Pain Management Drugs Market Size, Share, Trends and Forecast by Drug Class, Indication, Distribution Channel, and Region, 2026-2034

Pain Management Drugs Market Size and Share:

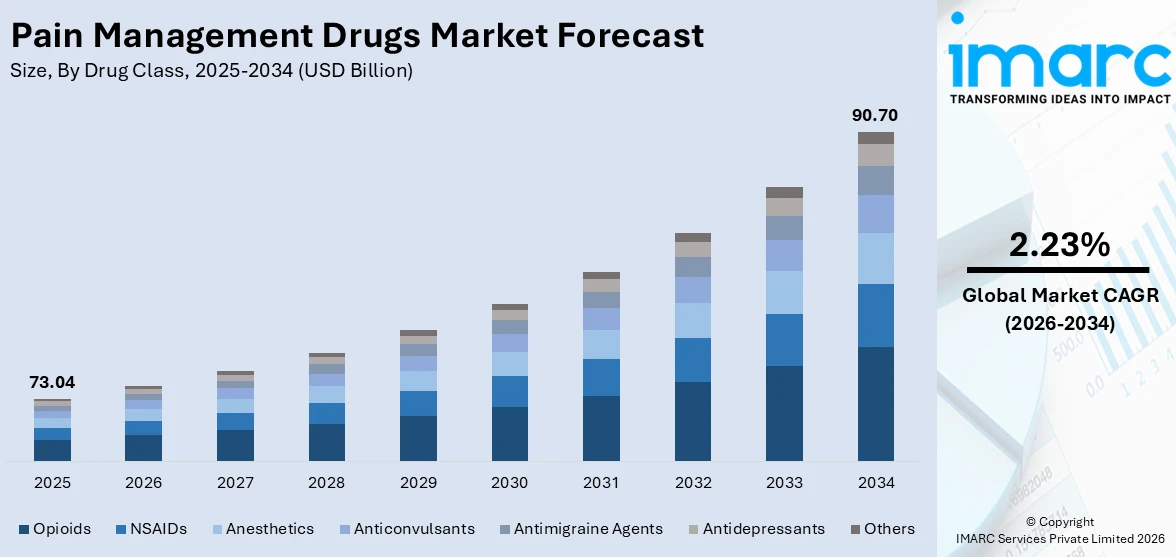

The global pain management drugs market size was valued at USD 73.04 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 90.70 Billion by 2034, exhibiting a CAGR of 2.23% from 2026-2034. North America currently dominates the market, holding a market share of 45% in 2025. The region benefits from its advanced healthcare infrastructure, comprehensive insurance coverage frameworks facilitating broad access to diverse and innovative pain therapies, a high prevalence of chronic pain conditions among its growing aging population, and substantial pharmaceutical research and development investments, all collectively reinforcing the pain management drugs market share.

The global pain management drugs market is being driven by the rising prevalence of chronic pain disorders, including arthritis, lower back pain, and neuropathic conditions, which affect a substantial portion of the global population. The increasing geriatric demographic worldwide is contributing to a higher demand for effective pain relief solutions, as older adults are more susceptible to degenerative musculoskeletal conditions and postoperative pain. Additionally, the growing burden of lifestyle-related ailments such as obesity and diabetes-related neuropathy is fueling the need for advanced analgesic therapies. Ongoing advancements in drug delivery technologies, including transdermal patches and extended-release formulations, are enhancing patient compliance and therapeutic outcomes, thereby supporting the pain management drugs market growth on a global scale.

The United States has emerged as a major region in the pain management drugs market owing to many factors. The well-developed healthcare infrastructure supports early diagnosis and treatment of pain-related conditions, while extensive insurance coverage facilitates patient access to a broad range of pain management therapies. In 2025, the U.S. Food and Drug Administration approved Journavx (suzetrigine) a first‑in‑class non‑opioid analgesic developed by Vertex Pharmaceuticals offering a novel alternative to traditional opioids for moderate‑to‑severe acute pain. Furthermore, the presence of leading pharmaceutical companies and research institutions in the country fosters continuous innovation in pain management drug formulations, ensuring a robust pipeline of novel therapeutic agents aimed at improving efficacy and minimizing adverse effects for patients.

To get more information on this market Request Sample

Pain Management Drugs Market Trends:

Growing Shift Toward Non-Opioid Therapies

The pharmaceutical industry is witnessing a significant transition toward non-opioid pain management therapies driven by heightened awareness of the risks associated with long-term opioid use. Healthcare providers and policymakers are prioritizing the development and adoption of safer analgesic alternatives, including nonsteroidal anti-inflammatory drugs, anticonvulsants, and novel biologics targeting specific pain pathways. According to reports, survey data following the first year of the U.S. Non‑Opioids Prevent Addiction (NOPAIN) Act showed that over 80 % of hospitals and surgical centers reported decreasing perioperative opioid prescribing and increasing use of qualifying non‑opioid options in pain protocols. This shift is reinforced by updated clinical guidelines that recommend non-opioid treatments as first-line options for many pain conditions, particularly chronic musculoskeletal and neuropathic pain.

Advancements in Targeted Drug Delivery

Innovations in targeted drug delivery systems are transforming the pain management drugs market outlook by enabling more precise and sustained analgesic effects while minimizing systemic side effects. Transdermal patches, liposomal formulations, and implantable drug delivery devices are gaining traction as preferred methods for administering pain medications over extended periods. In February 2025, Aveva Drug Delivery Systems launched its generic fentanyl transdermal patch in the U.S., using advanced matrix technology designed to provide consistent extended pain relief while incorporating features to deter misuse. These technologies allow for controlled release of active pharmaceutical ingredients directly to the site of pain, reducing the need for frequent dosing and improving patient adherence to treatment regimens.

Integration of Digital Health Solutions

The convergence of digital health technologies and pain management pharmacotherapy is reshaping treatment paradigms and influencing the pain management drugs market trends across the globe. Mobile health applications and wearable devices are being integrated with pharmaceutical interventions to provide comprehensive pain monitoring and management solutions. These digital tools enable healthcare providers to track patient pain levels, medication usage patterns, and treatment outcomes in real time, facilitating data-driven adjustments to therapeutic regimens. In September 2025, Pier 88 Health and Theranica received regulatory approval in China for the Nerivio® REN wearable device, a prescribed digital therapeutic for migraine that exemplifies how digital pain technologies are gaining global clinical acceptance beyond traditional drug therapy. Telemedicine platforms are expanding access to pain specialists in underserved regions, improving diagnosis and prescription accuracy for patients with complex pain conditions.

Pain Management Drugs Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global pain management drugs market, along with forecast at the global, and regional levels from 2026-2034. The market has been categorized based on drug class, indication, and distribution channel.

Analysis by Drug Class:

- NSAIDs

- Anesthetics

- Anticonvulsants

- Antimigraine Agents

- Antidepressants

- Opioids

- Others

Opioids currently occupy a market share of 35%, which is a prominent category in pain management. Opioids are prescribed for moderate to severe pain conditions, such as postoperative pain, cancer pain, and advanced musculoskeletal diseases. Opioids work by interacting with opioid receptors in the central and peripheral nervous system, thus modulating pain perception. The use of opioids in the healthcare setting continues to be high due to their proven efficacy in the management of acute and chronic pain that is unresponsive to non-opioid options. Long-acting and abuse-deterrent formulations of opioids have been introduced to mitigate concerns about opioid abuse while still providing therapeutic benefits to patients who require chronic pain management. Healthcare professionals are increasingly turning to multimodal therapy that combines opioids with other treatments to provide improved pain relief while minimizing opioid use. Guidelines for opioid prescription continue to be refined to ensure prudent use while providing patients with access to pain management options.

Analysis by Indication:

- Musculoskeletal Pain

- Surgical and Trauma Pain

- Cancer Pain

- Neuropathic Pain

- Migraine Pain

- Obstetrical Pain

- Fibromyalgia Pain

- Burn Pain

- Dental/Facial Pain

- Pediatric Pain

- Others

Musculoskeletal pain leads the market with a share of 38%. Musculoskeletal pain encompasses a broad spectrum of conditions affecting bones, joints, muscles, tendons, and ligaments, making it one of the most prevalent pain categories globally. The high demand for medications targeting musculoskeletal pain is driven by the increasing incidence of osteoarthritis, rheumatoid arthritis, lower back pain, and sports-related injuries across diverse demographic groups. Aging populations worldwide are particularly susceptible to degenerative joint diseases and spinal disorders, sustaining consistent demand for effective pharmacological interventions. Treatment protocols for musculoskeletal pain typically involve nonsteroidal anti-inflammatory drugs, muscle relaxants, corticosteroids, and topical analgesics, with biologic therapies gaining prominence for refractory cases. The rising adoption of combination therapies and the development of disease-modifying agents are positively influencing the pain management drugs market forecast for this indication. Rehabilitation-focused treatment strategies that integrate pharmacotherapy with physical therapy are becoming standard practice, enhancing overall patient outcomes and driving sustained demand for targeted musculoskeletal pain medications.

Analysis by Distribution Channel:

Access the comprehensive market breakdown Request Sample

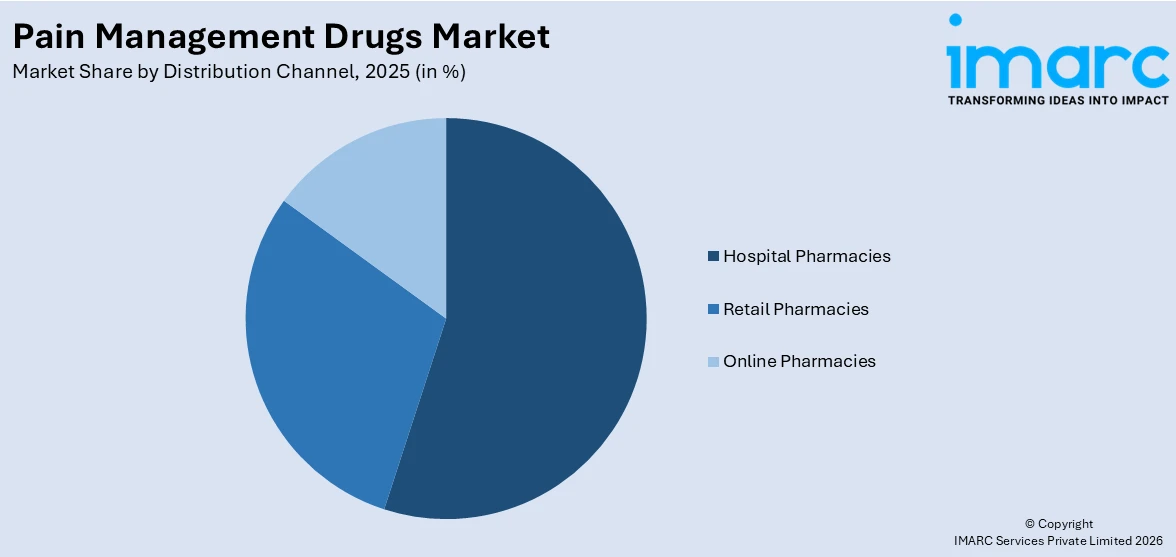

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Hospital pharmacies account for the largest market share of 55%, as they are the main distribution channel for pain management medications due to their direct link with the healthcare system. These pharmacies handle the distribution of controlled medications such as opioids and anesthetics. They are regulated by the relevant authorities to ensure that patients receive the medication correctly. The main reason for the large market share of hospital pharmacies is that they play a crucial role in the management of acute pain, surgical pain, and pain resulting from chronic illnesses. The hospital pharmacists work in collaboration with pain management teams to ensure that the drug selection and monitoring programs are optimized for individual patients. The rising number of surgeries, trauma cases, and cancer treatments in hospitals continues to drive the market through this distribution channel. The hospital pharmacies also handle formulary and bulk purchases that affect prescribing practices and ensure that patients have access to a wide range of analgesic medications at an affordable cost.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- Europe

- Asia Pacific

- Middle East and Africa

- Latin America

North America, with a market share of 45%, retaining the leading market position. The region enjoys a well-developed healthcare infrastructure with a strong focus on sophisticated diagnostic facilities, comprehensive insurance coverage, and universal access to both primary and specialty pain management care. The large number of patients with chronic pain conditions such as lower back pain, arthritis, and neuropathies in the region supports strong demand for various analgesic treatments. Well-developed pharmaceutical research infrastructure and the presence of major pharmaceutical companies in the region have helped to ensure steady innovation in pain management products, such as abuse-deterrent opioid formulations and new non-opioid modalities. Government policies to counter opioid abuse have spurred the development and launch of safer pain management products, promoting the concept of multimodal pain management. Reimbursement-friendly policies and government-sponsored pain management programs have also helped to ensure better accessibility to prescription pain management products in the region.

Key Regional Takeaways:

United States Pain Management Drugs Market Analysis

The United States represents a significant contributor to the pain management drugs market within North America, supported by the high prevalence of chronic and acute pain conditions across the population. The country possesses a well-established pharmaceutical ecosystem with robust research and development capabilities focused on developing next-generation analgesic therapies. In August 2025, the U.S. FDA approved Tonmya a non‑opioid treatment for fibromyalgia‑related pain, marking the first new therapy for this chronic pain condition in over 15 years and expanding patient options beyond traditional drugs. Healthcare providers are increasingly adopting evidence-based pain management protocols that integrate pharmacological treatments with complementary and alternative approaches, reflecting the evolving clinical landscape. The regulatory environment has shifted toward encouraging non-opioid alternatives, with expedited approval pathways for novel pain therapeutics that demonstrate improved safety profiles. The growing emphasis on personalized medicine is driving the development of genetic testing tools that help clinicians identify optimal pain medications for individual patients, reducing trial-and-error prescribing. Additionally, the expansion of outpatient pain management clinics and ambulatory surgical centers is diversifying drug distribution channels and improving access for patients in rural and underserved communities.

Europe Pain Management Drugs Market Analysis

The European market for pain management drugs is driven by a complex regulatory environment and well-established national healthcare systems that ensure widespread patient access to analgesic treatments. The region has a large burden of chronic pain disorders such as osteoarthritis, rheumatoid arthritis, and cancer pain, which continues to fuel demand for effective pharmacologic therapies. The European regulatory bodies have established tough guidelines for the use of opioids, thus encouraging the use of non-opioid alternatives and multimodal approaches to pain management. The focus on value-based healthcare in the major European economies is shaping formulary inclusion and encouraging the use of cost-effective generic analgesics in combination with innovative branded therapies. Research organizations and pharmaceutical companies in the region are working together on clinical trials for new pain therapies, including biologic and gene therapies that target specific pain pathways. In addition, the aging population in Western European nations is fueling the burden of degenerative musculoskeletal disorders, thus sustaining demand for long-term pain management strategies and rehabilitation pharmacotherapy.

Asia-Pacific Pain Management Drugs Market Analysis

The Asia-Pacific pain management drugs market is experiencing significant expansion driven by improving healthcare infrastructure, growing awareness of pain management options, and increasing healthcare expenditure across developing economies. The large and aging population base in countries throughout the region contributes to a rising burden of chronic pain conditions, including osteoarthritis, diabetic neuropathy, and cancer-related pain. Government initiatives aimed at expanding universal health coverage and improving access to essential medications are supporting increased utilization of analgesic therapies. The growing middle-class population with enhanced purchasing power is driving demand for advanced branded pain medications in addition to affordable generic alternatives. The region is also witnessing increased investment in pharmaceutical manufacturing capabilities, enabling local production of pain management drugs and reducing dependence on imports.

Latin America Pain Management Drugs Market Analysis

The Latin American pain management drugs market is expanding as healthcare infrastructure development progresses across the region, improving access to diagnostic and therapeutic services for pain management. The growing burden of chronic diseases, including diabetes and cardiovascular conditions, is increasing the prevalence of associated pain disorders that require pharmacological intervention. Government healthcare reforms aimed at expanding medication coverage and reducing out-of-pocket expenses are supporting broader patient access to analgesic therapies. The increasing urbanization across the region is facilitating greater awareness of pain treatment options and improving distribution networks for pharmaceutical products. Local generic drug manufacturers are playing a vital role in expanding access.

Middle East and Africa Pain Management Drugs Market Analysis

The Middle East and Africa pain management drugs market is developing steadily as regional healthcare systems undergo modernization and expansion. Growing government investment in healthcare infrastructure is improving access to pain management services, particularly in urban centers across the region. The increasing prevalence of chronic pain conditions linked to lifestyle changes, aging demographics, and road traffic injuries is driving demand for analgesic medications. International pharmaceutical companies are expanding their presence in the region through strategic partnerships with local distributors. Regulatory frameworks governing controlled substance distribution are evolving, facilitating safer and broader access to essential pain management medications for underserved populations.

Competitive Landscape:

The pain management drugs market is characterized by intense competition among established pharmaceutical companies, generic drug manufacturers, and emerging biotechnology firms. Major market players are focusing on expanding their product portfolios through the development of novel analgesic formulations, including abuse-deterrent opioids, non-opioid alternatives, and targeted biologic therapies. Strategic initiatives such as mergers, acquisitions, and licensing agreements are being pursued to strengthen market positions and gain access to innovative drug delivery technologies. Companies are investing heavily in clinical research to advance pipeline candidates through regulatory approval processes, with particular emphasis on drugs addressing unmet medical needs in chronic and neuropathic pain management. Competitive differentiation is being achieved through the development of extended-release formulations, combination therapies, and patient-centric drug delivery systems.

The report provides a comprehensive analysis of the competitive landscape in the pain management drugs market with detailed profiles of all major companies, including:

- Abbott Laboratories Inc.

- AbbVie Inc.

- Bausch + Lomb.

- Bayer AG

- Eli Lilly & Company

- GSK plc

- Pfizer Inc.

- Purdue Pharma L.P.

- Sanofi S.A

- Viatris Inc

Latest News and Developments:

- In January 2025, Strides Pharma Science received USFDA approval for its generic OTC Acetaminophen and Ibuprofen tablets (125 mg/250 mg), bioequivalent to Advil Dual Action, expanding its pain management portfolio and offering accessible dual-action pain relief from its Bengaluru manufacturing facility.

- In February 2025, VIVOZON Pharmaceutical received MFDS approval for UNAFRA Inj., the world’s first non-opioid, non-NSAID analgesic for moderate-to-severe pain. Using a dual mechanism targeting GlyT2 and 5HT2a, UNAFRA provides rapid pain relief with fewer side effects and zero addiction risk, marking a breakthrough in pain management therapies.

Pain Management Drugs Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Drug Classes Covered | NSAIDs, Anesthetics, Anticonvulsants, Antimigraine Agents, Antidepressants, Opioids, Others |

| Indications Covered | Musculoskeletal Pain, Surgical and Trauma Pain, Cancer Pain, Neuropathic Pain, Migraine Pain, Obstetrical Pain, Fibromyalgia Pain, Burn Pain, Dental/Facial Pain, Pediatric Pain, Others |

| Distribution Channels Covered | Hospital Pharmacies, Retail Pharmacies, Online Pharmacies |

| Regions Covered | North America, Europe, Asia Pacific, Middle East and Africa, Latin America |

| Companies Covered | Abbott Laboratories Inc., AbbVie Inc., Bausch + Lomb., Bayer AG, Eli Lilly & Company, GSK plc, Pfizer Inc., Purdue Pharma L.P., Sanofi S.A, Viatris Inc, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the pain management drugs market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global pain management drugs market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the pain management drugs industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Pain Management Drugs Market Report

The pain management drugs market was valued at USD 73.04 Billion in 2025.

The pain management drugs market is projected to exhibit a CAGR of 2.23% during 2026-2034, reaching a value of USD 90.70 Billion by 2034.

The pain management drugs market is driven by the rising prevalence of chronic pain conditions, increasing geriatric population, growing demand for non-opioid analgesic alternatives, advancements in drug delivery technologies, expanding healthcare access in emerging economies, and the integration of digital health solutions with pharmacological interventions for comprehensive pain management.

North America currently dominates the pain management drugs market, accounting for a share of 45%. The region benefits from advanced healthcare infrastructure, high chronic pain prevalence, strong pharmaceutical innovation, and favorable reimbursement policies supporting market expansion.

Some of the major players in the pain management drugs market include Abbott Laboratories Inc., AbbVie Inc., Bausch + Lomb., Bayer AG, Eli Lilly & Company, GSK plc, Pfizer Inc., Purdue Pharma L.P., Sanofi S.A, Viatris Inc, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)