Orthopedic Braces and Supports Market Size, Share, Trends and Forecast by Product, Type, Application, End-User, and Region, 2026-2034

Global Orthopedic Braces and Supports Market Size, Share, Trends & Forecast (2026-2034)

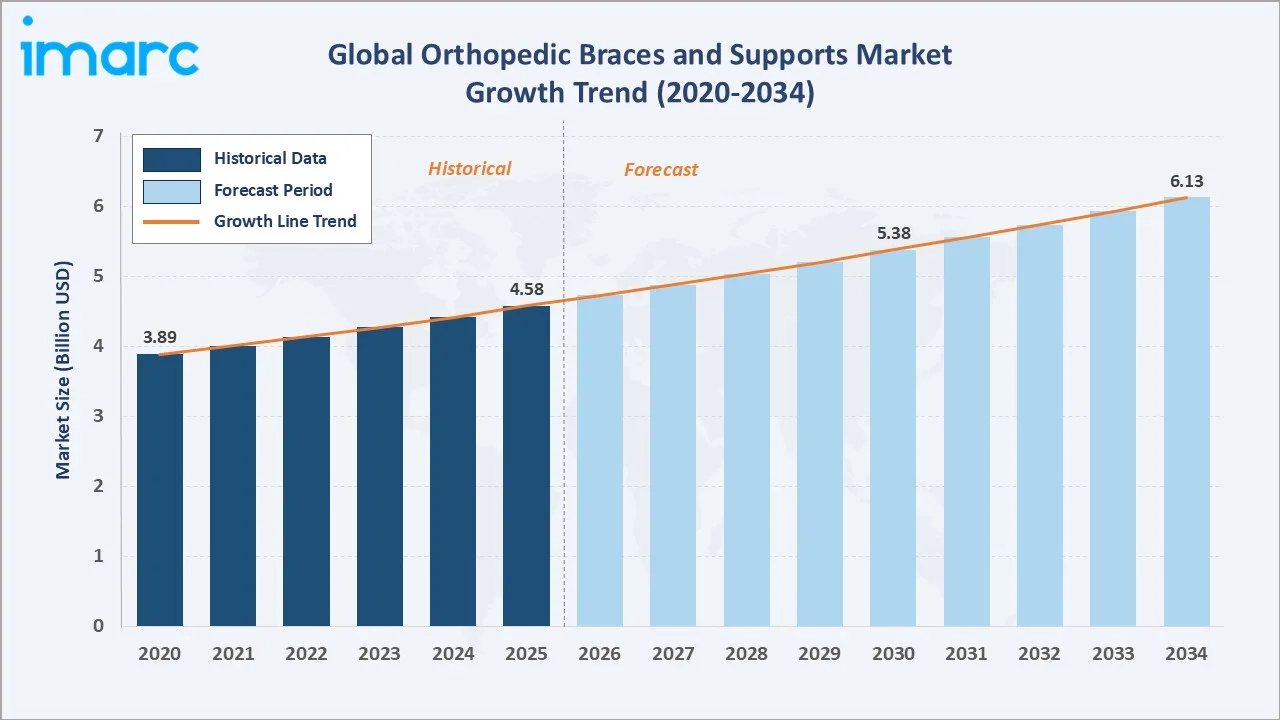

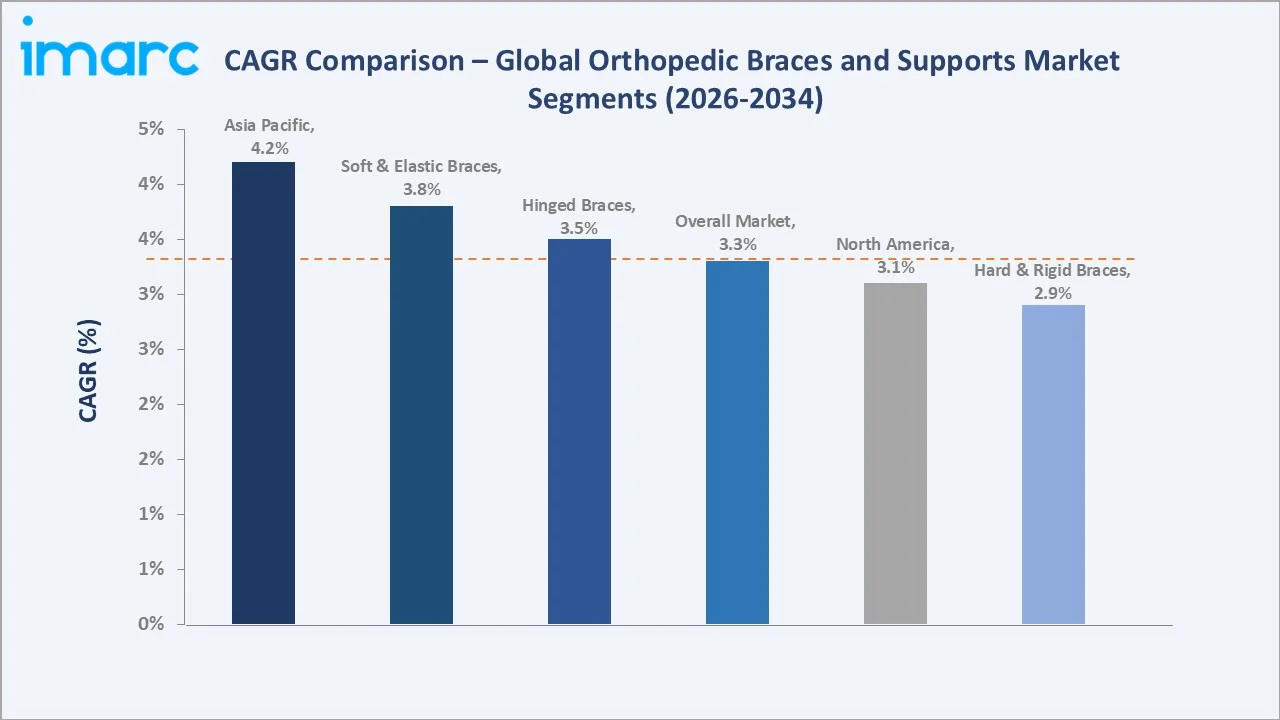

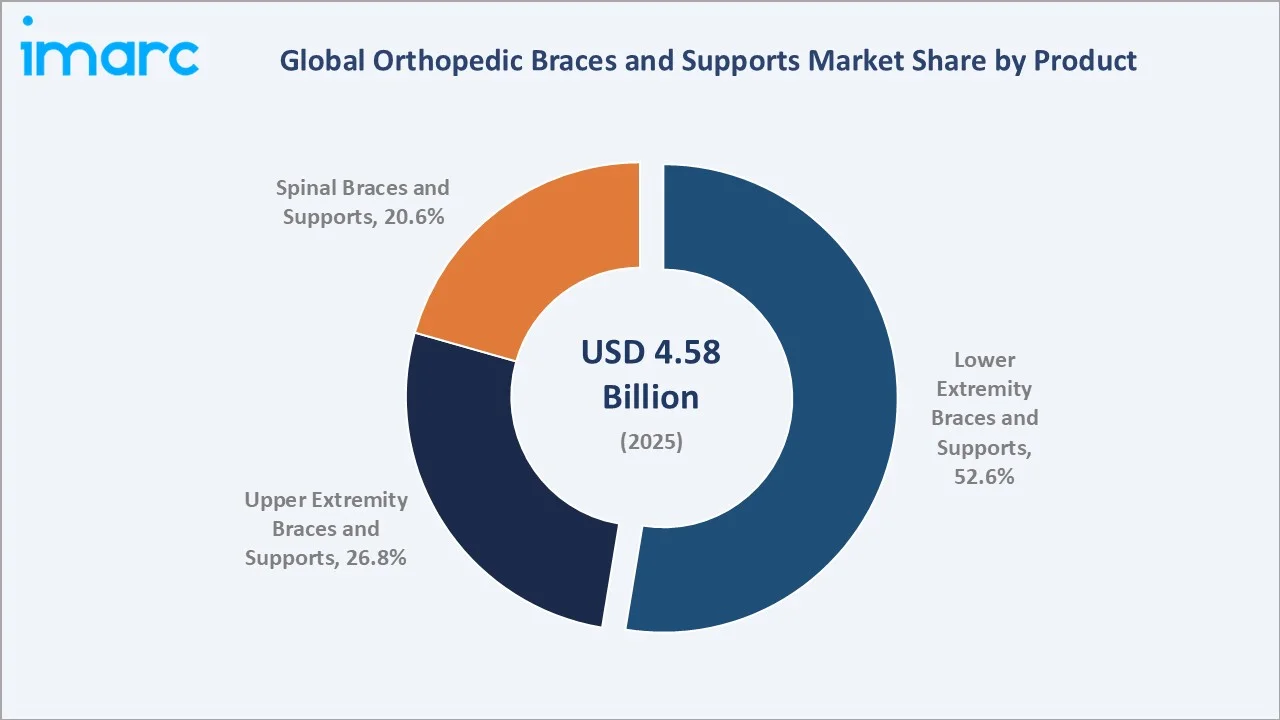

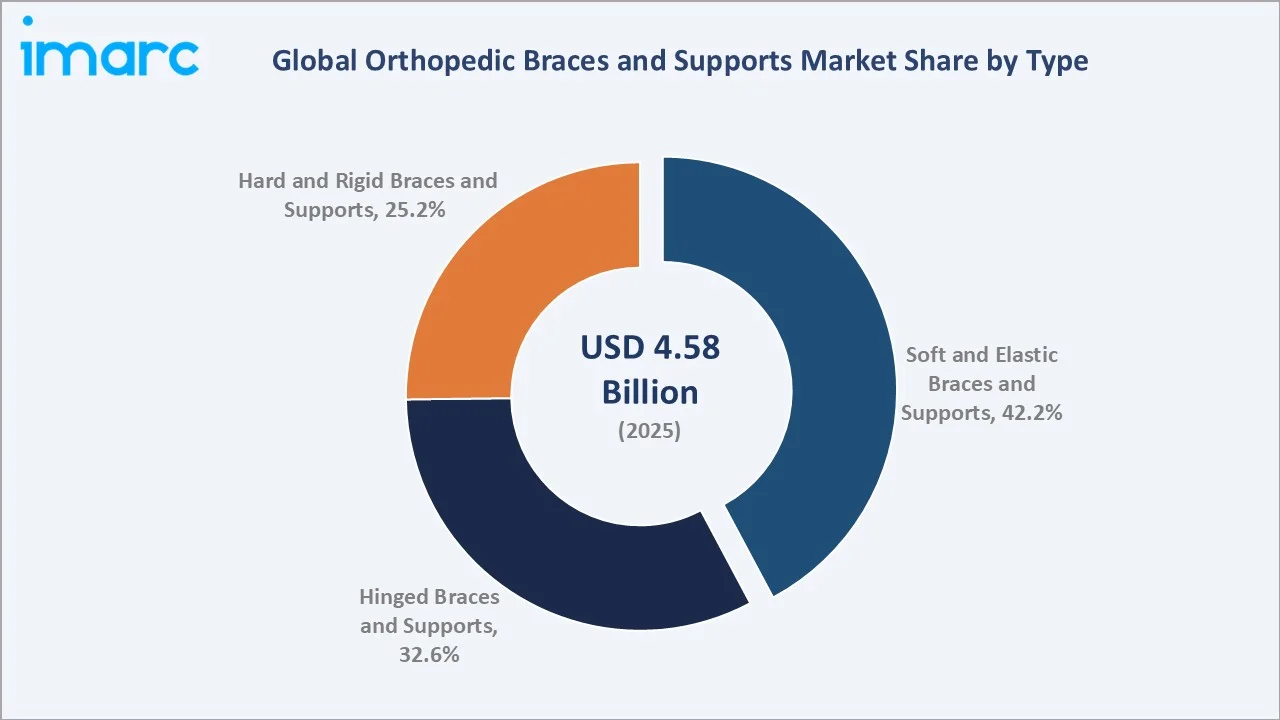

The global orthopedic braces and supports market size was valued at USD 4.58 Billion in 2025. It is projected to reach USD 6.13 Billion by 2034, exhibiting a CAGR of 3.30% during the forecast period 2026-2034. Growth is primarily driven by rising incidences of musculoskeletal disorders, an aging global population, expanding sports injury cases, and rapid material science innovations.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.58 Billion |

|

Forecast Market Size (2034) |

USD 6.13 Billion |

|

CAGR (2026-2034) |

3.30% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (44.7% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~4.2%) |

|

Leading Product Segment |

Lower Extremity Braces & Supports (52.6%, 2025) |

|

Leading Type Segment |

Soft & Elastic Braces & Supports (42.2%, 2025) |

The chart below outlines the market growth trajectory from 2020 to 2034, highlighting a transition from steady historical expansion to a more accelerated and sustained growth phase. This shift is primarily driven by evolving demographic patterns, particularly the rising aging population and increasing prevalence of musculoskeletal conditions, which continue to elevate demand for orthopedic braces and supports globally.

To get more information on this market, Request Sample

The forecast period reflects strong momentum supported by expanding healthcare infrastructure and increasing adoption of next-generation brace materials across key regions such as North America, Europe, and Asia Pacific.

Executive Summary

The global orthopedic braces and supports market is undergoing steady transformation, driven by an aging population, increased musculoskeletal disease burden, and accelerating product innovation. Valued at USD 4.58 Billion in 2025, the market is forecast to expand to USD 6.13 Billion by 2034 at a CAGR of 3.30%.

Lower extremity braces and supports dominate the product landscape at 52.6% share in 2025, reflecting the high clinical incidence of knee injuries, ankle sprains, and hip-related disorders. Soft and elastic brace types hold the largest type-level share at 42.2%, owing to their comfort, versatility, and widespread OTC availability. Hinged braces are the second-largest type at 32.6%, commanding demand from post-operative rehabilitation and sports performance segments. Hard and rigid braces account for 25.2% share, catering to trauma recovery and spinal stabilization use cases.

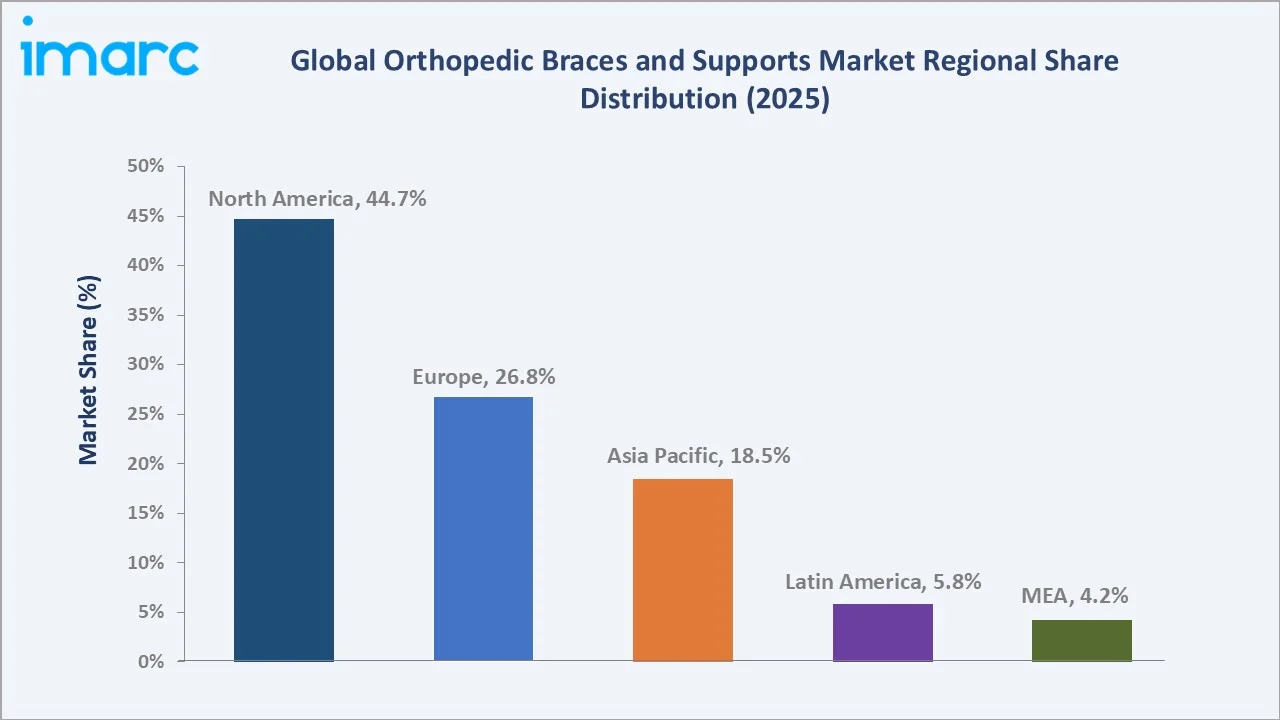

North America leads all regions at 44.7% global revenue share in 2025, underpinned by robust healthcare expenditure, high sports injury incidence, and well-developed orthopedic clinical networks. Asia Pacific is the fastest-growing region with an estimated CAGR of 4.2%, driven by expanding healthcare access, government-backed aging care programs, and growing middle-class spending on preventive health. The market outlook remains positive as technology convergence—including 3D-printed custom braces, smart sensor integration, and biodegradable materials—redefines product innovation through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Product |

Lower Extremity Braces & Supports – 52.6% share (2025) |

|

Second Product |

Upper Extremity Braces & Supports – 26.8% share (2025) |

|

Largest Type |

Soft & Elastic Braces & Supports – 42.2% share (2025) |

|

Fastest Growing Region |

Asia Pacific – ~4.2% CAGR (2026-2034) |

|

Leading Region |

North America – 44.7% revenue share (2025) |

|

Top Companies |

Embla Medical, Enovis Corporation, Bauerfeind, Breg Inc., and Aspen Medical Products |

|

Market Opportunity |

Smart wearable integration, 3D customization, Asia Pacific expansion |

The Following Bullet Points Expand on The key Data Points Above With Supporting Analysis:

- Lower Extremity Braces Lead at 52.6% (2025): Knee braces account for the largest share within this segment, driven by the high incidence of ligament injuries among athletes. Rising cases of ACL injuries continue to support strong demand from sports clinics and rehabilitation centers.

- Upper Extremity Braces at 26.8% (2025): Wrist, elbow, and shoulder braces are increasingly adopted for occupational therapy. Rising repetitive strain disorders from digital work environments are a primary volume driver for this segment.

- Soft & Elastic Type Dominates at 42.2% (2025): Consumer preference for comfort-focused, self-fit solutions is driving increased sales of soft braces through pharmacies and e-commerce channels. The growing shift toward over-the-counter products reflects rising demand for convenient and easily accessible support solutions.

- North America Holds 44.7% (2025): The Centers for Disease Control and Prevention estimates that a large number of Americans live with physician-diagnosed arthritis, creating a substantial and sustained demand base for orthopedic support products.

- Asia Pacific Fastest Growing at ~4.2% CAGR: China and India are emerging as high-volume markets due to government elder care initiatives and rising sports participation. India's sports industry reached USD 2.1 Billion in 2025.

Global Orthopedic Braces and Supports Market Overview

Orthopedic braces and supports are external medical devices designed to immobilize, restrict, align, or support injured or surgically treated musculoskeletal structures. The global market encompasses a broad product range—including knee braces, ankle supports, spinal orthoses, wrist splints, shoulder stabilizers, and elbow guards—manufactured using advanced materials such as neoprene, carbon fiber composites, thermoplastic polymers, memory foam, and hinged aluminum alloys.

The industry operates at the intersection of healthcare services, sports medicine, rehabilitation, and consumer wellness. Macroeconomic factors such as population aging, urbanization-driven lifestyle changes, rising sports participation, and increased healthcare spending are reshaping demand profiles. Product innovation—centered on 3D printing, smart sensor embedding, and biomechanically optimized designs—is elevating clinical efficacy standards. At the same time, regulatory frameworks across North America, Europe, and Asia Pacific are defining quality benchmarks, directly influencing procurement decisions in hospital and clinical channels.

Market Dynamics

To evaluate market opportunities, Request Sample

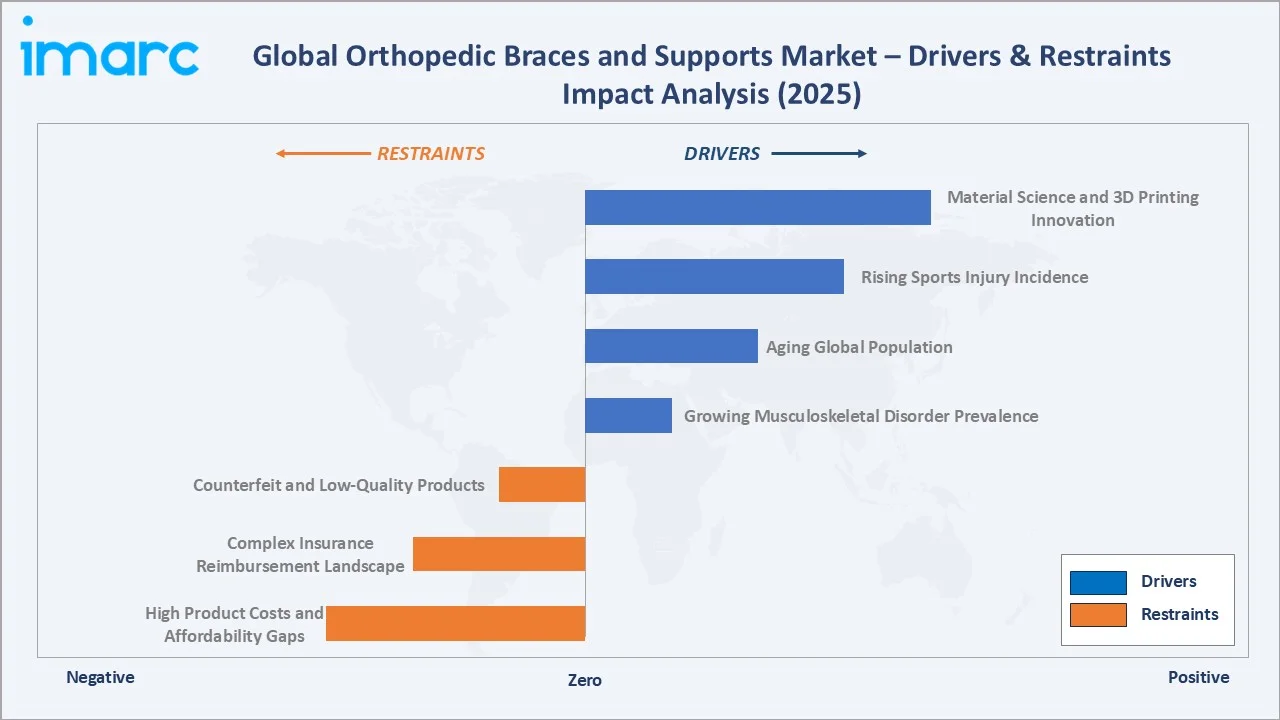

The orthopedic braces and supports market are shaped by a complex interplay of demand-side drivers, structural restraints, emerging opportunities, and persistent challenges. Understanding these dynamics is essential for stakeholders evaluating market entry, capacity expansion, and product development strategies.

Market Drivers

- Growing Musculoskeletal Disorder Prevalence: Estimates exceed 50% prevalence, or 1 in every 2 adults, and nearly 3 in every 4 adults over 65 years old have a musculoskeletal condition. Rising rates of arthritis, osteoporosis, and ligament injuries are generating consistent clinical prescription demand for bracing and support products.

- Aging Global Population: By 2050, the world’s population of people aged 60 years and older will double (2.1 billion). Older adults are disproportionately affected by joint degeneration and fracture risk, creating long-term structural demand for orthopedic support solutions in developed and emerging economies alike.

- Rising Sports Injury Incidence: The U.S. Consumer Product Safety Commission recorded a high volume of sports-related injuries in 2024. Globally, participation in recreational sports and fitness activities is expanding post-pandemic, increasing demand for both preventive bracing and post-injury rehabilitation devices.

- Material Science and 3D Printing Innovation: Technological advances in lightweight composites, carbon fiber, memory foam, and breathable polymer blends are elevating comfort and therapeutic performance. Three-dimensional printing enables precise patient-specific customization, reducing recovery times and improving compliance.

Market Restraints

- High Product Costs and Affordability Gaps: Premium custom-fitted and smart-enabled orthopedic braces remain relatively expensive, limiting adoption in price-sensitive emerging markets where out-of-pocket healthcare spending is dominant.

- Complex Insurance Reimbursement Landscape: Inconsistent reimbursement coverage across payers and regions continues to limit market adoption. Rising denial rates for durable medical equipment claims, including braces, further constrain patient access and overall market conversion.

- Counterfeit and Low-Quality Products: The proliferation of unregulated braces, especially through online retail channels undermines clinical trust and creates pricing pressure on compliant OEM manufacturers.

Market Opportunities

- Smart Wearable and IoT Integration: Embedding sensors into orthopedic braces for real-time biomechanical monitoring and telerehabilitation is emerging as a key premium product opportunity. These advanced solutions enable continuous tracking of patient movement and recovery, improving clinical outcomes and patient compliance.

- Asia Pacific Market Penetration: India’s expanding healthcare infrastructure investment and China’s growing focus on elder care are creating under-penetrated opportunities for orthopedic braces. Both markets are witnessing increasing demand driven by aging populations and improving access to medical services.

- OTC Channel Expansion: Consumer awareness and self-directed healthcare are driving growth in pharmacy and e-commerce OTC brace sales. Digital-first distribution strategies can materially reduce customer acquisition costs.

Market Challenges

- Clinical Efficacy Skepticism: Growing body of research questioning the long-term therapeutic benefit of some brace types, particularly for knee osteoarthritis (OA) may slow prescription-driven demand in certain sub-segments.

- Regulatory Compliance Complexity: Manufacturers face complex multi-jurisdictional regulatory requirements, including approvals from the U.S. Food and Drug Administration, CE marking in Europe, and oversight by the Central Drugs Standard Control Organization, which collectively increase time-to-market and compliance costs.

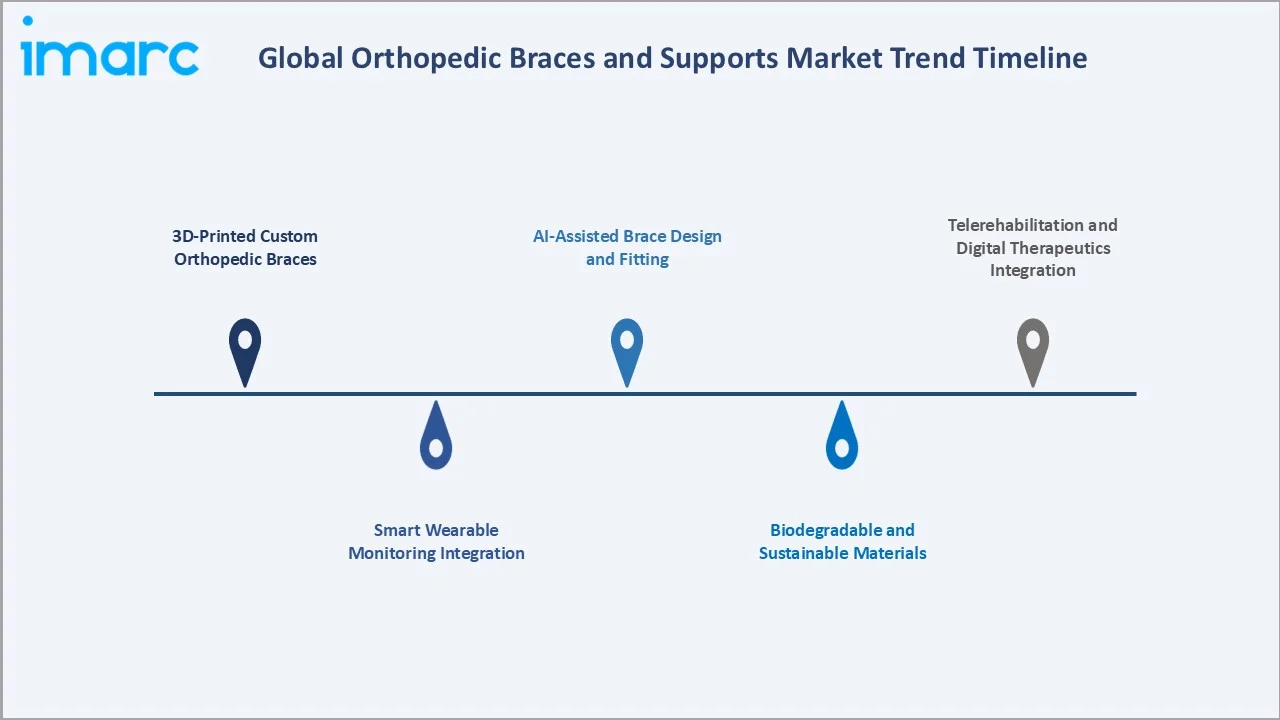

Emerging Market Trends

The orthopedic braces and supports market are being reshaped by five converging innovation and adoption trends. These trends are collectively elevating clinical outcomes, expanding consumer access, and creating new competitive differentiation vectors for leading manufacturers.

1. 3D-Printed Custom Orthopedic Braces

Three-dimensional printing is transforming brace manufacturing by enabling patient-specific designs that are lighter, more comfortable, and biomechanically superior to standard off-the-shelf solutions. Clinics and OEMs adopting point-of-care 3D printing workflows are reducing lead times from weeks to hours.

2. Smart Wearable Monitoring Integration

Next-generation braces embedded with pressure sensors, accelerometers, and Bluetooth connectivity enable real-time data collection on joint loading, range of motion, and patient compliance. This data can be transmitted to orthopedic specialists for remote monitoring, supporting telerehabilitation ecosystems.

3. Biodegradable and Sustainable Materials

Environmental sustainability concerns and regulatory pressure are motivating manufacturers to develop bio-based polymer braces that reduce plastic waste. Early-stage biodegradable orthotics using polylactic acid (PLA) composites are entering clinical trials.

4. AI-Assisted Brace Design and Fitting

Artificial intelligence algorithms trained on anatomical datasets are being deployed to automate brace size prediction, fit optimization, and pressure distribution modeling. AI integration reduces fitting errors a known contributor to non-compliance and enables mass customization at scale, particularly for high-volume OTC products.

5. Telerehabilitation and Digital Therapeutics Integration

As digital health platforms expand, orthopedic braces are becoming connected endpoints within broader virtual care ecosystems. Partnerships between brace OEMs and telehealth providers are emerging, with braces serving as data collection tools that feed into AI-powered rehabilitation protocols.

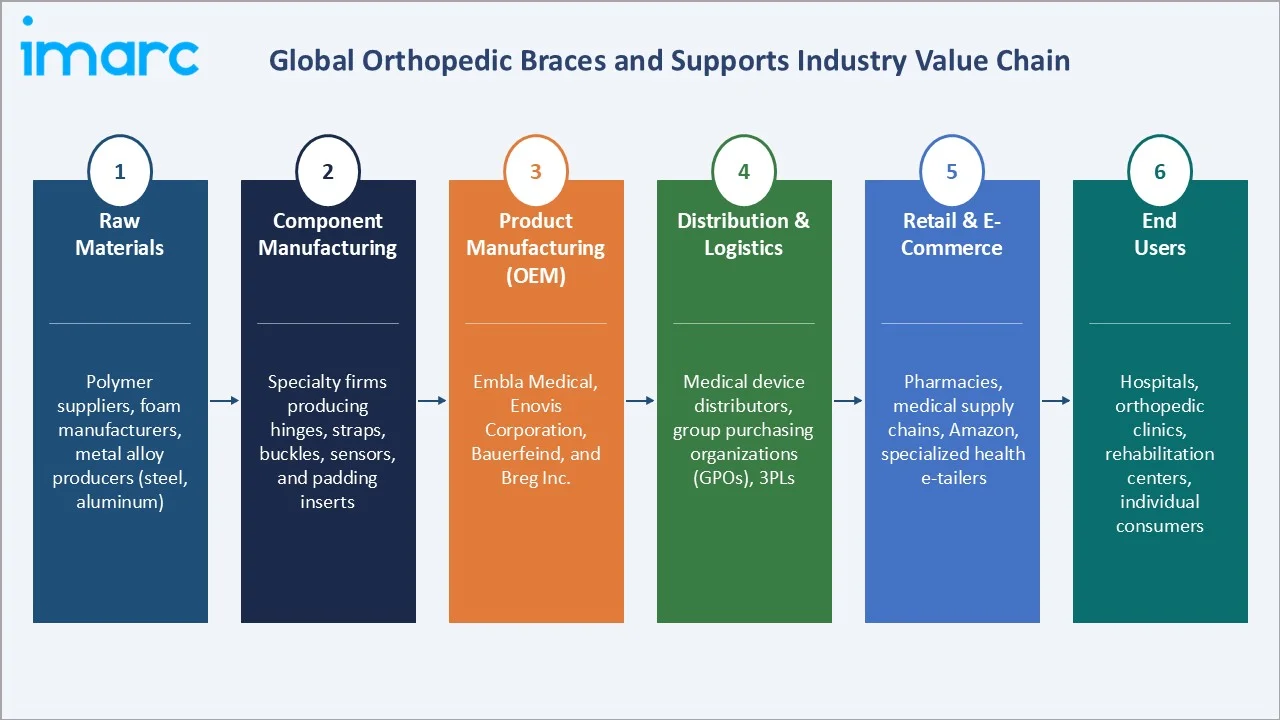

Industry Value Chain Analysis

The global orthopedic braces and supports market value chain begins with raw material suppliers and component manufacturers, followed by product design, manufacturing, and regulatory compliance.

|

Stage |

Key Players / Activities |

Value-Add |

|

Raw Materials |

Polymer suppliers, foam manufacturers, metal alloy producers (steel, aluminum) |

Supply of neoprene, carbon fiber, thermoplastics, and metal components |

|

Component Manufacturing |

Specialty firms producing hinges, straps, buckles, sensors, and padding inserts |

Precision-engineered sub-components enabling product differentiation |

|

Product Manufacturing (OEM) |

Embla Medical, Enovis Corporation, Bauerfeind, and Breg Inc |

Assembly, quality testing, regulatory certification (FDA, CE, ISO 13485) |

|

Distribution & Logistics |

Medical device distributors, group purchasing organizations (GPOs), 3PLs |

Warehousing, cold-chain management, cross-border compliance |

|

Retail & E-Commerce |

Pharmacies, medical supply chains, Amazon, specialized health e-tailers |

Consumer-facing channel enabling OTC access and DTC model growth |

|

End Users |

Hospitals, orthopedic clinics, rehabilitation centers, individual consumers |

Prescription use, physical therapy application, self-management |

Companies then move into distribution through hospitals, orthopedic clinics, rehabilitation centers, and e-commerce platforms, ensuring wide accessibility across both clinical and homecare settings.

Technology Landscape in the Orthopedic Braces and Supports Industry

Advanced Materials Innovation

Traditional neoprene and elastic fabric braces are increasingly being supplanted by high-performance alternatives including carbon fiber composites, silicone gel padding, moisture-wicking fabrics, and shape-memory polymers. Memory foam-integrated liners are reducing pressure ulcer incidence in post-operative brace users, a clinical priority highlighted in orthopedic nursing literature.

3D Printing and Customization Platforms

Additive manufacturing—primarily fused deposition modeling and selective laser sintering—is enabling clinic-level production of anatomically precise orthotic devices. Scan-to-print workflows using handheld 3D scanners allow the creation of fully customized braces within a short turnaround time.

Smart Connectivity and Sensor Integration

Embedded piezoelectric sensors, MEMS accelerometers, and IoT connectivity modules are enabling real-time biomechanical monitoring. Smart braces can track angular velocity, joint load, gait symmetry, and wear compliance—transmitting data to mobile applications and EMR systems. The clinical utility of such data in optimizing rehabilitation protocols is gaining recognition in sports medicine, with adoption growing fastest in North America and Germany.

Automation and Manufacturing Excellence

Robotic assembly lines and automated quality inspection systems are increasingly being adopted to reduce per-unit production costs and ensure consistent regulatory-compliant build quality. These advanced manufacturing approaches enhance precision, minimize human error, and support scalable production.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product | Lower Extremity Braces and Supports | 52.61% | 2025 |

| Type | Soft and Elastic Braces and Supports | 42.2% | 2025 |

| Application | Ligament Injury | 36.5% | 2025 |

| End-User | Orthopedic Clinics | 41.5% | 2025 |

| Region | North America | 44.7% | 2025 |

By Product

To access detailed market analysis, Request Sample

The product segmentation of the orthopedic braces and supports market in 2025 is defined by three major categories. Lower extremity braces dominate with 52.6% share, reflecting the clinical predominance of knee, ankle, and foot disorders. Upper extremity braces follow at 26.8%, driven by wrist, elbow, and shoulder injury management. Spinal braces hold 20.59%, anchored by post-surgical rehabilitation and degenerative spinal condition management.

By Type

The type-level segmentation reflects a spectrum from flexible consumer-grade supports to rigid clinical-grade immobilization devices. Soft and elastic braces dominate at 42.2% in 2025, favored for their comfort, washability, and OTC accessibility. Hinged braces command 32.6% share, serving mid-tier clinical applications including ligament injury recovery and sports performance protection. Hard and rigid braces account for 25.2%, concentrated in hospital and clinic procurement for post-surgical and high-force stabilization needs.

Regional Market Insights

Regional demand for orthopedic braces and supports is shaped by demographics, healthcare infrastructure maturity, regulatory environments, and sports culture. North America leads, but Asia Pacific is the primary engine of incremental growth through 2034.

|

Region |

Market Share (2025) |

Key Growth Drivers |

|

North America |

44.7% |

High sports injury incidence, aging population, strong insurance reimbursement, robust orthopedic clinical networks |

|

Europe |

26.8% |

Aging demographics, post-surgical rehab expansion, high OTC consumer awareness, EU MDR compliance driving innovation |

|

Asia Pacific |

18.5% |

Expanding healthcare access, government elder care programs, growing sports participation, rising middle-class spending |

|

Latin America |

5.8% |

Urbanization, growing sports injuries, expanding private healthcare sector in Brazil and Mexico |

|

Middle East & Africa |

4.2% |

GCC healthcare infrastructure investment, medical tourism, growing sports culture |

North America

North America dominated the global orthopedic braces and supports market in 2025 with a 44.7% revenue share. supported by a well-established healthcare infrastructure, high awareness of injury prevention, and strong adoption of advanced orthopedic solutions across both clinical and homecare settings.

Asia Pacific

Asia Pacific is the fastest-growing regional market, estimated at 18.5% global share in 2025, with an anticipated CAGR of approximately 4.2% through 2034. China represents the largest national market within the region, driven by its massive elderly populations. India is the highest-growth market within Asia Pacific, supported by rising sports participation.

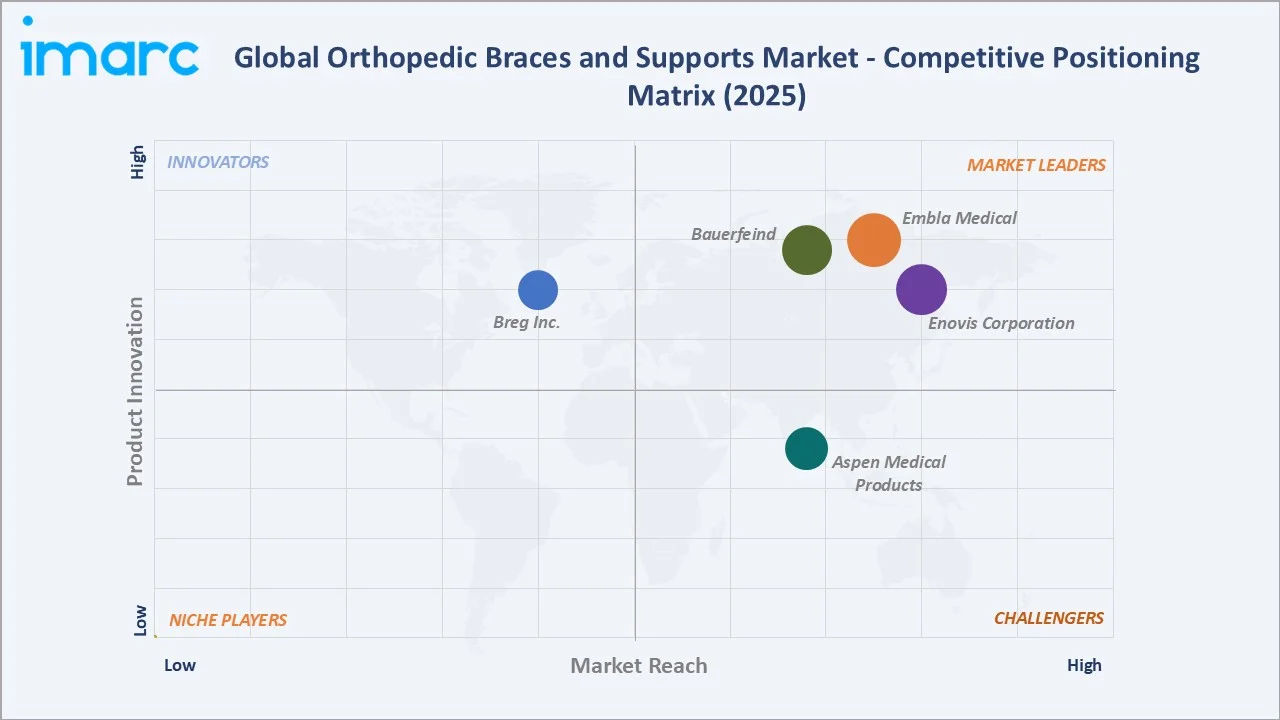

Competitive Landscape

|

Company Name |

Brand Name(s) |

Market Position |

Strategic Focus |

|

Embla Medical |

Ossur |

Leader |

Innovation-led portfolio, bionic technology, global sports partnerships |

|

Enovis Corporation |

DonJoy, Aircast, ProCare, Compex |

Leader |

Comprehensive orthopedic portfolio, strong North America clinical distribution |

|

Bauerfeind |

Bauerfeind (GenuTrain, MalleoTrain) |

Leader |

German engineering precision, evidence-based clinical positioning |

|

Breg Inc. |

Polar Care |

Challenger |

ACL/ligament specialist, sports medicine channel leadership |

|

Aspen Medical Products |

Vista, TLSO |

Challenger |

Spinal brace specialist, recent PJK brace innovation (Aug 2024) |

The global orthopedic braces and supports competitive landscape is moderately fragmented, with established global leaders competing alongside regional specialists and emerging innovators. Leading players differentiate on clinical evidence, material innovation, digital health integration, and distribution network strength. Strategic acquisitions and partnerships are reshaping competitive positioning.

Key Company Profiles

Embla Medical

Embla Medical is a global provider of non-invasive orthopedic solutions, headquartered in Reykjavik, Iceland. Established as the parent company of Össur hf, the company focuses on improving mobility through advanced bracing and supports, prosthetics, and patient care solutions.

- Product Portfolio: Embla Medical’s orthopedic braces and supports portfolio is primarily delivered through Össur and includes flagship product lines such as the Rebound, Unloader One (for knee OA), Formfit (ankle), and CTi.

- Recent Developments: In 2024, Embla Medical announced that its subsidiary Össur has signed an agreement to acquire all shares of Fior & Gentz, a specialist in advanced orthotic joint systems. This strategic acquisition strengthens Embla Medical’s position in the orthopedic braces and supports segment, particularly in high-performance lower-limb orthotic solutions such as knee-ankle-foot orthoses (KAFOs).

- Strategic Focus: Embla Medical’s strategy centers on strengthening its leadership in non-invasive orthopedics through continuous innovation in bracing technologies and patient-centric design. The company is focused on expanding in high-growth regions such as Asia-Pacific.

Enovis Corporation

Enovis Corporation is a US-based medical technology company headquartered in Wilmington, Delaware. The company focuses on orthopedic solutions, operating across prevention, rehabilitation, and surgical reconstruction segments, with a strong global footprint.

- Product Portfolio: Enovis corporation offers a orthopedic braces and supports through its flagship DonJoy brand and include product line such as the DonJoy (ligament braces), Aircast (pneumatic ankle and fracture braces), ProCare (OTC consumer line), Compex (neuromuscular electrical stimulation), and CMF Bone Growth Stimulation product lines.

- Recent Developments: In 2025, Enovis announced next-generation innovations in its orthopedic braces and supports portfolio, focusing on improving patient comfort and clinical outcomes. The company highlighted the use of advanced materials, next-generation technologies, and patient feedback-driven design to enhance usability and performance across its bracing solutions.

- Strategic Focus: Enovis is focused on integrating bracing with digital health and rehabilitation ecosystems, strengthening its leadership in sports medicine and post-acute care.

Bauerfeind

Bauerfeind is a Germany-based manufacturer of premium orthopedic braces, supports, and compression products, headquartered in Zeulenroda-Triebes. Founded in 1929, the company operates in over 20 countries and is widely recognized for its high-quality, medically certified orthopedic solutions, particularly in Europe.

- Product Portfolio: Bauerfeind’s orthopedic braces and supports portfolio includes the GenuTrain (knee braces), MalleoTrain (ankle supports), LumboTrain (back braces), and SecuTec (ligament braces) product lines.

- Recent Developments: In 2024, Bauerfeind AG announced the launch of its new AchilloTrain orthopedic support designed to treat Achilles tendon conditions, reinforcing its innovation in the orthopedic braces segment. The updated brace incorporates a high-friction massage pad and optional heel wedges to reduce strain on the tendon, improve circulation, and support healing during movement.

- Strategic Focus: Bauerfeind focuses on premiumization, clinical efficacy, and brand positioning in sports and medical rehabilitation segments. The company is investing in R&D for advanced materials and expanding its footprint in North America and Asia-Pacific.

Market Concentration Analysis

The global orthopedic braces and supports market exhibits moderate fragmentation. The top five players including Embla Medical, Enovis Corporation, Bauerfeind, Breg Inc., and Aspen Medical Products - collectively account for an estimated 35–42% of global market revenue in 2025.

A bifurcated competitive dynamic is emerging. At the premium clinical tier, consolidation is occurring around clinical evidence, proprietary material platforms, and digital health capabilities. Simultaneously, Asian manufacturers particularly from China and India are gaining share in the mid-market through cost-competitive products with improving design quality. This dual dynamic is intensifying competition across all price tiers and geographies through 2034, with premium positioning remaining the primary defense strategy for established Western OEMs.

Market consolidation activity is expected to accelerate. Merger and acquisition (M&A) activity in the broader orthopedic device space has remained consistently active in recent years, with the bracing and supports segment attracting growing interest from both strategic buyers and private equity investors seeking durable, recurring revenue profiles.

Investment & Growth Opportunities

Fastest-Growing Segments

Smart sensor-integrated braces represent the highest-growth technology opportunity within the market, with adoption accelerating in sports medicine and remote patient monitoring applications. The smart orthopedic device sub-segment is projected to witness strong growth through 2030. Soft and elastic OTC braces are emerging as the fastest-growing distribution channel sub-segment, supported by rising e-commerce penetration across North America and Europe.

Emerging Market Expansion

India represents the highest-potential emerging market, driven by rising sports participation, expanding orthopedic clinic infrastructure, and government health schemes increasing access to medical devices. The population of people over 60 years old in China is projected to reach 28% by 2040 creates a large structural demand base for lower extremity braces and spinal supports. Southeast Asia's expanding private healthcare sector and the GCC's medical tourism ecosystems collectively represent significant volume growth opportunities for manufacturers with established regional distribution.

Venture and Strategic Investment Trends

Venture capital and strategic investment in the orthopedic wearable and digital health intersection is accelerating. Key investment focus areas include IoT-enabled brace platforms, AI-assisted custom fit technologies, biodegradable material R&D, and telerehabilitation integration. Corporate venture arms of medical device conglomerates are targeting early-stage companies developing sensor-embedded orthotic platforms, as the convergence of orthopedics and digital health creates scalable, recurring revenue business models.

Future Market Outlook (2026-2034)

The global orthopedic braces and supports market is projected to expand steadily from USD 4.58 Billion in 2025 to USD 6.13 Billion by 2034, representing a CAGR of 3.30%. North America will retain regional leadership throughout the forecast period.

Three structural shifts will define the market through 2034. First, smart orthopedic convergence will embed sensor-based monitoring into mainstream brace products, with connected devices becoming standard in new clinical prescriptions by 2028–2030.

Second, 3D printing and AI-assisted design are expected to transform manufacturing economics, enabling cost-effective mass customization for both clinical and OTC applications. Additionally, Asian manufacturers particularly Chinese and Indian OEMs are anticipated to reach premium design and quality standards by the end of the decade, intensifying global competition and potentially displacing mid-range Western products in emerging markets.

Regulatory evolution will play an important role. Tightening Class II medical device requirements in major markets is expected to increase compliance costs while simultaneously creating stronger competitive moats for certified industry leaders. In parallel, the convergence of ESG priorities with medical device procurement particularly in European institutional markets is likely to accelerate demand for sustainable and biodegradable brace materials toward the end of the decade.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024–2025 with orthopedic braces and supports industry stakeholders, including product directors at OEM manufacturers, procurement managers at hospital systems and orthopedic group practices, retail buyers at medical supply chains, physical therapists, orthopedic surgeons, and institutional investors in medical device companies. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines.

Secondary Research

Secondary sources include WHO global musculoskeletal disorder prevalence reports, U.S. CDC arthritis and chronic disease statistics, U.S. Census Bureau health expenditure data, EU MDR regulatory publications, company annual reports and investor presentations, trade publications including Orthopaedic Business News and Medical Device and Diagnostic Industry (MD+DI), and regional orthopedic association databases.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models. Top-down analysis incorporated global healthcare expenditure indices, aging population projections, and musculoskeletal disease burden trajectories. Bottom-up modeling aggregated product-level demand by region, end-user segment, and distribution channel. Scenario analysis—encompassing base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty, regulatory shifts, and technology adoption velocity risks.

Orthopedic Braces and Supports Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Lower Extremity Braces and Supports, Spinal Braces and Supports, Upper Extremity Braces and Supports |

| Types Covered | Soft and Elastic Braces and Supports, Hinged Braces and Supports, Hard and Rigid Braces and Supports |

| Applications Covered | Ligament Injury, Preventive Care, Post-Operative Rehabilitation, Osteoarthritis, Others |

| End Users Covered | Orthopedic Clinics, Hospitals and Surgical Centers, Over-The-Counter (OTC) Platforms, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Embla Medical, Enovis Corporation, Bauerfeind, Breg Inc., Aspen Medical Products, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the orthopedic braces and supports market from 2020-2034.

- The orthopedic braces and supports market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the orthopedic braces and supports industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Orthopedic Braces and Supports Market Report

The global orthopedic braces and supports market was valued at USD 4.58 Billion in 2025, driven by rising musculoskeletal disorders, aging populations, and growing sports injury incidence worldwide.

The market is projected to reach USD 6.13 Billion by 2034, growing at a CAGR of 3.30% during 2026-2034, supported by demographic trends, material innovation, and smart device adoption.

Lower extremity braces and supports lead with a 52.6% share in 2025, driven by high clinical incidence of knee, ankle, and foot disorders, and expanding OTC channel penetration.

Soft and elastic braces and supports hold the largest type share at 42.2% in 2025, preferred for comfort, versatility, and OTC availability across pharmacy and e-commerce channels.

North America dominates with 44.7% revenue share in 2025, driven by high sports injury rates, aging demographics, strong insurance reimbursement, and advanced healthcare infrastructure.

Asia Pacific is the fastest-growing region at an estimated 4.2% CAGR through 2034, fueled by China's aging population, India's sports infrastructure expansion, and government elder care programs.

Key drivers include the rising global burden of musculoskeletal disorders, aging demographics, increasing incidence of sports-related injuries, ongoing advancements in material science, and the growing adoption of 3D printing–enabled customization.

Major players include Embla Medical, Enovis Corporation, Bauerfeind, Breg Inc., and Aspen Medical Products.

Key technologies include 3D-printed custom orthotics, smart sensor integration for real-time biomechanical monitoring, AI-assisted fit design, biodegradable materials, and telerehabilitation connectivity.

Investment opportunities include smart wearable brace platforms, Asia Pacific market expansion, OTC e-commerce channel growth, biodegradable material R&D, and AI-driven orthotic customization solutions.

Soft and elastic braces and supports account for 42.2% of global market share in 2025, with the segment benefiting from strong OTC demand growth estimated at 6.3% year-over-year in 2024.

North America's orthopedic braces market was valued at approximately USD 2.05 Billion in 2025, with growth supported by high arthritis prevalence.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)