Pharmaceutical Packaging Market Size, Share, Trends and Forecast by Material, Product, End User, and Region, 2026-2034

Pharmaceutical Packaging Market Size and Share:

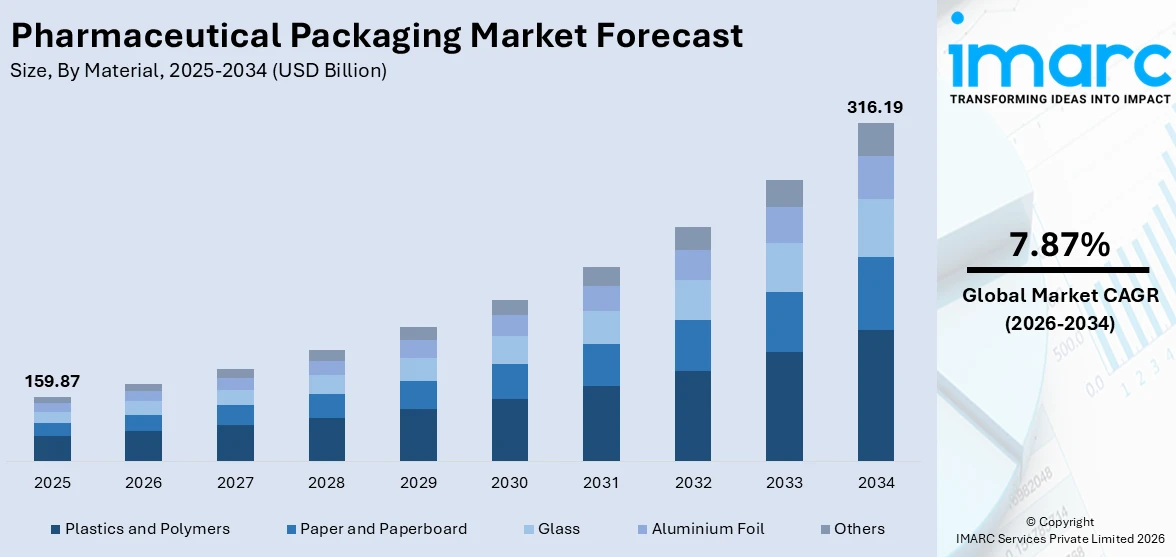

The global pharmaceutical packaging market size was valued at USD 159.87 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 316.19 Billion by 2034, exhibiting a CAGR of 7.87% from 2026-2034. Asia Pacific currently dominates the market, holding a market share of 33% in 2025. The region benefits from its rapidly expanding pharmaceutical manufacturing base, increasing healthcare investments, a growing patient population, and rising demand for innovative drug delivery systems, all of which contribute significantly to the pharmaceutical packaging market share.

The pharmaceutical packaging market is driven by a set of factors that are changing the pharmaceutical packaging industry’s landscape. The rising incidence of chronic and infectious diseases worldwide has led to an increase in pharmaceutical manufacture, leading to the need for pharmaceutical packaging. The regulatory bodies in different regions continue to enforce strict packaging regulations to ensure the safety, efficacy, and tamper-resistance of pharmaceutical products, thus driving the demand for packaging solutions that meet these requirements. The development of biologics and biosimilars requires specialized packaging solutions that can maintain the integrity of the product throughout the supply chain. The growing awareness of consumers on counterfeit drugs has driven the adaption of anti-counterfeiting packaging solutions. The pharmaceutical packaging market is further fueled by innovative sustainable packaging solutions and smart packaging formats that are increasingly sought after by pharmaceutical companies committed to regulatory and sustainability solutions.

The United States has emerged as a major region in the pharmaceutical packaging market owing to many factors. As one of the world's largest pharmaceutical markets, the United States generates substantial and consistent demand for diverse packaging solutions spanning prescription drugs, over-the-counter medications, and biologics. The country's well-established pharmaceutical manufacturing ecosystem, combined with the presence of leading drug developers and contract manufacturing organizations, creates a strong foundation for packaging demand. In May 2024, Gerresheimer AG announced a USD 180 million expansion of its pharmaceutical packaging and drug-delivery production facility in Peachtree City, Georgia, adding nearly 194,000 square feet of capacity and creating over 400 jobs to strengthen supply of inhalers and autoinjector packaging systems for the U.S. market. Regulatory frameworks enforced by the U.S. Food and Drug Administration mandate rigorous packaging compliance, including child-resistant closures, tamper-evident features, and clear labeling standards, driving investments in advanced packaging technologies. The pharmaceutical packaging market outlook in the United States is further bolstered by the growing adoption of unit-dose and patient-specific packaging formats that enhance medication adherence and reduce dosing errors across pharmacy settings.

To get more information on this market Request Sample

Pharmaceutical Packaging Market Trends:

Growing Adoption of Smart Packaging Technologies

The pharmaceutical sector is increasingly embracing smart packaging technologies to enhance drug safety, patient engagement, and supply chain transparency. Smart packaging integrates advanced electronic components, sensors, and connectivity features into traditional formats, enabling real-time monitoring of temperature, humidity, and light exposure during storage and transportation. These capabilities are especially critical for biologics, vaccines, and other temperature-sensitive products requiring stringent environmental controls. In January 2025, Avery Dennison, in collaboration with Becton, Dickinson and Company, introduced the BD iDFill™ RFID-enabled prefillable syringe identification solution, embedding RFID tags directly into syringe components to provide unit-level traceability, authentication, and lifecycle monitoring. Near-field communication chips and QR codes allow patients and healthcare providers to access dosing instructions and authenticity verification through smartphones. Regulatory authorities are also actively encouraging serialization and track-and-trace systems, positioning smart packaging as a central area of innovation across the pharmaceutical industry.

Rising Demand for Sustainable Packaging Solutions

Environmental sustainability has emerged as a transformative force in pharmaceutical packaging, reshaping material selection, manufacturing processes, and end-of-life disposal strategies. Pharmaceutical companies face increasing pressure from regulatory bodies and environmentally conscious consumers to minimize the ecological footprint of their packaging operations. This has driven significant interest in recyclable polymers, biodegradable materials, and reduced-consumption packaging designs that maintain product protection and regulatory compliance. According to reports, Amcor announced customer trials of its AmSky™ recyclable polyethylene-based blister packaging, eliminating PVC and enabling compatibility with existing recycling streams while maintaining pharmaceutical safety standards. The innovation was designed as a sustainable alternative for regulated healthcare packaging and can reduce carbon footprint by up to 70% compared to conventional blister packs. The shift toward mono-material structures is gaining prominence as it simplifies recycling streams. The pharmaceutical packaging market trends reflect a growing commitment to circular economy principles, where packaging materials are designed for recovery and reuse rather than single-use disposal.

Expansion of Biologics and Specialty Drug Packaging

The rapid proliferation of biologics, biosimilars, and specialty drugs is fundamentally transforming packaging requirements within the pharmaceutical industry. Unlike conventional small-molecule drugs, biologics are complex, fragile molecules highly sensitive to temperature fluctuations, physical agitation, and chemical interactions with packaging materials. This complexity necessitates advanced primary packaging formats, including pre-filled syringes, vials, and autoinjectors, crafted from specialized glass and polymer materials ensuring chemical inertness and structural integrity. In March 2024, SCHOTT Pharma announced a USD 371 million investment to build a new manufacturing facility in North Carolina to produce prefillable polymer and glass syringes for biologics, vaccines, and mRNA therapies, strengthening the domestic supply chain for advanced injectable drugs and supporting rising biologics demand. The growing pipeline of monoclonal antibodies, gene therapies, and cell-based treatments is driving demand for high-barrier packaging systems. The pharmaceutical packaging market forecast highlights sustained expansion of specialty packaging segments, further accelerated by increasing patient self-administration trends worldwide.

Pharmaceutical Packaging Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global pharmaceutical packaging market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on material, product, and end user.

Analysis by Material:

- Plastics and Polymers

- Polyvinyl Chloride (PVC)

- Polypropylene (PP)

- Homo

- Random

- Polyethylene Terephthalate (PET)

- Polyethylene (PE)

- HDPE

- LDPE

- LLDPE

- Polystyrene (PS)

- Others

- Paper and Paperboard

- Glass

- Aluminium Foil

- Others

Plastics and polymers currently occupy a market share of 40%. Plastics and polymers are the most widely used material type in pharmaceutical packaging due to their unparalleled blend of flexibility, cost-effectiveness, lightweight characteristics, and outstanding barrier properties. This particular material type encompasses a broad range of polymer materials such as polyvinyl chloride (PVC), polypropylene (PP), polyethylene terephthalate (PET), polyethylene (PE), and polystyrene (PS), each possessing unique functional properties suited to specific pharmaceutical packaging needs. Plastics and polymers are widely used in blister packaging, bottles, closures, parenteral packaging, and flexible pouches, reflecting their versatility in meeting the needs of various dosage forms and drug delivery systems. Their ability to be processed into complex shapes, coupled with their outstanding moisture and oxygen barrier properties, makes them essential for protecting solid, liquid, and semi-solid pharmaceutical formulations.

Analysis by Product:

- Primary

- Plastic Bottles

- Caps and Closures

- Parenteral Containers

- Syringes

- Vials and Ampoules

- Others

- Blister Packs

- Prefillable Inhalers

- Pouches

- Medication Tubes

- Others

- Secondary

- Prescription Containers

- Pharmaceutical Packaging Accessories

- Tertiary

Primary leads the market with 51% market share. Hence, primary packaging represents the most tightly regulated element of pharmaceutical packaging due to its contact with the drug product. This segment covers a large number of packaging formats such as plastic bottles, caps and closures, parenteral containers (syringes, vials, and ampoules), blister packs, prefillable inhalers, pouches, and medication tubes for various pharmaceutical purposes in different therapy categories. Primary packaging plays an irreplaceable role in maintaining drug sterility, stability and efficacy by providing robust physical barriers against moisture, oxygen, light and microbial contamination throughout the product lifecycle. The growth of injectable therapeutics (particularly biologics and vaccines) continues to raise demand for sophisticated parenteral primary packaging formats, maintaining the cycle of technological advancement in vial-system and prefilled delivery devices. Also, the growing number of patient self-administration trends necessitated the development of highly intuitive primary packaging designs focused on patient ease of use, dosing accuracy, and patient safety worldwide across retail and institutional healthcare settings.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

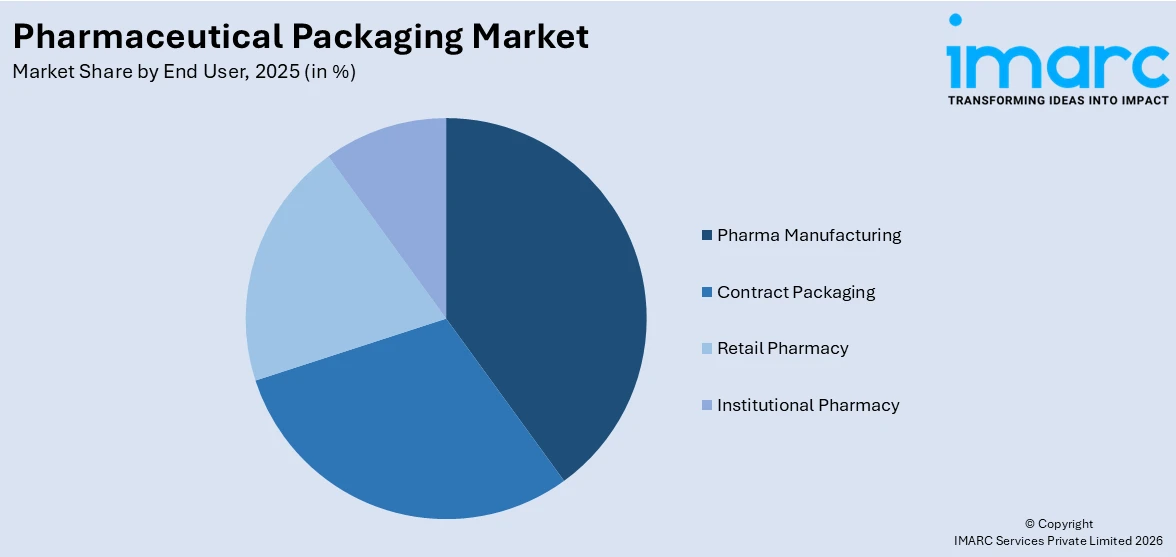

- Pharma Manufacturing

- Contract Packaging

- Retail Pharmacy

- Institutional Pharmacy

Pharma manufacturing dominates the market, with a share of 35%. Pharmaceutical manufacturing companies represent the primary and most significant consumers of pharmaceutical packaging solutions, driven by the large-scale production of prescription drugs, over-the-counter medications, biologics, and active pharmaceutical ingredients. These entities require packaging that meets exacting regulatory standards for sterility, product protection, tamper-evidence, and compliance with pharmacopeial specifications enforced by agencies such as the U.S. Food and Drug Administration, European Medicines Agency, and other national regulatory bodies worldwide. Pfizer announced a USD 750 million investment to expand its Kalamazoo, Michigan manufacturing facility to increase production of injectable medicines and vaccines, including advanced sterile injectable and prefilled formats that require specialized filling and packaging infrastructure. The pharmaceutical manufacturing sector demands a diverse portfolio of primary and secondary packaging formats, including bottles, vials, ampoules, blister packs, cartons, and labels, necessitating fully integrated packaging solutions capable of efficiently handling high-volume production environments. Ongoing capacity expansions at manufacturing facilities, particularly across emerging economies in Asia Pacific and Latin America, are contributing to sustained growth in packaging demand from this segment. Furthermore, the widespread adoption of automated filling, sealing, and inspection systems within pharmaceutical plants continues to drive demand for standardized, high-precision packaging formats that are fully compatible with increasingly sophisticated and advanced production technologies deployed globally.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific, accounting for 33% of the share, enjoys the leading position in the market. Asia Pacific has established itself as the dominant region in the global pharmaceutical packaging landscape, underpinned by the presence of one of the world's largest and most rapidly growing pharmaceutical manufacturing ecosystems. Countries such as China, India, Japan, and South Korea collectively account for a substantial share of global generic and specialty drug production, generating consistent and expanding demand for diverse packaging solutions across all material and product categories. The region's large and aging population base, coupled with rising per capita healthcare expenditure and steadily improving access to healthcare infrastructure, continues to drive pharmaceutical consumption at an accelerating pace. Government-led initiatives aimed at strengthening domestic pharmaceutical manufacturing capacities are further catalyzing investments in local packaging production facilities. Additionally, Asia Pacific's competitive labor and raw material costs make it a highly attractive destination for packaging manufacturing operations, attracting significant foreign direct investment and fostering a dynamic, innovation-driven, and rapidly evolving pharmaceutical packaging ecosystem throughout the region.

Key Regional Takeaways:

North America Pharmaceutical Packaging Market Analysis

The North America pharmaceutical packaging market is experiencing steady growth, driven by increasing demand for safe, efficient, and patient-centric packaging solutions. The U.S. and Canada dominate the region due to strict regulatory frameworks enforced by agencies like the FDA and Health Canada, requiring compliance with Good Manufacturing Practices (GMP) and serialization for anti-counterfeiting. Rising adoption of biologics, specialty drugs, and personalized medicine is boosting demand for advanced packaging technologies, including child-resistant closures, blister packs, pre-filled syringes, and smart packaging with track-and-trace capabilities. Sustainability is gaining importance, with manufacturers incorporating recyclable and eco-friendly materials to meet environmental standards and consumer expectations. Market players such as WestRock, Amcor, and Gerresheimer are focusing on innovation, automation, and strategic partnerships to enhance packaging efficiency and safety. Overall, the market is evolving toward solutions that combine regulatory compliance, patient convenience, and environmentally responsible materials.

United States Pharmaceutical Packaging Market Analysis

The United States pharmaceutical packaging market is driven by a highly complex set of factors, including the presence of highly stringent regulations, technological innovation, and the largest consumption base of pharmaceuticals in the world. The healthcare infrastructure in the United States requires pharmaceutical packaging solutions that meet highly stringent requirements for safety, labeling, and patient protection, as mandated by the U.S. Food and Drug Administration, including child-resistant packaging, tamper-evident closures, and the Drug Supply Chain Security Act, which requires serialization. The increasing incidence of chronic diseases such as diabetes, cardiovascular diseases, and oncological disorders is fueling the growth of pharmaceutical dispensing volumes, thereby ensuring consistent demand for primary and secondary packaging in retail and institutional pharmacies. The increasing focus on personalized medicine and specialty biologics is significantly altering the growth trajectory of the pharmaceutical packaging market, thereby fueling demand for high-barrier primary packaging solutions that can ensure the preservation of complex pharmaceutical formulations throughout their shelf life. The highly advanced pharmaceutical manufacturing infrastructure in the United States, as well as the increasing trend of reshoring pharmaceutical manufacturing within the country, continues to fuel significant additional demand for packaging.

Europe Pharmaceutical Packaging Market Analysis

The European pharmaceutical packaging market is shaped by a robust regulatory environment, a sophisticated pharmaceutical manufacturing base, and a strong emphasis on sustainability and patient safety. The European Medicines Agency and national regulatory bodies across member states enforce comprehensive packaging requirements mandating serialization, tamper-evidence, and multilingual labeling for pharmaceutical products distributed within the bloc. The European Union's Falsified Medicines Directive has played a pivotal role in accelerating the adoption of serialization and verification technologies across the packaging supply chain, significantly strengthening product authenticity safeguards. In October 2025, Gerresheimer AG announced a €30 million investment to construct a new production facility in Wertheim, Germany, dedicated to ready-to-fill pharmaceutical vials. The expansion will enhance sterile primary packaging capacity and support growing demand from European pharmaceutical and biotech manufacturers for biologics and injectable therapies. Europe's pharmaceutical industry is characterized by a significant concentration of innovative drug manufacturers across Germany, France, the United Kingdom, and Spain, generating substantial and consistent demand for high-quality primary and secondary packaging solutions.

Asia Pacific Pharmaceutical Packaging Market Analysis

The Asia-Pacific pharmaceutical packaging market is underpinned by some of the world’s fastest-growing pharmaceutical production hubs, with China and India serving as global centers for both generic and specialty drug manufacturing. The region’s vast and increasingly health-conscious population base, expanding middle class, and growing healthcare infrastructure investments are collectively driving strong pharmaceutical consumption growth and, consequently, sustained packaging demand. Government-led programs across multiple countries are actively strengthening domestic pharmaceutical manufacturing capabilities, creating parallel growth opportunities for both local and international packaging suppliers. Japan and South Korea continue to be notable contributors to the region’s demand for high-precision and technologically advanced packaging formats aligned with their innovative pharmaceutical pipelines. The growing penetration of modern retail pharmacy chains and institutional healthcare networks across emerging markets within the region is further expanding the addressable market for diverse pharmaceutical packaging formats.

Latin America Pharmaceutical Packaging Market Analysis

The Latin American pharmaceutical packaging market is experiencing steady growth, supported by expanding pharmaceutical manufacturing activities and increasing healthcare access across the region. Brazil and Mexico represent the two largest pharmaceutical markets in Latin America, collectively accounting for a dominant share of regional packaging consumption. Rising chronic disease prevalence, expanding health insurance coverage, and government health initiatives are driving pharmaceutical demand, which in turn stimulates packaging requirements. The region is also witnessing growing interest in sustainable packaging solutions among manufacturers seeking to align with global environmental standards. Investments in local pharmaceutical production capacity are anticipated to further strengthen packaging demand across Latin America’s key markets in the coming years.

Middle East And Africa Pharmaceutical Packaging Market Analysis

The Middle East and Africa pharmaceutical packaging market is driven by increasing healthcare investments, expanding pharmaceutical manufacturing infrastructure, and growing drug import activities across the region. Gulf Cooperation Council countries are investing in domestic pharmaceutical production as part of broader economic diversification strategies, generating new demand for packaging materials and systems. In Africa, rising population growth, improving healthcare access, and government programs targeting communicable and non-communicable disease management are driving pharmaceutical consumption. The region’s dependence on imported pharmaceutical products also sustains demand for robust primary and secondary packaging that maintains product quality through complex distribution chains operating across diverse climatic and logistical conditions.

Competitive Landscape:

The global pharmaceutical packaging market is characterized by intense competition among established multinational corporations and regional specialists, each striving to enhance their market positions through product innovation, strategic partnerships, and geographic expansion. Leading companies are investing in advanced packaging technologies, including smart packaging solutions, sustainable materials, and high-barrier systems, to differentiate their offerings and meet evolving regulatory and customer requirements. The market faces challenges related to rising raw material costs, increasingly stringent environmental regulations, and the need for continuous adaptation to diverse and complex global regulatory frameworks. Companies are increasingly pursuing mergers, acquisitions, and joint ventures to strengthen their product portfolios, expand geographic reach, and leverage complementary technological capabilities. The competitive landscape is also shaped by growing demand from the biologics segment, which requires highly specialized packaging solutions, driving sustained research and development investments among key market participants seeking leadership in this high-growth area.

The report provides a comprehensive analysis of the competitive landscape in the pharmaceutical packaging market with detailed profiles of all major companies, including:

- Amcor plc

- AptarGroup Inc.

- Berry Global Inc.

- CCL Industries Inc.

- Comar LLC

- Drug Plastics Group

- Gerresheimer AG

- Schott AG

- SGD Pharma

- West Pharmaceutical Services Inc.

- WestRock Company

Latest News and Developments:

- In January 2026 West Pharmaceutical Services announced the global commercial availability of its Synchrony™ S1 prefillable syringe system designed for biologics and vaccines. The platform features advanced barrier film plungers and multiple needle configurations to enhance drug protection and delivery reliability. The launch strengthens ready-to-use injectable packaging solutions, supporting growing demand for biologics and home-based drug administration.

- In January 2026 SGD Pharma introduced new molded and tubular glass vial packaging solutions, expanding its portfolio following the acquisition of Alphial. The enhanced range improves packaging strength, sterility, and scalability for biologics and injectable therapies. This development reinforces the company’s capacity to support growing demand for high-value biopharmaceutical packaging.

Pharmaceutical packaging Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Materials Covered |

|

| Products Covered |

|

| End Users Covered | Pharma Manufacturing, Contract Packaging, Retail Pharmacy, Institutional Pharmacy |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Amcor plc, AptarGroup Inc., Berry Global Inc., CCL Industries Inc., Comar LLC, Drug Plastics Group, Gerresheimer AG, Schott AG, SGD Pharma, West Pharmaceutical Services Inc., WestRock Company, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the pharmaceutical packaging market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global pharmaceutical packaging market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the pharmaceutical packaging industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Pharmaceutical Packaging Market Report

The pharmaceutical packaging market was valued at USD 159.87 Billion in 2025.

The pharmaceutical packaging market is projected to exhibit a CAGR of 7.87% during 2026-2034, reaching a value of USD 316.19 Billion by 2034.

The pharmaceutical packaging market is driven by rising pharmaceutical production volumes, stringent regulatory compliance requirements, growth in biologics and biosimilars, increasing adoption of anti-counterfeiting technologies, expansion of e-commerce pharmaceutical distribution channels, and sustained innovation in sustainable and smart packaging solutions.

Asia Pacific currently dominates the pharmaceutical packaging market, accounting for a share of 33%. The region benefits from a vast pharmaceutical manufacturing base in China and India, a large and growing patient population, rising healthcare expenditure, and strong government support for domestic pharmaceutical production expansion.

Some of the major players in the pharmaceutical packaging market include Amcor plc, AptarGroup Inc., Berry Global Inc., CCL Industries Inc., Comar LLC, Drug Plastics Group, Gerresheimer AG, Schott AG, SGD Pharma, West Pharmaceutical Services Inc., WestRock Company, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)