Osmometers Market Size, Share, Trends and Forecast by Product Type, Sampling Capacity, Application, End User, and Region, 2026-2034

Osmometers Market Size, Share, Trends & Forecast (2026-2034)

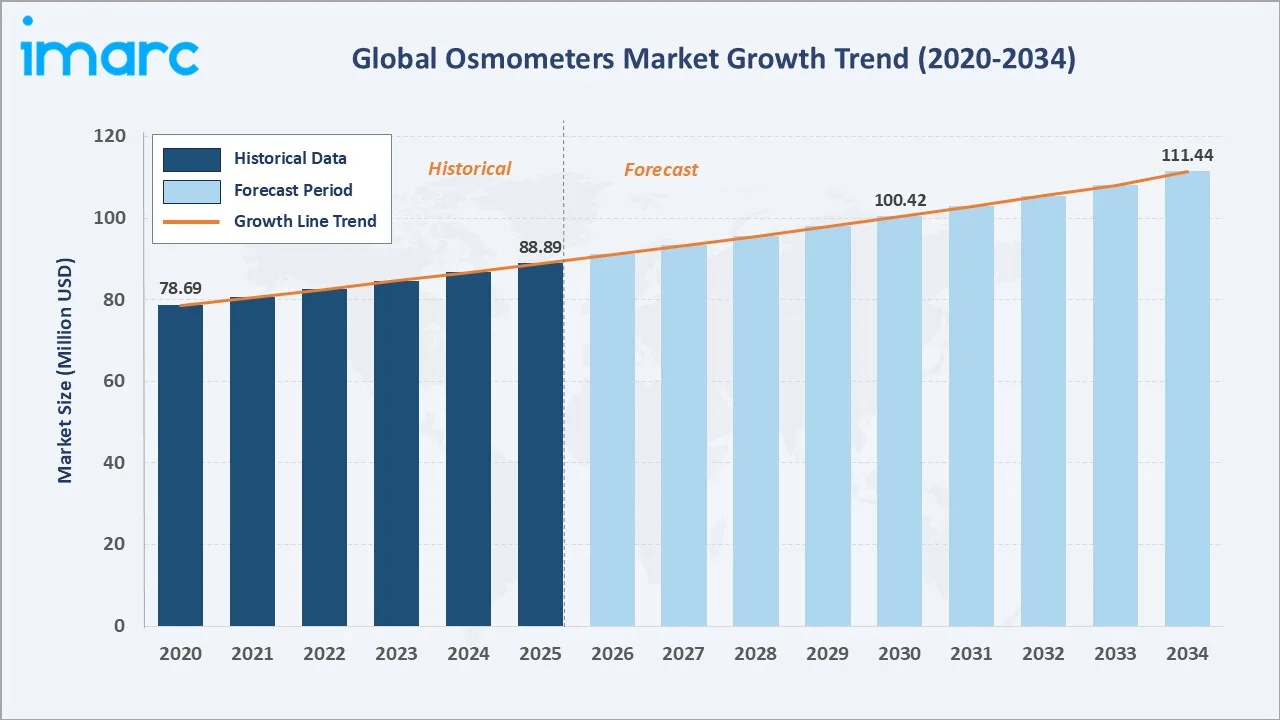

The global osmometers market size reached USD 88.89 Million in 2025 and is projected to reach USD 111.44 Million by 2026-2034, exhibiting a CAGR of 2.47% during 2026-2034. Rising prevalence of chronic diseases, pharmaceutical quality control demand, technological advancements, and expanding diagnostic laboratories are the primary growth forces shaping this market.

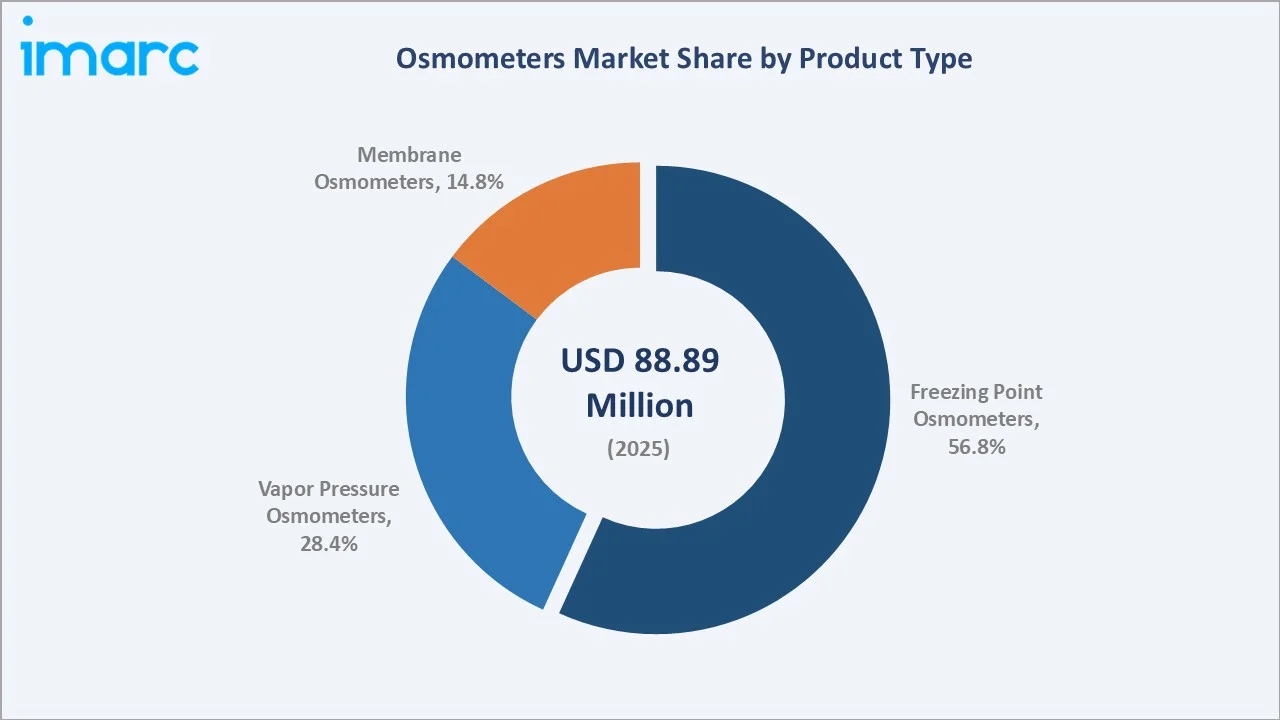

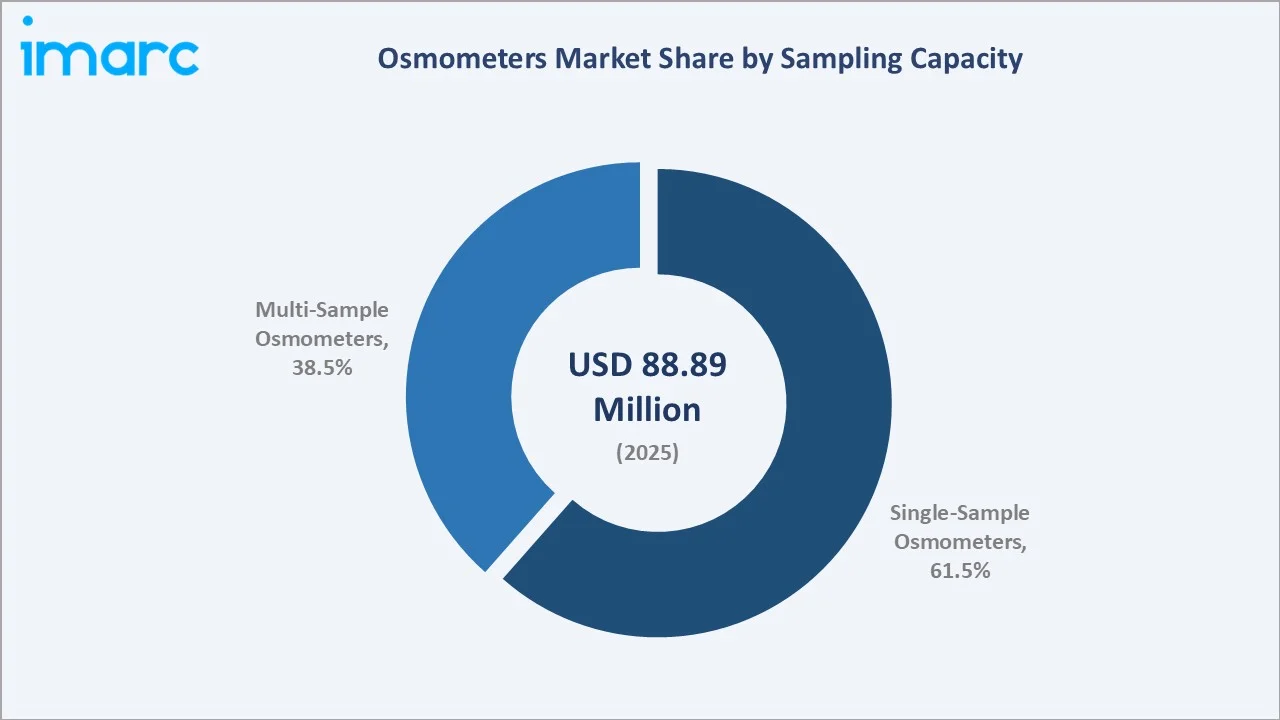

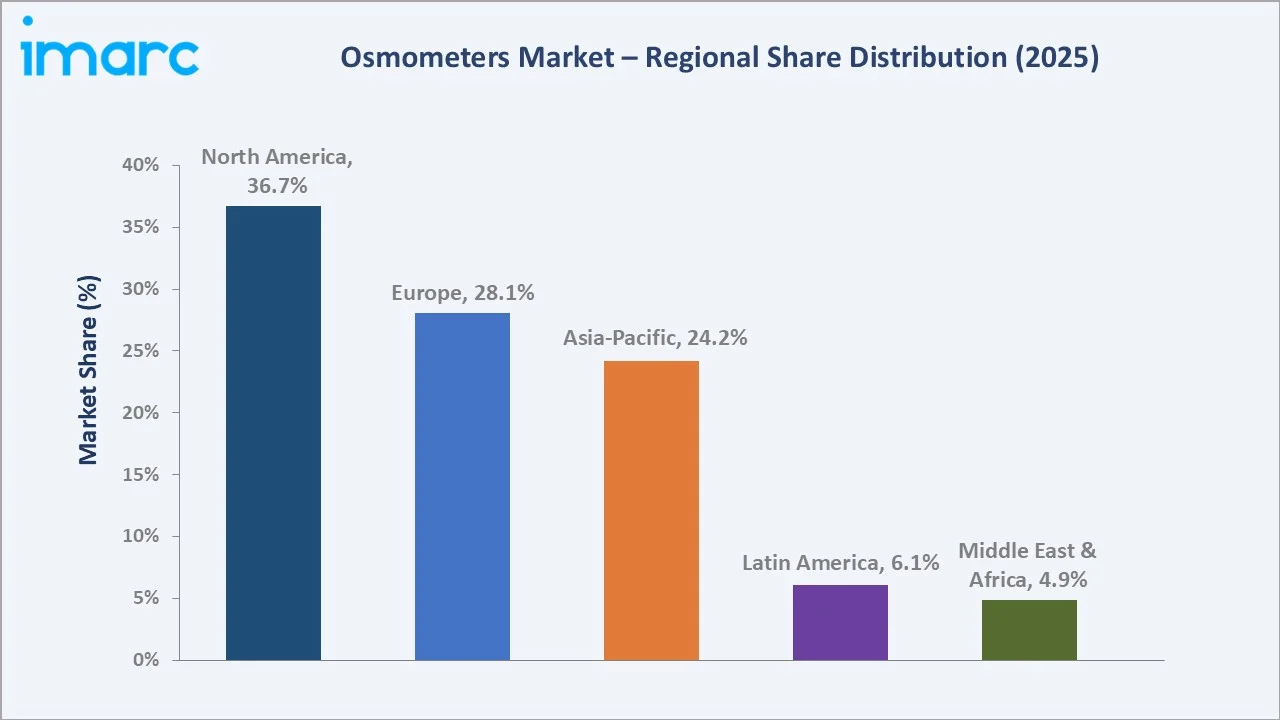

Freezing Point Osmometers lead product type segmentation at 56.8% in 2025, driven by their reliability and wide adoption across clinical chemistry and pharmaceutical quality control. Single-Sample Osmometers command 61.5% sampling capacity share. North America dominates the regional landscape with a 36.7% share, underpinned by advanced healthcare and pharma infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 88.89 Million |

|

Forecast Market Size (2026-2034) |

USD 111.44 Million |

|

CAGR (2026-2034) |

2.47% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Product Type |

Freezing Point Osmometers (56.8% share, 2025) |

|

Leading Sampling Capacity |

Single-Sample Osmometers (61.5% share, 2025) |

|

Leading Region |

North America (36.7% share, 2025) |

The osmometers market growth trajectory from 2020 through 2034 reflects consistent demand driven by chronic disease diagnostics, pharmaceutical manufacturing expansion, and the adoption of automated laboratory instruments. The forecast to USD 111.44 Million by 2034 captures accelerating biopharma investment and broader clinical application adoption across global laboratory networks.

To get more information on this market, Request Sample

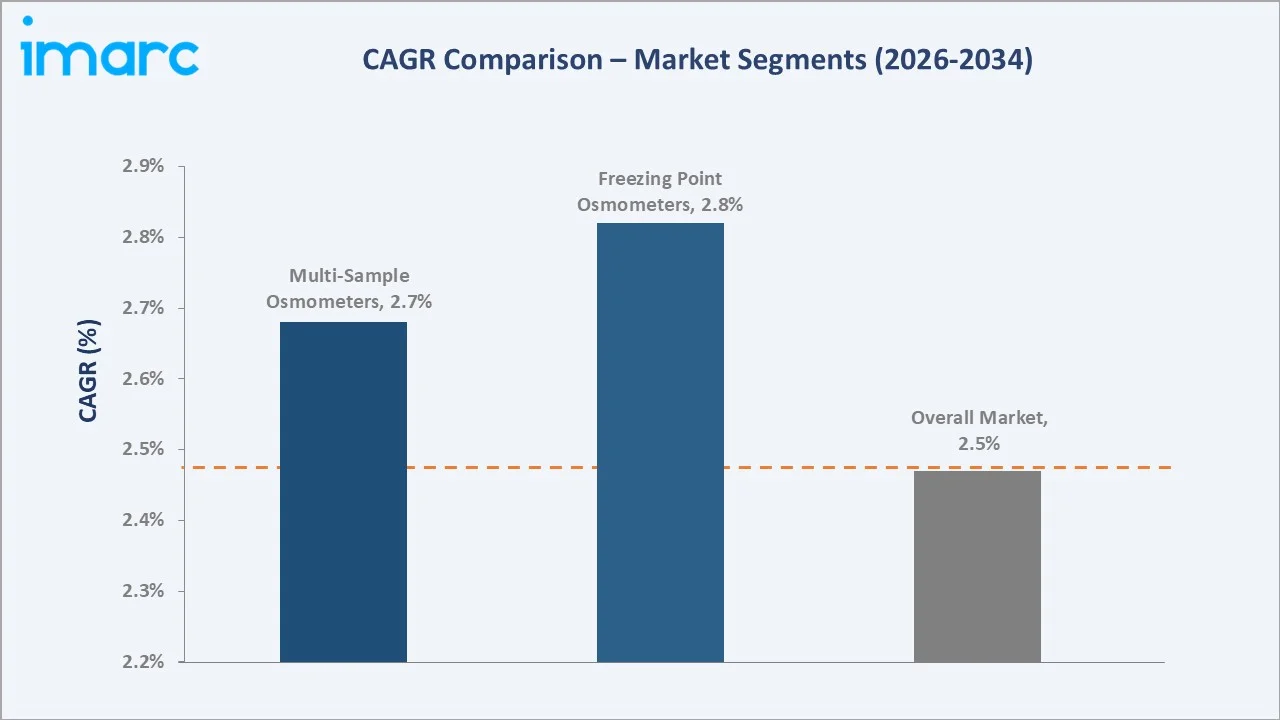

The CAGR trajectories across key segments highlight Multi-Sample Osmometers at approximately 2.68% CAGR and Freezing Point Osmometers at approximately 2.82% CAGR as the fastest-growing categories within the osmometers market through 2034.

Executive Summary

The global osmometers market is on a sustained growth trajectory from USD 88.89 Million in 2025 to USD 111.44 Million by 2034. The sector encompasses freezing point, vapor pressure, and membrane osmometers, benefiting from expanding pharmaceutical quality control requirements and rising chronic disease diagnostics worldwide.

Freezing Point Osmometers lead product type at 56.8% in 2025 owing to their cost-effectiveness, reproducibility, and widespread adoption across clinical and pharmaceutical applications. Vapor Pressure Osmometers (28.4%) serve high-precision research applications, while Membrane Osmometers (14.8%) address specialized polymer and macromolecule characterization needs globally.

Single-Sample Osmometers command 61.5% sampling capacity share in 2025, reflecting established clinical laboratory workflows. Multi-Sample Osmometers (38.5%) are gaining rapid adoption in high-throughput pharmaceutical and biotech environments demanding greater processing efficiency and seamless automation integration across regulated manufacturing environments.

North America dominates the market at 36.7% in 2025, driven by advanced healthcare infrastructure and substantial pharmaceutical R&D investment. Europe follows at 28.1%, driven by stringent regulatory compliance standards and established laboratory networks across Germany, the United Kingdom, and France.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Freezing Point Osmometers – 56.8% share (2025) |

|

Leading Sampling Capacity |

Single-Sample Osmometers – 61.5% share (2025) |

|

Leading Region |

North America – 36.7% share (2025) |

|

Second Largest Region |

Europe – 28.1% share (2025) |

|

Top Companies |

Nova Biomedical, ARKRAY, Inc., KNAUER Wissenschaftliche Geräte GmbH, Precision Systems, Inc., and Labtron Equipment Ltd. |

- Freezing Point Osmometers, at 56.8% in 2025, dominate because clinical and pharmaceutical laboratories require reliable, cost-effective osmolality measurement. These instruments deliver reproducible results across serum, urine, and pharmaceutical formulation testing with minimal sample preparation, making them the default choice for regulated laboratory environments globally.

- Single-Sample Osmometers command 61.5% share because standard clinical diagnostic workflows prioritize per-sample accuracy over throughput. Most hospital and reference laboratories process individual samples requiring detailed analysis before making clinical decisions on hydration status, electrolyte balance, and renal concentrating function in patients.

- North America's 36.7% regional dominance reflects its concentration of major pharmaceutical manufacturers, advanced hospital infrastructure, and significant investment in clinical diagnostic equipment driven by high chronic disease burden and rigorous FDA quality requirements for parenteral drug manufacturing and clinical diagnostic operations.

- Multi-Sample Osmometers, growing at approximately 2.68% CAGR, are accelerated by pharmaceutical industry demand for high-throughput biological testing, laboratory automation adoption, and integration with laboratory information management systems across large-scale manufacturing facilities and high-volume clinical reference laboratories worldwide.

Osmometers Market Overview

The osmometers market encompasses analytical instruments measuring osmotic concentration across clinical, pharmaceutical, food and beverage, and research applications. The market structure integrates instrument manufacturers, component suppliers, distributors, and end users including hospitals, pharmaceutical companies, and academic research institutions worldwide.

The ecosystem integrates global instrument manufacturers, reagent suppliers, calibration service providers, regulatory bodies, hospital procurement teams, pharmaceutical quality managers, and academic researchers requiring precise osmolality measurement for diagnostics, drug formulation validation, and scientific investigation across diverse laboratory environments globally.

Market Dynamics

To evaluate market opportunities, Request Sample

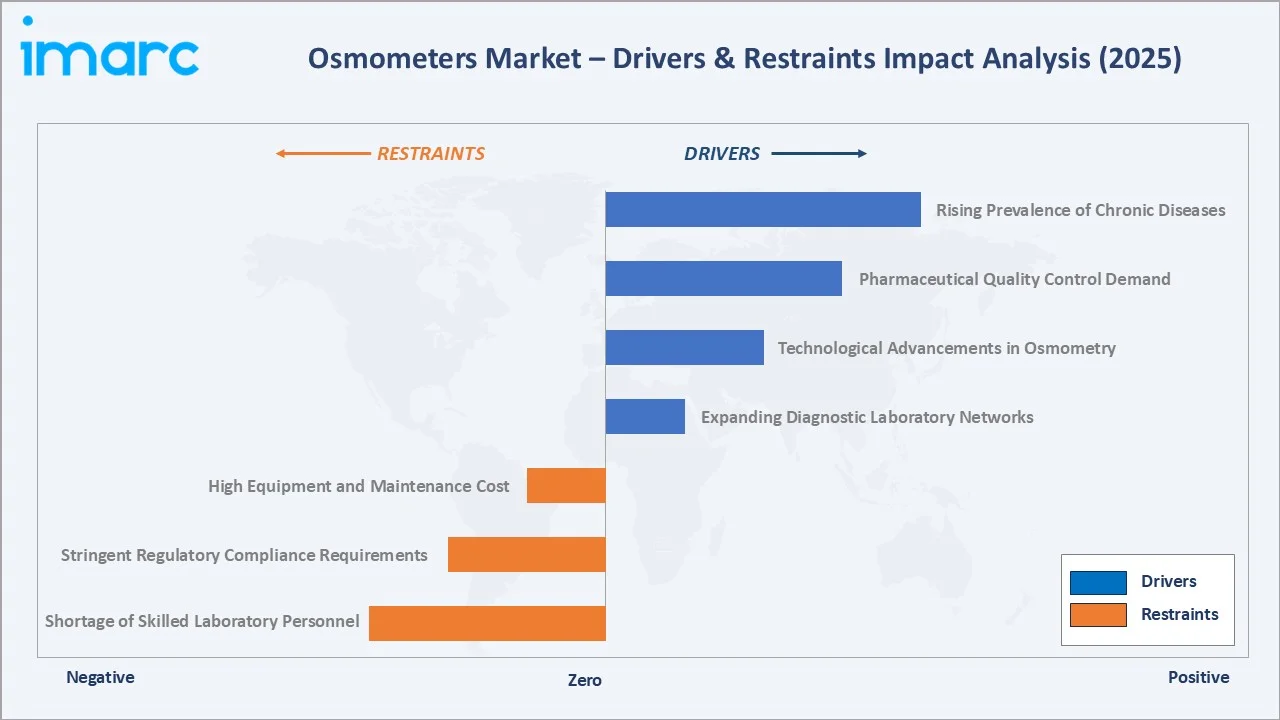

Market Drivers

- Rising Prevalence of Chronic Diseases: Increasing incidence of chronic kidney disease, diabetes, and cardiovascular conditions globally has expanded demand for routine osmolality testing. Clinical osmometers are essential for evaluating hydration status, electrolyte imbalance, and renal concentrating ability in affected patient populations, driving sustained instrument adoption across clinical laboratory networks.

- Pharmaceutical Quality Control Demand: Stringent pharmaceutical manufacturing regulations require osmolality testing of injectable formulations, parenteral solutions, and biologic drugs. Growing biologics pipeline and contract manufacturing expansion are increasing osmometer installations within quality control laboratories at pharmaceutical and biopharmaceutical manufacturing facilities worldwide.

- Technological Advancements in Osmometry: Innovations in automated sample handling, touchscreen interfaces, digital connectivity, and miniaturized detection systems have enhanced osmometer usability and accuracy. New instrument generations reduce sample volume requirements, enable faster analysis, and facilitate seamless integration with laboratory information management systems across regulated environments.

- Expanding Diagnostic Laboratory Networks: Rapid growth of hospital-based and independent diagnostic laboratories across emerging economies is creating new installation opportunities for clinical osmometers. Government healthcare spending increases and private laboratory network expansion across Asia-Pacific and Latin America are broadening the accessible osmometer market base significantly.

Market Restraints

- High Equipment and Maintenance Cost: Advanced osmometers carry significant capital investment requirements and recurring maintenance costs that limit adoption in budget-constrained clinical settings. Smaller hospitals and diagnostic laboratories in developing markets frequently defer osmometer procurement, creating a price-sensitivity barrier that constrains overall market penetration growth.

- Stringent Regulatory Compliance Requirements: Evolving medical device regulations, including EU MDR implementation and FDA quality system requirements, impose rigorous validation, documentation, and post-market surveillance obligations. Compliance costs increase instrument lifecycle expenses and extend procurement timelines, creating friction in the adoption of new osmometer platforms globally.

- Shortage of Skilled Laboratory Personnel: Operating and maintaining advanced osmometers require trained laboratory technicians with specialized calibration and quality management expertise. Growing vacancies for certified clinical chemists and laboratory technologists across healthcare systems constrain effective instrument utilization and slow adoption rates in resource-limited environments.

Market Opportunities

- AI and Digital Integration: Integration of AI-driven analytics and cloud connectivity into osmometer platforms enables real-time remote monitoring, predictive maintenance, and advanced data trend analysis, creating premium product differentiation opportunities for leading manufacturers targeting sophisticated biopharma and hospital laboratory customers seeking comprehensive digital laboratory solutions.

- Biologics Manufacturing Expansion: Growing biopharmaceutical production of high-concentration monoclonal antibodies and cell therapies demands precise osmolality control during formulation development, creating significant incremental demand for advanced multi-sample osmometer platforms in biologics manufacturing quality control and process development laboratory environments.

Market Challenges

- Regulatory Approval Complexity: Extended product registration timelines and increasing post-market clinical requirements under updated medical device regulations delay new osmometer launches and raise compliance costs, creating barriers for smaller manufacturers and slowing market innovation cycles in major regulated markets, including the United States and European Union.

- Market Maturity and Price Competition: Mature instrument replacement cycles in established North American and European laboratory networks limit near-term unit volume growth. Market penetration in emerging economies faces competition from lower-cost local manufacturers offering basic osmometry solutions at price points that constrain premium product adoption rates across cost-sensitive markets.

Emerging Market Trends

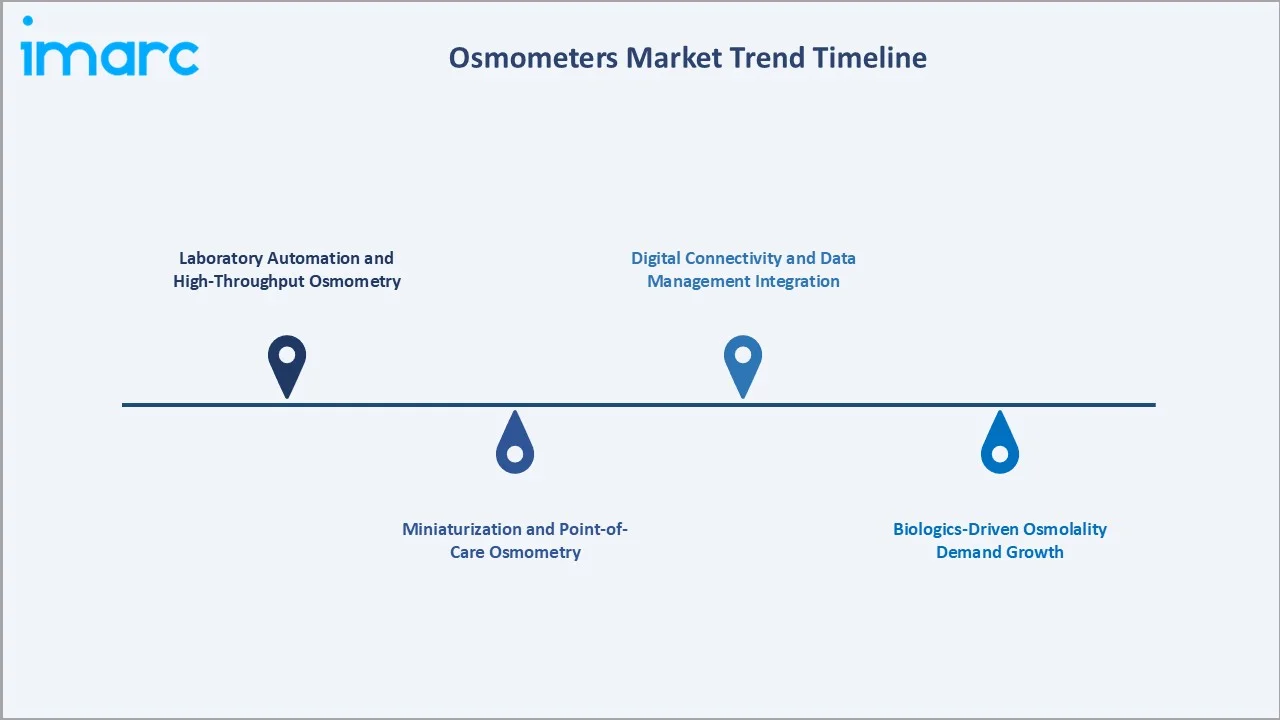

1. Laboratory Automation and High-Throughput Osmometry

Pharmaceutical and biotech laboratories are transitioning to automated multi-sample osmometers integrated with robotic sample handlers and LIMS platforms, enabling unattended batch processing, improved reproducibility, and reduced manual intervention across high-volume quality control workflows in regulated pharmaceutical and biopharmaceutical manufacturing environments.

2. Miniaturization and Point-of-Care Osmometry

Handheld and portable osmometer development is enabling bedside osmolality testing in intensive care and emergency settings. Reduced sample volume requirements and faster turnaround times are improving clinical decision-making for critically ill patients requiring rapid fluid management assessment and electrolyte balance monitoring at the point of care.

3. Biologics-Driven Osmolality Demand Growth

The expanding biologics pipeline, encompassing monoclonal antibodies, vaccines, and cell therapies, requires precise osmolality control across formulation development and manufacturing. This trend is sustaining long-term multi-sample osmometer demand within pharmaceutical quality assurance and process development laboratories across global biopharmaceutical manufacturing networks.

4. Digital Connectivity and Data Management Integration

Modern osmometers increasingly feature Ethernet, USB, and cloud connectivity enabling direct data transfer to laboratory information management systems and electronic laboratory notebooks. Regulatory data integrity requirements are accelerating adoption of instruments with comprehensive audit trails and electronic record management capabilities across regulated laboratory environments.

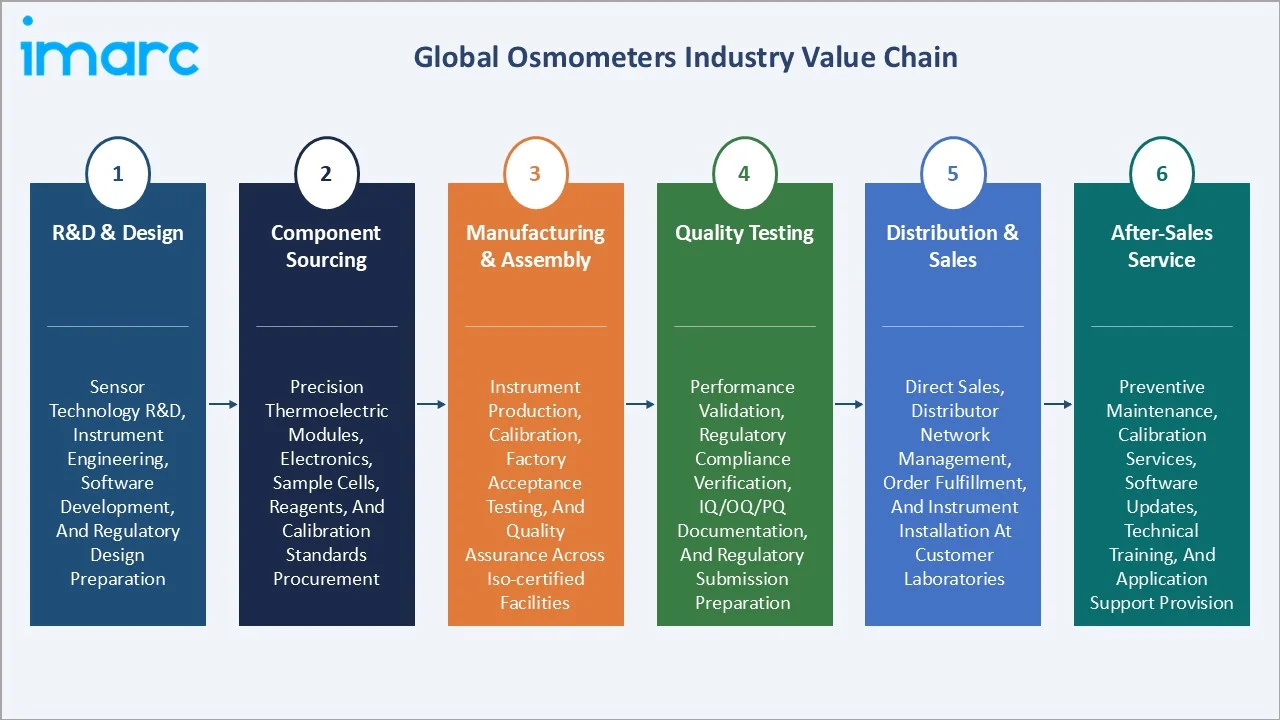

Industry Value Chain Analysis

The osmometers value chain spans six integrated stages from research and design through after-sales service. Instrument manufacturing and quality testing capture primary value, while distribution networks and technical service operations deliver instruments to end users across clinical, pharmaceutical, and research laboratory environments globally.

|

Stage |

Key Activities |

|

R&D & Design |

Sensor technology research, product engineering, software development, and regulatory design dossier preparation |

|

Component Sourcing |

Precision thermoelectric modules, electronic assemblies, sample cells, reagents, and calibration standards procurement |

|

Manufacturing & Assembly |

Instrument production, calibration, factory acceptance testing, and quality assurance across ISO-certified facilities |

|

Quality Testing |

Performance validation, regulatory compliance verification, IQ/OQ/PQ documentation, and regulatory submission preparation |

|

Distribution & Sales |

Direct sales, distributor network management, order fulfillment, and instrument installation at customer laboratories |

|

After-Sales Service |

Preventive maintenance, calibration services, software updates, technical training, and application support provision |

Manufacturing and quality testing stages capture the highest value, incorporating proprietary sensor technologies and validated calibration processes that define instrument performance and regulatory compliance. After-sales service represents a growing recurring revenue stream as laboratories increasingly adopt service contract models to ensure continuous instrument uptime.

Technology Landscape in the Osmometers Industry

Freezing Point Depression Technology

Freezing point depression osmometry remains the gold standard for clinical and pharmaceutical osmolality measurement. Modern implementations incorporate Peltier-based thermoelectric cooling, supercooling vibration detection, and automated cleaning cycles that enhance reproducibility, throughput, and ease of use across clinical and regulated pharmaceutical laboratory settings.

Vapor Pressure Osmometry Technology

Vapor pressure osmometers measure osmolality via dew point depression, offering advantages for non-aqueous solutions, viscous samples, and applications where freezing point measurement is impractical. Advanced thermocouple sensor designs and temperature-controlled sample chambers improve measurement precision for polymer and macromolecule characterization applications.

Automation and Digital Platform Integration

Next-generation osmometers integrate automated sample aspiration, waste disposal, and rinsing cycles that minimize operator interaction and contamination risk. Touchscreen interfaces with embedded method libraries, barcode reading, and bidirectional LIMS communication streamline workflow integration in regulated pharmaceutical and clinical laboratory environments.

Microfluidic and Miniaturized Sensor Technology

Emerging microfluidic osmometer designs reduce sample volume requirements to sub-microliter levels, enabling osmolality measurement from precious biological specimens and miniaturized cell culture volumes. These platforms support single-cell and organoid research applications demanding ultra-low volume, high-sensitivity osmolality analysis capabilities globally.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Freezing Point Osmometers |

56.8% |

2025 |

|

Sampling Capacity |

Single-Sample Osmometers |

61.5% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

North America |

36.7% |

2025 |

By Product Type

Freezing Point Osmometers command a 56.8% majority share in 2025 owing to their reliability, cost-effectiveness, and widespread adoption across clinical diagnostic and pharmaceutical quality control applications. Their compatibility with diverse aqueous sample matrices and established regulatory acceptance drive sustained dominance across global laboratory networks.

To access detailed market analysis, Request Sample

Vapor Pressure Osmometers (28.4%) serve specialized research and pharmaceutical applications requiring non-aqueous or viscous sample analysis. Membrane Osmometers (14.8%) address niche high-molecular-weight polymer characterization applications in academic research and advanced materials science laboratories requiring number-average molecular weight determination.

By Sampling Capacity

Single-Sample Osmometers dominate at 61.5% in 2025, driven by established clinical diagnostic workflows and cost considerations across hospital and independent laboratory settings. Their widespread installed base, lower acquisition cost, and suitability for low-to-medium throughput applications reinforce continued leadership in the sampling capacity segment globally.

Multi-Sample Osmometers (38.5%) are gaining rapid adoption in pharmaceutical quality control and high-volume biotech laboratories. Their capacity to process multiple samples simultaneously, integrate with automated sample handling systems, and deliver higher throughput supports expanding adoption in high-productivity manufacturing and clinical research environments.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

36.7% |

Advanced healthcare infrastructure; large pharmaceutical manufacturing base; high chronic disease diagnostics demand; FDA quality compliance requirements |

|

Europe |

28.1% |

Stringent EU MDR regulatory compliance; established pharmaceutical industry; hospital laboratory modernization programs across Germany, UK, and France |

|

Asia-Pacific |

24.2% |

Expanding diagnostic laboratory networks; growing pharmaceutical manufacturing; rising chronic disease burden; government healthcare investment |

|

Latin America |

6.1% |

Healthcare infrastructure development; growing private laboratory sector; pharmaceutical sector expansion in Brazil and Mexico |

|

Middle East & Africa |

4.9% |

Hospital capacity expansion; increasing pharmaceutical manufacturing investment; government healthcare modernization programs |

North America's 36.7% market dominance in 2025 is driven by its concentration of major pharmaceutical and biopharmaceutical manufacturers, comprehensive hospital networks, and significant investment in clinical diagnostic infrastructure. FDA quality system requirements mandate osmolality testing across parenteral drug manufacturing, sustaining consistent instrument demand.

Europe, at 28.1% in 2025, is underpinned by its well-established pharmaceutical industry, rigorous EU MDR compliance frameworks, and national laboratory quality accreditation systems. Germany, France, and the United Kingdom anchor European demand, with Eastern European markets representing incremental growth opportunities as healthcare infrastructure investment increases.

Competitive Landscape

The global osmometers market is moderately consolidated, with specialized analytical instrument manufacturers from North America and Europe collectively commanding significant market share. Leading players leverage proprietary sensor technology, regulatory expertise, and global distribution networks to maintain competitive positions against emerging regional manufacturers.

|

Company Name |

Key Products / Operations |

Market Position |

Global Strategic Focus |

|

Nova Biomedical |

OsmoTECH XT Single-Sample Osmometer, OsmoTECH PRO Multi-Sample Micro-Osmometer, OsmoTECH HT Automated Micro-Osmometer, OsmoPRO MAX Automated Osmometers, Osmo1 Single-Sample Micro-Osmometer |

Leader |

Expanding automated osmometer portfolio; advancing digital connectivity and LIMS integration capabilities globally |

|

ARKRAY, Inc. |

OM-6070, OM-6060 |

Established |

Strengthening clinical diagnostic portfolio; expanding Asia-Pacific distribution network and product localization |

|

KNAUER Wissenschaftliche Geräte GmbH |

K-7400S |

Established |

Focused on high-precision research and polymer characterization across academic and industrial markets |

|

Precision Systems, Inc. |

2430 Multi-OSMETTE, 2430E Multi-OSMETTE, 5002 OSMETTE A, 5004 MICRO-OSMETTE, 5005 OSMETTE II, 5007 OSMETTE XL, 5010 OSMETTE III |

Established |

Maintaining strong installed base in North American clinical laboratories; developing next-generation automated systems |

|

Labtron Equipment Ltd. |

LOSM-A10, LOSM-A11 |

Emerging |

Cost-effective clinical/pharma/research osmometers, expanding through online and regional distribution partners |

Key players include Nova Biomedical, ARKRAY, Inc., KNAUER Wissenschaftliche Geräte GmbH, Precision Systems, Inc., and Labtron Equipment Ltd., among others.

Key Company Profiles

Nova Biomedical

Nova Biomedical is a leading global provider of osmolality testing solutions, operating across clinical and biopharmaceutical market segments with a comprehensive portfolio of freezing point osmometers.

- Product Portfolio: OsmoTECH XT Single-Sample Osmometer, OsmoTECH PRO Multi-Sample Micro-Osmometer, OsmoTECH HT Automated Micro-Osmometer, OsmoPRO MAX Automated Osmometers, Osmo1 Single-Sample Micro-Osmometer

- Recent Developments: In October 2025, Advanced Instruments began operating under Nova Biomedical name, creating a larger global life sciences tools company focused on analytical instruments, consumables, and diagnostic solutions for the biopharmaceutical and clinical markets.

- Strategic Focus: Nova Biomedical's strategy centres on maintaining osmometry market leadership across clinical diagnostics and biopharmaceutical bioprocessing segments, leveraging its broad product portfolio to address diverse laboratory throughput requirements while expanding automation capabilities, digital connectivity, and regulatory compliance features to meet evolving customer needs globally.

ARKRAY, Inc.

ARKRAY, Inc. is a global in vitro diagnostics company offering a range of clinical laboratory instruments, including osmometers, across an extensive international distribution network.

- Product Portfolio: OM-6070, OM-6060

- Strategic Focus: ARKRAY's strategy centres on strengthening its clinical osmometer portfolio through ongoing platform upgrades and broadening its global distribution footprint, particularly across Asia-Pacific markets, while providing continued product support for its widely installed legacy osmometer base across hospital and diagnostic laboratory customers worldwide.

Precision Systems, Inc.

Precision Systems, Inc. is a manufacturer of freezing point osmometers serving clinical, pharmaceutical, and research laboratory markets, primarily in North America. The company offers a broad range of single-sample and multi-sample osmometer models distributed through established scientific supply channels, providing cost-effective osmolality measurement solutions to a wide range of laboratory customers.

- Product Portfolio: 2430 Multi-OSMETTE, 2430E Multi-OSMETTE, 5002 OSMETTE A, 5004 MICRO-OSMETTE, 5005 OSMETTE II, 5007 OSMETTE XL, 5010 OSMETTE III

- Strategic Focus: Precision Systems' strategy centres on sustaining its established North American market position through consistent product availability, reliable customer support, and cost-effective instrument solutions, while leveraging its long-standing distribution relationships to serve laboratory replacement demand across hospital, pharmaceutical, and research institution customer segments.

Market Concentration Analysis

The osmometers market exhibits moderate concentration, with advanced instrument manufacturers from North America and Europe collectively holding substantial combined market share. Specialized technology barriers, regulatory approval requirements, and established customer relationships create meaningful competitive moats that sustain incumbent player positions over time.

At the product segment level, Freezing Point Osmometers dominate concentration metrics, reflecting clinical laboratory preference for proven measurement technologies with established regulatory acceptance. Emerging automation and digital connectivity capabilities are becoming key competitive differentiators that leading players are actively developing to maintain their technology leadership positions through the forecast period to 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Multi-Sample Osmometers represent the highest-growth sampling capacity segment through 2034 at approximately 2.68% CAGR, capturing pharmaceutical quality control and biotech automation investment. Freezing Point Osmometers benefit from new clinical installation opportunities in Asia-Pacific laboratory networks at approximately 2.82% CAGR across the forecast period.

Emerging Markets

Asia-Pacific and Latin America are emerging as significant investment frontiers, with expanding diagnostic laboratory networks, growing pharmaceutical manufacturing investments, and rising chronic disease burden creating new osmometer adoption opportunities. Government healthcare infrastructure programs are catalyzing instrument procurement across these high-growth regions.

Venture & Investment Trends

Strategic acquisitions, including Advanced Instruments' merger with Nova Biomedical, reflect industry consolidation toward integrated analytical platforms. Private equity and corporate development investment is flowing toward companies with strong pharmaceutical quality control positioning and established digital connectivity product portfolios in the osmometers market.

Future Market Outlook (2026-2034)

The global osmometers market is forecast to expand from USD 88.89 Million in 2025 to USD 111.44 Million by 2034 at a CAGR of 2.47%, driven by expanding pharmaceutical biologics production, growing chronic disease diagnostics demand, and technology advancements enabling automated, connected osmometry across clinical and quality control laboratory settings globally.

Three structural forces will shape the market through 2034: pharmaceutical biologics pipeline expansion will drive multi-sample osmometer demand; digital transformation and automation integration will redefine product value propositions; and emerging market laboratory network growth will create new geographic revenue streams for leading instrument manufacturers worldwide.

Research Methodology

Primary Research

Primary research encompassed structured interviews with osmometer manufacturers, clinical laboratory directors, pharmaceutical quality managers, hospital procurement specialists, and distributor representatives. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption trends within the global osmometers market.

Secondary Research

Key secondary sources include FDA medical device registration databases, EMA regulatory publications, WHO laboratory equipment guidelines, scientific literature on osmometry applications, company annual reports, trade association publications from AACC and EFLM, and market intelligence from healthcare analytical instrument industry databases globally.

Forecasting Models

Market size estimations and growth projections were derived using combined top-down and bottom-up forecasting models incorporating global pharmaceutical manufacturing output growth, chronic disease prevalence trends, diagnostic laboratory expansion rates, and instrument replacement cycle analysis. Scenario modelling encompassed base, optimistic, and conservative cases.

Osmometers Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Freezing Point Osmometers, Vapor Pressure Osmometers, Membrane Osmometers |

| Sampling Capacities Covered | Single-Sample Osmometers, Multi-Sample Osmometers |

| Applications Covered | Clinical, Pharmaceutical and Biotech, Others |

| End Users Covered | Laboratory and Diagnostic Centers, Hospitals, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Nova Biomedical, ARKRAY, Inc., KNAUER Wissenschaftliche Geräte GmbH, Precision Systems, Inc., Labtron Equipment Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the osmometers market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global osmometers market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the osmometers industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Osmometers Market Report

The global osmometers market reached USD 88.89 Million in 2025, reflecting sustained demand driven by pharmaceutical quality control requirements, rising chronic disease diagnostics, and expanding clinical laboratory networks across North America, Europe, and Asia-Pacific globally.

The market is projected to reach USD 111.44 Million by 2034, growing at a CAGR of 2.47% during 2026-2034, driven by biologics manufacturing expansion, clinical diagnostics growth, laboratory automation adoption, and emerging market laboratory infrastructure investment worldwide.

Freezing Point Osmometers lead with a 56.8% market share in 2025, driven by widespread clinical and pharmaceutical adoption. Vapor Pressure Osmometers (28.4%) serve research applications, while Membrane Osmometers (14.8%) address specialized polymer characterization needs.

Single-Sample Osmometers dominate with a 61.5% share in 2025, reflecting established clinical workflows and cost considerations. Multi-Sample Osmometers (38.5%) are gaining adoption in high-throughput pharmaceutical and biotech quality control laboratory environments.

North America leads with a 36.7% market share in 2025, underpinned by pharmaceutical manufacturing, advanced hospital infrastructure, and FDA quality compliance requirements. Europe follows at 28.1%, driven by regulatory standards and established laboratory networks.

Multi-Sample Osmometers represent the fastest-growing sampling capacity segment at approximately 2.68% CAGR through 2034, driven by pharmaceutical automation demand. Asia-Pacific is the fastest-growing region, supported by laboratory network expansion and healthcare investment.

Leading companies include Nova Biomedical, ARKRAY, Inc., KNAUER Wissenschaftliche Geräte GmbH, Precision Systems, Inc., and Labtron Equipment Ltd., among others.

Key drivers include rising chronic disease prevalence, increasing clinical osmolality testing, pharmaceutical quality control requirements mandating osmometer use, technological advancements improving instrument usability and throughput, and expanding diagnostic laboratory networks across emerging economies globally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)