Philippines Commercial Vehicles Market Size, Share, Trends and Forecast by Vehicle Type, Propulsion Type, End Use, and Region, 2026-2034

Philippines Commercial Vehicles Market Summary:

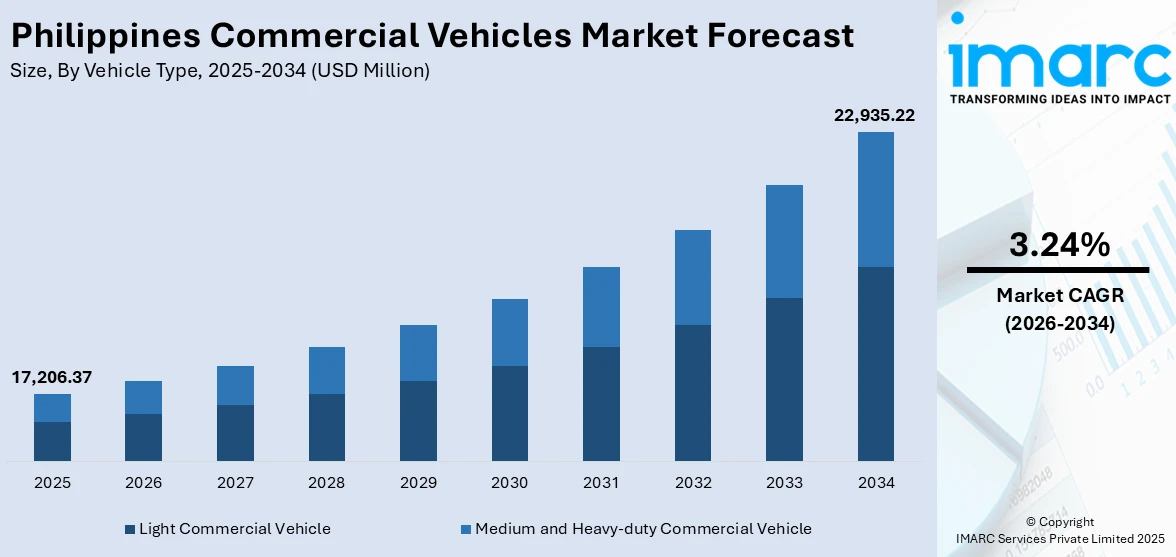

The Philippines commercial vehicles market size was valued at USD 17,206.37 Million in 2025 and is projected to reach USD 22,935.22 Million by 2034, growing at a compound annual growth rate of 3.24% from 2026-2034.

The Philippines commercial vehicles market is experiencing a stable growth, aided by the acceleration of infrastructure development; advancement of logistics and distribution networks; and increase in demand for effective transportation of freight across the archipelago. Continuous commitment from the government towards mega transportation and connectivity projects is raising demand for different types of commercial vehicles. At the same time, rapidly growing e-commerce, continuous urbanization, and modernization of the public transport fleet are changing the requirements for mobility and creating sustained prospects for various manufacturers and fleet operators across the Philippines commercial vehicles market share.

Key Takeaways and Insights:

- By Vehicle Type: Light commercial vehicles dominate the market with a share of 58.4% in 2025, driven by strong demand from small and medium enterprises, last-mile logistics providers, and retail distribution networks requiring versatile and cost-effective transport solutions across urban and provincial areas.

- By Propulsion Type: IC engine lead the market with a share of 94.1% in 2025, reflecting the continued reliance on diesel-powered commercial vehicles owing to their proven durability, established refueling infrastructure, and favorable total cost of ownership for fleet operators.

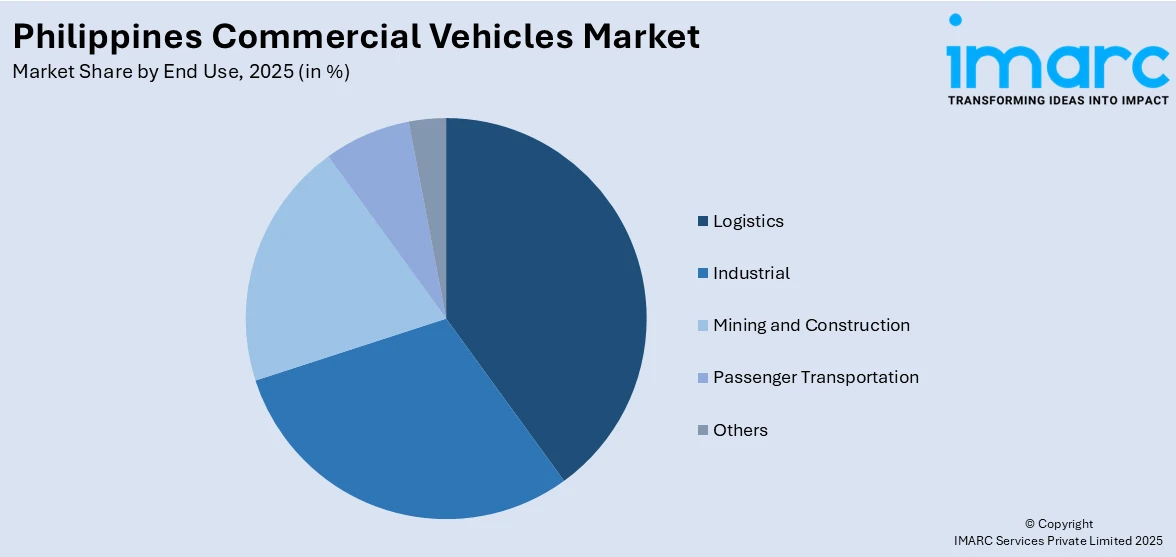

- By End Use: Logistics holds the largest market share at 36.7% in 2025, supported by the rapid expansion of e-commerce activities, growing domestic trade volumes, and increasing investments in warehousing and freight transportation infrastructure throughout the archipelago.

- By Region: Luzon represents the largest segment with a market share of 63.2% in 2025, owing to the concentration of major economic zones, industrial hubs, port facilities, and the national capital region that collectively generate the highest commercial vehicle demand.

- Key Players: The Philippines commercial vehicles market is moderately competitive, with established Japanese manufacturers holding significant share alongside emerging Chinese brands, as companies invest in expanded dealer networks, after-sales support, and diversified product lineups to capture growing demand.

To get more information on this market Request Sample

The Philippines commercial vehicles market is witnessing a transformative phase driven by the convergence of infrastructure modernization, evolving trade dynamics, and shifting consumer mobility preferences. The government’s ambitious infrastructure spending agenda is generating sustained demand for construction and logistics vehicles, while the rapid expansion of digital commerce is accelerating the need for last-mile delivery solutions. In 2025, Isuzu Philippines Corporation maintained its leadership in the truck segment, selling 4,794 units and capturing a 42.2% market share across light‑, medium‑, and heavy‑duty segments, underscoring strong commercial vehicle uptake amid growing logistics and infrastructure activities. Additionally, the country’s strategic geographic position within Southeast Asia is strengthening its role as a regional logistics hub, further driving demand for trucks, buses, vans, and specialized utility vehicles across both urban centers and provincial markets.

Philippines Commercial Vehicles Market Trends:

Rising Adoption of Electric and Hybrid Commercial Vehicles

The Philippines is witnessing growing interest in electrified commercial transportation as fleet operators and logistics providers explore cleaner alternatives to conventional diesel-powered vehicles. The introduction of battery-electric trucks and buses is gaining traction, supported by government policies encouraging low-emission mobility solutions. In 2025, DHL Summit Solutions deployed one of the country’s largest electric vehicle fleets, including 23 electric vehicles and 22 prime movers, as part of its plan to increase EV share and reduce logistics emissions, signaling stronger corporate commitments to electrified transport. Improved battery technologies, declining production costs, and expanding charging infrastructure are creating favorable conditions for electrified commercial vehicles. This trend is expected to accelerate the Philippines commercial vehicles market growth as sustainability becomes a key consideration in fleet procurement decisions.

Expansion of Last-Mile Delivery Vehicle Demand

The rapid growth of e-commerce and digital retail platforms is significantly reshaping the commercial vehicle landscape in the Philippines. Increasing consumer expectations for faster and more reliable deliveries are driving demand for light commercial vehicles tailored for urban logistics operations. In January 2026, logistics provider 2GO Group, Inc. expanded its express and e‑commerce fulfilment capabilities, including nationwide pickup, sorting, and last‑mile delivery supported by digital tracking platforms, to better meet rising online order volumes and strengthen urban delivery networks. Logistics companies are investing in compact, fuel-efficient, and technologically advanced delivery vehicles equipped with real-time tracking and route optimization capabilities. This shift is encouraging manufacturers to develop purpose-built vehicles that address the unique requirements of dense urban environments and island connectivity.

Fleet Modernization and Public Transport Transformation

The Philippines is undergoing a comprehensive transformation of its public transportation system, with legacy vehicles being progressively replaced by modern, safer, and more fuel-efficient alternatives. The utility vehicle program is accelerating the adoption of compliant commercial vehicles that meet updated emission and safety standards. According to the Land Transportation Franchising and Regulatory Board (LTFRB), nearly 90% of public utility vehicle operators nationwide have now consolidated under the Public Transport Modernization Program (PTMP), marking widespread industry compliance and progress toward modernized fleets. This national initiative is creating substantial demand for modern jeepneys, minibuses, and medium-duty passenger transport vehicles. The emphasis on organized fleet operations through cooperatives and corporations is further professionalizing the commercial vehicle sector.

Market Outlook 2026-2034:

The commercial vehicles market in the Philippines is expected to grow and sustain its growth rate over the forecasted period, driven by ongoing infrastructure development, changing logistics needs, and improving regulations supporting cleaner transportation alternatives. The country’s ongoing transport modernization plan, coupled with robust growth rates in electronic commerce transportation infrastructure and construction activity, is expected to foster strong commercial vehicle demand across various markets. Moreover, urbanization and transport needs are also expected to support strengthened momentum in commercial vehicle demand within the country in coming years. The market generated a revenue of USD 17,206.37 Million in 2025 and is projected to reach a revenue of USD 22,935.22 Million by 2034, growing at a compound annual growth rate of 3.24% from 2026-2034.

Philippines Commercial Vehicles Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Vehicle Type |

Light Commercial Vehicle |

58.4% |

|

Propulsion Type |

IC Engine |

94.1% |

|

End Use |

Logistics |

36.7% |

|

Region |

Luzon |

63.2% |

Vehicle Type Insights:

- Light Commercial Vehicle

- Medium and Heavy-duty Commercial Vehicle

The light commercial vehicles dominates with a market share of 58.4% of the total Philippines commercial vehicles market in 2025.

Light commercial vehicles, encompassing pickups, vans, and small trucks, form the backbone of commercial transport in the Philippines. Their versatility makes them highly serviceable for both small and large applications, such as retail goods distribution, agricultural produce, construction material delivery, and passenger services. Strong demand within micro, small, and medium enterprises that make up the lion's share of Philippine businesses relies on affordable and adaptable transport solutions for daily operations.

Meanwhile, expanding e-commerce logistics, growing last-mile delivery volumes, and urban congestion that favors smaller, maneuverable vehicles continue to reinforce the dominance of light commercial vehicles. Better access to vehicle financing through government-backed lending programs and competitive dealer promotions is likewise allowing more people to participate in the market. Demand is likewise being driven by the ongoing Public Utility Vehicle Modernization Program, wherein transport cooperatives are upgrading aging jeepney fleets to modern, Euro 4-compliant LCVs designed for passenger service.

Propulsion Type Insights:

- IC Engine

- Electric Vehicle

The IC engine leads with a share of 94.1% of the total Philippines commercial vehicles market in 2025.

Internally Combustion Engine vehicles remain firmly entrenched in their dominant position in the market for commercial vehicles in the Philippines, owing to factors such as the extensive availability of diesel stations throughout the country, competitive acquisition costs, and reliability under harsh conditions. These factors combine to make diesel-engined commercial vehicles extremely popular for transporting goods over distance, for construction work, and mining activities, owing to factors such as fuel range, payload-carrying capabilities, and availability of refueling stations.

The continued support for IC engine-run vehicles is a pointer to the practical realities of fleet operators in dealing with the diversified geography of the Philippines—which includes mountainous regions, rural areas, and island routes and routes yet to be serviced in terms of alternative fuel technologies. Moreover, the growing number of Euro 4 engines in the market, along with improvements in fuel efficiency technologies and competitive pricing of well-established manufacturers, are further giving a push to IC engines as the dominant technology for the majority of commercial transport needs in the country.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Industrial

- Mining and Construction

- Logistics

- Passenger Transportation

- Others

The logistics dominates with a market share of 36.7% of the total Philippines commercial vehicles market in 2025.

The logistics sector is the primary demand driver for commercial vehicles in the Philippines, fueled by the rapid expansion of domestic and cross-border e-commerce, growing retail distribution networks, and increasing cold chain requirements for perishable goods. The country's logistics market continues to expand as businesses invest in fleet modernization to meet rising consumer expectations for faster and more reliable deliveries across the archipelago's dispersed island geography, driving sustained procurement of transport vehicles.

The sector's vehicle demand spans a diverse range, from light delivery vans for urban last-mile operations to heavy-duty trucks for inter-island cargo transport via roll-on/roll-off ferry networks. Strategic partnerships between logistics providers and commercial vehicle manufacturers, investment in warehouse and fulfillment infrastructure, and the government's focus on transforming the Philippines into a regional logistics hub are collectively sustaining strong demand for commercial vehicles optimized for freight and distribution operations.

Regional Insights:

- Luzon

- Visayas

- Mindanao

Luzon exhibits a clear dominance with a 63.2% share of the total Philippines commercial vehicles market in 2025.

Luzon dominates the Philippines commercial vehicles market owing to its concentration of the National Capital Region, major economic zones, and the country's largest industrial corridors. The island houses the majority of manufacturing facilities, logistics hubs, port infrastructure, and retail distribution centers, generating the highest commercial vehicle demand nationwide. Ongoing government infrastructure projects spanning road networks, railway systems, and urban transit developments continue to drive substantial requirements for construction and transport vehicles across the region.

Luzon's commercial vehicle demand is further bolstered by the presence of prominent special economic zones, expanding expressway networks, and the highest concentration of e-commerce fulfillment operations in the country. The region benefits from the most developed dealer networks, vehicle financing infrastructure, and comprehensive after-sales service coverage, enabling higher commercial vehicle penetration rates compared to Visayas and Mindanao. These advantages position Luzon as the central hub for commercial vehicle sales, distribution, and fleet operations throughout the Philippines.

Market Dynamics:

Growth Drivers:

Why is the Philippines Commercial Vehicles Market Growing?

Accelerating Infrastructure Development and Government Spending

The Philippines government’s sustained commitment to large-scale infrastructure development is a primary catalyst for commercial vehicle demand across the country. The administration’s flagship infrastructure program has allocated substantial budgets toward the construction and expansion of roads, bridges, railways, airports, and seaports, creating significant demand for heavy-duty trucks, construction equipment carriers, and specialized transport vehicles. In April 2024, government infrastructure spending rose to P1.545 trillion, equivalent to about 5.8% of GDP, reflecting accelerated implementation of major transport and construction projects such as national highways and foreign‑assisted rail systems that support logistics and heavy transport activity. These infrastructure projects span multiple regions and require extensive logistics support, including the movement of construction materials, heavy machinery, and workforce transportation. The cascading economic effects of infrastructure spending are also stimulating demand for light and medium-duty commercial vehicles as new businesses and distribution networks emerge to serve growing communities connected by improved transportation corridors. This sustained investment trajectory ensures a long-term pipeline of commercial vehicle demand.

Rapid Growth of E-Commerce and Digital Logistics

The explosive expansion of e-commerce and digital retail platforms in the Philippines is fundamentally transforming logistics requirements and driving substantial demand for commercial vehicles tailored to modern distribution needs. The Philippines e-commerce market reached USD 28.0 billion in 2025, reflecting the rapid growth of online retail and increasing consumer reliance on digital platforms. The increasing penetration of internet and smartphone usage, combined with a growing middle class and shifting consumer preferences toward online shopping, has created an urgent need for efficient last-mile delivery solutions. Logistics companies are investing heavily in expanding their vehicle fleets to handle rising order volumes, particularly in urban centers where delivery speed and reliability are critical competitive advantages. The emergence of on-demand logistics services, third-party delivery platforms, and specialized cold chain distribution networks is further diversifying commercial vehicle demand. This digital commerce revolution is creating new market segments for compact delivery vans, temperature-controlled vehicles, and technologically equipped fleet solutions.

Public Utility Vehicle Modernization Program

The government’s comprehensive public utility vehicle modernization program is generating substantial replacement demand for commercial passenger transport vehicles across the Philippines. The initiative mandates the phaseout of aging public utility vehicles that fail to meet updated emission and safety standards, compelling transport cooperatives and operators to invest in modern, compliant alternatives. This nationwide program is creating significant procurement volumes for modern jeepneys, minibuses, and medium-duty passenger transport vehicles equipped with improved engines, enhanced passenger safety features, and accessible design configurations. According to reports, the Development Bank of the Philippines (DBP) granted a ₱60.8 million loan to the Mandaluyong Transport Service Cooperative for 30 modern public utility vehicles under its PASADA financing program, helping cooperatives acquire safer, environment‑friendly units aligned with the modernization mandate. The transition from individual operator models to cooperative-based fleet management is professionalizing the sector and encouraging larger-scale vehicle purchases. Financial support mechanisms, including government-backed loans and manufacturer financing programs, are facilitating the transition and ensuring that commercial vehicle manufacturers benefit from this structural transformation of the Philippines’ public transportation system.

Market Restraints:

What Challenges the Philippines Commercial Vehicles Market is Facing?

High Vehicle Acquisition and Financing Costs

The significant upfront cost of commercial vehicles, particularly modern and emission-compliant models, poses a substantial barrier to market expansion in the Philippines. Many small and medium-sized fleet operators and individual transport entrepreneurs face challenges in securing affordable financing, with stringent credit requirements and high interest rates limiting their ability to invest in newer vehicles. This financial burden slows fleet renewal cycles and constrains the adoption of advanced commercial vehicle technologies across the broader market.

Archipelagic Geography and Infrastructure Gaps

The Philippines’ unique archipelagic geography, comprising over seven thousand islands, creates significant logistical complexities for commercial vehicle distribution, servicing, and utilization. Poor road conditions in rural and remote areas, limited maintenance facility coverage, and uneven infrastructure development across regions affect vehicle performance and increase operating costs. These geographic challenges restrict the efficient deployment of commercial vehicles outside major urban centers and hinder the development of comprehensive national logistics networks.

Regulatory Compliance and Operational Complexities

Evolving emission standards, safety regulations, and franchise requirements add layers of compliance complexity and cost to commercial vehicle ownership and operation in the Philippines. Transport operators must navigate changing regulatory frameworks, including franchise consolidation requirements and modernization mandates, which create uncertainty and financial strain. The absence of uniform implementation timelines and support mechanisms across different regions further complicates strategic fleet planning and investment decisions for commercial vehicle operators.

Competitive Landscape:

The Philippines commercial vehicles market is characterized by a dynamic and increasingly competitive environment, with established international manufacturers maintaining strong market positions while new entrants introduce innovative product offerings. Market participants are expanding their dealer networks, enhancing after-sales service capabilities, and diversifying their vehicle portfolios to address the evolving requirements of fleet operators, logistics companies, and public transport cooperatives. Competition is intensifying across all vehicle segments, with manufacturers differentiating through pricing strategies, financing solutions, fuel efficiency improvements, and the introduction of electrified commercial vehicle models. Local assembly operations are becoming an important competitive advantage, enabling manufacturers to offer more competitively priced products while supporting domestic employment and industrial development. Strategic partnerships with financial institutions and logistics technology providers are further strengthening the market positioning of key players across the commercial vehicle value chain.

Recent Developments:

-

In Augst 2025, Foton Motor Philippines unveiled a comprehensive range of 100% electric commercial vehicles for logistics and transport at its “EV Forward” event in Clark Freeport, advancing sustainable mobility in the country.

Philippines Commercial Vehicles Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Vehicle Types Covered |

Light Commercial Vehicle, Medium and Heavy-duty Commercial Vehicle |

|

Propulsion Types Covered |

IC Engine, Electric Vehicle |

|

End Uses Covered |

Industrial, Mining and Construction, Logistics, Passenger Transportation, Others |

|

Regions Covered |

Luzon, Visayas, Mindanao |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Philippines Commercial Vehicles Market Report

The Philippines commercial vehicles market size was valued at USD 17,206.37 Million in 2025.

The Philippines commercial vehicles market is expected to grow at a compound annual growth rate of 3.24% from 2026-2034 to reach USD 22,935.22 Million by 2034.

Light commercial vehicles, holding the largest share of 58.4%, remain the dominant segment driven by strong demand from small and medium enterprises, expanding e-commerce logistics, and urban distribution networks across the Philippines.

Key factors driving the Philippines commercial vehicles market include accelerating infrastructure development under the government’s flagship program, rapid e-commerce expansion driving logistics vehicle demand, public utility vehicle modernization mandates, growing urbanization, and increasing inter-island trade volumes.

Major challenges include high vehicle acquisition and financing costs, logistical complexities arising from the archipelagic geography, infrastructure gaps in rural and remote areas, evolving regulatory compliance requirements, and limited charging infrastructure for electric commercial vehicles.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade