Pet Insurance Market Size, Share, Trends and Forecast by Policy, Animal, Provider, and Region 2026-2034

Global Pet Insurance Market Size, Share, Trends & Forecast (2026-2034)

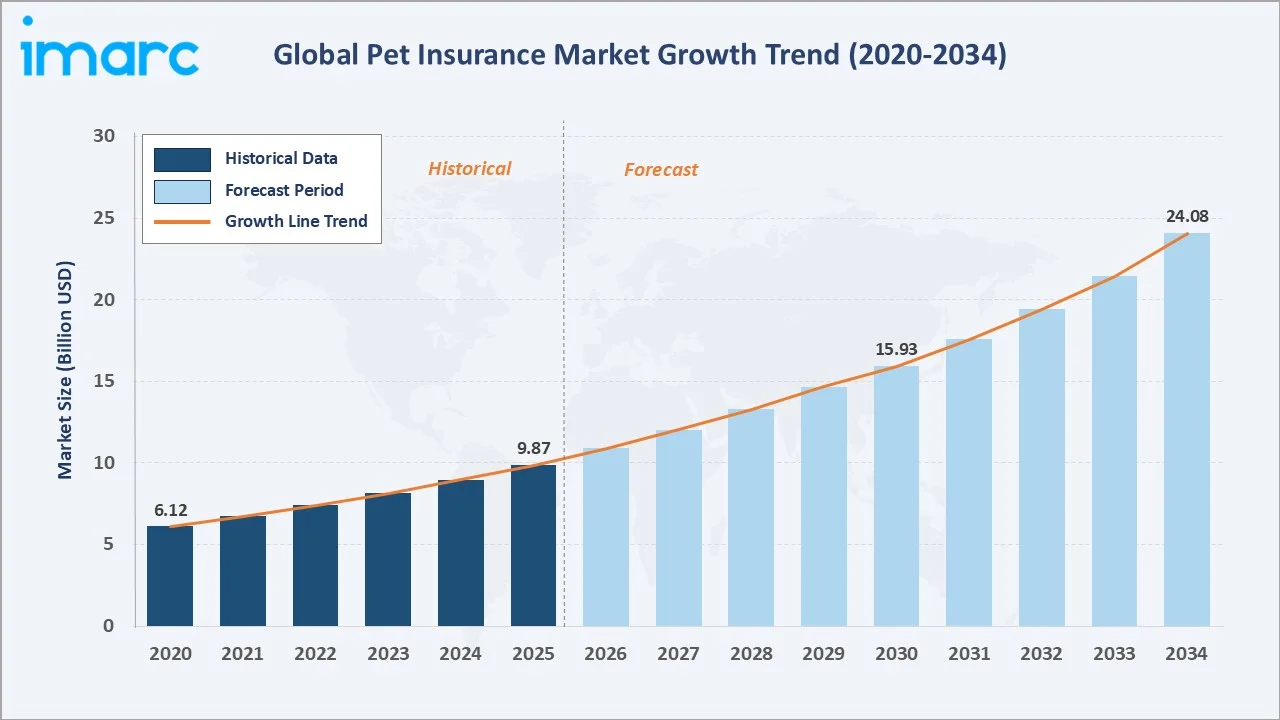

The global pet insurance market size reached USD 9.87 Billion in 2025 and is projected to reach USD 24.08 Billion by 2034, exhibiting a CAGR of 10.05% during the forecast period 2026-2034. Rising veterinary costs, accelerating pet humanization, growing pet ownership rates, and increasing awareness of comprehensive coverage options are driving the pet insurance market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 9.87 Billion |

|

Forecast Market Size (2034) |

USD 24.08 Billion |

|

CAGR (2026-2034) |

10.05% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

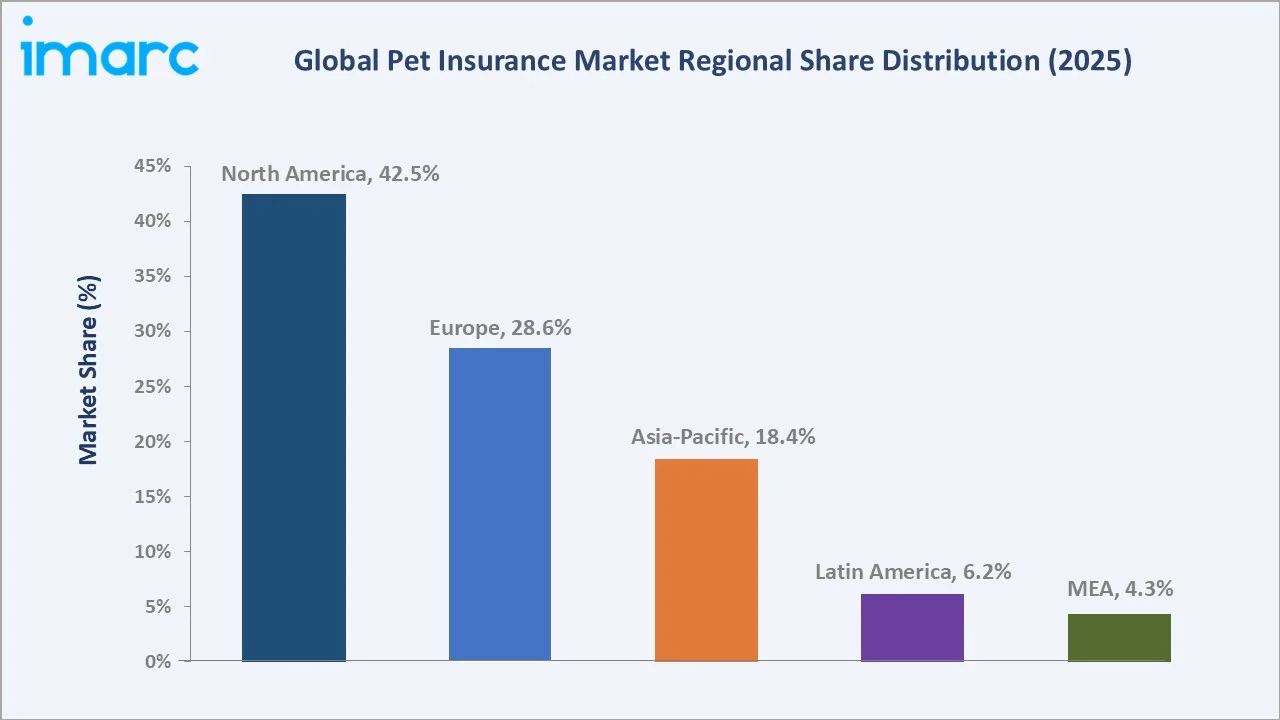

Largest Region |

North America (42.5% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (~13.5% CAGR) |

|

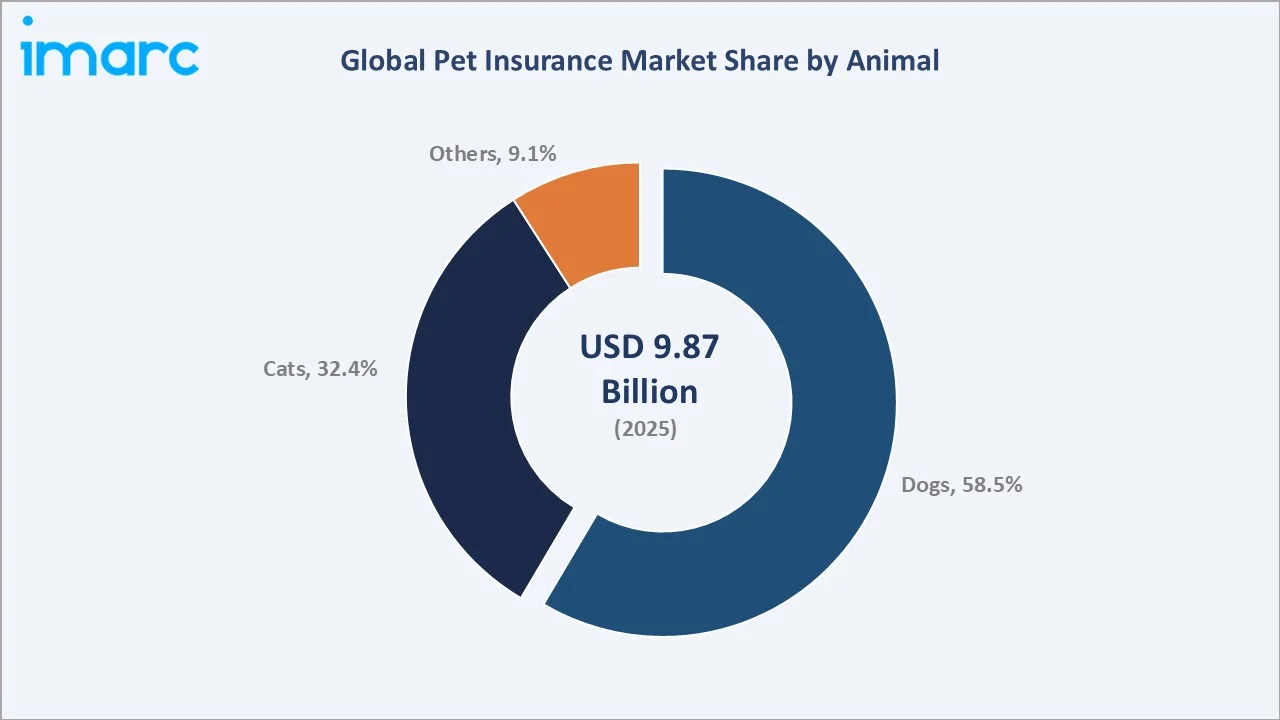

Leading Animal |

Dogs (58.5%, 2025) |

|

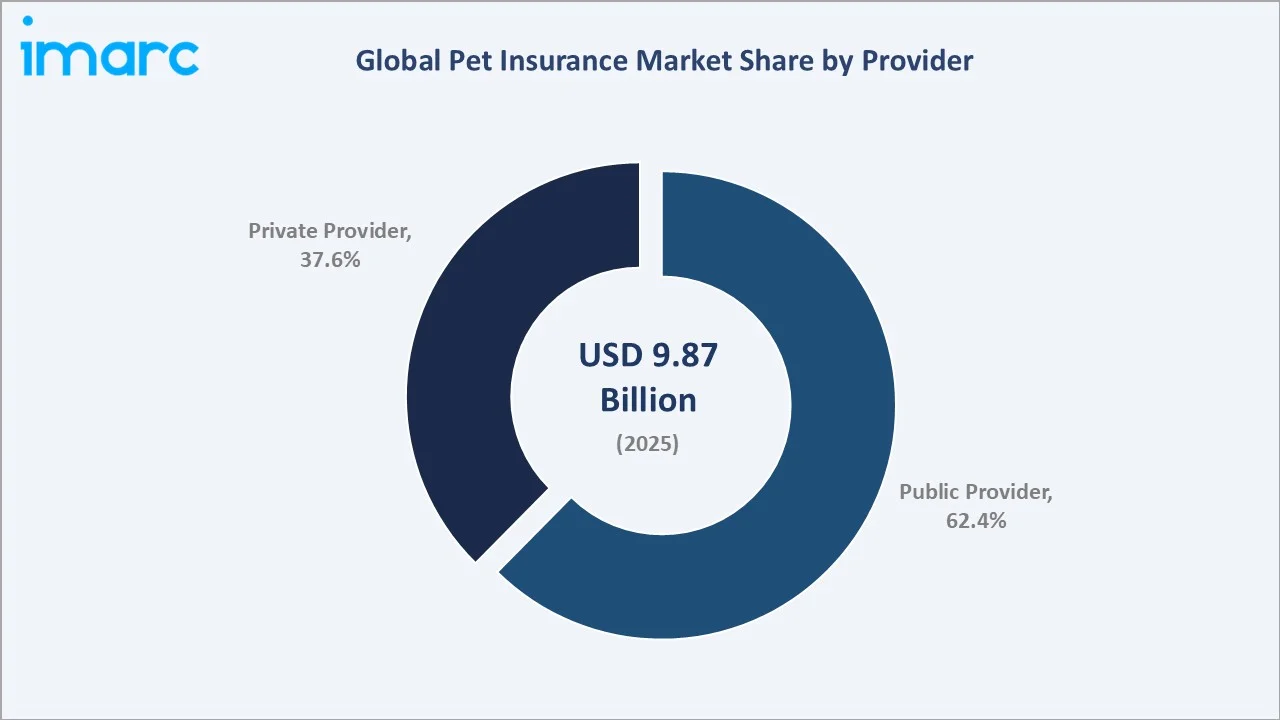

Leading Provider |

Public (62.4%, 2025) |

The following chart illustrates the pet insurance market growth trajectory from 2020 through 2034, contrasting historical expansion against a sustained forecast curve powered by rising veterinary costs, growing pet ownership, and expanding insurance awareness across all key regions.

To get more information on this market, Request Sample

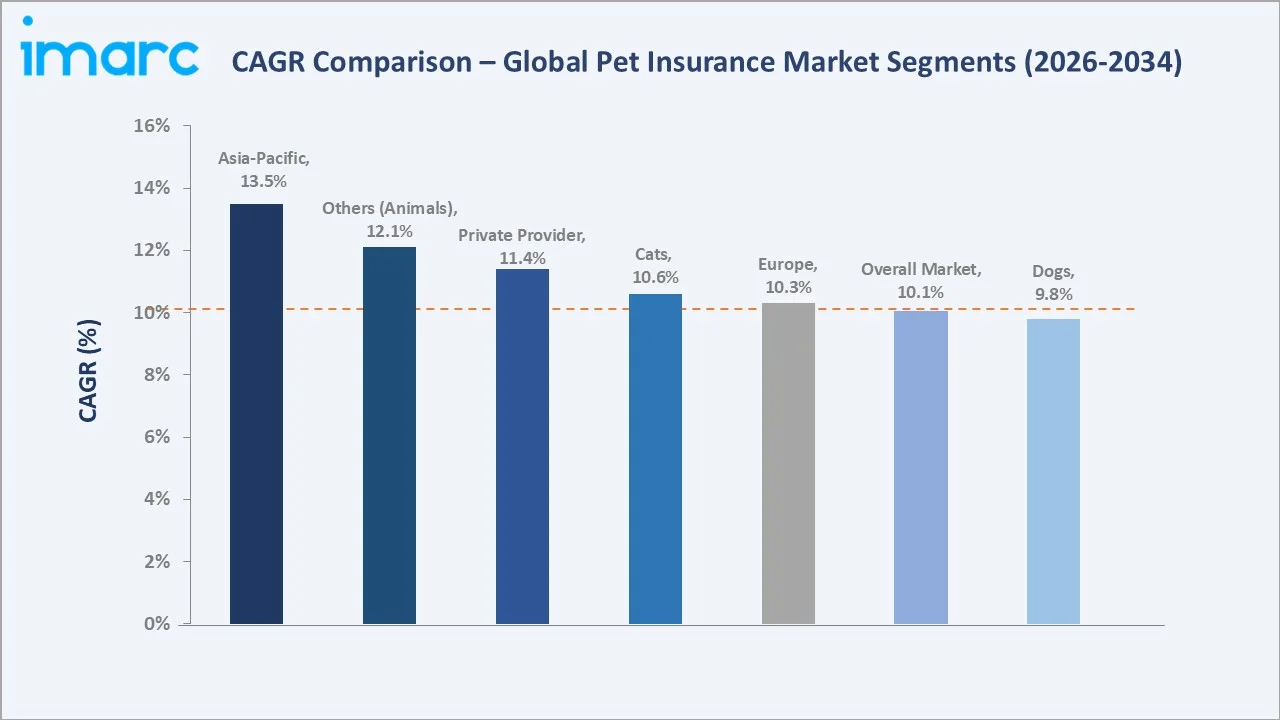

Segment-level CAGR comparisons highlight Asia-Pacific and private provider segments as the fastest-growing sub-categories within the global pet insurance market forecast through 2034.

Executive Summary

The global pet insurance market is undergoing a significant transformation, driven by escalating veterinary care costs, the humanization of pets, and rapid technological innovations in the insurance sector. Valued at USD 9.87 Billion in 2025, the market is forecast to reach USD 24.08 Billion by 2034 at a CAGR of 10.05%.

The public provider segment commands 62.4% share in 2025, supported by government-backed schemes and established insurer networks in Europe and Asia. Dogs represent 58.5% of the insured animal market, reflecting their dominance in global pet ownership. Cats follow with 32.4%, while other animals account for the remaining 9.1% – a segment growing at an estimated 12.1% CAGR through 2034 as exotic pet ownership rises.

North America holds 42.5% of global revenue in 2025, underpinned by high disposable incomes, strong veterinary infrastructure, and employer-sponsored pet benefits uptake. The pet insurance market outlook remains strongly positive as digital distribution, AI-driven underwriting, wellness plan integration, and untapped emerging markets converge to create robust long-term growth opportunities.

Key Market Insights

|

Insight |

Data |

|

Largest Provider |

Public – 62.4% share (2025) |

|

Fastest Growing Provider |

Private – ~11.4% CAGR (2026-2034) |

|

Largest Animal |

Dogs – 58.5% share (2025) |

|

Fastest Growing Animal |

Others (Exotic Pets) – ~12.1% CAGR (2026-2034) |

|

Leading Region |

North America – 42.5% revenue share (2025) |

|

Fastest Growing Region |

Asia-Pacific – ~13.5% CAGR (2026-2034) |

|

Top Companies |

Trupanion, Nationwide Mutual Insurance Company, Allianz, Anicom Holdings Inc., Agria Djurförsäkringar, and Direct Line Insurance Group Limited |

|

Market Opportunity |

Employer-sponsored pet benefits; Large number of pets remain uninsured in the USA |

Key Analytical Observations Supporting The Above Data:

- Public providers' 62.4% dominance in 2025 reflects established reimbursement frameworks and broad policy availability in the UK, Sweden, and Germany, where public-private hybrid models have driven adoption since the early 2000s.

- Private providers' 11.4% CAGR is driven by InsurTech start-ups offering flexible, digitally native policies with customizable deductibles, wellness add-ons, and real-time claims settlement via mobile platforms.

- Dogs' 58.5% share mirrors global dog population dominance. Dogs are the most popular pet in the U.S. (In 2024, 65.1 million U.S. households own a dog).

- Cats' 32.4% share is growing steadily as feline-specific coverage options expand Pet ownership in the U.S. includes approximately 46.5 million cat-owning households in 2024, reflecting a strong base for demand in specialized insurance products such as oncology and dental plans tailored for felines.

- North America's 42.5% dominance is supported by a large and well-established veterinary services industry in the United States, which directly elevates demand for financial protection against medical expense.

- Asia-Pacific's 13.5% CAGR reflects early-stage but rapidly accelerating market development in Japan and China, where urban pet ownership has increased significantly since 2020.

Global Pet Insurance Market Overview

Pet insurance is a specialized financial product that covers veterinary expenses for companion animals, including dogs, cats, and a growing range of exotic species. Policies typically include accident and illness coverage, chronic condition management, and optional wellness riders for preventive care. The global market encompasses public and private providers across direct, digital, employer-sponsored, and broker distribution channels.

The industry operates at the intersection of rising healthcare expenditure, the humanization of pets, and digital transformation of the insurance sector. Macroeconomic tailwinds include growth in disposable incomes, expanding middle-class populations in emerging markets, and increasing regulatory support for standardized reimbursement models.

Market Dynamics

To evaluate market opportunities, Request Sample

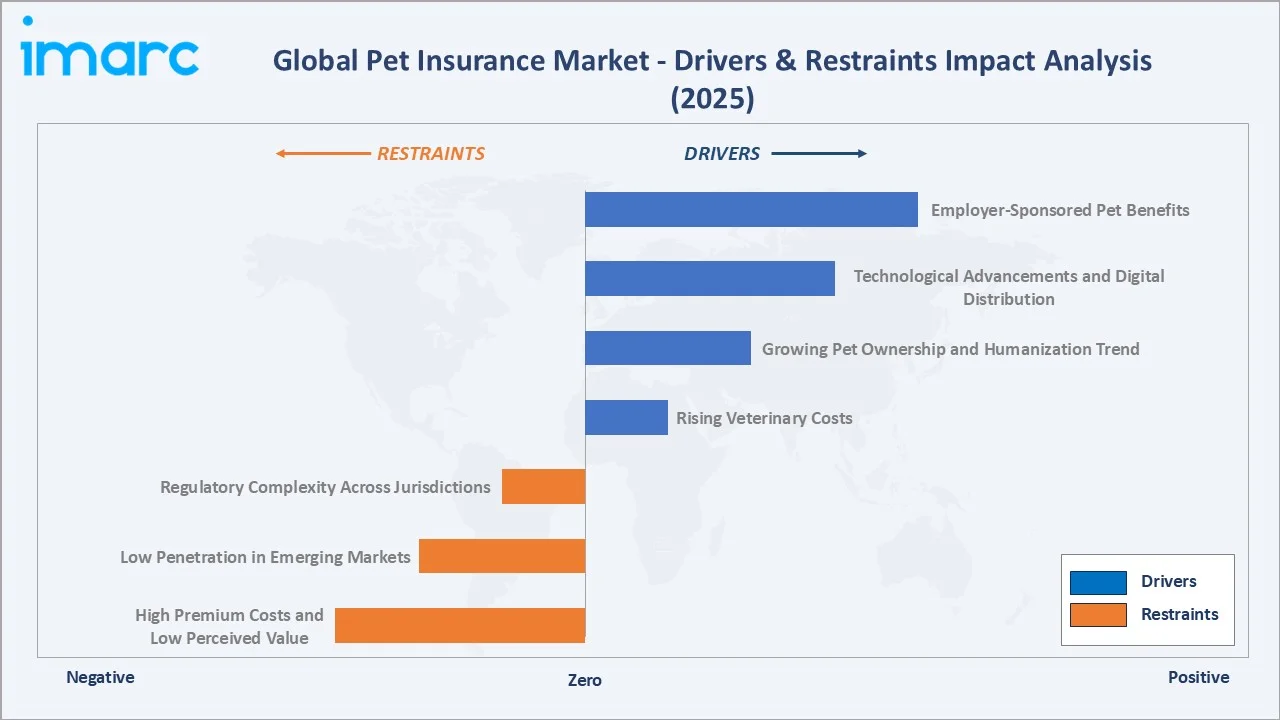

Market Drivers

- Rising Veterinary Costs: Veterinary care expenses have escalated sharply. The ASPCA estimates first-year dog ownership medical costs between USD 1,904–USD 3,221 in 2022. Routine care for dogs involves expenses, while accident-related procedures can exceed high costs per incident, making insurance a financial necessity.

- Growing Pet Ownership and Humanization Trend: The APPA reported 95 million pet-owning U.S. households in 2025– more than 70% of all households. This emotional bond intensifies willingness to invest in premium healthcare and financial protection.

- Technological Advancements and Digital Distribution: InsurTech innovations including AI underwriting, mobile-first claims apps, telemedicine integrations, and real-time policy comparisons – have dramatically reduced policy acquisition costs and improved customer experience, driving adoption among younger demographics.

- Employer-Sponsored Pet Benefits: An increasing number of large companies now include pet insurance in employee benefits packages. Employer adoption has risen significantly over recent years, thereby expanding the addressable market.

Market Restraints

- High Premium Costs and Low Perceived Value: Average monthly premiums in the US are approximately USD 53 for dogs and USD 32 for cats. Many pet owners perceive premiums as high relative to benefits, particularly for older animals with pre-existing conditions.

- Low Penetration in Emerging Markets: In Asia-Pacific, Latin America, and the Middle East, cultural perceptions around animal healthcare spending and limited awareness of insurance products constrain market growth, even as pet ownership rises rapidly.

- Regulatory Complexity: Varying reimbursement structures, exclusion clauses, and lack of standardized policy frameworks across jurisdictions create friction for cross-border insurers and reduce policy transparency for consumers.

Market Opportunities

- Untapped Emerging Markets: China’s urban pet population is very large, while insurance penetration remains low, indicating a significant market opportunity. India and Brazil show similar trends with rapidly rising middle-class pet ownership.

- Wellness and Preventive Care Integration: Bundling preventive care such as vaccinations, dental cleanings, and annual exams into insurance policies enhances long-term customer value. Insurers offering wellness riders reported notably higher retention rates.

- Embedded Insurance and Partnerships: Collaborations with veterinary chains, pet retailers, e-commerce platforms, and breeders offer low-cost distribution and embedded enrollment at the point of pet acquisition.

Market Challenges

- Adverse Selection and Claims Fraud: Insurers face challenges when policyholders enroll only after a diagnosis. This adverse selection increases loss ratios for leading insurers.

- Standardization of Veterinary Pricing: The absence of transparent, standardized veterinary billing makes it difficult for insurers to model risk accurately, leading to conservative underwriting and coverage gaps.

- Consumer Education Gaps: Many pet owners remain unaware of coverage options, exclusions, and the claims process. Insurer investment in educational marketing remains critical to converting awareness into policy uptake.

Emerging Market Trends

The pet insurance market is shaped by five transformative trends that are redefining product design, distribution, and consumer engagement globally.

1. Shift Toward Customizable and Modular Policies

Insurers are moving away from one-size-fits-all products. By 2025, a majority of new policies issued by leading US insurers featured customizable deductibles, reimbursement levels, and coverage limits. Modular plan designs allow pet owners to tailor coverage based on breed, age, and health risks.

2. InsurTech-Driven Digital Transformation

Digital-native platforms use AI to enable faster claims processing. Digital-first insurers have significantly reduced settlement times, improving overall customer satisfaction.

3. Integration with Employer Benefits Ecosystems

Pet insurance is increasingly being included in corporate benefits packages alongside health and dental coverage. Employer interest has risen significantly, reflecting growing employee demand driven by higher pet ownership in recent years.

4. Wellness Plan Expansion and Preventive Care Focus

Coverage is expanding beyond illness and accidents to include preventive wellness services. A growing share of new policies in North America now include wellness riders covering vaccinations, flea prevention, and annual examinations, helping reduce long-term healthcare costs.

5. AI-Powered Underwriting and Telemedicine

Artificial intelligence is transforming risk assessment in pet insurance. Insurers are incorporating breed-specific genetic risk data, wearable health monitors, and telehealth consultations to improve pricing accuracy and enable more proactive pet health management, while veterinary telehealth continues to expand rapidly.

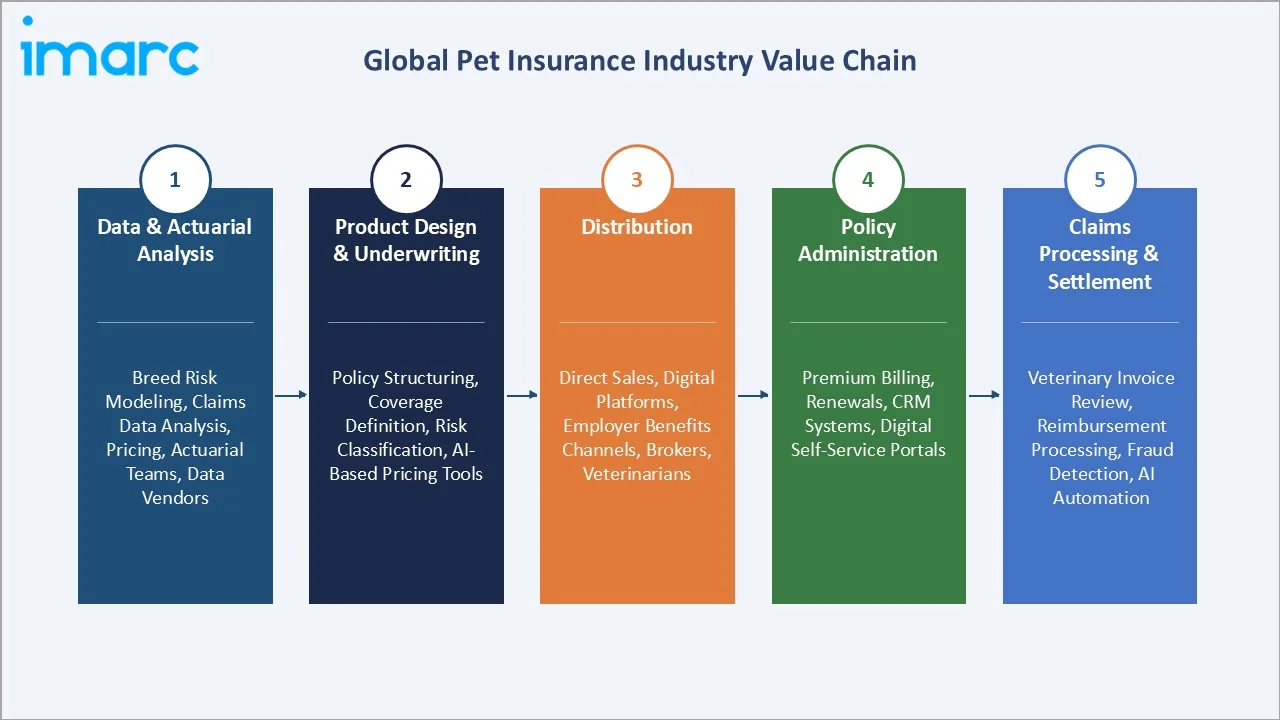

Industry Value Chain Analysis

The pet insurance industry value chain spans five interconnected stages – from actuarial data modeling to end-user claims settlement – with technology integration redefining efficiency at each stage.

|

Stage |

Key Activities |

|

Data & Actuarial Analysis |

Breed risk modeling, claims data analysis, pricing |

|

Product Design & Underwriting |

Policy structuring, coverage definition, risk classification |

|

Distribution |

Direct sales, digital platforms, employer benefits, brokers/vets |

|

Policy Administration |

Premium billing, renewals, CRM, digital portals |

|

Claims Processing & Settlement |

Veterinary invoice review, reimbursement, fraud detection |

Technology integration is transforming efficiency across this value chain, enabling faster underwriting, digital policy management, and automated claims processing. Advanced analytics and AI-driven tools are enhancing decision-making, reducing operational costs, and improving overall customer experience from enrollment to claims settlement.

Technology Landscape in the Pet Insurance Industry

Technology is the central growth enabler in the pet insurance market, reshaping underwriting accuracy, distribution reach, and claims efficiency across the value chain.

AI and Machine Learning in Underwriting

Advanced algorithms analyze breed genetics, age, geographic health data, and historical claims to build individualized risk profiles. Leading insurers have reported reduced underwriting costs through AI adoption, highlighting clear returns on technology investment.

Wearables and IoT Health Monitoring

GPS and biometric pet wearables from companies like FitBark, and PetPace provide continuous health data. Insurers integrating wearable data into policy underwriting can offer usage-based or health-linked premium discounts of up to 15%, incentivizing preventive pet care.

Digital Claims Processing and Telehealth

Mobile-first claims submission, AI-powered invoice parsing, and real-time eligibility checks are now standard features on leading platforms. Telehealth integrations with veterinary providers also enable 24/7 consultations for policyholders. The pet telehealth segment is growing rapidly, further expanding digital touchpoints for insurance engagement.

Blockchain for Policy Transparency

Pilot programs in Europe and North America are deploying blockchain for immutable policy records, transparent claim histories, and cross-insurer data sharing to reduce fraud. Insurance fraud worldwide estimated to exceed $80b annually in 2025, underscoring the urgency of this initiative.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Policy | Illnesses and Accidents | 🔒 | 2025 |

| Animal | Dogs | 58.5% | 2025 |

| Provider | Public | 62.4% | 2025 |

| Region | North America | 42.5% | 2025 |

By Provider

To access detailed market analysis, Request Sample

The public provider segment commands 62.4% of the market in 2025, supported by state-backed schemes in Sweden, Germany, and Japan – countries where pet insurance was first mandated or publicly subsidized. These programs benefit from broad distribution through national postal networks and municipal services. However, the private provider segment is the fastest-growing at ~11.4% CAGR, driven by InsurTech disruption, flexible policy design, and direct-to-consumer digital platforms that significantly lower customer acquisition costs.

By Animal

Dogs lead with 58.5% share in 2025, reflecting higher per-incident veterinary costs and stronger owner willingness to insure. Average annual dog insurance premiums in the US reached approximately USD 636 in 2024 (USD 53/month). Cats hold 32.4% – a growing segment as specialized feline coverage for chronic conditions like hyperthyroidism and diabetes gains traction. The Others category (9.1%) is the fastest-growing at ~12.1% CAGR, driven by rising ownership of rabbits, birds, reptiles, and small mammals, particularly in Europe and Asia-Pacific where exotic pet markets are expanding.

Regional Market Insights

The pet insurance industry exhibits distinct regional dynamics shaped by pet ownership rates, veterinary cost structures, regulatory environments, and insurer penetration strategies.

|

Region |

Market Share (2025) |

Key Growth Drivers |

|

North America |

42.5% |

High vet costs, employer benefits, strong InsurTech ecosystem |

|

Europe |

28.6% |

Mature public-private models, Sweden/Germany leadership |

|

Asia-Pacific |

18.4% |

Rapidly growing pet ownership, Japan's Anicom, China expansion |

|

Latin America |

6.2% |

Rising middle-class pet ownership, early-stage market development |

|

Middle East & Africa |

4.3% |

Premium pet market growth in UAE, South Africa's dotsure expansion |

North America

North America dominates with 42.5% of global revenue in 2025. The US accounts for the bulk, with an estimated 4.8 million insured pets as of 2024 – though penetration remains under 4% of the total pet population. High veterinary costs (average emergency visit USD 1,500–USD 5,000), rising employer adoption, and aggressive InsurTech competition (Trupanion, Lemonade, Spot, Pumpkin) are driving strong growth at an estimated 9.0% CAGR through 2034.

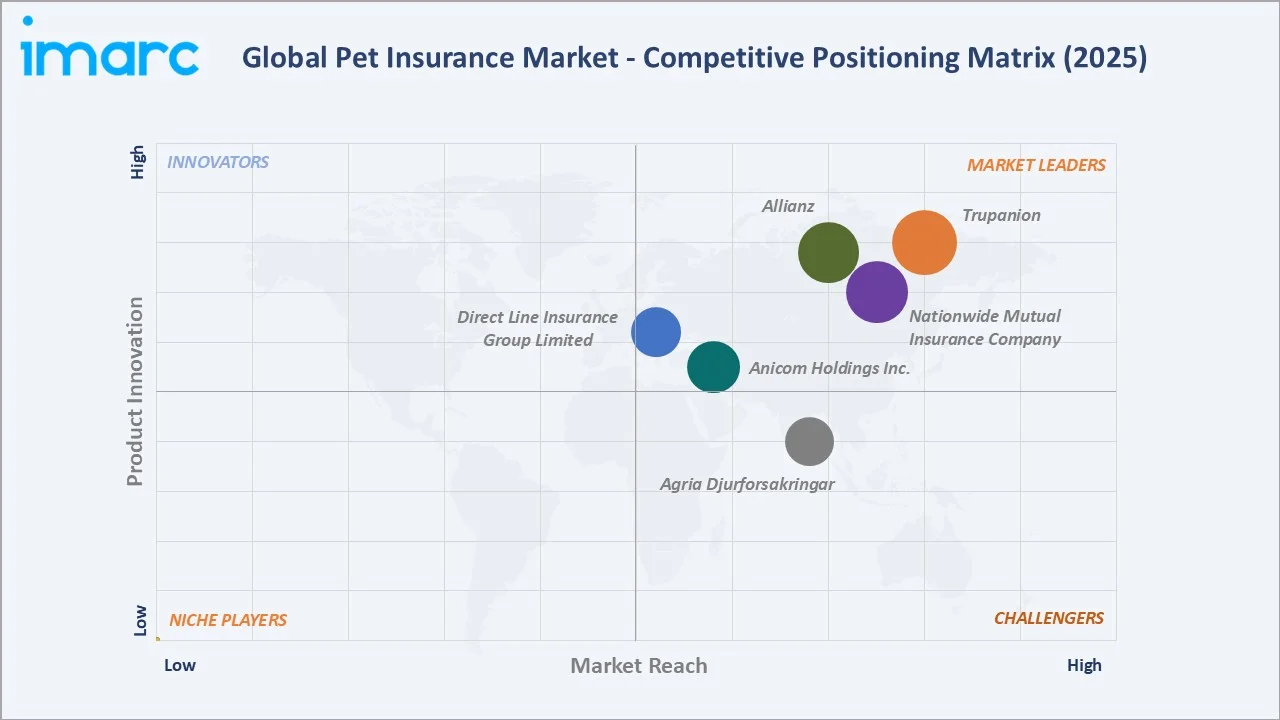

Competitive Landscape

The global pet insurance market is moderately fragmented, with a mix of large multi-line insurers, dedicated pet insurance specialists, and emerging InsurTech disruptors competing across geographies.

|

Company Name |

Brand / Subsidiary |

Market Position |

|

Trupanion |

Trupanion |

Leader |

|

Nationwide Mutual Insurance Company |

Nationwide Pet |

Leader |

|

Allianz |

Petplan |

Leader |

|

Anicom Holdings Inc. |

Anicom Insurance |

Regional Leader (APAC) |

|

Agria Djurförsäkringar |

Agria |

Regional Leader (Europe) |

|

Direct Line Insurance Group Limited |

Direct Line Pet |

Established Player |

Competition is further shaped by increasing technology adoption and distribution partnerships, as both traditional insurers and digital-first platforms expand their reach. This evolving landscape is driving innovation while intensifying rivalry across established and emerging markets.

Key Company Profiles

Trupanion

Trupanion is a leading pet medical insurance provider headquartered in Seattle, USA, specializing in coverage for cats and dogs across the United States, Canada, and select international markets. The company operates a subscription-based model focused on reimbursing veterinary care cost.

- Product Portfolio: Single, comprehensive plans with 90% reimbursement and no payout limits, distinguishing itself from multi-tiered competitors.

- Recent Developments: In 2025, Trupanion reported strong growth in its U.S. pet insurance business in 2025, with direct premiums written reaching $1.22 billion, reflecting steady expansion in demand. The company continued to scale its underwriting operations while maintaining disciplined risk management.

- Strategic Focus: Veterinary hospital partnerships and technology-led distribution.

Nationwide Mutual Insurance Company

Nationwide Mutual Insurance Company is one of the largest U.S.-based mutual insurance and financial services organizations, headquartered in Columbus, Ohio. The company operates across multiple segments including auto, home, life, commercial insurance, and financial services.

- Product Portfolio: Whole Pet with Wellness, Major Medical, and Avian & Exotic plans.

- Recent Developments: In 2024, Nationwide Mutual Insurance Company expanded its presence in the pet insurance segment through an enhanced partnership with Petco Health and Wellness Company, strengthening its integrated pet care and insurance ecosystem.

- Strategic Focus: Employer benefits channels and multi-species coverage.

Allianz

Allianz is a global financial services and insurance company headquartered in Munich, Germany. It is one of the world’s largest insurers and serving millions of customers in property & casualty insurance, life & health insurance, and asset management.

- Product Portfolio: Covered for Life, Time Limited, and Maximum Benefit plans with comprehensive chronic condition coverage.

- Recent Developments: In 2024, Petplan (Allianz) launched a new digital Cover Certainty tool designed to streamline communication between veterinary practices and pet insurance policyholders. The tool allows vets to instantly verify insurance coverage, remaining benefits, and excess amounts, helping reduce delays in treatment decisions and administrative workload.

- Strategic Focus: Chronic condition coverage and digital transformation of claims.

Market Concentration Analysis

The global pet insurance market is characterized by moderate fragmentation at the global level, with concentration varying significantly by geography. At the regional level, especially in the US and UK, the top five players command substantial shares.

The top 5 companies – Trupanion, Nationwide Mutual Insurance Company, Allianz, Anicom Holdings Inc., Agria Djurförsäkringar– collectively account for an estimated 45–50% of global premiums in 2025. The remaining market is served by a diverse mix of regional specialists, white-label insurers, InsurTech disruptors, and direct-to-consumer digital platforms.

Market consolidation is accelerating. Key M&A and partnership activity has increased, as large multi-line insurers seek to acquire InsurTech capabilities, distribution networks, and veterinary partnerships. The entry of technology-led platforms (Lemonade, Spot, Pumpkin) has intensified price competition in the direct-to-consumer segment, pressuring loss ratios industry-wide. Long-term, the market is expected to consolidate around 8–10 global players with strong regional specialists operating in high-growth markets.

Investment & Growth Opportunities

Fastest-Growing Segments

- Private InsurTech providers are experiencing strong growth, driven by expanding digital adoption and shifting customer preferences toward online-first insurance solutions. These companies are leveraging technology to streamline distribution, improve underwriting efficiency, and enhance customer engagement.

- The exotic and other animals’ segment is witnessing significant growth, driven by increasing ownership of non-traditional pets that remain underserved by standard insurance offerings. This creates opportunities for insurers to design specialized products tailored to unique care and risk requirements.

- Wellness and preventive insurance plans are gaining strong traction as insurers increasingly integrate services such as vaccinations, routine check-ups, and dental care into coverage offerings. These value-added benefits are helping strengthen long-term customer engagement.

Emerging Markets

- China – A large and growing urban pet population combined with very low insurance penetration highlights significant untapped potential, creating a substantial long-term market opportunity.

- India and Brazil – Rapid urbanization and rising middle-class incomes are driving increased spending on pets, supporting steady expansion of the pet insurance market in both countries.

- Middle East – Markets such as the UAE and Saudi Arabia are witnessing growing pet ownership among affluent urban populations, supported by the adoption of Western-style pet care practices and increasing demand for premium services.

Venture and Strategic Investment Trends

Global venture investment in pet insurance and pet health technology exceeded USD 500 Million in 2024, focused on AI underwriting platforms, telehealth integrations, and embedded insurance distribution. This influx of capital is accelerating innovation across the value chain, enabling insurers to enhance pricing accuracy, streamline claims processing, and improve customer engagement through digital-first experiences.

Future Market Outlook (2026-2034)

The global pet insurance market forecast is highly positive. The market is projected to grow from USD 9.87 Billion in 2025 to USD 24.08 Billion by 2034, supported by structural tailwinds that are unlikely to reverse.

Technological disruptions – including AI underwriting, wearable-linked premiums, and blockchain-enabled policy transparency – will compress operating costs while improving policyholder experience. The integration of pet insurance into broader pet wellness ecosystems (veterinary chains, pet retail, e-commerce) will dramatically lower customer acquisition costs and expand the insured base beyond traditional demographics.

Emerging market development in China, India, Brazil, and Southeast Asia represents the most significant incremental volume opportunity for the next decade. Regulatory evolution – particularly the standardization of veterinary billing and the introduction of mandated consumer disclosures – will improve market trust and accelerate conversion. The pet insurance sector is positioned to enter a phase of accelerated growth and consolidation through 2034, making it one of the most compelling investment frontiers in the global specialty insurance landscape.

Research Methodology

Primary Research

IMARC Group conducts comprehensive primary research through structured interviews with senior executives, underwriters, veterinary professionals, distribution channel partners, and regulatory authorities across key markets. Primary inputs validate quantitative estimates and provide qualitative market intelligence on emerging trends, pricing dynamics, and competitive strategies.

Secondary Research

Secondary research incorporates data from regulatory filings, national insurance association reports, financial statements, industry publications (NAPHIA, PFMA, AVMA), academic journals, and established databases. Historical market data is cross-validated against multiple sources to ensure accuracy.

Forecasting Models

Market forecasts are developed using a combination of bottom-up and top-down methodologies. Bottom-up models aggregate segment-level data (provider type, animal, and region) to build global estimates. Top-down models apply macroeconomic indicators – GDP growth, pet ownership rates, veterinary cost inflation indices – to project forward trajectories. All models are stress-tested against conservative, base, and optimistic scenarios.

Pet Insurance Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Policies Covered | Illnesses and Accidents, Chronic Conditions, Others |

| Animals Covered | Dogs, Cats, Others |

| Providers Covered | Public, Private |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Trupanion, Nationwide Mutual Insurance Company, Allianz, Anicom Holdings Inc., Agria Djurförsäkringar, Direct Line Insurance Group Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the pet insurance market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global pet insurance market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the pet insurance industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Pet Insurance Market Report

The global pet insurance market reached USD 9.87 Billion in 2025. It is forecast to reach USD 24.08 Billion by 2034 at a CAGR of 10.05% during 2026-2034.

The market is growing at a CAGR of 10.05% from 2026 to 2034, driven by rising veterinary costs, growing pet ownership, and expanding awareness of insurance coverage.

North America leads with 42.5% of global revenue in 2025, driven by high veterinary costs, employer-sponsored benefits, and a mature InsurTech ecosystem.

Asia-Pacific is the fastest-growing region at an estimated 13.5% CAGR, led by Japan's Anicom Holdings and rapidly expanding urban pet ownership in China.

By animal, the market is segmented into dogs (58.5%), cats (32.4%), and others including exotic animals (9.1%). Dogs represent the largest share in 2025.

The public provider segment holds 62.4% share in 2025. Private providers account for 37.6% but are growing faster at approximately 11.4% CAGR through 2034.

Key companies include Trupanion, Nationwide Mutual Insurance Company, Allianz, Anicom Holdings Inc., Agria Djurförsäkringar, and Direct Line Insurance Group Limited.

Key drivers include rising veterinary costs, growing pet humanization, expanding pet ownership, technological advancements in InsurTech, and the rise of employer-sponsored pet benefits.

Challenges include high premium costs, low market penetration globally, adverse selection risks, regulatory complexity across jurisdictions, and consumer education gaps about policy coverage.

The global pet insurance market is projected to reach approximately USD 15.93 Billion by 2030, due to rising pet ownership and increasing awareness of pet healthcare coverage.

AI-driven underwriting, mobile claims apps, veterinary telehealth integration, and wearable pet health monitors are transforming cost structures, improving customer experience, and enabling risk-based pricing.

Fastest-growing opportunities include private InsurTech platforms, wellness plan integration, exotic animal coverage, and untapped emerging markets in China, India, and Latin America.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)