup by Type:

- Anesthesia Devices

- Endoscopes

- Operating Room Tables and Lights

- Electrosurgical Devices

- Surgical Imaging Devices

- Patient Monitors

- Others

Surgical imaging devices account for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the type. This includes anesthesia devices, endoscopes, operating room tables and lights, electrosurgical devices, surgical imaging devices, patient monitors, and others. According to the report, surgical imaging devices represented the largest segment.

The escalating demand for surgical imaging devices due to the rising prevalence of chronic diseases among individuals such as diabetes, cardiovascular disorders, respiratory issues, and cancer is bolstering the market growth. People are increasingly suffering from these diseases due to inactive lifestyles, poor dietary patterns, and environmental factors. These disorders are catalyzing the demand for surgical imaging devices to detect problems accurately. The American Cancer Society claims that there will be around 106,590 colon cancer cases and approximately 46,220 rectal cancer cases in the US in 2024.

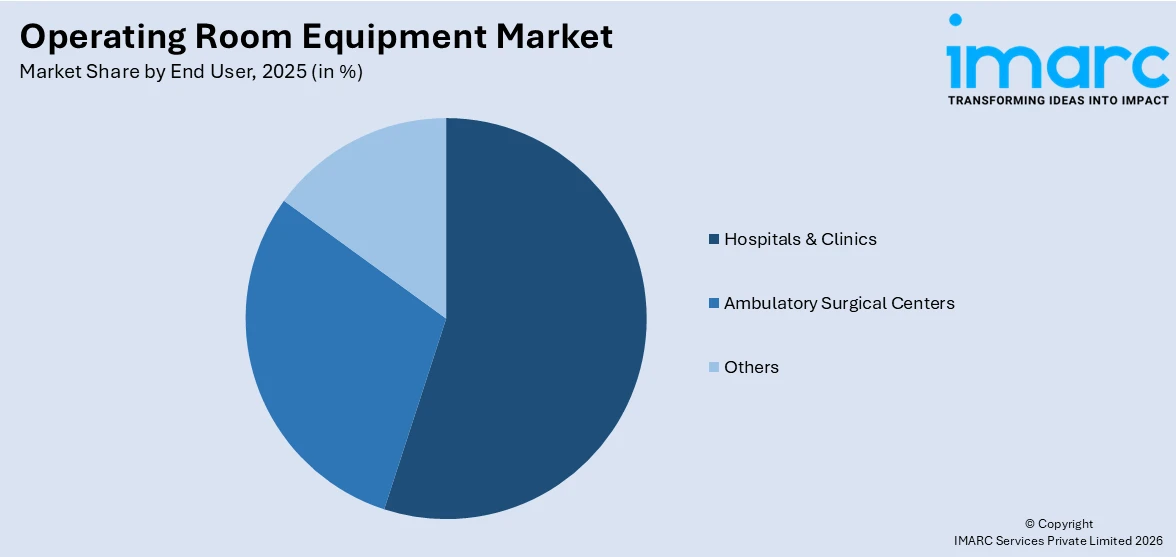

Breakup by End User:

Access the comprehensive market breakdown Request Sample

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Others

Hospitals and clinics hold the largest share of the industry

A detailed breakup and analysis of the market based on the end user have also been provided in the report. This includes hospitals and clinics, ambulatory surgical centers, and others. According to the report, hospitals & clinics accounted for the largest market share.

Hospitals & clinics perform a vast majority of surgical procedures as compared to specialized surgical centers or outpatient settings. This high volume of surgeries drives the need for extensive and varied operating room equipment. On 3 December 2023, USA Health unveiled five high-tech operating rooms at University Hospital. This expansion demonstrates USA Health’s commitment to provide more access to world-class surgical care for people in communities. The new operating rooms integrate the latest equipment with the most advanced ceiling-mounted lighting systems and booms, enhancing efficiency and safety. The rooms also have space for robotics for minimally invasive (MI) surgery, radiology C-arms for orthopedic surgery, and advanced image guidance systems for neurosurgery.

Breakup by Region:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East

- Africa

North America leads the market, accounting for the largest operating room equipment market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Latin America (Brazil, Mexico, and others); Middle East; and Africa. According to the report, North America represents the largest regional market for operating room equipment.

According to the American Hospital Association (AHA), there were around 6,120 hospitals in the financial year 2022. This indicated that North America has a well-established healthcare infrastructure. In addition, the rising prevalence of numerous severe diseases among individuals in the region is contributing to the market growth. Besides this, favorable government initiatives are supporting the market growth. Furthermore, innovations in medical technology like robotics, minimally invasive (MI) surgery devices, and imaging technologies, drive demand for new and upgraded operating room equipment in the North America region.

Analysis Covered Across Each Country:

- Historical, current, and future market performance

- Historical, current, and future performance of the market based on type and end user.

- Competitive landscape

- Government regulations

Competitive Landscape:

The market research report has provided a comprehensive analysis of the competitive landscape covering market structure, market share by key players, market player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant, among others. Detailed profiles of all major companies have also been provided. This includes business overview, product offerings, business strategies, SWOT analysis, financials, and major news and events. Some of the major market players in the operating room equipment industry include Dragerwerk AG & Co. KGaA, General Electric Company, Getinge AB, Hill-Rom Holdings Inc. (Baxter International Inc.), Karl Storz SE & Co. KG, Koninklijke Philips N.V., Medtronic plc., MIZUHO Corporation., Siemens Healthineers AG (Siemens AG), and Skytron LL. Top players in the market are focusing on meeting stringent regulatory requirements and achieving compliance with international standards, which is crucial for product approval and market access. Ensuring compliance helps in building trust and credibility among healthcare providers. In addition, companies are forming alliance, collaborations, and partnerships to create innovative operating room equipment. On 10 May 2022, Zimmer Biomet Holdings, Inc. introduced the availability of new artificial intelligence (AI) capabilities within Omni™ Suite, an intelligent operating room (OR) designed to optimize surgical workflow and procedural efficiency by automating manual tasks and streamlining unnecessary technology and redundant hardware.

Analysis Covered for Each Player:

- Market Share

- Business Overview

- Products Offered

- Business Strategies

- SWOT Analysis

- Major News and Events

Operating Room Equipment Market News:

- 31 January 2024: Scientific & Medical Equipment House Company, announced an exclusive distribution agreement with Haier Germany, a specialist in the sale and distribution of operating room equipment worldwide and the Middle East. The agreement would help the company expand its consumer base and portfolio of exclusive agencies for medical equipment companies in the Kingdom, a distinction that the company holds in the Middle East.

- 22 March 2023: Medtronic and NVIDIA unveiled a partnership to accelerate the development of AI in the healthcare system and bring new AI-based solutions into patient care.

Operating Room Equipment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Anesthesia Devices, Endoscopes, Operating Room Tables and Lights, Electrosurgical Devices, Surgical Imaging Devices, Patient Monitors, Others |

| End Users Covered | Hospitals & Clinics, Ambulatory Surgical Centers, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East, Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Dragerwerk AG & Co. KGaA, General Electric Company, Getinge AB, Hill-Rom Holdings Inc. (Baxter International Inc.), Karl Storz SE & Co. KG, Koninklijke Philips N.V., Medtronic plc., MIZUHO Corporation., Siemens Healthineers AG (Siemens AG), Skytron LL., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global operating room equipment market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global operating room equipment market?

- What is the impact of each driver, restraint, and opportunity on the global operating room equipment market?

- What are the key regional markets?

- Which countries represent the most attractive operating room equipment market?

- What is the breakup of the market based on the type?

- Which is the most attractive type in the operating room equipment market?

- What is the breakup of the market based on the end user?

- Which is the most attractive end user in the operating room equipment market?

- What is the competitive structure of the market?

- Who are the key players/companies in the global operating room equipment market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the operating room equipment market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global operating room equipment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the operating room equipment industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)