Ovarian Cancer Market Size, Share, Trends and Forecast by Type, Treatment Type, End User, and Region, 2026-2034

Ovarian Cancer Market Size, Share, Trends & Forecast (2026-2034)

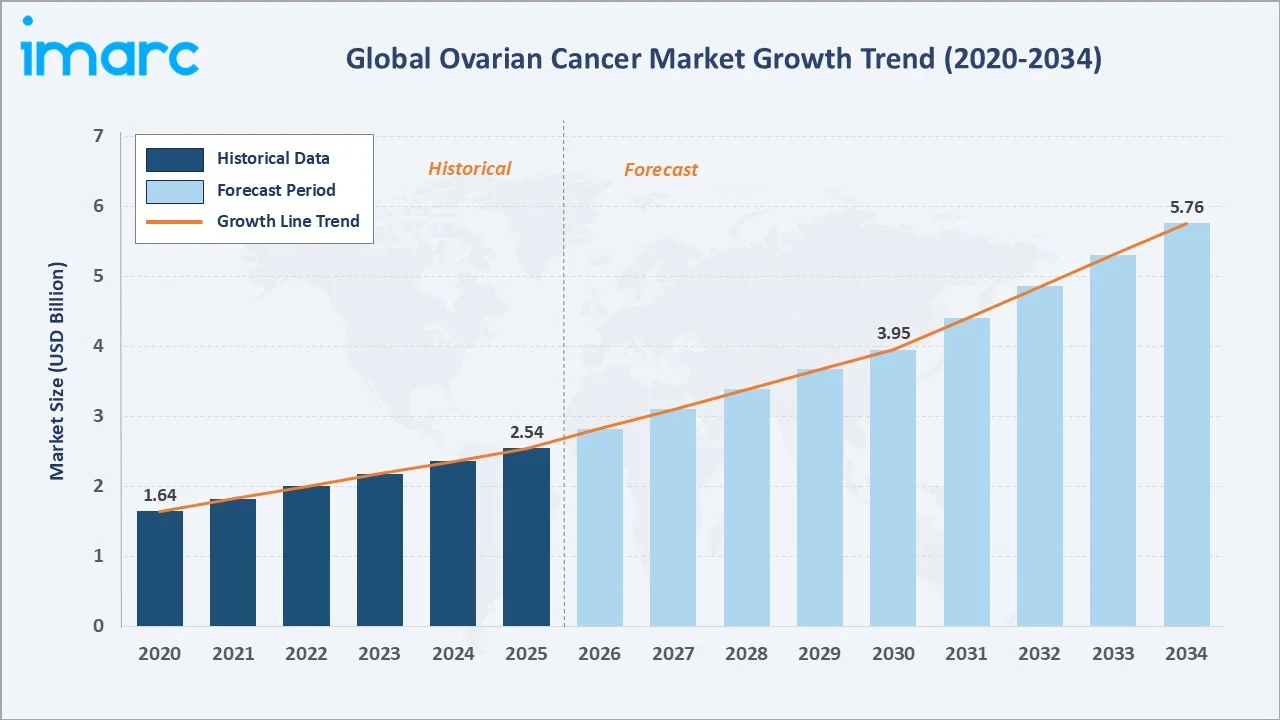

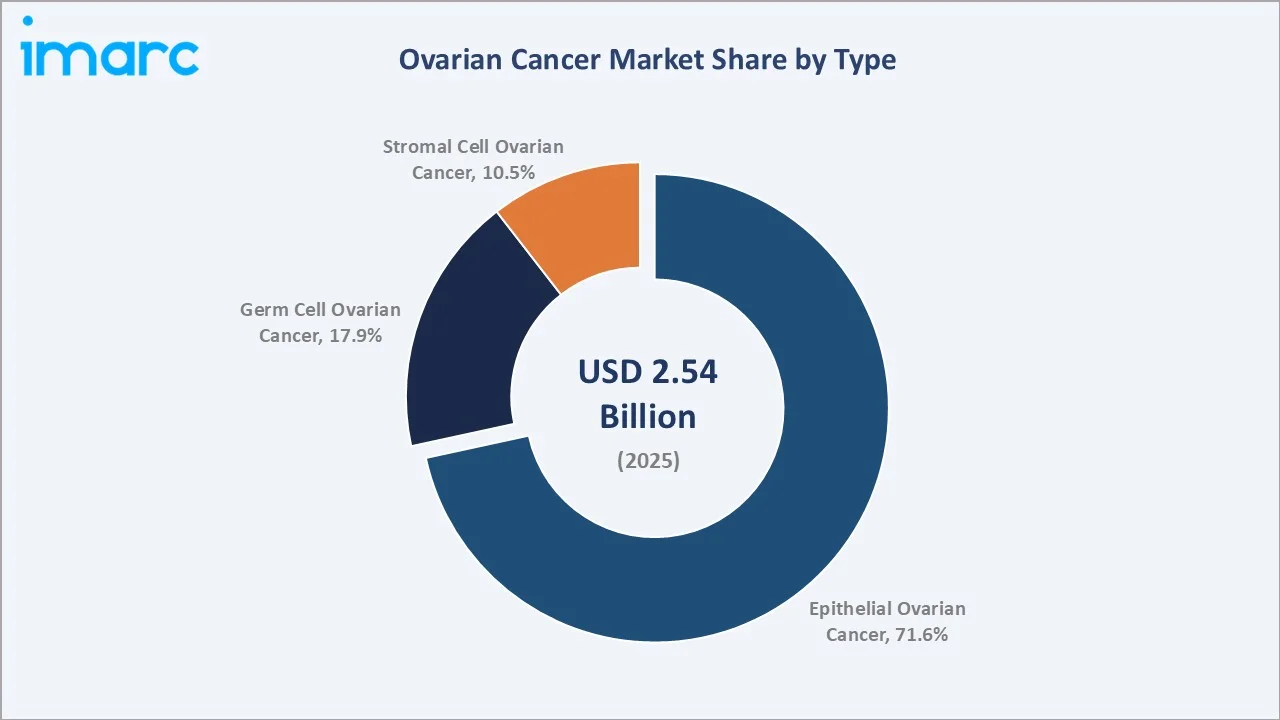

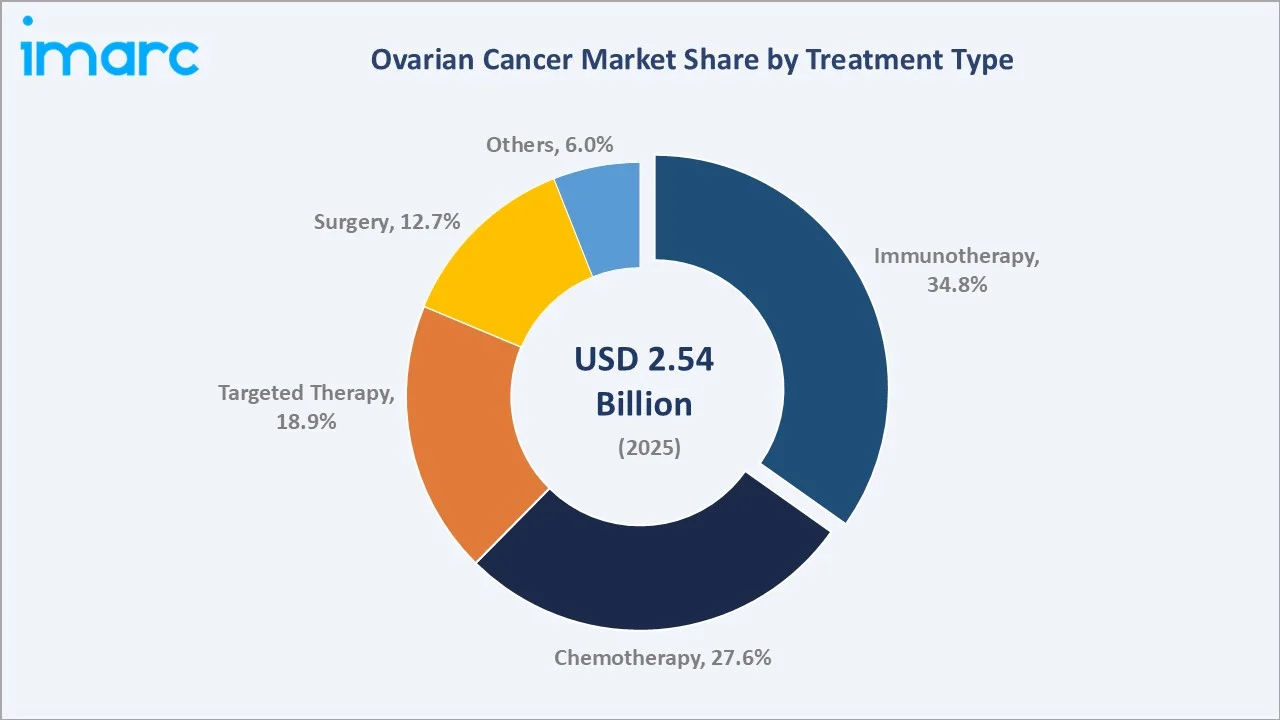

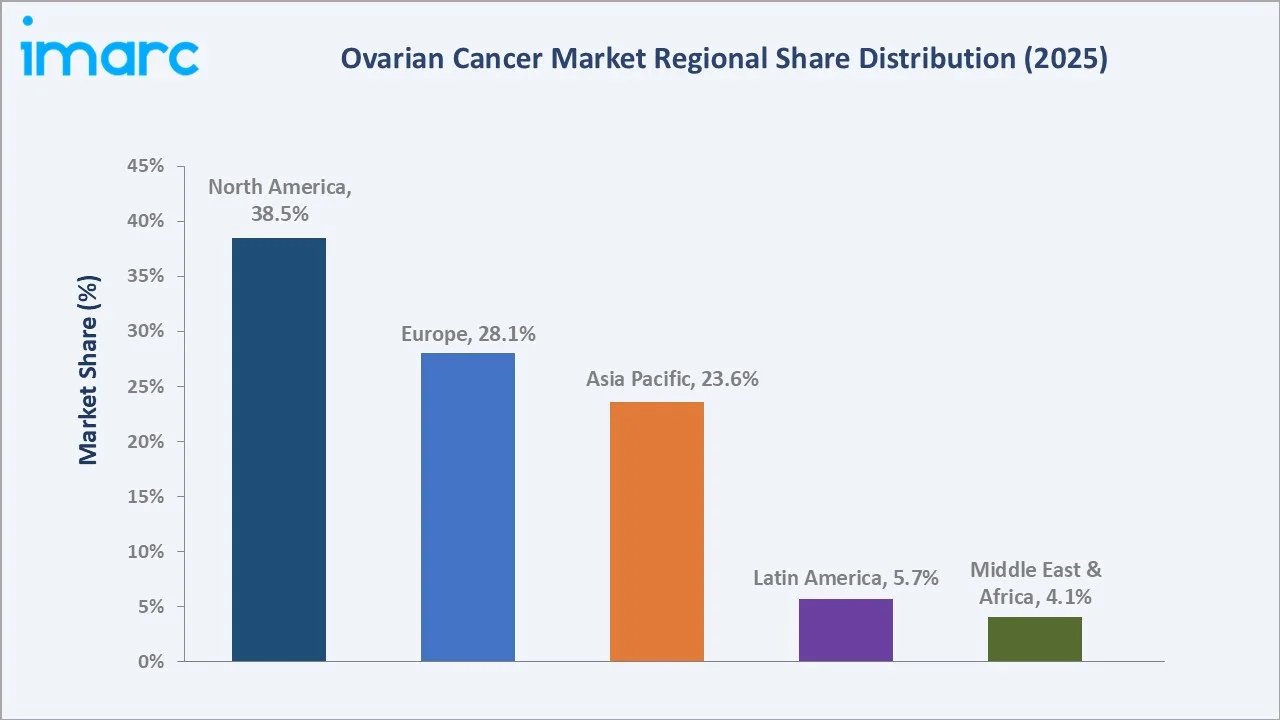

The global ovarian cancer market reached USD 2.54 Billion in 2025 and is projected to reach USD 5.76 Billion by 2034, growing at a CAGR of 9.21% during 2026-2034. According to the American Cancer Society, ovarian cancer is a significant health burden in the United States in 2026, with about 21,010 women newly diagnosed and about 12,450 women are expected to die from the disease by the end of 2026. These figures highlight the continued clinical need for better ovarian cancer detection, treatment, and disease management. Epithelial ovarian cancer dominates at 71.6%. Immunotherapy leads the treatment at 34.8%. North America commands 38.5% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.54 Billion |

|

Forecast Market Size (2034) |

USD 5.76 Billion |

|

CAGR (2026-2034) |

9.21% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Epithelial Ovarian Cancer (71.6%, 2025) |

|

Dominant Treatment Type |

Immunotherapy (34.8%, 2025) |

|

Leading Region |

North America (38.5%, 2025) |

The market expanded from USD 1.64 Billion in 2020 to USD 2.54 Billion in 2025, anchored at USD 3.95 Billion in 2030, and forecast to reach USD 5.76 Billion by 2034. The FDA's March 2024 full approval of mirvetuximab soravtansine-gynx for adult patients with FRα-positive, platinum-resistant epithelial ovarian cancer is opening a new era of targeted therapy.

To get more information on this market, Request Sample

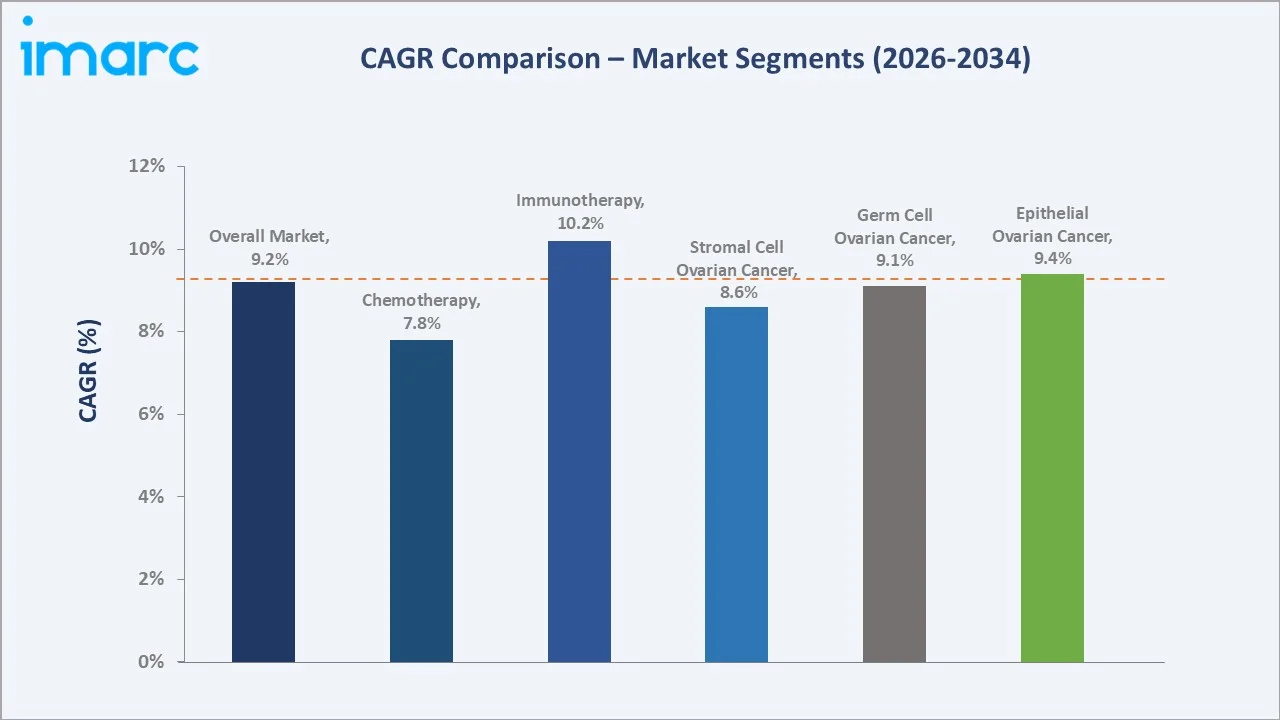

Immunotherapy grows fastest at ~10.2% CAGR as checkpoint inhibitor combinations with PARP inhibitors, ADCs, and bevacizumab progress through late-stage clinical development. Epithelial OC grows fastest at ~9.4% CAGR within the cancer type segmentation, as HGSOC's molecular complexity continues generating the most active pharmaceutical development.

Executive Summary

The global ovarian cancer market reached USD 2.54 Billion in 2025, representing a therapeutic area that has undergone more transformative pharmaceutical innovation in the preceding decade than the preceding five decades combined. Ovarian cancer remains the deadliest gynaecologic malignancy. The disease's poor prognosis, driven by late-stage diagnosis and high relapse rates, creates a large, medically underserved patient population representing a commercially attractive therapeutic target for sustained pharmaceutical investment. The market is projected to reach USD 5.76 Billion by 2034.

Immunotherapy at 34.8% leads the treatment revenue through the broad commercial use of checkpoint inhibitors in biomarker-selected ovarian cancer populations. Epithelial ovarian cancer at 71.6% dominates through the high-grade serous ovarian carcinoma (HGSOC) subtype's near-universal platinum sensitivity that creates the foundation for post-chemotherapy maintenance therapy. North America dominates regionally at 38.5%.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Epithelial Ovarian Cancer - 71.6% share (2025) |

|

Dominant Treatment Type |

Immunotherapy - 34.8% market share (2025) |

|

Leading Region |

North America - 38.5% market share (2025) |

|

Market Opportunity |

PARP inhibitor maintenance therapy expansion; BRCA/HRD biomarker-guided treatment; immunotherapy combination regimens; Asia-Pacific access program scale-up |

Key Analytical Observations Supporting the Above Data:

- Epithelial ovarian cancer at 71.6%: Epithelial ovarian cancer (EOC) accounts for the majority of ovarian cancer cases, making it the dominant segment due to its high prevalence and significant treatment demand. Its late-stage diagnosis and aggressive nature further drive the need for targeted therapies and innovative treatments.

- Immunotherapy at 34.8%: The immunotherapy segment leads the market because it offers promising outcomes by harnessing the immune system to target tumor cells, especially in patients resistant to conventional therapies. Ongoing clinical advancements and increasing adoption of checkpoint inhibitors and personalized immunotherapies fuel its growth.

- North America at 38.5%: North America dominates the market due to advanced healthcare infrastructure, high awareness of early detection, strong R&D investment, and widespread adoption of innovative therapies. The region’s favorable reimbursement policies and robust clinical trial activity further support market growth.

Ovarian Cancer Market Overview

The global ovarian cancer market encompasses the pharmaceutical and therapeutic interventions for all histological subtypes of ovarian malignancy, epithelial ovarian cancer, germ cell tumours and sex cord-stromal tumours, across all lines of therapy from initial surgical staging and first-line chemotherapy through maintenance therapy, platinum-sensitive relapsed treatment, and platinum-resistant salvage regimens.

The market ecosystem integrates pharmaceutical and biotechnology manufacturers, clinical trial sponsors and contract research organisations, gynaecologic oncology academic medical centres and community oncology practices, molecular diagnostic companies, payers, and patient advocacy organisations. Macroeconomic factors include rising healthcare expenditure, increasing government and private funding for cancer research, and higher patient access to advanced diagnostics and therapies.

Market Dynamics

To evaluate market opportunities, Request Sample

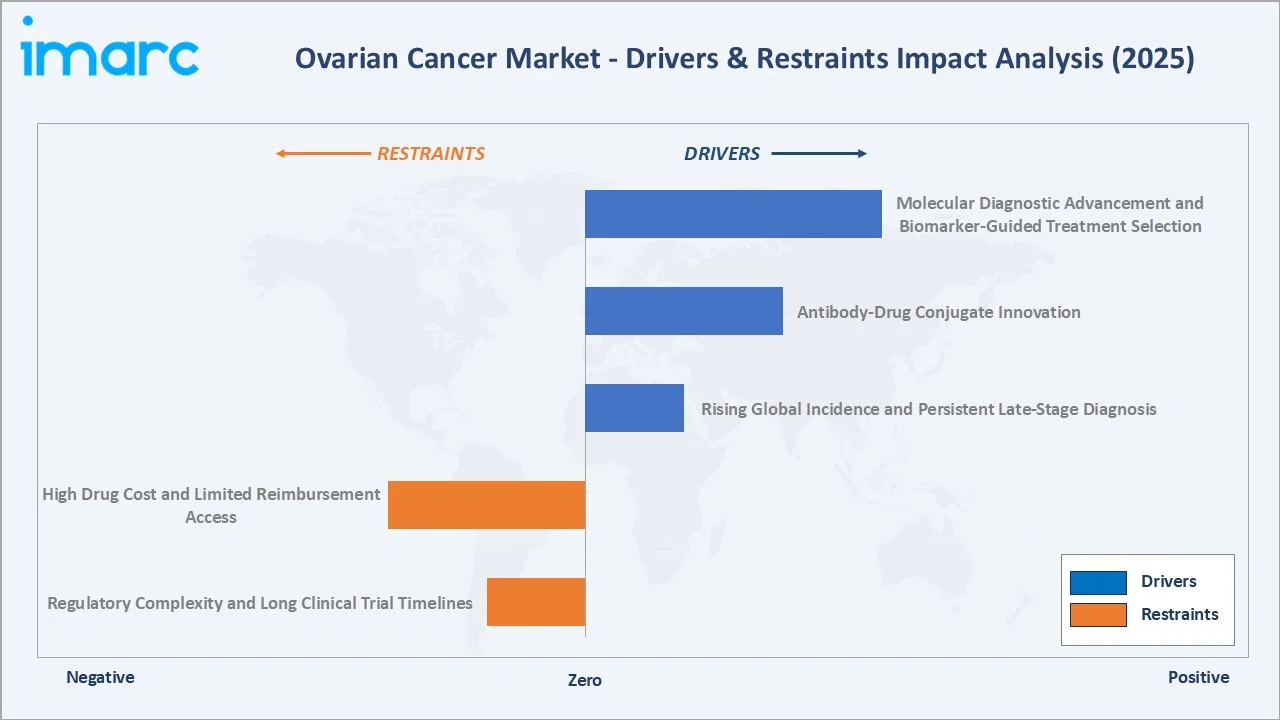

Market Drivers

- Rising Global Incidence and Persistent Late-Stage Diagnosis: The American Cancer Society estimated that about 21,010 women will receive a new diagnosis of ovarian cancer and about 12,450 women will die from ovarian cancer in the United States by the end of 2026. This rising global incidence of ovarian cancer is expanding the pool of patients in need of diagnosis and treatment, while the persistent late-stage diagnosis creates an urgent demand for effective therapies and advanced diagnostic solutions.

- Antibody-Drug Conjugate Innovation: Antibody-drug conjugate (ADC) innovations are offering highly targeted therapies that deliver cytotoxic drugs directly to cancer cells while minimizing damage to healthy tissue. These advancements improve treatment efficacy, reduce side effects, and address unmet needs in recurrent or resistant ovarian cancer cases, boosting adoption and fueling market growth.

- Molecular Diagnostic Advancement and Biomarker-Guided Treatment Selection: Advancements in molecular diagnostics and biomarker-guided treatment selection are enabling early detection, precise patient stratification, and personalized therapy choices. These technologies help identify patients most likely to benefit from targeted treatments or immunotherapies, improving outcomes and reducing unnecessary interventions. Consequently, the demand for genetic testing, companion diagnostics, and precision medicine approaches is rapidly expanding, driving market growth.

Market Restraints

- High Drug Cost and Limited Reimbursement Access: High drug costs and limited reimbursement access are making advanced therapies less affordable and less accessible for many patients. This financial burden can delay treatment initiation, reduce therapy adherence, and limit the adoption of innovative drugs, particularly in emerging markets or underinsured populations, thereby slowing overall market growth.

- Regulatory Complexity and Long Clinical Trial Timelines: Regulatory complexity and long clinical trial timelines are delaying the approval and launch of new therapies. Lengthy trials, stringent regulatory requirements, and extensive safety evaluations increase development costs and slow patient access to innovative treatments, which can limit market expansion and investment in novel drugs.

Market Opportunities

- PARP Inhibitor Combination Strategies Creating Additive Revenue Beyond Single-Agent PARP Monotherapy: PARP inhibitor combination strategies improve efficacy over monotherapy. Combining PARP inhibitors with other targeted therapies or immunotherapies can improve patient outcomes, expand treatment eligibility, and generate additional revenue streams, driving both clinical adoption and market growth.

- Asia-Pacific Generic PARP Inhibitor Market Creating Volume-Driven Growth Independent of Brand-Drug Pricing: The Asia-Pacific generic PARP inhibitor market is making effective therapies more affordable and widely accessible, independent of high brand-drug pricing. This expansion enables broader patient access, increases treatment uptake, and stimulates market growth in the region, especially in cost-sensitive healthcare systems.

Market Challenges

- PARP Inhibitor Market Saturation and Generic Competition Threatening Originator Revenue Streams: PARP inhibitor market saturation and rising generic competition pose a challenge by eroding revenue for originator drugs. As multiple brands and generics enter the market, pricing pressures intensify, profit margins shrink, and companies face increased competition, potentially limiting investment in new drug development and innovation.

- Clinical Failure Risk in Immunotherapy Ovarian Cancer Programs: Clinical failure risk in immunotherapy programs poses a challenge by creating uncertainty around the efficacy and approval of new treatments. Failed or inconclusive trials can delay drug launches, reduce investor confidence, and limit patient access to innovative therapies, ultimately slowing market growth and adoption in this high-potential segment.

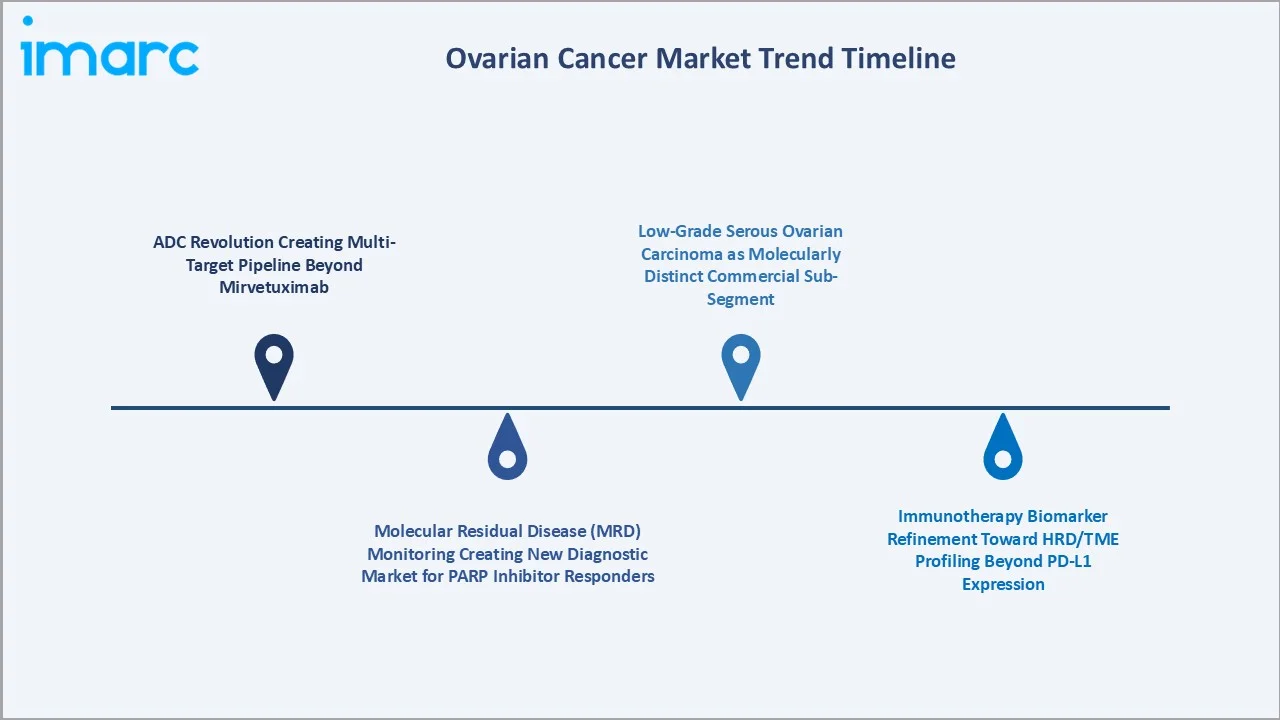

Emerging Market Trends

1. ADC Revolution in Ovarian Cancer Creating Multi-Target Pipeline Beyond Mirvetuximab

The ADC (antibody-drug conjugate) revolution is expanding the pipeline beyond Mirvetuximab to target multiple tumor antigens. This innovation enables more precise, effective therapies, addresses treatment-resistant cases, and drives market expansion through novel, next-generation ADC candidates under development. In March 2024, AbbVie announced that the U.S. Food and Drug Administration (FDA) granted full approval for ELAHERE (mirvetuximab soravtansine-gynx) for the treatment of folate receptor alpha (FRα)-positive, platinum-resistant epithelial ovarian, fallopian tube or primary peritoneal adult cancer patients treated with up to three prior therapies. ELAHERE is the first and only antibody-drug conjugate (ADC) approved.

2. Molecular Residual Disease (MRD) Monitoring Creating New Diagnostic Market for PARP Inhibitor Responders

Molecular Residual Disease (MRD) monitoring enables early detection of minimal residual disease and identifies patients who respond to PARP inhibitors. This approach supports personalized treatment decisions, optimizes therapy duration, and opens a new diagnostic market, driving adoption of companion diagnostics and precision oncology tools.

3. Immunotherapy Biomarker Refinement Toward HRD/TME Profiling Beyond PD-L1 Expression

Immunotherapy biomarker refinement is emerging in the market by moving beyond PD-L1 expression to focus on HRD (homologous recombination deficiency) and TME (tumor microenvironment) profiling. This enables more precise patient selection, improved treatment response prediction, and tailored immunotherapy strategies, driving innovation and adoption in precision oncology.

4. Low-Grade Serous Ovarian Carcinoma Emerging as Molecularly Distinct Commercial Sub-Segment

Low-Grade Serous Ovarian Carcinoma (LGSOC) is emerging as a molecularly distinct commercial sub-segment within the ovarian cancer market due to its unique genetic and biological profile compared to high-grade tumors. Recognizing LGSOC as a separate entity is driving targeted drug development, specialized clinical trials, and tailored therapeutic strategies. Approximately 3 to 9% of ovarian cancers are pathologically defined as the low-grade serous type. This segmentation creates opportunities for precision medicine approaches, niche treatments, and dedicated commercial strategies, expanding the overall market by addressing previously underserved patient populations.

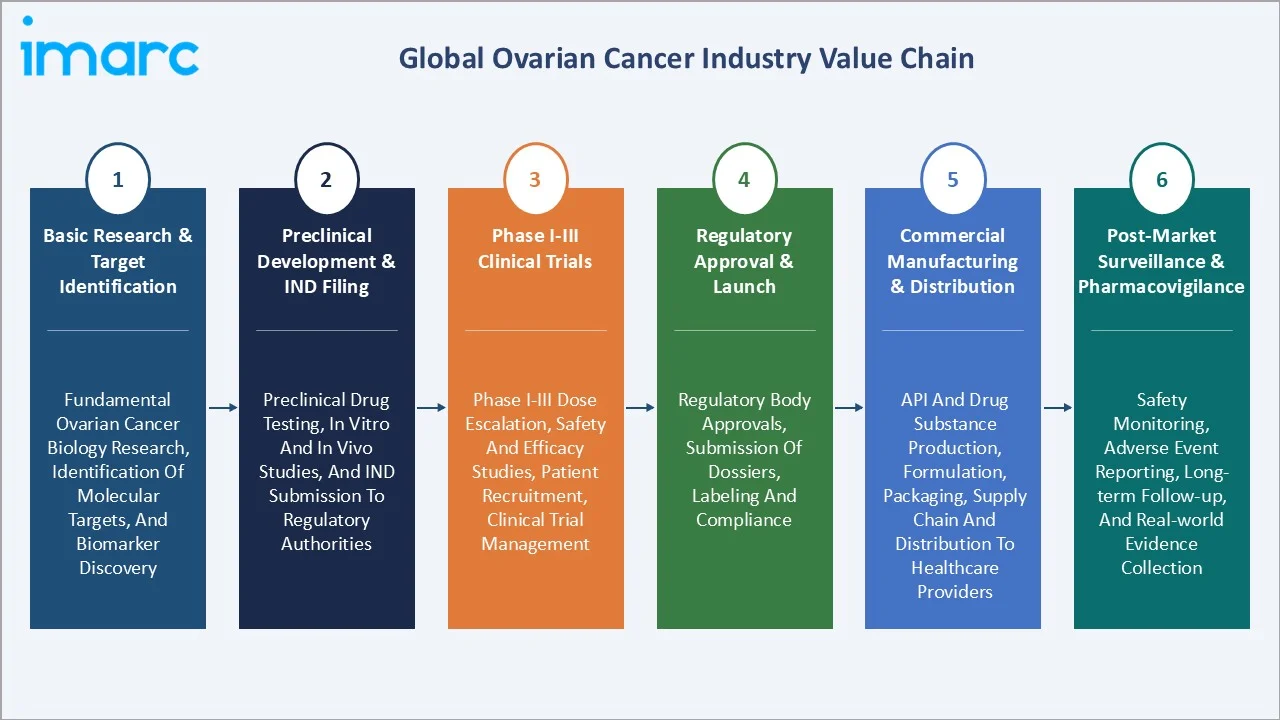

Industry Value Chain Analysis

The ovarian cancer drug development value chain integrates basic research and target identification, preclinical development and IND filing, Phase I-III clinical trials, regulatory approval and launch, commercial manufacturing and distribution, and post-market surveillance and pharmacovigilance.

|

Stage |

Key Participants |

|

Basic Research & Target Identification |

Fundamental ovarian cancer biology research, identification of molecular targets, and biomarker discovery |

|

Preclinical Development & IND Filing |

Preclinical drug testing, in vitro and in vivo studies, and IND submission to regulatory authorities |

|

Phase I-III Clinical Trials |

Phase I-III dose escalation, safety and efficacy studies, patient recruitment, clinical trial management |

|

Regulatory Approval & Launch |

Regulatory body approvals, submission of dossiers, labeling and compliance |

|

Commercial Manufacturing & Distribution |

API and drug substance production, formulation, packaging, supply chain and distribution to healthcare providers |

|

Post-Market Surveillance & Pharmacovigilance |

Safety monitoring, adverse event reporting, long-term follow-up, and real-world evidence collection |

The post-market surveillance and real-world evidence tier has become commercially important in ovarian cancer beyond standard pharmacovigilance. The companion diagnostic value chain is co-dependent with the PARP inhibitor commercial chain, creating a diagnostic revenue stream that compounds with expanding PARP inhibitor treatment rates.

Technology Landscape in the Ovarian Cancer Industry

PARP Inhibitor Technology

PARP inhibitor technology is establishing a robust technology landscape focused on DNA repair-targeted therapies. These inhibitors enable personalized treatment strategies, combination therapy development, and companion diagnostic integration, fostering innovation and creating a competitive ecosystem for research, clinical development, and commercial opportunities. In January 2026, 858 Therapeutics announced that the U.S. Food and Drug Administration (FDA) granted Fast Track designation to ETX-19477, a PARG inhibitor granted for the treatment of adult patients with BRCA-mutated, platinum-resistant, high-grade serous ovarian cancer (HGSOC).

Antibody-Drug Conjugate Technology

Antibody-drug conjugate (ADC) technology creates a precision-targeted therapeutic landscape that combines monoclonal antibodies with cytotoxic payloads. This technology enables highly selective tumor targeting, minimizes off-target toxicity, and supports combination regimens. It drives innovation in next-generation ADC development, multi-antigen targeting, and pipeline diversification, establishing a competitive and rapidly evolving technological ecosystem in ovarian cancer treatment.

Immunotherapy and Checkpoint Inhibitor Technology

Immunotherapy and checkpoint inhibitor technology are developing therapies that activate the immune system to recognize and attack tumor cells. This technology enables personalized treatment approaches based on biomarkers like PD-L1, HRD, and TME profiling, supports combination regimens with PARP inhibitors or chemotherapy, and drives a growing pipeline of novel immunotherapies, creating a dynamic and evolving technological landscape in ovarian cancer care.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Epithelial Ovarian Cancer | 71.6% | 2025 |

| Treatment Type | Immunotherapy | 34.8% | 2025 |

| End User | 🔒 | 🔒 | 2025 |

| Region | North America | 38.5% | 2025 |

By Type

Epithelial ovarian cancer leads at 71.6% market share (2025). EOC encompasses high-grade serous, low-grade serous, endometrioid, clear cell, and mucinous histological subtypes, each with distinct molecular biology, treatment response, and emerging targeted therapy landscape. HGSOC within EOC dominates clinical and commercial activity, generating the entire PARP inhibitor maintenance therapy market revenue.

To access detailed market analysis, Request Sample

Germ cell ovarian cancer at 17.9% primarily generates chemotherapy revenue from this predominantly young-patient, curable malignancy. Stromal cell ovarian cancer at 10.5% encompasses granulosa cell tumour and hormonal therapy revenue, plus chemotherapy for aggressive stromal tumours.

By Treatment Type

Immunotherapy leads at 34.8% market share (2025). Immunotherapy encompasses FDA-approved checkpoint inhibitors as an indirect immune modulator and investigational combination revenue. Chemotherapy at 27.6% reflects the universal first-line carboplatin-paclitaxel regimen plus salvage chemotherapy in platinum-resistant disease.

Targeted therapy at 18.9% covers PARP inhibitors and Elahere (mirvetuximab soravtansine-gynx) as the primary targeted therapy products. Surgery at 12.7% encompasses cytoreductive surgery, laparoscopic staging, and fertility-preserving surgery revenue. Others at 6.0% includes radiation therapy, hormonal therapy in stromal and LGSOC, and supportive care oncology products.

Regional Market Insights

|

Region |

Share (2025) |

Key Ovarian Cancer Market Drivers & Characteristics |

|

North America |

38.5% |

Driven by advanced healthcare infrastructure, high healthcare expenditure, strong R&D presence, and early adoption of innovative therapies. |

|

Europe |

28.1% |

Supported by well-established healthcare systems, growing awareness, and access to advanced diagnostics and targeted therapies. |

|

Asia-Pacific |

23.6% |

Driven by a large patient population, increasing incidence rates, rising awareness, and expanding access to diagnostics and treatment options. |

|

Latin America |

5.7% |

Characterized by limited access to advanced therapies, late-stage diagnosis, and evolving healthcare infrastructure. |

|

Middle East and Africa |

4.1% |

Market growth is influenced by emerging healthcare systems, rising awareness, and the adoption of targeted and precision therapies. |

North America, at 38.5%, leads through US commercial drug pricing and the FDA's innovative regulatory pathway enabling rapid new drug access. Europe, at 28.1%, reflects one of the major markets for established PARP inhibitors alongside active clinical trial participation. Asia-Pacific, at 23.6%, is the market's fastest-growing region, driven by Chinese generic PARP inhibitor expansion and improving oncology infrastructure across India, Japan, and South Korea.

Latin America, at 5.7%, reflects Brazil and Mexico's growing PARP inhibitor access through private insurance and progressive reimbursement evaluation, while MEA, at 4.1%, encompasses GCC high-income country access alongside sub-Saharan Africa's largely chemotherapy-limited treatment environment.

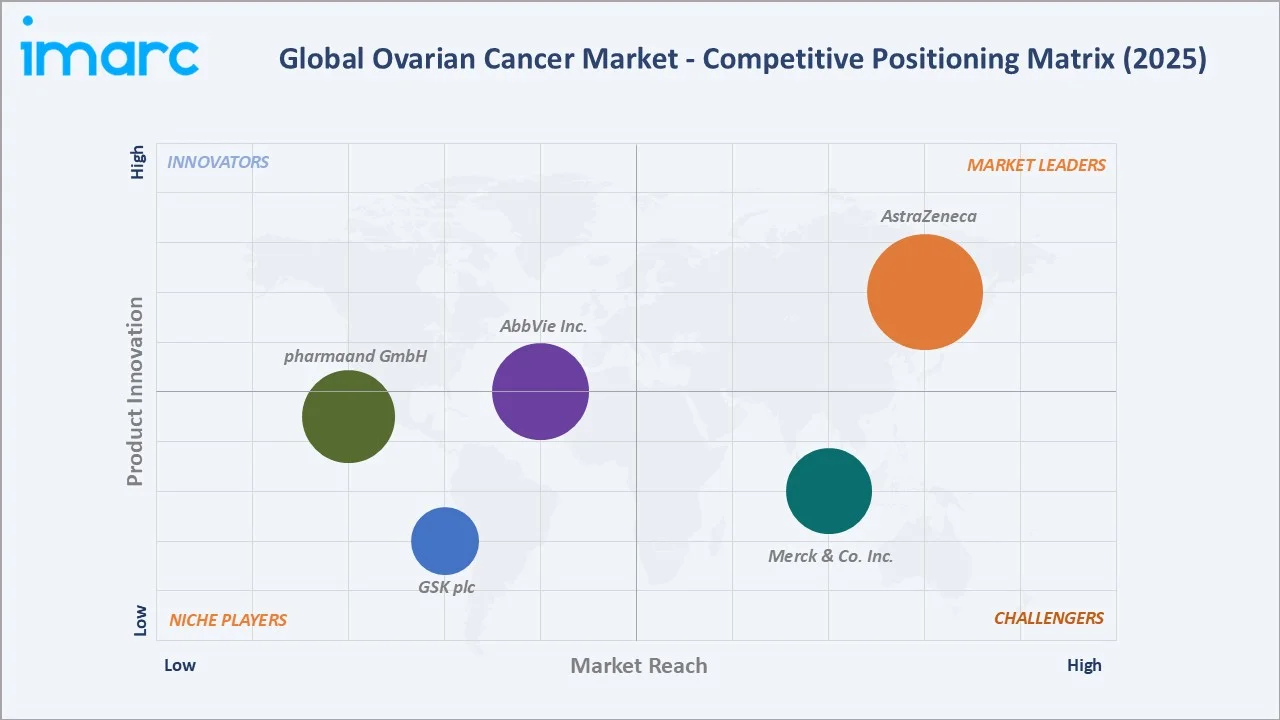

Competitive Landscape

The ovarian cancer competitive landscape is highly concentrated. The competitive landscape is being redefined by patent expiry and generic competition pressures on first-generation PARP inhibitors, the clinical and commercial validation of ADCs as the new targeted therapy class, and the ongoing Phase III immunotherapy combination trials that will determine whether checkpoint inhibitors achieve meaningful commercial penetration beyond biomarker-selected subpopulations.

| Company Name | Key Products | Market Position | Core Strength |

|---|---|---|---|

| AstraZeneca | Lynparza (olaparib) | Market Leader | LYNPARZA is a prescription medicine used to treat adults with ovarian, fallopian tube, or primary peritoneal cancer. |

| GSK plc | ZEJULA (niraparib) | Niche Player | ZEJULA is a prescription medication indicated for maintenance treatment in adults with advanced ovarian, fallopian tube, or primary peritoneal cancer. |

| AbbVie Inc. | ELAHERE (mirvetuximab soravtansine-gynx) | Established Player | ELAHERE is a prescription medicine for adults with folate receptor-alpha positive (FRα+) ovarian cancer, fallopian tube cancer, or primary peritoneal cancer. |

| Merck & Co. Inc. | KEYTRUDA (pembrolizumab) and KEYTRUDA QLEX (pembrolizumab and berahyaluronidase alfa-pmph) | Challenger | KEYTRUDA and KEYTRUDA QLEX are the first and only PD-1 inhibitors approved for the treatment of platinum-resistant epithelial ovarian, fallopian tube or primary peritoneal carcinoma with PD-L1+ tumors. |

| pharmaand GmbH | Rubraca (rucaparib) | Established Player | RUBRACA tablets are a prescription medicine used as the maintenance treatment for ovarian cancer, fallopian tube cancer, or primary peritoneal cancer. |

The competitive dynamics are shaped by the companion diagnostic tie. AbbVie's Elahere occupies a distinct competitive position, enabling Elahere to expand the addressable treatment market rather than compete with PARP inhibitors for the same patients.

Key Company Profiles

AstraZeneca

AstraZeneca is one of the world's leading ovarian cancer drug companies through Lynparza (olaparib), the approved PARP inhibitor and one of the highest-revenue ovarian cancer drugs globally.

- Key Products: Lynparza (olaparib).

- Strategic Focus: Advancing targeted therapies and PARP inhibitors to provide personalized maintenance treatment for patients with ovarian cancer.

GSK plc

GSK plc is also one of the world's largest PARP inhibitor companies through Zejula (niraparib). GSK's Zejula (niraparib) is a once-daily, oral PARP inhibitor approved for maintenance treatment in adults with advanced ovarian, fallopian tube, or primary peritoneal cancer.

- Key Products: ZEJULA (niraparib).

- Recent Developments: In August 2025, GSK launched its two leading endometrial and ovarian cancer drugs Jemperli (Dostarlimab) and Zejula (Niraparib) in India.

- Strategic Focus: Developing innovative immunotherapies and combination treatments to improve outcomes in hard-to-treat ovarian cancer patients.

Market Concentration Analysis

The ovarian cancer drug market is moderately concentrated among the top-3 revenue-generating companies, AstraZeneca, GSK plc, and AbbVie Inc., collectively representing approximately 65-70% of total ovarian cancer drug market revenue (2025) through their approved drugs as the three highest-revenue products. The competitive dynamics will shift materially by 2028-2030 as the top-3 company revenue concentration decreases to approximately 50-55% and a more fragmented multi-class treatment environment emerges with PARP inhibitors, ADCs, IO combinations, and novel synthetic lethal agents each contributing meaningful revenue.

Investment & Growth Opportunities

Highest Growth Segments

Immunotherapy (~10.2% CAGR), epithelial OC (~9.4% CAGR), ADC targeted therapy within targeted therapy segment (~20-25% CAGR from small base through Elahere launch), Asia-Pacific regional market (~11-12% CAGR), molecular diagnostic companion testing (~15-18% CAGR), and next-generation synthetic lethality drugs beyond PARP (~30-40% CAGR from near-zero base as Phase III data emerge 2026-2030) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

The combination of ADC expansion in ovarian cancer and the emerging post-PARP inhibitor synthetic lethality pipeline creates a multi-wave clinical development opportunity where sequential drug development waves are generating recurring commercial opportunities across the decade. Companies positioned in ADC manufacturing and next-generation biomarker development are commercially advantaged by participation across multiple waves rather than a single drug platform.

Investment Themes

- Post-PARP inhibitor treatment landscape development for PARP inhibitor-resistant EOC: The PARP inhibitor-resistant platinum-resistant EOC patient population represents the most commercially valuable unmet need in ovarian cancer, patients who have already been treated with platinum, bevacizumab, and a PARP inhibitor and are progressing through all standard options.

- Asia-Pacific generic PARP inhibitor access program development for volume-driven market expansion: The commercialisation of generic drugs through China insurance negotiation, India regulatory approval, and other Asia-Pacific national health insurance programs at 10-20% of US reference pricing creates volume-driven market expansion that benefits generic manufacturers, API producers, and the broader drug distribution ecosystem in Asia-Pacific.

Future Market Outlook (2026-2034)

The global ovarian cancer market is projected to grow from USD 2.54 Billion in 2025 to USD 5.76 Billion by 2034, delivering a 9.21% CAGR over the forecast period. The market's anchor value of USD 3.95 Billion in 2030 represents an ovarian cancer treatment landscape at a pivotal commercial and clinical transition, PARP inhibitor maintenance therapy is approaching market maturity with generic competition, ADC therapy with Elahere is establishing commercial scale as the new standard for platinum-resistant EOC, and the Phase III immunotherapy combination trial data are resolving whether checkpoint inhibitor combinations achieve a meaningful commercial role in the first-line and maintenance settings.

Three structural forces define ovarian cancer market growth through 2034. The PARP inhibitor maintenance treatment rate expansion creates incremental treatment rate-driven growth that is independent of price changes and represents the largest near-term commercial growth driver for AstraZeneca and GSK. The ADC pipeline maturation creates a multi-drug ADC commercial expansion that cumulatively adds USD 1.0-2.0 Billion to the ovarian cancer market by 2030 as multiple ADC approvals are achieved. The Asia-Pacific access expansion collectively adds USD 400-700 Million in Asia-Pacific market revenue by 2030 at regional pricing, reflecting the volume-driven market expansion complementing the pricing-driven Western market growth.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including Gynaecologic Oncology Directors; Senior Medical Affairs Directors; Payer and Health Technology Assessment analysts; Clinical Trial Leaders; Molecular Diagnostic Directors; and patient advocacy representatives.

Secondary Research

Secondary research encompassed FDA Oncology Drug Approval Data; EMA European Public Assessment Reports; ovarian cancer incidence and survival data; GLOBOCAN global ovarian cancer epidemiology; Annual Meeting ovarian cancer presentations; ovarian cancer clinical practice guidelines; company annual reports; ovarian cancer drug sales forecast; ovarian cancer pipeline database. Over 65 secondary sources reviewed.

Forecasting Models

Market revenue forecasts were developed using an epidemiology-based bottom-up model: (i) annual incidence projection by region; (ii) treatment pathway penetration modelling; (iii) per-patient drug cost by country; (iv) treatment rate progression forecasts, calibrated against Historical drug sales data by indication, sales forecasts, and company-disclosed product revenue guidance.

Ovarian Cancer Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Epithelial Ovarian Cancer, Germ Cell Ovarian Cancer, Stromal Cell Ovarian Cancer |

| Treatment Types Covered | Immunotherapy, Chemotherapy, Targeted Therapy, Surgery, Others |

| End Users Covered | Hospitals, Homecare, Speciality Centre, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | AstraZeneca, GSK plc, AbbVie Inc., Merck & Co. Inc., pharmaand GmbH, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the ovarian cancer market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global ovarian cancer market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the ovarian cancer industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Ovarian Cancer Market Report

The global ovarian cancer market reached USD 2.54 Billion in 2025, driven by PARP inhibitor maintenance therapy as the highest-revenue drug class, bevacizumab Avastin across multiple ovarian cancer indications, the commercial launch of Elahere as the first FDA-approved ADC, expanding companion diagnostic testing enabling targeted therapy patient selection, and growing Asia-Pacific market access for PARP inhibitors through generic entry and national health insurance coverage expansion.

The market grows at 9.21% CAGR during 2026-2034, reaching USD 5.76 Billion by 2034, driven by PARP inhibitor treatment rate expansion, ADC commercial launch and label expansion, immunotherapy combination Phase III data, next-generation synthetic lethality drugs entering Phase III 2026-2030, and Asia-Pacific market access expansion through China's generic PARP inhibitor coverage and India approval.

Epithelial ovarian cancer (EOC) leads at 71.6% through HGSOC's near-universal platinum sensitivity, creating the first-line chemotherapy and PARP inhibitor maintenance therapy market. EOC also grows fastest at ~9.4% CAGR.

Immunotherapy leads at 34.8% through checkpoint inhibitors in bevacizumab indirect immune modulation, and investigational IO combination revenue. Immunotherapy also grows fastest at ~10.2% CAGR.

North America leads at 38.5% through US commercial drug pricing, the FDA accelerated approval pathway enabling the fastest new drug access, and an established oncology infrastructure.

Leading companies include AstraZeneca, GSK plc, AbbVie Inc., Merck & Co. Inc., and pharmaand GmbH, among others.

The market is projected to reach approximately USD 3.95 Billion by 2030, with Elahere annual revenue growth, immunotherapy combination Phase III results determining the IO commercial trajectory, and generics entry in the US beginning to reduce branded revenue.

Three priority opportunities: ADC ovarian cancer approval, liquid biopsy monitoring platform, and post-PARP inhibitor synthetic lethality drug development.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)