Particle Board Market Size, Share, Trends and Forecast by Application, Sector, and Region, 2026-2034

Particle Board Market Size and Share:

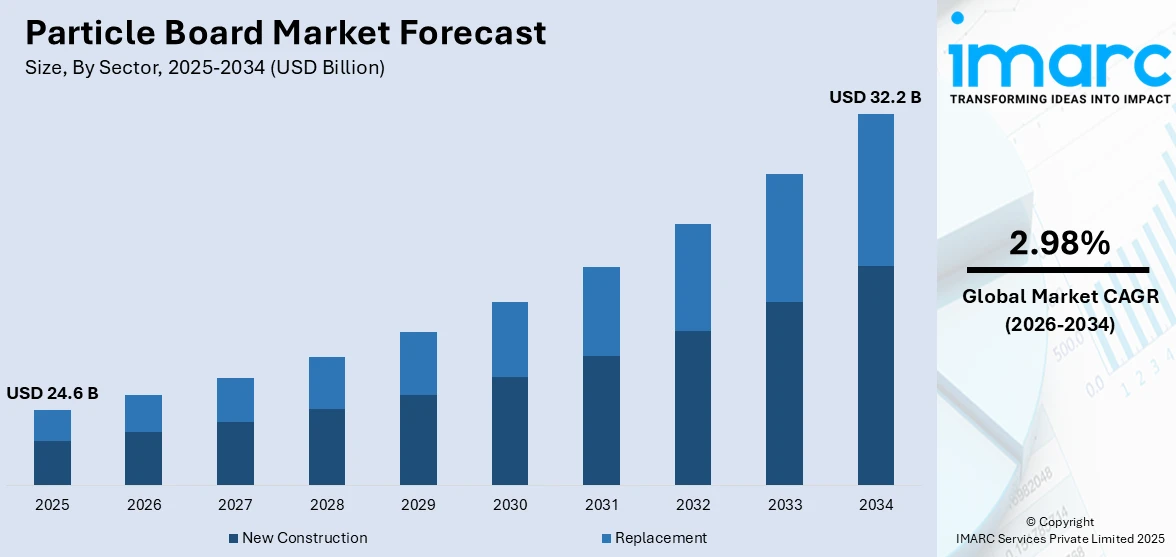

The global particle board market size was valued at USD 24.6 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 32.2 Billion by 2034, exhibiting a CAGR of 2.98% from 2026-2034. Europe currently dominates the market, holding a market share of 30% in 2025. The region benefits from a well-established furniture manufacturing base, strict environmental regulations promoting sustainable building materials, and steady demand driven by ongoing residential renovation activities across major economies, alongside government incentives supporting energy-efficient construction, all contributing to the particle board market share.

The global particle board market is being driven by several interconnected factors. The rapid pace of urbanization across developing and developed nations is fueling the need for cost-effective interior construction and furnishing materials. Particle board, known for its affordability, versatility, and ease of customization, continues to be a preferred material for residential and commercial furniture manufacturing, wall paneling, flooring underlayment, and cabinetry. The rising trend of ready-to-assemble furniture, supported by the expansion of e-commerce platforms and flat-pack retail models, is further augmenting demand. Additionally, the growing emphasis on sustainable building practices is encouraging manufacturers to adopt recycled wood content and low-emission adhesive systems, expanding the appeal of particle board among environmentally conscious consumers and builders. The increasing adoption of engineered wood products as substitutes for solid timber in interior applications, driven by favorable cost-to-performance ratios, supports favorable particle board market outlook.

The United States has emerged as a major region in the particle board market owing to many factors. The country's construction sector, encompassing both residential and commercial segments, underpins consistent demand for engineered wood panels. Particle board is extensively utilized in kitchen cabinetry, shelving, office furniture, and subflooring applications across newly built and renovated properties. The growing preference for affordable and lightweight interior materials among homebuilders and furniture manufacturers sustains consumption volumes. According to the US Census Bureau, an estimated 1,358,700 housing units were started in 2025 in the United States, reflecting continued residential construction activity that supports demand for interior finishing materials. Furthermore, advancements in surface lamination technologies and moisture-resistant coatings are enhancing the performance characteristics of particle board products, enabling their use in a wider range of applications across both residential and commercial environments throughout the country.

To get more information on this market Request Sample

Particle Board Market Trends:

Rising Focus on Low-Emission Products

The increasing regulatory emphasis on reducing formaldehyde emissions from composite wood products is reshaping the particle board market landscape. Governments across North America and Europe are tightening emission standards, prompting manufacturers to invest in ultra-low-emitting resins and bio-based adhesive systems. These advancements are enabling particle board producers to meet stringent indoor air quality requirements while maintaining competitive production costs. Consumer awareness regarding the health implications of volatile organic compounds in household materials is also driving preference toward certified low-emission panels. For instance, in February 2026, the US Environmental Protection Agency proposed updates to the Formaldehyde Emission Standards for Composite Wood Products under the Toxic Substances Control Act, introducing a new quality control test method, ISO 12460-2:2024, for measuring formaldehyde air emissions from wood-based panels. This regulatory momentum is encouraging innovation in adhesive technologies and accelerating the transition toward healthier building materials across the residential and commercial construction sectors globally.

Expanding Circular Economy in Wood Panels

The growing adoption of circular economy principles is emerging as a significant trend in the particle board market, driven by both regulatory requirements and corporate sustainability commitments. Manufacturers are increasingly incorporating recycled wood content, including post-consumer waste from furniture, pallets, and construction debris, into their production processes. This approach reduces reliance on virgin timber, lowers raw material costs, and supports carbon sequestration goals across the value chain. Advanced sorting and processing systems are enabling manufacturers to incorporate recycled raw materials while maintaining panel strength, durability, and overall quality. Many producers are upgrading their facilities with automated and sustainability-focused technologies to enhance resource efficiency and operational performance. This shift toward resource-efficient production methods is expected to strengthen the long-term competitiveness of particle board against alternative materials, bolstering the particle board market forecast.

Surging Ready-to-Assemble Furniture Demand

The proliferating demand for ready-to-assemble and modular furniture is positively influencing the particle board market, driven by urbanization, rising living costs, and the expansion of e-commerce distribution channels. Particle board serves as a primary substrate in flat-pack furniture manufacturing owing to its uniform density, smooth surface finish, and compatibility with various laminating and veneering processes. As consumers in both developed and emerging economies increasingly seek affordable yet functional furnishing solutions, the adoption of particle board in residential and commercial furniture applications continues to expand. Simultaneously, infrastructure development initiatives are creating additional demand for cost-effective construction materials. For example, in March 2025, the European Investment Bank and European Commission launched a pan-European investment platform planning EUR 10 billion to fund affordable, sustainable housing, and energy-efficient construction projects. These demand-side dynamics are reinforcing the role of particle board as a foundational material in the global furniture and construction supply chain, underpinning particle board market trends.

Particle Board Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global particle board market, along with forecast at the global and regional levels from 2026-2034. The market has been categorized based on application and sector.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

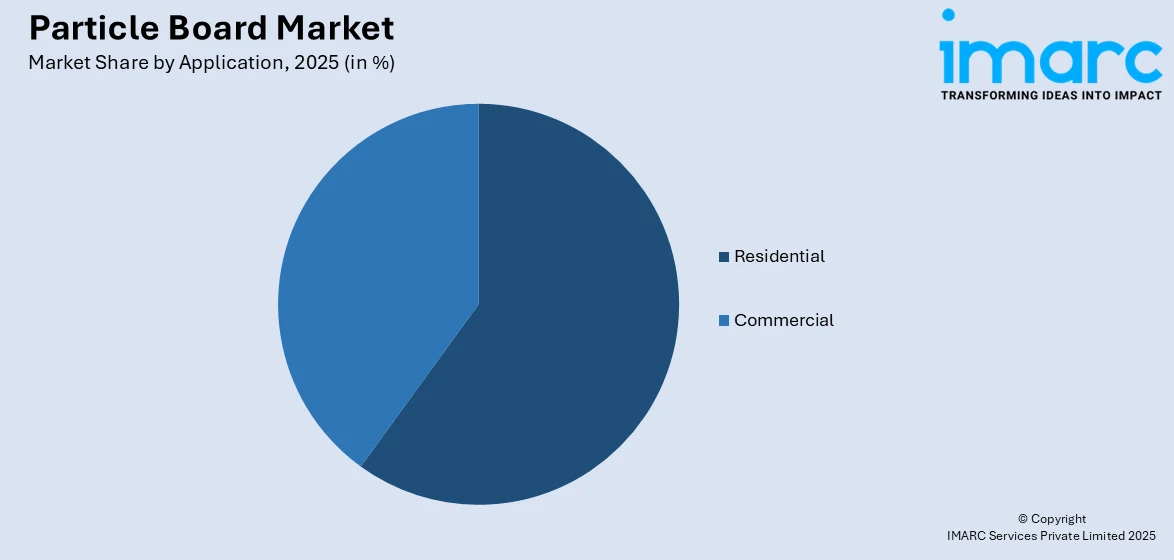

- Residential

- Commercial

Residential holds 72% of the market share. Residential applications represent the dominant consumption segment for particle board, underpinned by its widespread use in home furniture, kitchen cabinetry, wardrobe systems, wall paneling, and flooring underlayment. The material's cost-effectiveness and ease of machining make it an ideal choice for mass-produced residential furniture and interior fittings. Rising urbanization and increasing disposable incomes in developing economies are accelerating housing construction, thereby sustaining demand for affordable interior materials. Additionally, the growing trend of home renovation and remodeling in mature markets is reinforcing consumption patterns. According to Eurostat, in 2024, 68% of the EU population owned their homes while 32% lived in rented housing, underscoring sustained residential demand for furnishing materials. The expanding availability of pre-laminated and decorative particle board variants enables consumers and manufacturers to achieve aesthetic finishes at competitive prices, further strengthening the position of the particle board market growth in the residential segment.

Analysis by Sector:

- New Construction

- Replacement

New construction leads the market with a share of 65%. The new construction sector drives substantial demand for particle board, as the material is extensively utilized in interior applications during the initial build phase of residential, commercial, and industrial structures. Particle board is favored for cupboards, built-in wardrobes, workstations, partition walls, and subflooring in new buildings due to its uniform composition and cost efficiency. The ongoing expansion of urban infrastructure and government-supported housing programs in both developed and emerging markets sustains this demand. According to the Federation of European Construction Industry, civil engineering activity expanded by 5.8% in the EU in 2024, supported by public investment and green infrastructure projects, reflecting broader construction momentum. Builders and contractors increasingly specify particle board for non-structural interior applications where dimensional stability, smooth surface quality, and laminate compatibility are prioritized, reinforcing its essential role in the new construction supply chain.

Regional Analysis:

- Asia Pacific

- North America

- Europe

- Latin America

- Middle East and Africa

Europe, accounting for 30% of the share, enjoys the leading position in the market. The region's dominance is attributed to its well-established furniture manufacturing industry, stringent environmental regulations promoting sustainable building materials, and a strong tradition of using engineered wood products in residential and commercial interiors. Countries such as Germany, France, and Italy serve as major production and consumption hubs for particle board. The growing emphasis on energy-efficient renovation and the revival of the real estate sector across key European economies further sustain demand. For instance, Germany's KfW restarted its climate-friendly loan line in 2024, earmarking EUR 762 million to boost green residential construction, directly supporting demand for sustainable interior materials. Additionally, the increasing adoption of recycled wood content in particle board production aligns with the EU's circular economy objectives, enhancing the region's competitive position in the global market.

Key Regional Takeaways:

North America Particle Board Market Analysis

The North American particle board market is supported by robust construction activity, a well-developed furniture manufacturing sector, and increasing adoption of engineered wood products across residential and commercial applications. The region also has a high density of the distribution network in terms of composite wood panels, with large-scale production plants in the country and an efficient supply chain framework. The US and Canada are the leading consumers of the region due to the current housing developments and renovations of houses. The increasing use of cost-effective and lightweight interior materials by homebuilders continues to drive the use of particle board in the building of cabinets, shelving, and subflooring. Moreover, regulatory trends in the area of formaldehyde emission regulations are also pushing manufacturers to invest in more sophisticated resin systems and cleaner production technologies. According to the National Association of Home Builders, regulatory costs add approximately USD 93,870 per single-family home in the United States, influencing material selection toward affordable options such as particle board. The expansion of ready-to-assemble furniture distribution channels, particularly through e-commerce platforms, is also contributing to sustained particle board consumption across the region.

United States Particle Board Market Analysis

The United States represents the largest national market for particle board within North America, driven by sustained residential and commercial construction activity and a mature furniture manufacturing industry. Its application extends widely in the kitchen cabinetry, office furniture, retail fixtures, and interior paneling in new and remodeled structures. The increased needs of low-cost housing resources and the rise of suburban residential construction in the area contribute to the constant demand for low-cost interior construction materials. Also, the growing popularity of flat pack and pre-assembled furniture, and hence online stores, underpins the need to push particle board as a major substrate material. According to the US Census Bureau, an estimated 1,425,200 housing units were authorized by building permits in 2025, which was 3.6% below the 2024 figure, reflecting ongoing residential development activity. The US market is further supported by domestic production capabilities, with major manufacturers investing in continuous pressing technologies, improved surface lamination processes, and sustainable production methods to meet evolving consumer and regulatory requirements.

Europe Particle Board Market Analysis

The dominance of Europe as the most successful regional market for particle board is supported by a stable furniture production framework with properly established recycled wood and sustainably procured wood supply chains, and strict environmental regulations that spur product development. Centers of production and consumption include Germany, France, Italy, and Spain, and the demand has been backed up by the new construction and large-scale renovation of the residential sector. The EU Renovation Wave initiative, targeting 35 million dwelling upgrades by 2030, is creating significant opportunities for interior finishing materials. For instance, France's MaPrimeRénov scheme funds up to EUR 20,000 per household and targets 500,000 annual retrofits for energy-efficient housing upgrades, supporting demand for sustainable panel products. The regional market also benefits from the growing integration of recycled wood content into particle board manufacturing, aligned with the EU's broader circular economy framework and climate neutrality objectives.

Asia-Pacific Particle Board Market Analysis

The Asia-Pacific region represents a significant and rapidly expanding market for particle board, driven by accelerating urbanization, expanding residential construction, and growing furniture manufacturing capacity across key economies including China and India. Rising disposable incomes and evolving consumer preferences toward modern, affordable furnishing solutions are sustaining demand for engineered wood panels in both domestic and export-oriented production. According to Invest India, the country's building and construction industry was estimated to reach USD 1.4 trillion by 2025, reflecting robust demand for cost-effective construction materials. The region's expanding middle class and increasing adoption of modular furniture designs are further supporting particle board consumption in residential applications.

Latin America Particle Board Market Analysis

The Latin American particle board market is supported by growing urbanization, expanding residential construction activity, and increasing demand for affordable furniture solutions across key economies. Brazil and Mexico lead regional consumption, driven by housing development programs and a rising middle class. In 2024, approximately 80% of the Latin American population resided in urban areas, fueling demand for cost-effective interior materials and furnishing solutions. The region's abundant timber resources and expanding furniture manufacturing base are supporting domestic particle board production and consumption growth.

Middle East and Africa Particle Board Market Analysis

The Middle East and Africa particle board market is expanding, driven by large-scale infrastructure development programs, rapid urbanization, and growing demand for residential and commercial furnishings. Under Saudi Vision 2030, the Kingdom aims to increase homeownership rates from 47% to 60% by 2030, driving significant demand for affordable construction and interior finishing materials across the region. The expanding hospitality and tourism sectors, particularly in the Gulf Cooperation Council countries, are also contributing to rising consumption of particle board in commercial furniture and interior design applications.

Competitive Landscape:

The global particle board market exhibits a moderately consolidated competitive structure, with leading manufacturers focusing on capacity expansion, technological innovation, and sustainability-driven product development to strengthen their market positions. Key strategies include investments in continuous pressing technologies, recycled wood processing facilities, and advanced surface lamination capabilities. Manufacturers are also expanding their geographic footprint through strategic acquisitions and greenfield investments to access growing demand in emerging markets. The competitive landscape is further shaped by increasing emphasis on circular economy principles, with major producers incorporating post-consumer recycled wood into their production processes. Product differentiation through low-emission, moisture-resistant, and fire-retardant particle board variants is enabling companies to address evolving regulatory requirements and consumer preferences. Strategic partnerships with furniture manufacturers and construction firms are facilitating market penetration, while investments in automated production lines are enhancing operational efficiency and cost competitiveness across the industry.

The report provides a comprehensive analysis of the competitive landscape in the particle board market with detailed profiles of all major companies, including:

- Kastamonu Entegre

- Roseburg Forest Products Co.

- Norbord Inc.

- Boise Cascade Company

- Columbia Forest Products, Inc.

Latest News and Developments:

- In December 2025, EGGER Group reported that its new recycled wood processing facility at the Markt Bibart particleboard plant in Germany has gradually started operations since autumn 2025. The facility is part of a EUR 200 million multi-stage investment project focused on sustainability, automation, and the creation of lamination capacities at the location, with full completion planned by autumn 2026.

- In July 2025, Century Plyboards (India) Ltd. commissioned India's largest particle board manufacturing facility at Therovy Kandigai, near Chennai, Tamil Nadu, with an investment of Rs 600 crore. The 30-acre plant features a daily production capacity of 800 cubic meters and is expected to generate over 1,000 direct and indirect jobs while incorporating eco-friendly manufacturing practices.

Particle Board Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD, Million Cubic Metre |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Applications Covered | Residential, Commercial |

| Sectors Covered | New Construction, Replacement |

| Region Covered | Asia Pacific, North America, Europe, Latin America, Middle East and Africa |

| Companies Covered | Kastamonu Entegre, Roseburg Forest Products Co., Norbord Inc., Boise Cascade Company, Columbia Forest Products, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Particle Board market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global Particle Board market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Particle Board industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Particle Board Market Size Report

The particle board market was valued at USD 24.6 Billion in 2025.

The particle board market is projected to exhibit a CAGR of 2.98% during 2026-2034, reaching a value of USD 32.2 Billion by 2034.

The particle board market is driven by rapid urbanization and expanding residential construction activity, growing demand for affordable and ready-to-assemble furniture solutions, increasing adoption of sustainable and recycled wood-based production processes, supportive government housing policies, rising preference for cost-effective engineered wood products in interior applications, and advancements in low-emission adhesive technologies that enhance product appeal.

Europe currently dominates the particle board market, accounting for a share of 30%. The region benefits from a well-established furniture manufacturing base, strict environmental regulations promoting sustainable building materials, and ongoing renovation activities supported by government incentive programs.

Some of the major players in the particle board market include Kastamonu Entegre, Roseburg Forest Products Co., Norbord Inc., Boise Cascade Company, Columbia Forest Products, Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)