Osteosynthesis Devices Market Size, Share, Trends and Forecast by Type, Material, Fracture Type, End User, and Region, 2026-2034

Osteosynthesis Devices Market Size and Share:

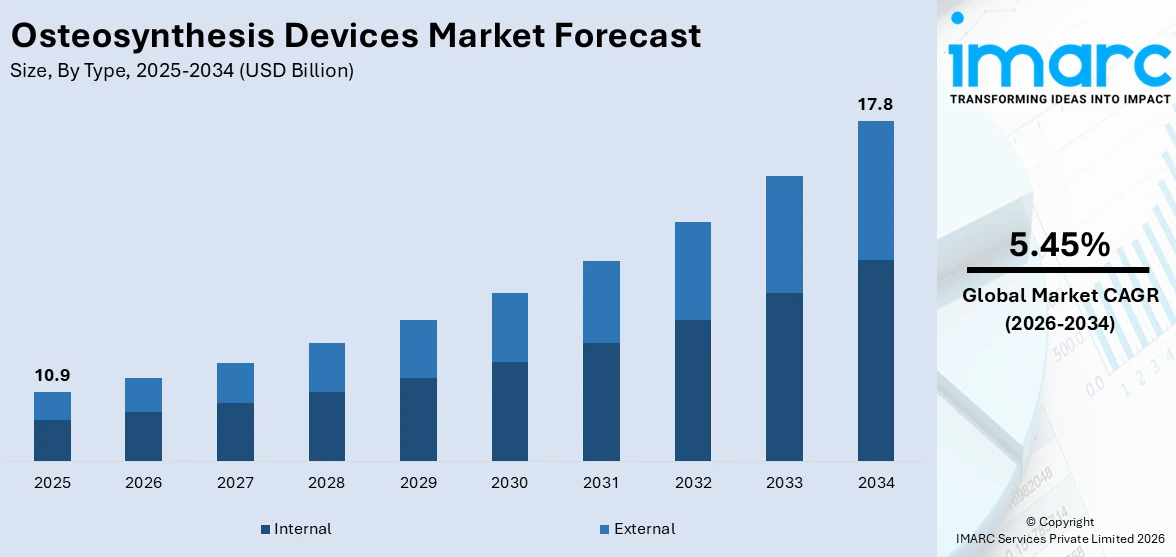

The global osteosynthesis devices market size was valued at USD 10.9 Billion in 2025. The market is projected to reach USD 17.8 Billion by 2034, exhibiting a CAGR of 5.45% from 2026-2034. North America currently dominates the market, holding a market share of 52.3% in 2025. The growing number of road accidents across the globe and the rising prevalence of bone fractures and osteoarthritis, especially amongst the geriatric population, are contributing to the expansion of the osteosynthesis devices market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 10.9 Billion |

|

Market Forecast in 2034

|

USD 17.8 Billion |

| Market Growth Rate 2026-2034 | 5.45% |

The osteosynthesis devices market is being driven by the rising count of people experiencing bone fractures, trauma cases, and orthopedic injuries resulting from road accidents, sports activities, and falls, especially among the aging population that is highly susceptible to osteoporosis and bone fragility. The growing awareness about advanced orthopedic treatments and the increasing incidence of musculoskeletal disorders are further catalyzing the demand. Technological advancements, including the development of minimally invasive surgical techniques and innovative biocompatible materials like titanium and bioresorbable polymers, are improving treatment efficiency and patient recovery times. Additionally, expanding healthcare infrastructure and insurance support are impelling the osteosynthesis devices market growth.

To get more information on this market Request Sample

The United States has emerged as a major region in the osteosynthesis devices market owing to many factors. Rising prevalence of bone fractures, trauma cases, and orthopedic injuries caused by road accidents, workplace hazards, sports activities, and age-related falls is fueling the market expansion. A rapidly growing elderly population with higher risks of osteoporosis and degenerative bone diseases is further catalyzing the demand for advanced fixation solutions. In addition, continuous technological innovations, including minimally invasive surgical techniques, bioresorbable implants, and titanium-based fixation systems, are enhancing surgical outcomes and patient recovery. As per the IMARC Group, the United States minimally invasive surgery market size reached USD 25.7 Billion in 2024.

Osteosynthesis Devices Market Trends:

Increasing number of road accidents

Rising number of road accidents is among the major osteosynthesis devices market trends, as accidents often result in severe fractures and traumatic bone injuries that require immediate and effective fixation solutions. For instance, UP in India reported more than 13,000 road accidents, with almost 7,700 fatalities between January and May 2025. With increasing vehicular density and lifestyle changes, the frequency of such accidents has risen, catalyzing greater demand for advanced surgical interventions. Osteosynthesis devices like plates, screws, and intramedullary nails provide stability, faster healing, and improved recovery for patients with complex fractures. Hospitals and trauma centers are increasingly relying on these devices to manage emergency cases efficiently. Moreover, advancements in device design and availability of minimally invasive procedures make treatment outcomes more reliable.

Rising incidence of bone fractures and osteoarthritis

Increasing incidence of bone fractures and osteoarthritis is offering a favorable osteosynthesis devices market outlook, as both conditions require effective surgical fixation to restore stability and mobility. Fractures from falls, sports activities, and aging-related fragility are becoming more common, particularly in the elderly population. By the end of the 2070s, it is projected that the worldwide population aged 65 and above will hit 2.2 Billion, exceeding the count of children under 18. Osteoarthritis, a progressive degenerative joint disease, often leads to bone deformities and complications requiring surgical intervention with fixation devices. Osteosynthesis implants, such as plates, screws, and nails, help ensure proper alignment, stability, and faster recovery in these cases. With longer life expectancy and rising prevalence of musculoskeletal disorders, the demand for durable, biocompatible, and efficient fixation devices continues to rise.

Growing use of robotic-assisted and image-guided surgeries

The expanding utilization of robotic-assisted and image-guided surgeries is driving the market expansion by enhancing surgical precision, minimizing errors, and improving patient outcomes. In September 2025, the Orthopedics Department at BJ Government Medical College and Sassoon General Hospital, India, reached a significant milestone by completing three robotic knee replacement surgeries successfully. Utilizing computed tomography (CT)-guided demo robotic devices, the team offered complimentary total knee implants to each of the three patients. Advanced technologies allow surgeons to achieve accurate implant placement, optimal bone alignment, and reduced risks of complications. Robotic systems enable minimally invasive approaches, leading to smaller incisions, quicker recovery periods, and shorter hospital hospitalizations, while image-guided systems provide real-time visualization for complex fracture management. This technological integration is particularly beneficial in treating challenging cases, such as spine, hip, and long bone fractures.

Osteosynthesis Devices Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global osteosynthesis devices market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on type, material, fracture type, and end user.

Analysis by Type:

- Internal

- Screw and Plates

- Wires and Pins

- Intramedullary Rods and Nails

- Spinal Fixation Devices

- External

- Fracture Fixation

- Bone Lengthening

Internal (screw and plates, wires and pins, intramedullary rods and nails, and spinal fixation devices) held 70% of the market share in 2025. Internal osteosynthesis devices provide superior stability, faster healing, and reduced risk of complications compared to external fixation methods. Devices like screws and plates and intramedullary nails are widely preferred by surgeons, as they remain inside the body, allowing patients greater mobility during recovery and minimizing external infections. Their ability to provide direct stabilization of fractured bones improves alignment and healing outcomes. Moreover, internal devices are commonly used in complex fractures, such as hip, spine, or long bone injuries, which are increasingly prevalent among the aging population. Advancements in biocompatible materials, minimally invasive surgical techniques, and customized implant designs have further improved the safety and effectiveness of internal fixation devices. As per the osteosynthesis devices market forecast, with the rising incidence of trauma cases, sports injuries, and age-related fractures, coupled with patient preference for reliable long-term solutions, internal osteosynthesis devices will continue to dominate the industry.

Analysis by Material:

- Non-Degradable

- Degradable

Non-degradable accounts for 80% of the market share. Non-degradable osteosynthesis devices provide long-term stability, durability, and reliability in fracture fixation. Materials like titanium and stainless steel are widely used, as they offer excellent strength, corrosion resistance, and biocompatibility, making them suitable for complex and load-bearing fractures. Unlike degradable devices, which may not provide sufficient support for long healing durations, non-degradable implants remain effective throughout the recovery process, ensuring better alignment and reduced risk of implant failure. They are preferred in cases requiring permanent or long-term fixation, such as severe trauma injuries, spinal fractures, and orthopedic reconstructive surgeries. In addition, continuous improvements in non-degradable implant designs like locking plates and intramedullary nails have enhanced clinical outcomes and surgeon confidence. Their proven track record, availability in varied sizes, and compatibility with advanced surgical techniques further reinforce their dominance.

Analysis by Fracture Type:

- Patella, Tibia or Fibula or Ankle

- Clavicle, Scapula or Humerus

- Radius or Ulna

- Hand, Wrist

- Vertebral Column

- Pelvis

- Hip

- Femur

- Foot Bones

- Others

Patella, tibia or fibula or ankle hold 20% of the market share. These bones are highly susceptible to injuries from road accidents, falls, and sports activities. Being weight-bearing and critical for mobility, fractures in these areas often require surgical fixation to restore stability and function. Osteosynthesis devices like intramedullary nails, plates, and screws are commonly used to manage such fractures, providing better alignment and faster recovery. The increasing prevalence of osteoporosis among the elderly population is also contributing to frequent tibial and ankle fractures, driving strong demand for reliable fixation solutions. Additionally, the rise in physically active lifestyles has led to more sports-related lower limb injuries, further boosting adoption. Surgeons prefer internal fixation in these fractures due to its effectiveness in maintaining load-bearing capacity during healing. With technological advancements in minimally invasive fixation systems and biocompatible implants, the treatment of patella, tibia or fibula or ankle fractures has become more efficient.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

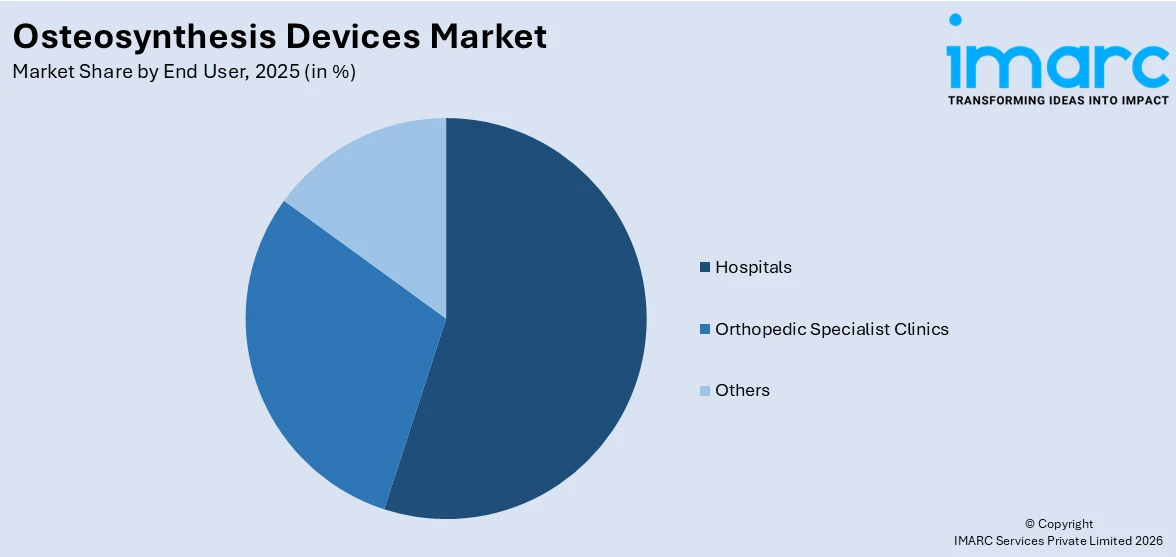

- Hospitals

- Orthopedic Specialist Clinics

- Others

Hospitals possess the capability to handle complex surgical procedures and provide comprehensive orthopedic care. These facilities are equipped with advanced operation theaters, imaging systems, and postoperative care units, enabling surgeons to perform fracture fixation, joint reconstruction, and trauma surgeries effectively. High patient inflow, including emergency trauma cases, is driving consistent demand for plates, screws, nails, and fixation systems. Hospitals also participate in clinical trials and research programs, adopting the latest devices and technologies.

Orthopedic specialist clinics focus on outpatient care and minor surgical procedures, contributing significantly to the market. These clinics often handle non-complex fractures, follow-up treatments, and rehabilitation, catalyzing the demand for minimally invasive fixation devices, screws, and small plates. They offer personalized patient care, shorter hospital stays, and faster recovery solutions, emphasizing cost-effective and efficient devices. Specialist clinics also educate patients about post-surgical care and implant options, supporting consistent adoption of osteosynthesis products.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

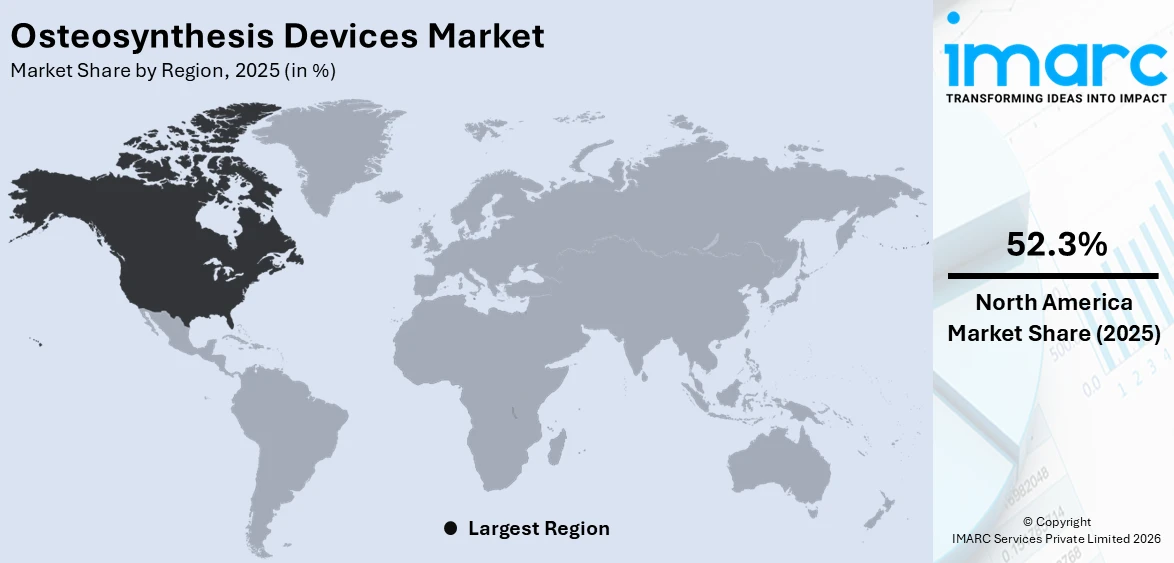

North America, accounting for a share of 52.3%, enjoys the leading position in the market. The region is noted for its advanced healthcare infrastructure, strong presence of leading medical device companies, and high patient awareness about advanced treatment options. The region has a large and growing geriatric population, which is more prone to osteoporosis, bone fragility, and fracture-related complications, catalyzing the demand for fixation devices. Rising rates of trauma cases, sports injuries, and road accidents is further creating a steady need for osteosynthesis solutions. According to the Sport Modern Statistics, around 8.6 Million sports injuries were documented in the United States in 2024. Additionally, high healthcare spending, favorable reimbursement policies, and widespread insurance coverage are encouraging patients to opt for advanced orthopedic procedures. The region also benefits from early adoption of innovative technologies, such as minimally invasive surgical techniques, bioresorbable implants, robotic-assisted surgeries, and image-guided systems that improve precision and recovery outcomes.

Key Regional Takeaways:

United States Osteosynthesis Devices Market Analysis

The United States holds 85% of the market share in North America. The United States is witnessing rising osteosynthesis devices adoption due to growing incidence of road accidents that lead to severe fractures and bone injuries requiring advanced fixation solutions. According to reports, 8,055 people were killed on US roads during Q1 2025. The increasing number of traumatic injuries is driving a higher demand for innovative devices that provide faster recovery and improved patient outcomes. Advancements in surgical procedures and the accessibility of minimally invasive fixation systems are further supporting the market expansion. Moreover, the growing awareness among patients and healthcare professionals about effective treatment options is boosting usage. Increasing insurance coverage and accessibility to trauma care facilities are also contributing to the growth of the osteosynthesis devices market, ensuring greater reliance on such technologies for fracture management and post-traumatic rehabilitation. Additionally, continuous product innovations, strong presence of global players, and rising preferences for durable implants are further accelerating the market growth across hospitals and specialized orthopedic centers.

Europe Osteosynthesis Devices Market Analysis

Europe is observing expanding osteosynthesis devices adoption due to the growing geriatric population that is more prone to bone fractures, osteoporosis, and degenerative orthopedic conditions. According to the WHO, the number of individuals aged 60 and above is increasing quickly in the WHO European Region. In 2021, the count was 215 Million. By 2030, it is expected to reach 247 Million and by 2050, it will surpass 300 Million. The higher incidence of fragility fractures among the elderly is driving consistent demand for fixation devices and advanced surgical techniques. Healthcare systems are focusing on improving orthopedic treatment efficiency by integrating innovative osteosynthesis solutions that promote rapid healing and reduce post-operative complications. Rising demand for joint reconstruction and fracture repair surgeries in aging demographics is fueling the adoption. Continuous research, technological advancements, and clinical support for elderly patients are further strengthening the market across the region, ensuring sustainable long-term growth.

Asia-Pacific Osteosynthesis Devices Market Analysis

The Asia-Pacific region is experiencing increasing osteosynthesis devices adoption due to the growing investments in healthcare sector aimed at strengthening medical infrastructure and expanding access to advanced orthopedic care. According to India Brand Equity Foundation, the Indian government designated INR 99,858 Crore (USD 11.50 Billion) to the healthcare sector in the Union Budget 2025-26 for the improvement, upkeep, and advancement of the national healthcare system. Rising healthcare expenditure and government-backed programs to modernize hospital facilities are driving the availability of technologically advanced bone fixation systems. The demand for better trauma management solutions is surging, as healthcare providers are focusing on reducing surgical complications and enhancing recovery times. The expansion of private healthcare facilities and collaborations with medical device manufacturers are also encouraging wider adoption.

Latin America Osteosynthesis Devices Market Analysis

Latin America shows rising osteosynthesis devices adoption, driven by increasing health investments across the region. For instance, per-capita health expenditure in Chile is set to increase 3.4 times by 2050, while in Belize, the anticipated growth factor is 2.5. Expanding public and private healthcare spending is enabling hospitals and clinics to upgrade orthopedic surgical infrastructure, supporting greater use of advanced fixation systems for trauma and fracture management. The growing access to health insurance and higher patient affordability are catalyzing the demand for modern implants, such as plates, screws, and intramedullary nails.

Middle East and Africa Osteosynthesis Devices Market Analysis

The Middle East and Africa region is demonstrating rising osteosynthesis devices adoption, as healthcare companies are increasing investments in advanced orthopedic solutions. For instance, as of August 2025, the United Arab Emirates healthcare industry included 1,000 firms, among which 96 were funded and had together secured USD 1.17 Billion in venture capital and private equity. Among these, 63 companies received Series A+ funding. Expanding private and public healthcare infrastructure, coupled with higher expenditure on surgical innovations, is catalyzing the demand for fracture fixation systems, plates, and screws. Regional hospitals are integrating modern trauma care technologies, supported by partnerships with global device manufacturers.

Competitive Landscape:

Key players are continuously investing in research and development (R&D) activities to introduce innovative fixation systems, advanced materials, and minimally invasive surgical solutions that improve patient outcomes. Through strategic collaborations, mergers, and acquisitions, they are expanding their product portfolios and strengthening global presence, enabling wider accessibility of devices. Leading companies also focus on clinical trials and evidence-based studies to validate the safety and effectiveness of their products, thereby increasing adoption among surgeons and healthcare providers. In addition, they are wagering heavily on training programs, workshops, and digital platforms to enhance surgeon expertise and promote advanced surgical techniques. By leveraging strong distribution networks and customer support, these players ensure availability of high-quality devices. For instance, in February 2025, Bioretec Ltd. received CE mark approval for its RemeOs™ Trauma Screw range, which included more than 200 products for various osteosynthesis indications, allowing the company to boost sales throughout Europe and enhance its global growth prospects beyond the US market.

The report provides a comprehensive analysis of the competitive landscape in the osteosynthesis devices market with detailed profiles of all major companies, including:

- Arthrex Inc.

- B. Braun Melsungen AG

- Globus Medical Inc.

- GS Medical USA

- Johnson & Johnson

- Life Spine Inc.

- MicroPort Scientific Corporation

- Neosteo SAS

- Precision Spine Inc.

- Smith & Nephew plc

- Stryker Corporation

- Zimmer Biomet

Latest News and Developments:

- June 2025: Smith+Nephew revealed the introduction of its TRIGEN MAX Tibia Nailing System, offering trauma surgeons side-specific nails, improved screw choices, and simplified instruments to maximize fixation, reduce soft tissue irritation, and refine efficiency in managing both stable and unstable tibial fractures.

- April 2025: Spineway bolstered its global presence by organizing worldwide surgeon training events, marked by the introduction of its VEOS posterior osteosynthesis system in South America and specialized workshops in France that improved proficiency in its cutting-edge spine implant products.

Osteosynthesis Devices Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

| Materials Covered | Non-Degradable, Degradable |

| Fracture Types Covered | Patella, Tibia, or Fibula, or Ankle, Clavicle, Scapula or Humerus, Radius or Ulna, Hand, Wrist, Vertebral Column, Pelvis, Hip, Femur, Foot Bones, Others |

| End Users Covered | Hospitals, Orthopedic Specialist Clinics, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Arthrex Inc., B. Braun Melsungen AG, Globus Medical Inc., GS Medical USA, Johnson & Johnson, Life Spine Inc., MicroPort Scientific Corporation, Neosteo SAS, Precision Spine Inc., Smith & Nephew plc, Stryker Corporation, Zimmer Biomet, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the osteosynthesis devices market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global osteosynthesis devices market.

- The study maps the leading as well as the fastest growing regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the osteosynthesis devices industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Osteosynthesis Devices Market Report

The osteosynthesis devices market was valued at USD 10.9 Billion in 2025.

The osteosynthesis devices market is projected to exhibit a CAGR of 5.45% during 2026-2034, reaching a value of USD 17.8 Billion by 2034.

Rising prevalence of bone-related disorders and the demand for faster and more effective healing solutions are also boosting the adoption of osteosynthesis devices. Moreover, advancements in surgical techniques, such as minimally invasive procedures, along with innovations in biocompatible materials like titanium and bioresorbable implants, are enhancing treatment outcomes and patient recovery. The expansion of healthcare infrastructure in developing regions, coupled with increasing healthcare expenditure and insurance coverage, is further supporting the market growth.

North America currently dominates the osteosynthesis devices market, accounting for a share of 52.3% in 2025, due to its sophisticated healthcare infrastructure, elevated healthcare expenditures, significant presence of major players, and increasing occurrence of bone disorders. The integration of cutting-edge surgical technologies that promote improved patient outcomes and quicker recovery is fueling the market expansion.

Some of the major players in the osteosynthesis devices market include Arthrex Inc., B. Braun Melsungen AG, Globus Medical Inc., GS Medical USA, Johnson & Johnson, Life Spine Inc., MicroPort Scientific Corporation, Neosteo SAS, Precision Spine Inc., Smith & Nephew plc, Stryker Corporation, Zimmer Biomet, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)