Optical Interconnect Market Size, Share, Trends and Forecast by Product Type, Interconnect Level, Fiber Mode, Application, End Use Industry, and Region, 2026-2034

Optical Interconnect Market Size and Share:

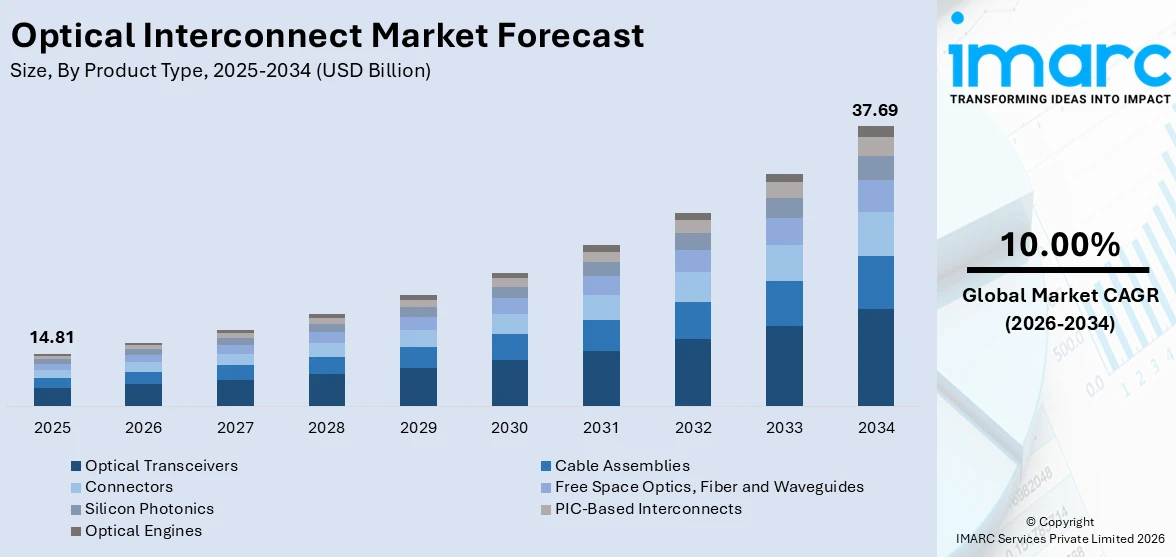

The global optical interconnect market size was valued at USD 14.81 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 37.69 Billion by 2034, exhibiting a CAGR of 10.00% from 2026-2034. North America currently dominates the market, holding a market share of 38% in 2025. The region benefits from a strong technology ecosystem, widespread deployment of hyperscale data centers, robust demand for high-speed networking solutions, and continuous investments in advanced optical technologies and semiconductor manufacturing capabilities, all contributing to the optical interconnect market share.

The increasing global demand for high-speed data transmission is a primary driver of the optical interconnect market growth. The rapid proliferation of cloud computing, big data analytics, and artificial intelligence applications has intensified the need for scalable and efficient networking infrastructure across industries. Rising internet traffic volumes, fueled by streaming services, remote work adoption, and connected devices, necessitate continuous upgrades to optical communication systems. Additionally, the widespread rollout of 5G networks demands robust backhaul and fronthaul infrastructure, further propelling the adoption of optical interconnects. Growing investments in smart city initiatives and industrial automation are creating new opportunities for fiber-based connectivity solutions. Moreover, the shift from traditional copper-based interconnects to optical alternatives, driven by their superior bandwidth capacity and energy efficiency, is reinforcing long-term demand across telecommunications, enterprise, and defense sectors globally.

The United States has emerged as a major region in the optical interconnect market owing to many factors. The country leads globally in hyperscale data center development, with unprecedented levels of investment driving large-scale construction activity across multiple states. This massive infrastructure buildout directly drives demand for advanced optical interconnect solutions to facilitate high-speed, low-latency data transmission within and between these facilities. The rapid deployment of AI training clusters, which require extensive GPU networks exchanging data at terabit-scale throughput, has accelerated the transition from electrical to optical interconnects. Furthermore, government-backed broadband expansion programs are supporting fiber network growth across underserved regions, thereby strengthening the broader optical connectivity infrastructure nationwide. The increasing adoption of cloud computing, edge processing, and real-time analytics platforms is further reinforcing the need for scalable and energy-efficient optical interconnect architectures throughout the country.

To get more information on this market Request Sample

Optical Interconnect Market Trends:

AI-Driven Data Center Expansion Fueling Demand

The explosive growth of artificial intelligence workloads is fundamentally reshaping data center architectures and driving unprecedented demand for optical interconnect solutions. Training frontier AI models requires thousands of GPUs exchanging data at terabit-scale, and optical links reduce latency while dramatically improving energy-per-bit efficiency compared to traditional copper interconnects. This surge in AI-related infrastructure investment is compelling hyperscale operators to adopt advanced optical solutions at an accelerated pace. For instance, in 2025, the datacom optical component market grew over 60% to exceed USD 16 billion in revenue, driven primarily by continued growth in 400G and 800G transceiver shipments for AI backend networks. The transition toward larger AI clusters with increasingly complex interconnect fabrics is creating sustained demand for high-bandwidth optical modules across both scale-out and scale-up network configurations, positioning optical interconnects as essential components in modern computing infrastructure.

Silicon Photonics Integration Advancing Connectivity

Silicon photonics technology is redefining the optical interconnect market outlook by enabling the integration of lasers, modulators, and detectors on CMOS-compatible platforms at scale. This approach significantly reduces cost per bit while allowing seamless integration with switch application-specific integrated circuits and accelerators used in modern data centers. Co-packaged optics solutions built on silicon photonics platforms are demonstrating substantial power savings and improved link reliability, making them particularly attractive for energy-intensive AI workloads. For instance, at GTC 2025, co-packaged silicon photonics switch systems were unveiled that deliver 3.5 times lower power consumption compared to traditional pluggable optical transceivers, along with improved network resiliency. The convergence of photonics with advanced semiconductor packaging techniques is accelerating commercial deployment timelines, with multiple hyperscale operators actively qualifying co-packaged optics solutions for production environments expected to scale significantly over the coming years.

Rapid Transition to Higher-Speed Optical Transceivers

The optical interconnect industry is experiencing an accelerated transition from 400G to 800G and emerging 1.6T optical transceivers, driven by the bandwidth requirements of AI training clusters and hyperscale cloud infrastructure. This migration represents a fundamental shift in the optical interconnect market forecast as operators seek to maximize cost-per-bit efficiency on each installed fiber. The standardization of OSFP-XD as the primary 1.6T carrier has provided procurement clarity for organizations planning multi-year infrastructure upgrades. For instance, in 2025, shipments of 800G optical transceivers achieved a 100% year-on-year increase, with approximately 34.5 million optical transceivers deployed globally across data center environments. The roadmap toward even higher data rates underscores the continuous innovation cycle within the transceiver segment, ensuring sustained demand as operators progressively upgrade their networking infrastructure to accommodate growing computational requirements.

Optical Interconnect Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global optical interconnect market, along with forecast at the global and regional levels from 2026-2034. The market has been categorized based on product type, interconnect level, fiber mode, application, and end-use industry.

Analysis by Product Type:

- Cable Assemblies

- Indoor Cable Assemblies

- Outdoor Cable Assemblies

- Active Optical Cables

- Multi-Source Agreement

- QSFP

- CXP

- CFP

- CDFP

- Connectors

- LC Connectors

- SC Connectors

- ST Connectors

- MPO/MTP Connectors

- Optical Transceivers

- Free Space Optics, Fiber and Waveguides

- Silicon Photonics

- PIC-Based Interconnects

- Optical Engines

Optical transceivers hold 35% of the market share. Optical transceivers serve as the fundamental building blocks for transmitting and receiving data across fiber-optic networks, enabling high-speed communication in data centers, telecommunications, and enterprise environments. These components convert electrical signals into optical signals and vice versa, facilitating seamless data transmission over varying distances. The segment benefits from the growing adoption of cloud computing, streaming services, and bandwidth-intensive AI applications that necessitate continuous upgrades in networking capacity. The rising demand for higher throughput and lower latency across modern digital infrastructure is accelerating the deployment of next-generation transceiver modules worldwide. The versatility of optical transceivers in supporting multiple data rates and form factors, including QSFP-DD and OSFP configurations, ensures their compatibility across diverse infrastructure deployments. Their role in both pluggable and emerging co-packaged architectures further reinforces their importance as the market transitions toward higher-speed interconnect solutions catering to evolving enterprise and hyperscale networking demands.

Analysis by Interconnect Level:

- Chip- & Board-Level Interconnect

- Board-To-Board and Rack-Level Optical Interconnect

- Metro & Long Haul Optical Interconnect

Chip- & board-level interconnect leads the market with a share of 38%. Chip- and board-level optical interconnects route light signals directly across a single chip or between closely positioned components, providing the fastest and highest-bandwidth connections inside processors and AI accelerators. By replacing traditional electrical traces, these interconnects significantly reduce power consumption and signal degradation, which are critical limitations in high-density computing environments. The growing complexity of AI training workloads and the emergence of chiplet-based architectures have intensified the need for efficient intra-chip and inter-chip communication pathways. For instance, in December 2024, a leading optical chiplet developer raised USD 155 million to scale production of optical interconnect chiplets, supported by major semiconductor companies and foundries. The integration of photonic components directly into processor packages enables new system designs that eliminate traditional bottleneck points, supporting higher aggregate bandwidth while consuming less energy per bit transferred across computing elements.

Analysis by Fiber Mode:

- Multi-Mode Fiber

- Step Index Multi-Mode Fiber

- Graded Index Multi-Mode Fiber

- Single-Mode Fiber

Multi-mode fiber dominates the market, with a share of 52%. Multi-mode fiber optical interconnects are widely utilized for short-distance data transmissions within data centers, enterprise campuses, and high-performance computing environments. These fibers allow simultaneous transmission of multiple light signals through the core, improving bandwidth density and scalability in applications where distances are typically within a few hundred meters. The growing demand for cloud computing infrastructure and the rapid expansion of hyperscale data centers continue to drive adoption of multi-mode fiber solutions, particularly for intra-rack and inter-rack connectivity. The development of bend-insensitive fiber variants has further enhanced deployment flexibility in high-density and space-constrained environments, improving network resilience and reducing signal degradation risks. The cost-effectiveness and ease of installation associated with multi-mode fiber systems make them a preferred choice for short-reach applications, while ongoing advances in fiber technology enhance their performance capabilities for next-generation networking requirements across both enterprise and hyperscale infrastructure deployments.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

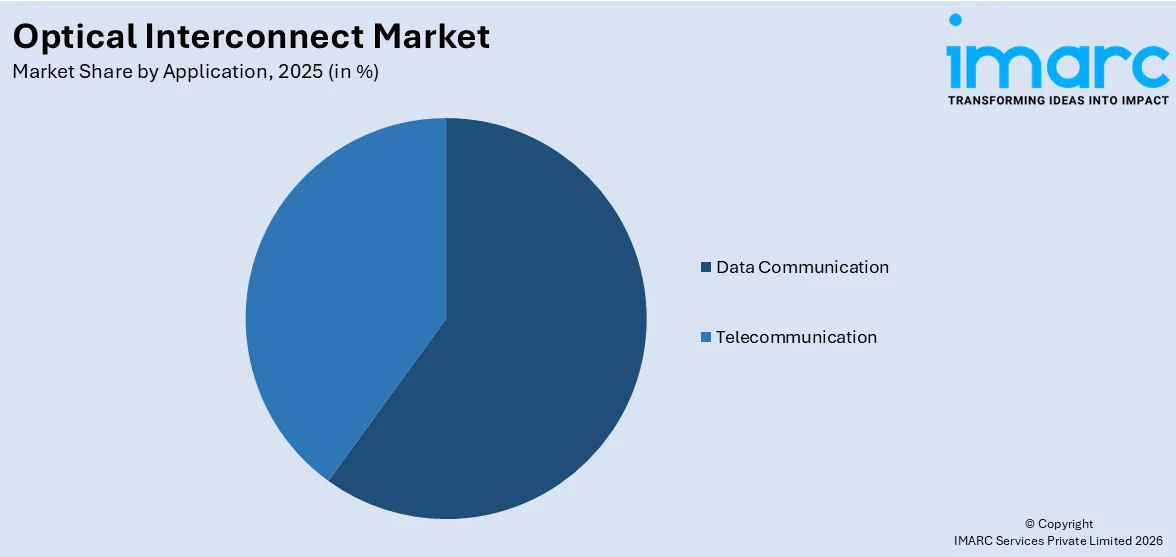

- Data Communication

- Data Center

- High-Performance Computing (HPC)

- Telecommunication

Data communication represents the leading segment, with a market share of 60%. The data communication segment encompasses optical interconnect solutions deployed within data centers and high-performance computing environments, where ultra-fast and scalable connectivity is essential to support massive data throughput and low-latency processing requirements. The booming demand from hyperscale data centers, the growing reliance on AI and machine learning analytics, and the expanding adoption of cloud services are collectively reinforcing the dominance of this segment. The unprecedented pace of data center infrastructure expansion worldwide, driven by rising computational workloads and digital transformation initiatives, continues to create strong demand for high-bandwidth optical solutions. Enterprise and service providers continue to expand their digital infrastructure across cloud and edge computing environments, necessitating higher-bandwidth optical interconnect solutions. The increasing integration of optical technologies into AI backend networks underscores the critical role of data communication applications in driving overall market expansion and supporting next-generation connectivity architectures.

Analysis by End-Use Industry:

- Military and Aerospace

- Consumer Electronics

- Automotive

- Chemicals

- Others

Consumer electronics holds 30% of the market share. The consumer electronics segment encompasses a broad range of devices including smartphones, gaming consoles, virtual reality headsets, and high-definition display systems that increasingly rely on optical interconnect technologies for enhanced performance and data transfer capabilities. The growing consumer demand for immersive experiences, ultra-high-definition streaming, and low-latency gaming is driving the integration of advanced optical components into next-generation consumer devices. The ongoing development of high-speed multimode optical platform components, including advanced laser drivers and transimpedance amplifiers, is enabling higher data throughput within compact consumer device architectures. The miniaturization of optical interconnect elements and improvements in energy efficiency are expanding their adaptability within compact consumer form factors. Additionally, the convergence of augmented reality, virtual reality, and mixed reality technologies is creating new pathways for optical interconnects in consumer electronics, supporting the transition toward more immersive and responsive user experiences.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- Europe

- Asia Pacific

- Middle East and Africa

- Latin America

North America, accounting for 38% of the share, enjoys the leading position in the market. The region benefits from a mature technology ecosystem, the presence of leading semiconductor and networking companies, and substantial investments in data center infrastructure that drive continuous demand for advanced optical interconnect solutions. The rapid adoption of AI workloads across hyperscale data centers and the transition to higher-speed networking standards are reinforcing regional dominance in optical connectivity markets. The expanding deployment of wavelength-division multiplexing equipment and growing direct procurement by cloud providers are contributing to sustained growth in optical transport solutions across the region. The deployment of 5G networks, expansion of edge computing facilities, and increasing government support for broadband infrastructure further strengthen the demand landscape. Additionally, collaborative innovation between research institutions, semiconductor foundries, and system integrators ensures continued technological advancement in optical interconnect solutions across the region, positioning it at the forefront of next-generation connectivity development.

Key Regional Takeaways:

United States Optical Interconnect Market Analysis

The United States represents the largest national market for optical interconnects, driven by its leadership in cloud computing, artificial intelligence, and advanced semiconductor technologies. The country hosts the majority of global hyperscale data centers, with major technology companies continuously expanding their infrastructure to accommodate growing AI training and inference workloads. The ongoing buildout of large-scale AI clusters requiring terabit-scale GPU-to-GPU connectivity is accelerating demand for high-bandwidth optical solutions. For instance, lenders committed USD 121 billion in credit for data center properties in the United States in 2025, reflecting the unprecedented scale of infrastructure investment supporting optical interconnect demand. Government initiatives promoting domestic semiconductor manufacturing and broadband expansion further stimulate market activity. The growing emphasis on energy-efficient networking solutions and the transition from copper to optical interconnects across enterprise and government networks are creating additional growth avenues, while the presence of leading optical component manufacturers and research institutions ensures sustained innovation in product development.

Europe Optical Interconnect Market Analysis

Europe presents a steadily growing market for optical interconnects, supported by extensive 5G network deployments, ambitious digital infrastructure goals, and expanding data center development across key markets including Germany, the United Kingdom, the Netherlands, and Ireland. Major cloud service providers are expanding their European data center footprints, driving demand for high-performance optical connectivity solutions to handle large-scale data processing with minimal latency and improved energy efficiency compared to traditional copper-based interconnects. The ongoing expansion of fiber-to-the-home networks across European Union member states is accelerating the foundation for advanced optical networking, with an increasing number of countries achieving high levels of full fiber coverage. Regulatory mandates to transition from legacy copper networks to modern fiber infrastructure are further reinforcing long-term demand for optical connectivity solutions across the region. Additionally, growing investment in smart city projects, industrial automation, and research initiatives in quantum computing and photonics integration are expanding the addressable market for optical interconnect solutions across the region.

Asia-Pacific Optical Interconnect Market Analysis

Asia-Pacific is emerging as the fastest-growing regional market for optical interconnect market trends, driven by massive investments in data center infrastructure, 5G network deployments, and semiconductor manufacturing expansion across China, Japan, South Korea, and Taiwan. The region's strong electronics manufacturing base facilitates rapid scaling of photonic packaging and module assembly capabilities. Major semiconductor companies are establishing dedicated silicon photonics research and development facilities across key manufacturing hubs in the region, strengthening the overall optical interconnect ecosystem. Government support for advanced manufacturing, increasing demand for cloud services, and the rapid digitization of industries are collectively driving sustained growth in optical connectivity solutions across the region.

Latin America Optical Interconnect Market Analysis

Latin America presents a developing market for optical interconnects, supported by increasing investments in telecommunications infrastructure, 5G deployment initiatives, and data center expansion across major economies including Brazil and Mexico. The rising adoption of cloud computing services and growing internet penetration are driving demand for high-speed connectivity solutions. Large-scale investment commitments to accelerate the nationwide deployment of fiber optic networks across key economies are strengthening the regional optical infrastructure landscape. Government-led broadband initiatives and private sector partnerships are helping bridge the digital divide, creating new opportunities for optical interconnect adoption across telecommunications and enterprise segments.

Middle East and Africa Optical Interconnect Market Analysis

The Middle East and Africa region shows significant growth potential for optical interconnects, driven by investments in cloud computing, 5G infrastructure, and smart city initiatives. The UAE and Saudi Arabia are leading regional demand through large-scale digital transformation programs and data center development projects. The rapid expansion of data center capacity worldwide is positioning the Middle East as a key growth hub, with Gulf states emerging as prominent destinations for next-generation AI infrastructure development. Rising broadband penetration and government-led connectivity programs across African nations are gradually expanding the addressable market for optical interconnect technologies in the region.

Competitive Landscape:

The global optical interconnect market exhibits a moderately consolidated competitive structure, with established semiconductor and networking companies investing heavily in research and development to maintain technological leadership. Key market participants are focusing on strategic partnerships, product portfolio expansion, and manufacturing capacity enhancements to capitalize on the surging demand driven by AI infrastructure buildout and data center modernization. The growing emphasis on co-packaged optics, silicon photonics integration, and higher-speed transceiver development is intensifying competitive dynamics, as companies seek to deliver solutions that address the bandwidth, power efficiency, and scalability requirements of next-generation AI clusters. Several leading players are pursuing vertical integration strategies, securing critical supply chain components such as indium phosphide wafer fabrication and advanced optical engine production. Collaborative initiatives between component manufacturers, system integrators, and hyperscale cloud operators are shaping industry standards and accelerating the commercialization of innovative optical interconnect architectures.

The report provides a comprehensive analysis of the competitive landscape in the optical interconnect market with detailed profiles of all major companies, including:

- Finisar

- Mellanox Technologies

- Molex

- Oclaro

- Sumitomo Electric Industries

- Broadcom

- TE Connectivity

- Amphenol

- Juniper Networks

- Fujitsu

- Infinera Corporation

- Lumentum Holdings

- OFS Fitel, LLC (FURUKAWA ELECTRIC CO., LTD)

- 3M Company

- Acacia Communication

- Dow Corning

- Huawei

- Intel

- Infineon Technologies

Optical Interconnect Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered |

|

| Interconnect Levels Covered | Chip- & Board-Level Interconnect, Board-To-Board and Rack-Level Optical Interconnect, Metro & Long Haul Optical Interconnect |

| Fiber Modes Covered | Multi-Mode Fiber (Step Index Multi-Mode Fiber, Graded Index Multi-Mode Fiber), Single-Mode Fiber |

| Applications Covered | Data Communication (Data Center, High-Performance Computing (HPC)), Telecommunication |

| End Use Industries Covered | Military and Aerospace, Consumer Electronics, Automotive, Chemicals, Others |

| Region Covered | North America, Europe, Asia Pacific, Middle East and Africa, Latin America |

| Companies Covered | Finisar, Mellanox Technologies, Molex, Oclaro, Sumitomo Electric Industries, Broadcom, TE Connectivity, Amphenol, Juniper Networks, Fujitsu, Infinera Corporation, Lumentum Holdings, OFS Fitel, LLC (FURUKAWA ELECTRIC CO., LTD), 3M Company, Acacia Communication, Dow Corning, Huawei, Intel, Infineon Technologies, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the optical interconnect market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global optical interconnect market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the optical interconnect industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Optical Interconnect Market Report

The optical interconnect market was valued at USD 14.81 Billion in 2025.

The optical interconnect market is projected to exhibit a CAGR of 10.00% during 2026-2034, reaching a value of USD 37.69 Billion by 2034.

The optical interconnect market is primarily driven by the rapid expansion of hyperscale data centers, growing demand for AI and high-performance computing infrastructure, the global rollout of 5G networks requiring robust backhaul systems, increasing adoption of cloud computing and big data analytics, and the transition from copper-based to optical interconnect solutions offering superior bandwidth and energy efficiency.

North America currently dominates the optical interconnect market, accounting for a share of 38%. The region benefits from its advanced technology infrastructure, concentration of hyperscale data centers, strong semiconductor ecosystem, and continuous investment in AI-driven networking solutions.

Some of the major players in the optical interconnect market include Finisar, Mellanox Technologies, Molex, Oclaro, Sumitomo Electric Industries, Broadcom, TE Connectivity, Amphenol, Juniper Networks, Fujitsu, Infinera Corporation, Lumentum Holdings, OFS Fitel, LLC (FURUKAWA ELECTRIC CO., LTD), 3M Company, Acacia Communication, Dow Corning, Huawei, Intel, Infineon Technologies, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)