Pallet Market Size, Share, Trends and Forecast by Type , Application , Structural Design, and Region 2026-2034

Global Pallet Market Size, Share, Trends & Forecast (2026-2034)

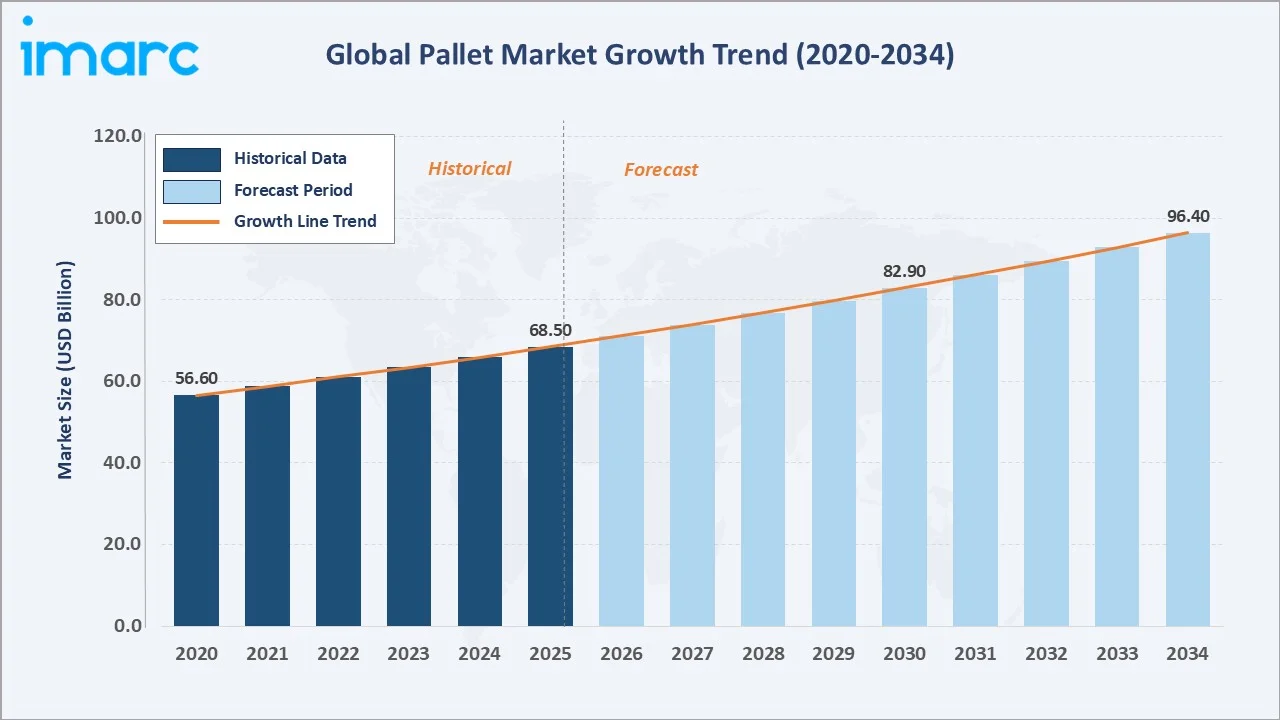

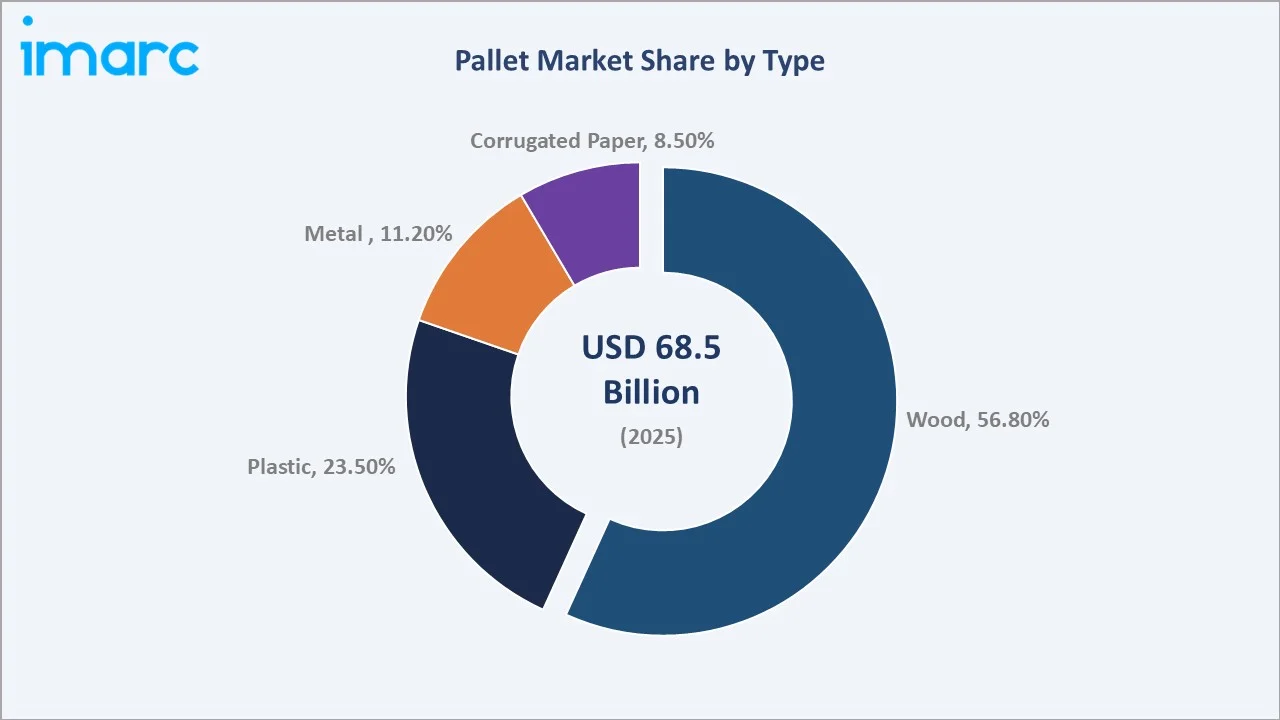

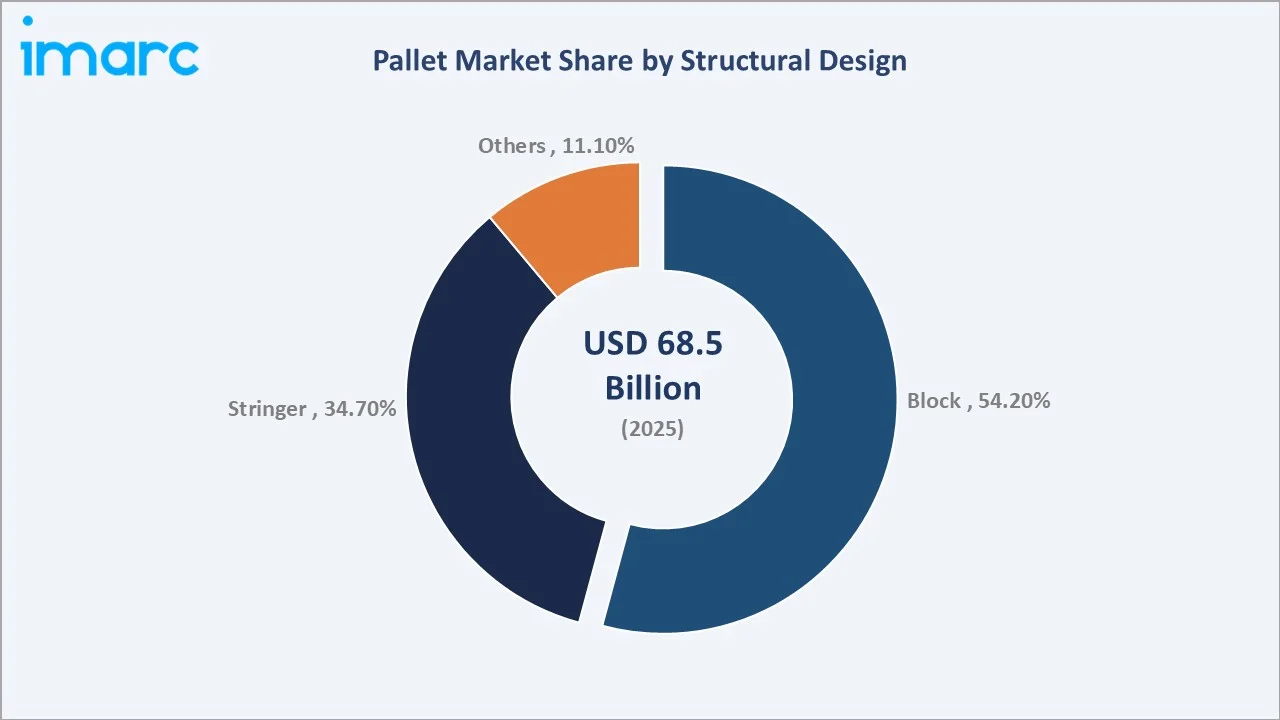

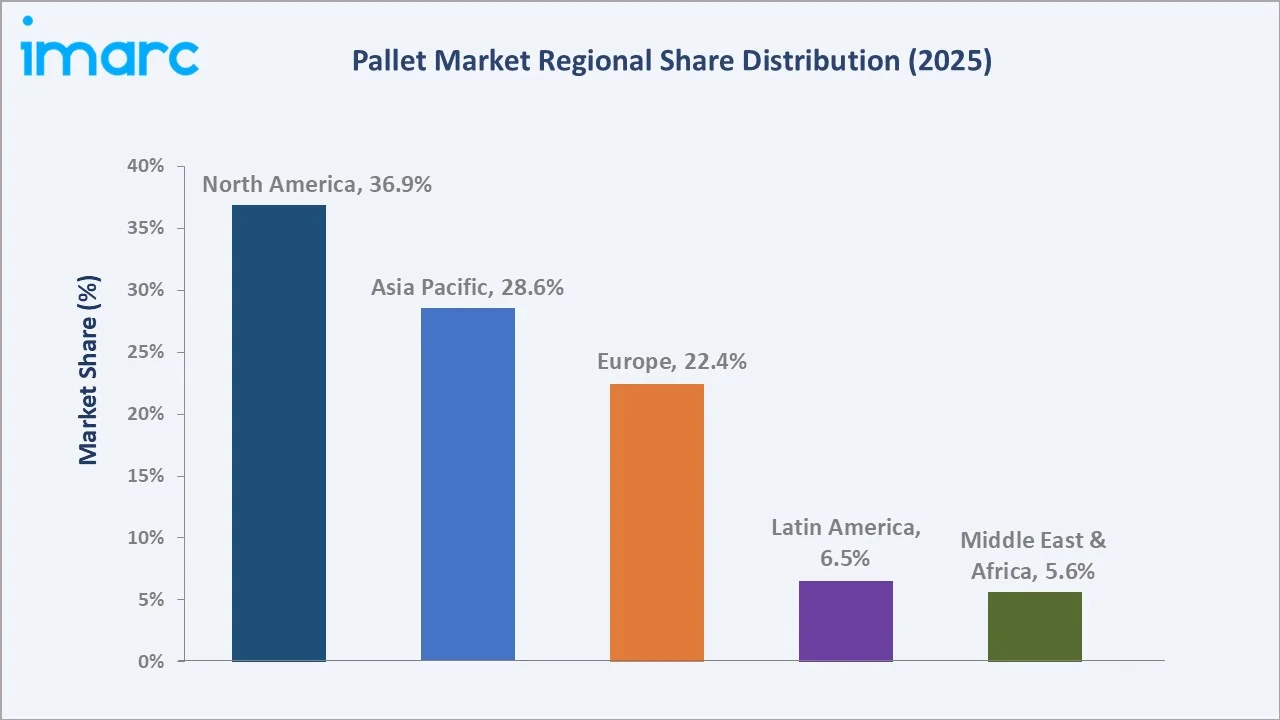

The global pallet market reached USD 68.5 Billion in 2025 and is projected to reach USD 98.4 Billion by 2034, exhibiting a CAGR of 3.9% during 2026-2034. North America leads with a 36.9% share in 2025, driven by mature pooling networks and strong food, beverage, and retail distribution demand.

Market Snapshot

|

Metric |

Value |

|

Market Size 2025 |

USD 68.5 Billion |

|

Forecast Market Size 2034 |

USD 98.4 Billion |

|

CAGR (2026-2034) |

3.9% |

|

Largest Region |

North America (36.9%, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Type |

Wood (56.8%, 2025) |

|

Leading Structural Design |

Block (54.2%, 2025) |

Rising global e-commerce activity, expanding warehouse automation, and growing international trade volumes are driving sustained pallet demand. Increasing pallet pooling adoption and ISPM-15 phytosanitary compliance requirements across international logistics are reinforcing demand for standardized pallet platforms. The pallet market growth trajectory remains positive through 2034.

The United States has emerged as a major region in the pallet market owing to many factors. Strong industrial production, high-volume food and beverage distribution, and advanced e-commerce fulfillment networks sustain consistent pallet demand. The USDA's Climate-Smart Commodities Program is encouraging sustainable pallet adoption across domestic agricultural supply chains, further supporting demand.

To get more information on this market, Request Sample

The pallet market outlook of 3.9% CAGR through 2034 reflects broad-based industrial demand resilience. Pallet pooling and circular-economy reuse models are displacing one-way pallet use, lowering cost-per-trip and material waste. RFID-tagged smart pallets are enhancing logistics visibility, reinforcing long-term market expansion across all geographies.

Executive Summary

The global pallet market stood at USD 68.5 Billion in 2025, supported by expanding cross-border trade and accelerating warehouse automation. North America commanded 36.9% in 2025, anchored by CHEP's extensive pooled pallet infrastructure and high-frequency food, beverage, and retail distribution requirements across US logistics networks.

Wood pallets hold 56.8% of the type segment in 2025, reflecting cost-effectiveness and broad supply chain compatibility. Block pallets lead structural design at 54.2%, driven by four-way forklift access and robotic compatibility, delivering 15–20% faster handling efficiency versus stringer formats in automated distribution center environments.

Key pallet market trends include rising smart RFID pallet adoption, growing circular-economy reuse solutions, and expanding warehouse automation investment. Asia Pacific is the fastest-growing region, propelled by rapid manufacturing growth, large-scale logistics infrastructure development, and e-commerce acceleration across China, India, and Southeast Asia.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Wood – 56.8% 2025 |

|

Largest Structural Design |

Block – 54.2% 2025 |

|

Leading Region |

North America – 36.9% 2025 |

|

Fastest Growing Region |

Asia Pacific |

|

Key Opportunity |

Smart RFID Pallet Integration & Cold-Chain Expansion |

|

Key Players |

CHEP (Brambles), ORBIS Corporation, UFP Industries, Cabka Group, Schoeller Allibert |

Key Analytical Observations Supporting The Data Points Above:

- Wood's 56.8% share 2025 reflects a significant cost advantage, widespread material availability, and strong alignment with sustainability through recyclability. Over 95% of wood pallets are recovered and reused in the US market, reinforcing circular economy credentials.

- Block pallets' 54.2% share is driven by four-way entry capability and seamless integration with automated storage and retrieval systems, delivering measurable handling efficiency improvements in modern distribution environments.

- North America's 36.9% dominance is anchored by CHEP's expansive pooled pallet network, robust demand from food and beverage distribution, and mature e-commerce fulfillment infrastructure requiring standardized, certified pallet platforms.

Global Pallet Market Overview

Pallets are horizontal load-bearing platforms used to store, handle, and transport goods via forklifts and front loaders. Manufactured from wood, plastic, metal, and corrugated paper, pallets are widely deployed across food and beverage, pharmaceutical, manufacturing, and retail sectors. ISPM-15 international phytosanitary standards govern cross-border pallet movement worldwide.

Market Dynamics

To evaluate market opportunities, Request Sample

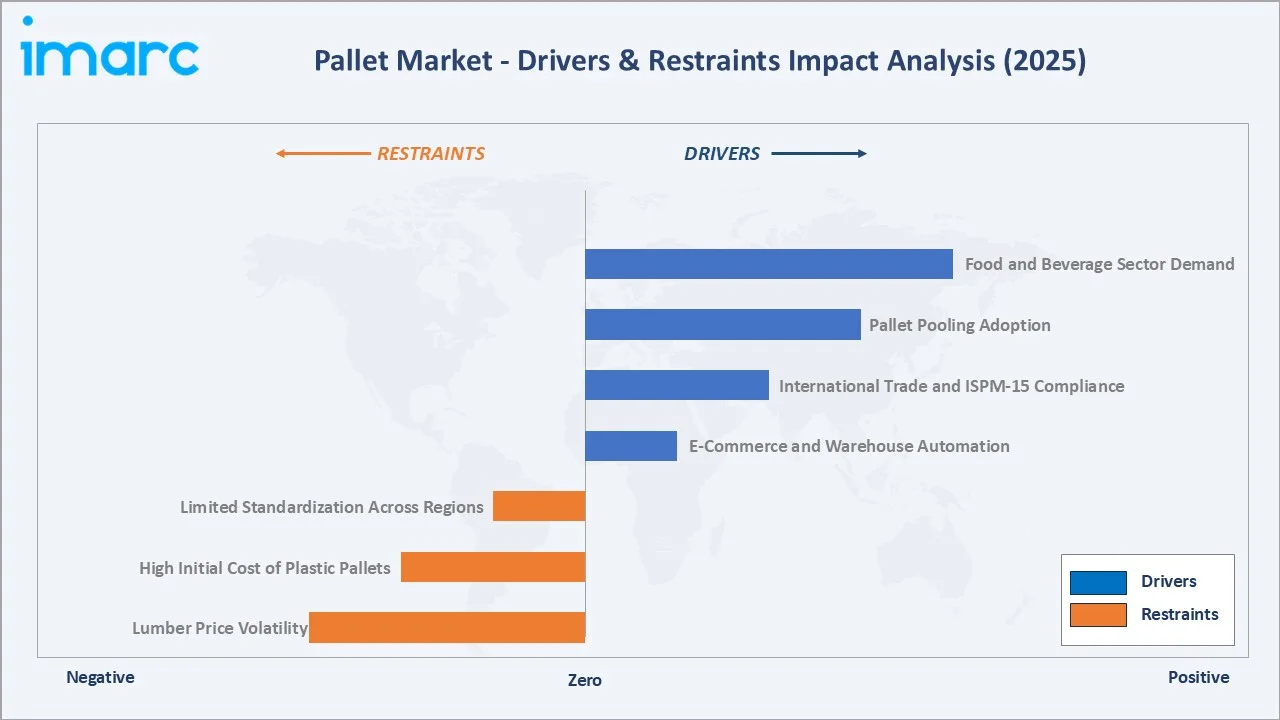

Market Drivers

- E-Commerce and Warehouse Automation: Rapid e-commerce expansion and automated fulfillment center growth are driving demand for automation-compatible, standardized pallet formats. Block pallets and RFID-tagged reusable platforms are increasingly specified in automated distribution centers, supporting consistent pallet market growth globally.

- International Trade and ISPM-15 Compliance: Expanding global trade volumes and ISPM-15 compliance requirements are reinforcing demand for certified, heat-treated pallet platforms. Cross-border logistics standardization initiatives in Asia Pacific and Europe are creating new demand for compliant pallet solutions across international shipping routes.

- Pallet Pooling Adoption: Circular economy practices and pallet pooling models are replacing one-way pallet use globally, reducing costs and waste. CHEP's share-and-reuse pools across India’s per capita CO2 emissions are about 1.9 tonnes per annum, which is less than 40% of the global average and about one-fourth of that of China.

- Food and Beverage Sector Demand: The food and beverage sector's stringent hygiene, safety, and load-bearing standards drive sustained demand for high-quality wood and plastic pallets. Consistent high-frequency shipments across complex cold-chain logistics networks require durable, compliant pallet platforms globally. The growing consumption of food is expected to reach US$ 1.2 trillion by CY26 in India, owing to urbanization and changing consumption patterns.

Market Restraints

- Lumber Price Volatility: Fluctuating raw timber prices driven by supply chain disruptions, seasonal demand, and tariff pressures create cost uncertainty for wood pallet manufacturers, compressing margins for downstream supply chain operators.

- High Initial Cost of Plastic Pallets: Higher upfront acquisition costs for plastic pallets compared to wood alternatives limit adoption, particularly among small and medium logistics operators in cost-sensitive emerging markets.

- Limited Standardization Across Regions: Variations in pallet sizes, specifications, and standards across regions create inefficiencies in global logistics operations, increasing handling complexity and limiting interoperability in international supply chains.

Market Opportunities

- Smart RFID and IoT Pallet Integration: Growing demand for real-time supply chain visibility creates significant opportunities for IoT and RFID-enabled smart pallets. Pharmaceutical, food, and retail sectors are investing in tracked pallet networks that deliver loss reduction and inventory accuracy.

- Pharmaceutical and Cold-Chain Growth: Accelerating pharmaceutical production and cold-chain logistics expansion is creating premium demand for plastic and composite pallets meeting stringent hygiene, temperature stability, and antimicrobial surface requirements. The pharmaceutical cold chain was also resilient towards the pandemic with double-digit value growth rates at 29% and 20% for 2021 and 2022 respectively.

- E-commerce and Warehousing Expansion: Rapid growth in global e-commerce and automated warehousing is increasing demand for durable, standardized pallets optimized for high-throughput logistics environments, particularly in fulfillment centers and last-mile distribution networks.

Market Challenges

- Reverse Logistics Complexity: Managing pallet return flows in asymmetric trade routes, particularly in e-commerce and one-way export shipments, creates operational challenges for pooling networks and reduces asset utilization efficiency.

- Regulatory Compliance: Evolving pallet material and treatment standards across EU, US, and Asia Pacific require continuous compliance investment. ISPM-15 heat treatment certification and evolving sustainability regulations create additional administrative burdens for manufacturers.

- Sustainability and Recycling Constraints: Increasing pressure to adopt sustainable and recyclable pallet solutions is creating challenges around material recovery, lifecycle management, and recycling infrastructure, particularly for plastic and composite pallets where end-of-life processing remains complex.

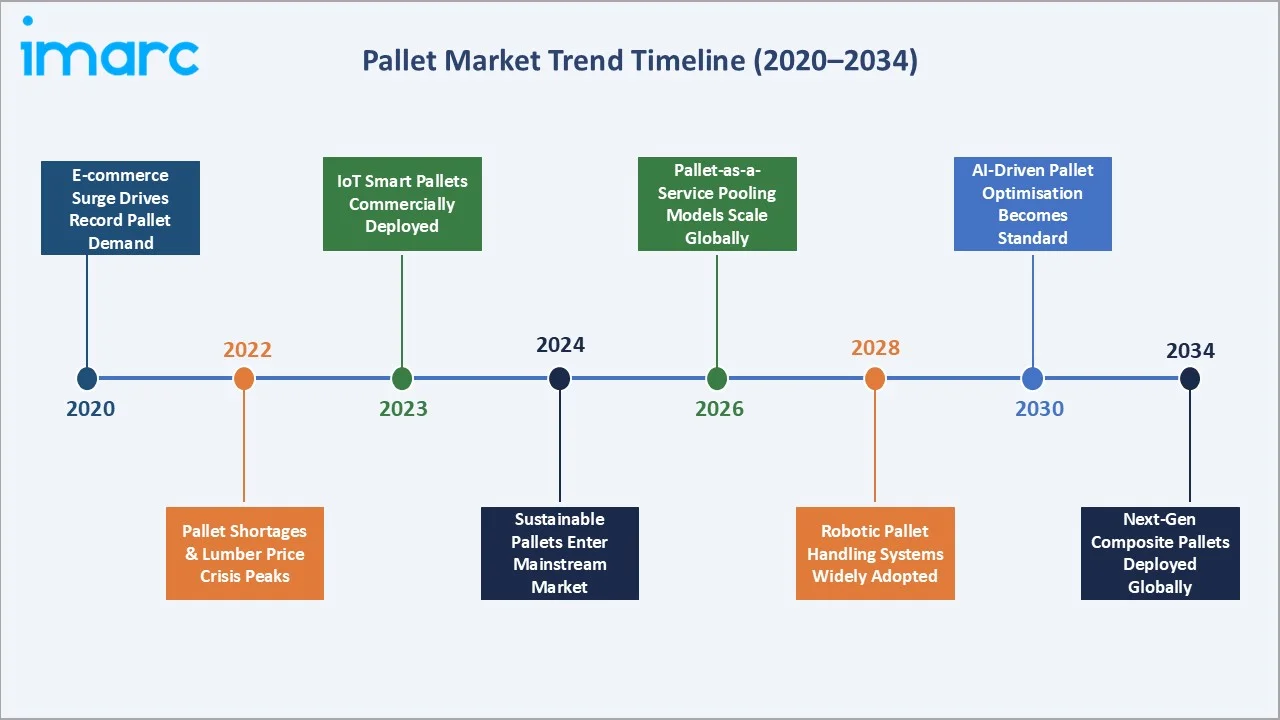

Emerging Market Trends

The global pallet market is being reshaped by three converging trends that are redefining product innovation, distribution models, and competitive dynamics across all geographies through 2034.

1. Rising Adoption of Automation-Compatible Pallet Designs

Growing warehouse automation and robotic fulfillment systems are accelerating demand for block pallets with standardized dimensions and four-way access. Companies are prioritizing automation-friendly designs to avoid costly recalibration of handling systems. The pallet market outlook reflects continued investment in standardized, RFID-compatible platforms optimized for automated distribution environments globally.

2. Sustainability and Circular Economy Practices

Environmental mandates and corporate ESG targets are accelerating adoption of reusable, recyclable, and sustainably sourced pallet solutions. Pallet pooling models and recycled-material composite pallets are gaining traction to reduce supply chain carbon footprint. In January 2025, VLS Environmental Solutions launched a pallet recycling program transforming discarded pallets into clean renewable energy resources.

3. Smart Pallet and IoT Tracking Integration

Integration of RFID tags and IoT sensors into pallet platforms is reshaping supply chain visibility globally. Pharmaceutical, food, and retail sectors are adopting smart pallets for real-time inventory tracking and loss prevention. The pallet market trends indicate growing investment in sensor-embedded networks across North America and Europe, improving asset utilization and recovery rates.

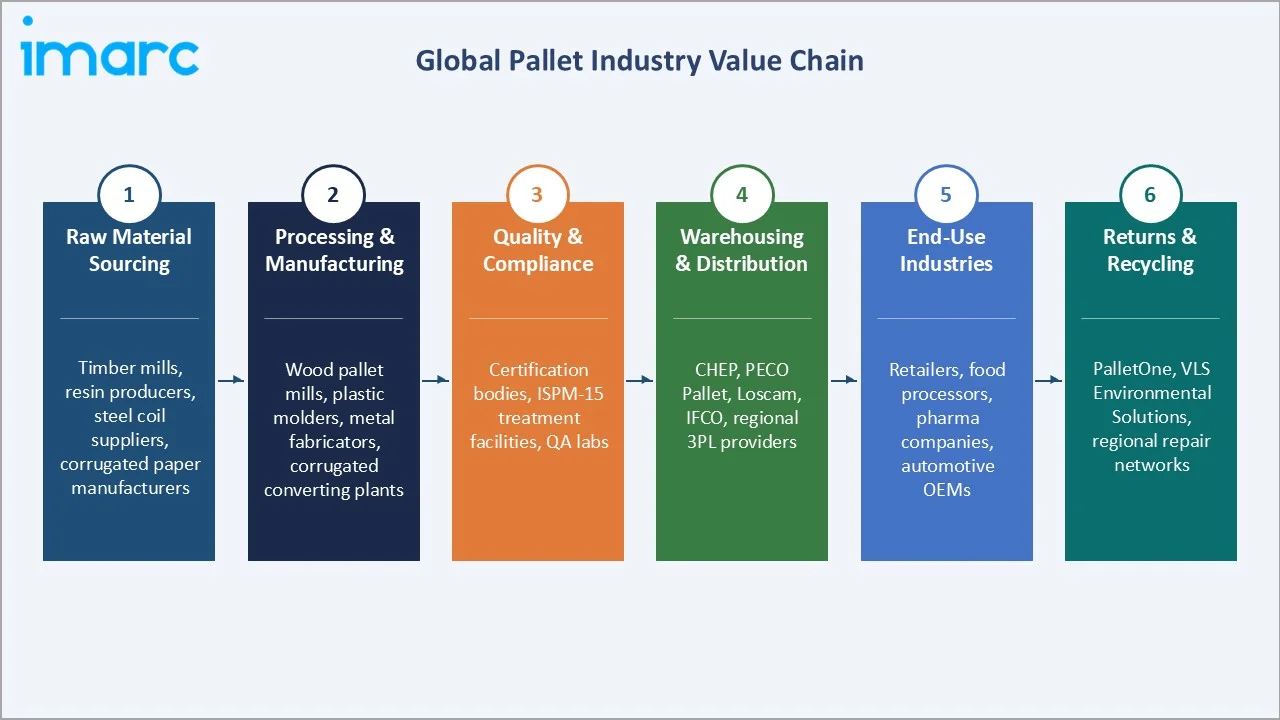

Industry Value Chain Analysis

The pallet industry value chain encompasses seven interconnected stages from raw material sourcing through to end-use industry deployment and recycling. Each stage requires specialized capabilities and quality management to ensure load-bearing performance, regulatory compliance, and supply chain efficiency.

|

Stage |

Key Activities |

Representative Players |

|

Raw Material Sourcing |

Timber procurement, plastic resin sourcing, metal coiling, corrugated fiber supply |

Timber mills, resin producers, steel coil suppliers, corrugated paper manufacturers |

|

Processing & Manufacturing |

Pallet fabrication, heat treatment (ISPM-15), injection molding, welding |

Wood pallet mills, plastic molders, metal fabricators, corrugated converting plants |

|

Quality & Compliance |

Dimensional inspection, load testing, phytosanitary certification, RFID tagging |

Certification bodies, ISPM-15 treatment facilities, QA labs |

|

Warehousing & Distribution |

Pallet pooling, inventory management, cross-docking, 3PL logistics |

CHEP, PECO Pallet, Loscam, IFCO, regional 3PL providers |

|

End-Use Industries |

Food & beverage handling, pharma cold-chain, retail distribution, manufacturing dispatch |

Retailers, food processors, pharma companies, automotive OEMs |

|

Returns & Recycling |

Pallet repair, reuse programs, recycled material conversion, AEF production |

PalletOne, VLS Environmental Solutions, regional repair networks |

The manufacturing and pooling stages represent the primary value creation points, where quality certification, dimensional standardization, and asset management services are delivered. Leading pooling operators including CHEP invest heavily in digital tracking platforms and sustainable sourcing to command service premiums and retain enterprise accounts across multiple sectors and geographies.

Technology Landscape in the Pallet Industry

RFID and IoT-Enabled Smart Pallets

RFID tags and IoT sensors embedded in pallets enable real-time location tracking, condition monitoring, and inventory management across complex supply chains. Brambles' CHEP serialization program has deployed advanced tracking technology across millions of pallets globally, providing customers with unprecedented visibility. Smart pallet adoption is fastest in pharmaceutical cold-chain and food distribution sectors.

Automated Pallet Handling and Robotics

Robotic palletizing and depalletizing systems are transforming warehouse operations globally. At ProMat 2025, Photoneo and Jacobi Robotics demonstrated AI-integrated 3D vision palletizing for mixed pallet types. ORBIS Corporation's automation-ready pallet designs and system tote platforms are directly enabling warehouse automation implementation across food, beverage, and retail distribution networks.

Sustainable Material Innovation

Bio-composite pallets derived from rice husk, corn stover, and agricultural waste are gaining traction as sustainable alternatives. In July 2025, AirX Carbon launched an enhanced NetZero Pallet crafted from coconut shells and coffee husks, achieving carbon-negative status. These innovations meet both regulatory sustainability requirements and corporate ESG objectives while maintaining load-bearing performance standards.

Digital Supply Chain Integration

Cloud-based pallet asset management platforms are enabling pooling operators to optimize fleet utilization and reduce deadhead miles. AI-assisted routing algorithms improve pallet flow efficiency, reducing carbon intensity. Doig Corporation's Pallet EZ solution launched in May 2025 introduced off-the-shelf automated palletizing via OnRobot's D:PLOY platform, reducing setup time and coding requirements significantly.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Wood |

56.8% |

2025 |

|

Application |

Food & Beverages |

🔒 |

2025 |

|

Structural Design |

Block |

54.2% |

2025 |

|

Region |

North America |

36.9% |

2025 |

By Type

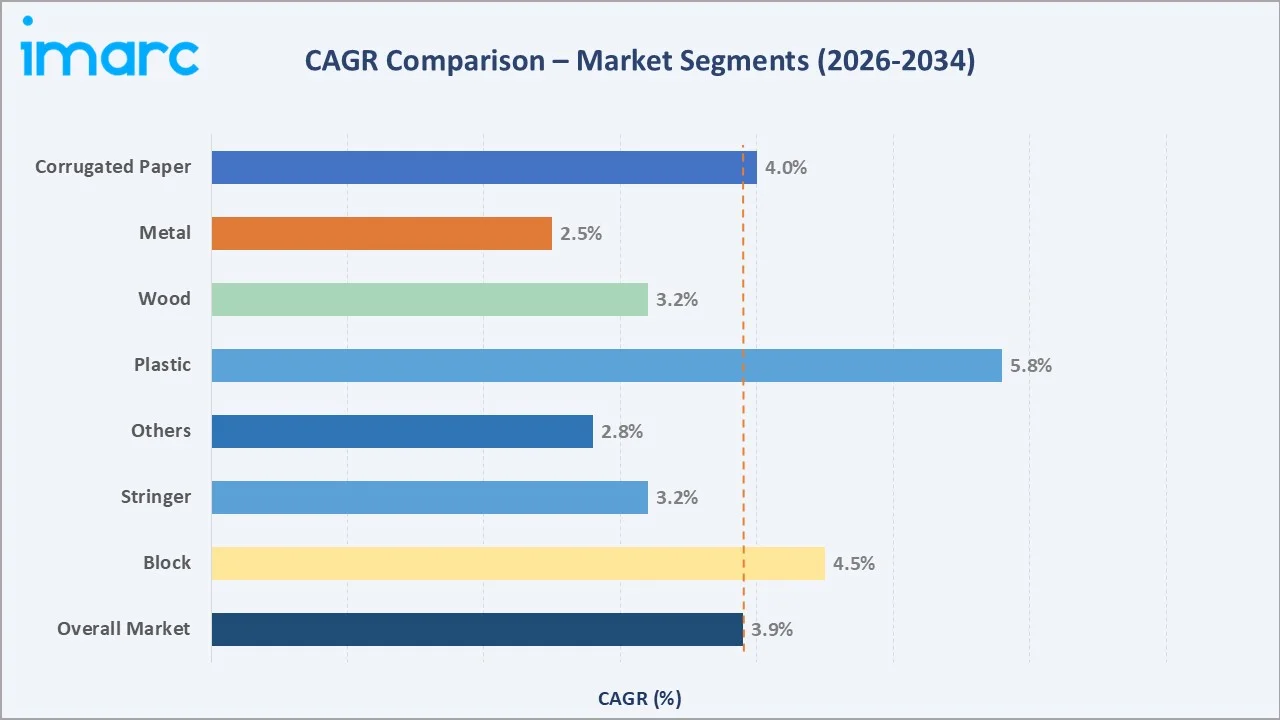

The pallet market is segmented by four primary material types, each with distinct cost profiles, application suitability, and growth trajectories. Wood pallets dominate at 56.8% in 2025, driven by cost-effectiveness and supply chain compatibility. Plastic pallets are the fastest-growing type, expanding at 5.8% CAGR through 2034.

Wood's 56.8% dominance reflects affordability, widespread repair infrastructure, and compliance with circular economy goals. Plastic pallets at 23.5% are gaining share in hygienic, wash-down intensive environments. Metal pallets at 11.2% serve heavy-duty industrial applications, while corrugated paper at 8.5% addresses lightweight export requirements.

To access detailed market analysis, Request Sample

By Structural Design

Structural design segmentation reflects compatibility with handling systems, forklift access requirements, and automation integration needs. Block pallets dominate at 54.2% in 2025, while stringer pallets at 34.7% serve traditional logistics cost-efficiently. Other designs including solid-deck and double-face formats address specialty segment requirements.

Block pallets' 54.2% leadership reflects four-way entry capability and seamless integration with ASRS systems. Stringer pallets at 34.7% remain cost-competitive for traditional two-way forklift logistics. Others at 11.1% include custom formats for specialty applications in produce, electronics, and automotive sectors.

Regional Market Insights

The global pallet market exhibits distinct regional dynamics in terms of pooling maturity, material preferences, regulatory environment, and growth trajectory. North America leads in revenue share and pooling infrastructure, while Asia Pacific represents the highest-growth frontier through 2034 driven by manufacturing expansion and logistics investment.

North America's 36.9% leadership is underpinned by CHEP's expansive network and high-frequency food and beverage demand, while Asia Pacific's 28.6% share is growing rapidly. Europe's 22.4% share reflects strong circular economy regulation driving reusable pallet adoption. Latin America and Middle East and Africa collectively represent emerging growth opportunities.

Competitive Landscape

The global pallet market is moderately consolidated, with leading players competing through pooling network expansion, RFID-enabled smart pallet development, and sustainable material adoption. Key differentiators include automation-compatible pallet design, digital asset tracking, and value-added logistics services. Strategic acquisitions and pooling network expansions are expected to further consolidate the competitive landscape through 2034.

|

Company |

Headquarters |

Market Position |

Primary Strategy |

|

Cabka Group GmbH |

Germany |

Established – Plastic Pallets |

Recycled-material plastic pallets, sustainability leadership, circular economy solutions |

|

CHEP (Brambles Limited) |

Australia |

Global Leader – Pooling |

Share-and-reuse pooling, digital pallet tracking, RFID serialization, ESG focus |

|

Craemer Holding GmbH |

Germany |

Established – Europe |

Premium injection-molded plastic pallets, food-grade hygienic designs |

|

Falkenhahn AG |

Germany |

Regional – Wood/Timber |

Wood pallet manufacturing |

|

Loscam International Holdings Co., Ltd. |

Australia |

Leader – Asia Pacific |

Pallet and crate pooling across APAC, closed-loop logistics, cross-border services |

|

Mondi Plc |

Weybridge, England (UK) |

Established – Paper/Packaging |

Corrugated paper pallets, sustainable fiber-based transport packaging |

|

ORBIS Corporation |

USA |

Leader – Reusable Plastic |

Reusable plastic pallets and containers, supply chain optimization, automation-ready designs |

|

PalletOne Inc. (UFP Industries) |

USA |

Leader – Wood (USA) |

Largest single-source US wood block pallets manufacturer |

|

PECO Pallet Inc. |

USA |

Leader – Pooling (USA) |

North America pallet pooling network, quality-certified platforms, food-grade service |

|

PGS Group |

France |

European Leader |

New EPAL pallets, reconditioned pallets, and offer pallet pooling |

The key players of the report include Cabka Group GmbH, CHEP (Brambles Limited), Craemer Holding GmbH, Falkenhahn AG, Loscam International Holdings Co., Ltd., Mondi Plc, ORBIS Corporation, PalletOne Inc (UFP Industries), PECO Pallet Inc., PGS Group, and others.

Key Company Profiles

CHEP

CHEP is the world's largest pallet and container pooling operator, operating across 60+ countries. Its share-and-reuse model has become both an ESG benchmark and commercial differentiator.

- Product Portfolio: Wood and plastic pooled pallets, reusable plastic crates (RPC), container solutions across CHEP Americas, CHEP EMEA, and CHEP Asia-Pacific segments.

- Recent Developments: In January 2025, Brambles sold its CHEP India unit to LEAP India Private Limited.

- Strategic Focus: Digital pallet tracking, RFID serialization, ESG-driven circular pooling, net new business conversions, and operational efficiency through supply chain automation.

ORBIS Corporation

ORBIS Corporation specializes in reusable plastic packaging, pallets, bulk containers, and custom dunnage, serving automotive, retail, food, and healthcare industries. The company collaborates with customers to develop tailored material handling solutions that enhance supply chain efficiency and promote circular economy practices.

- Product Portfolio: Reusable plastic pallets, bulk containers, system totes, IBCs, and automation-optimized platforms for diverse industrial applications.

- Recent Developments: In April 2025, ORBIS rolled out a new system tote for automation effectiveness and released the NPL640B tray for optimized bakery logistics ahead of EXPO PACK Guadalajara 2025.

- Strategic Focus: Reusable packaging systems, automation-compatible design, sustainability, and circular economy solutions for food, automotive, and retail clients.

PalletOne Inc (UFP Industries Inc.)

UFP Industries is a major US manufacturer of wood products, packaging, and pallets through its UFP Packaging division. Operating through PalletOne and other units, it is a leading supplier to retail, construction, and industrial markets. UFP continues expanding its national presence through strategic acquisitions.

- Product Portfolio: New wood pallets, recycled pallets, custom crates, skids, and pallet repair services across its nationwide manufacturing network.

- Recent Developments: In January 2025, UFP Industries expanded in the southeastern US by acquiring a company specializing in pallet and mulch manufacturing, strengthening its regional production capacity.

- Strategic Focus: National wood pallet manufacturing scale, geographic expansion through acquisitions, automation investment in assembly systems, and product diversification.

Cabka Group GmbH

Cabka Group is a leading manufacturer of plastic products for logistics and packaging, providing innovative and sustainable solutions across automotive, retail, and food industries. The company uses high-quality recycled materials and emphasizes circular economy through product reuse, recycling, and refurbishment.

- Product Portfolio: Plastic pallets, containers, transport packaging manufactured from recycled materials, offering sustainability-certified logistics solutions.

- Recent Developments: Cabka signed a supply contract with Target (approximately 2,000 US locations), expanding its strategic presence in large container and custom solutions markets in North America.

- Strategic Focus: Recycled-material plastic pallet manufacturing, sustainability leadership, US market expansion, and circular economy product lifecycle management.

Market Concentration Analysis

The global pallet market is moderately fragmented at the manufacturer level, with the largest single operator, CHEP (Brambles), holding an estimated 15–18% of global pooled pallet revenues. Regional manufacturers and local wood pallet producers account for most of the volume, particularly in emerging economies and domestic transport lanes.

In mature markets including North America and Europe, market concentration at the branded pooling tier is higher, with pooling operators representing 35–45% of industrial pallet revenue. CHEP, PECO Pallet, and Loscam dominate institutional pooling, while UFP Industries, PalletOne, and Cabka Group lead manufacturing. Consolidation is accelerating at both the pooling operator and manufacturer tiers.

In Asia Pacific, independent manufacturers and regional pooling operators dominate, creating significant white space for global pooling network expansion. Consolidation is expected to accelerate through 2034 as institutional logistics operators demand standardized, tracked, and pooled pallet solutions aligned with ISPM-15 and corporate ESG requirements across all major markets.

Investment & Growth Opportunities

Fastest Growing Segments

Smart RFID and IoT-enabled pallets, sustainable composite and bio-material pallet platforms, and pharmaceutical-grade cold-chain pallet solutions represent the highest-growth investment vectors through 2034. These segments collectively address a rapidly expanding total addressable market driven by regulatory requirements, automation demand, and ESG mandates.

Emerging Market Expansion

Asia Pacific's 28.6% market share and status as the fastest-growing region represents the highest regional investment opportunity. India's PM Gati Shakti logistics infrastructure program, combined with rapid e-commerce growth, creates large-scale pallet platform demand. GCC markets including UAE and Saudi Arabia are experiencing rapid warehousing and free trade zone expansion backed by Vision 2030 programs.

Technology and Innovation Investment Trends

RFID and IoT sensor integration into pallet platforms is experiencing strong B2B demand from major logistics operators and food and pharmaceutical companies seeking end-to-end supply chain visibility and loss prevention capabilities across complex distribution networks.

Future Market Outlook (2026-2034)

The global pallet market is poised for sustained growth through 2034, anchored by industrial production expansion, e-commerce logistics scaling, and continued transition from one-way to pooled and reusable pallet systems. The pallet market forecast of USD 98.4 Billion by 2034 reflects broad-based demand resilience across all major end-use sectors and geographies.

Sustainability and automation will be the primary competitive battlegrounds. Pallet operators that successfully navigate the transition from traditional wood supply to smart, tracked, RFID-enabled, and sustainably sourced pallet platforms will capture the widest enterprise customer base. The emergence of carbon-negative bio-composite pallets represents the highest premium opportunity of the next decade.

By 2034, pallet pooling models are expected to represent a significantly larger share of total pallet usage globally as circular economy principles become embedded in supply chain procurement mandates. Smart pallet platforms with embedded IoT sensors will be standard specification in pharmaceutical, food-grade, and premium retail distribution environments across all major global markets.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys conducted with over 150 industry participants in 2024–2025, comprising pallet manufacturers, pooling service operators, logistics and supply chain managers, raw material suppliers, end-use industry procurement managers, and institutional buyers across North America, Europe, Asia Pacific, and the Middle East.

Secondary Research

Secondary research encompassed a comprehensive review of company press releases, trade publications (Pallet Enterprise, Supply Chain Management Review, Packaging Digest), industry databases, and publicly available market data including government trade statistics, phytosanitary compliance records, and logistics industry association reports. Over 250 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of bottom-up manufacturing capacity and pallet unit volume modeling, combined with top-down end-use industry demand analysis incorporating logistics output data, e-commerce penetration rates, warehouse automation investment, and international trade volume analytics from 2020–2034.

Pallet Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD, Billion Units |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Wood, Plastic, Metal, Corrugated Paper |

| Applications Covered | Food and Beverages, Chemicals and Pharmaceuticals, Machinery and Metal, Construction, Others |

| Structural Designs Covered | Block, Stringer, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Cabka Group GmbH, CHEP (Brambles Limited), Craemer Holding GmbH, Falkenhahn AG, Loscam International Holdings Co., Ltd., Mondi Plc, ORBIS Corporation, PalletOne Inc. (UFP Industries), PECO Pallet Inc., PGS Group, etc |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the pallet market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global pallet market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the pallet industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Pallet Market Report

The global pallet market was valued at USD 68.5 Billion in 2025, making it one of the largest industrial packaging and logistics support markets globally.

The pallet market is projected to exhibit a CAGR of 3.9% during 2026-2034, reaching a value of USD 98.4 Billion by 2026-2034, driven by e-commerce expansion, warehouse automation, and pallet pooling adoption globally.

Key drivers include rapid e-commerce and warehouse automation growth, expanding international trade volumes and ISPM-15 compliance requirements, growing pallet pooling adoption for circular economy goals, and sustained food, beverage, and pharmaceutical distribution demand requiring durable, standardized pallet platforms.

North America currently dominates the pallet market, accounting for a share of 36.9% in 2025. The region benefits from mature pallet pooling infrastructure, high e-commerce logistics penetration, and strong food and beverage distribution demand sustaining consistent pallet platform requirements.

Asia Pacific is the fastest-growing region, driven by rapid industrialization, growing e-commerce activity, and large-scale logistics infrastructure investment across China, India, and Southeast Asian markets. Programs such as India's PM Gati Shakti and Japan's Smart Logistics 2025 are reshaping regional warehousing models.

Wood pallets represent the largest type segment with a 56.8% share in 2025, valued for their cost-effectiveness, ease of repair, broad supply chain compatibility, and alignment with circular economy goals through recyclability and biodegradability.

Block pallets represent the largest structural design segment at 54.2% in 2025, driven by their four-way forklift entry capability, seamless integration with automated storage and retrieval systems, and 15–20% faster handling efficiency compared to stringer formats in automated distribution environments.

Major players in the pallet market include Cabka Group GmbH, CHEP (Brambles Limited), Craemer Holding GmbH, Falkenhahn AG, Loscam International Holdings Co., Ltd., Mondi Plc, ORBIS Corporation, PalletOne Inc (UFP Industries), PECO Pallet Inc., PGS Group, and others.

High-growth investment opportunities include smart RFID and IoT-enabled pallet platforms, sustainable bio-composite and recycled plastic pallet manufacturing, pharmaceutical cold-chain pallet pooling, emerging market pallet network expansion in Asia Pacific and GCC, and digital supply chain visibility technology integration.

Key challenges include lumber price volatility compressing wood pallet manufacturer margins, high initial acquisition costs for plastic pallets limiting adoption in cost-sensitive markets, reverse logistics complexity in asymmetric trade flows, and evolving ISPM-15 and sustainability regulatory requirements creating continuous compliance investment needs.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)