Philippines Confectionery Market Size, Share, Trends and Forecast by Product Type, Age Group, Price Point, Distribution Channel, and Region, 2026-2034

Philippines Confectionery Market Overview:

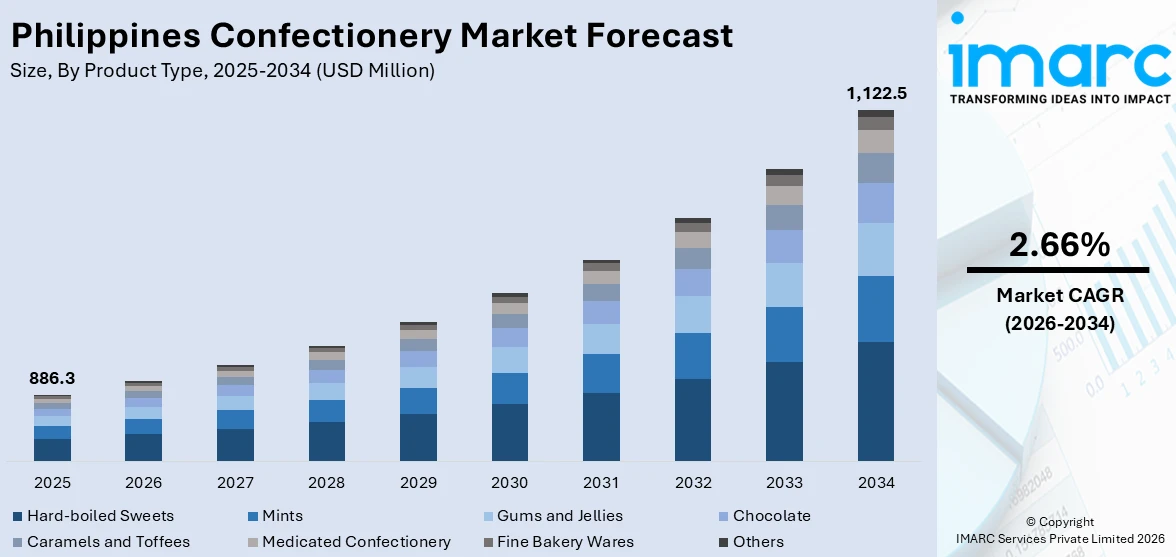

The Philippines confectionery market size reached USD 886.3 Million in 2025. Looking forward, the market is expected to reach USD 1,122.5 Million by 2034, exhibiting a growth rate (CAGR) of 2.66% during 2026-2034. The Philippines confectionery market share is expanding, driven by the rising popularity of foreign brands, which is encouraging local manufacturers to develop and introduce innovative and flavorful products, along with the expansion of retail channels and online marketplaces that assist in making confectionery items more accessible and improving their sales in the country.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 886.3 Million |

| Market Forecast in 2034 | USD 1,122.5 Million |

| Market Growth Rate 2026-2034 | 2.66% |

Key Trends of Philippines Confectionery Market:

Growing foreign brand influence

The rising foreign brand influence is offering a favorable Philippines confectionery market outlook. Imported sweets, especially chocolates and candies from big brands are hugely popular and often seen as a premium choice. Filipinos are drawn to these international brands because of their reputation for quality and unique flavors. Many people associate these foreign brands with a special treat or gift, which drives the demand for confectionery items during holidays or special occasions. As international brands expand into the Philippines, they bring new trends and products that entice Filipinos, ranging from novelty snacks to limited-edition flavors. In November 2024, Venchi, the Italian chocolatier and gelato producer, launched its initial store in Bonifacio Global City (BGC), Philippines, as it sought to meet the rising user demand. Venchi's stores in the Philippines intended to offer its chocolate bars along with more than 12 varieties of its gelato. Apart from this, social media platforms also help develop the preference for these products, with influencers and online ads introducing the latest imported treats. Moreover, the popularity of these foreign brands encourages local confectionery companies to innovate and create new and competitive items.

To get more information on this market Request Sample

Expansion of retail and e-commerce stores

The expansion of retail and e-commerce stores is impelling the Philippines confectionery market growth. In September 2024, Roberto Claudio, the President of the Philippine Retailers Association (PRA), informed reporters during the National Retail Conference and Export 2024 event, which ended on August 30, that the retail sector's contribution to the nation’s GDP could rise to 20% in 2024 or by early 2025, above from 18.6% in 2022. With convenience stores, supermarkets, and specialty shops opening up, people can easily buy chocolates, candies, and other sweet treats anytime they want. These stores play an important role in keeping confectionery products within reach for daily snacking. At the same time, online shopping platforms make it easier to purchase sweets without leaving home. Many brands offer exclusive online deals, discounts, and bundle promos, encouraging people to shop digitally. The rise of cashless payments and fast delivery services also make online purchases convenient. Social media ads and influencer promotions further increase sales by creating trends around new and imported confectionery items. Moreover, small and local confectionery businesses benefit since they can sell their products nationwide without needing a physical store. As both physical and online retail spaces continue to broaden, the variety of available confectionery items grows, giving individuals more choices and making sweets a bigger part of everyday life in the Philippines.

Growth Drivers of Philippines Confectionery Market:

Rising Middle Class, Urbanization, and Changing Lifestyle

A key growth driver in the Philippines confectionery market is the growing middle class and continued urbanization. When Filipinos live in urban areas such as Metro Manila, Cebu, and Davao, lifestyles change, as individuals work longer hours, travel further to and from work, and are looking for convenient indulgences. This is expressed in higher demand for snackable sweets, ready‑to‑eat confectioneries, and brand names that assure quality and status. Furthermore, as incomes increase, consumers are inclined to spend on luxury or imported confectionery types instead of accepting plain sugar candies. Urban retailing formats like malls, convenience stores, supermarkets, are expanding and reaching consumers. In addition, younger consumers, such as students and young adults, are exposed to international tastes through foreign travel, social media, and the digital web, so their tastes move toward novelty, international brands, international flavor, and high-end packaging. All of this pushes confectionery businesses toward more differentiated product portfolios and aggressive branding.

Cultural Traditions, Gifting, Occasions, and Local Flavor Preferences

Confectionery in the Philippines is closely linked to cultural ceremonies, festivals, and social practices, which serve as regular demand generators. Sweet foods are not merely eaten on a daily basis, yet are also at the center of celebrations, fiestas, holidays, birthdays, weddings, baptisms, and offering to guests. The gifting and hospitality culture ensure that well-packaged chocolates, novelty sweets, and artisan confectionery occupy spaces in markets that go beyond mere consumption. Additionally, the use of local flavors matters: Filipinos prefer native ingredients such as ube (purple yam), coconut, and local citrus fruits like calamansi, which are being used more often in confectioneries to produce chocolates representative of national identity. Cacao-producing regions (e.g. Davao) are becoming suppliers of single‑origin or bean‑to‑bar chocolate, appealing both to locals and tourists. The native sweet traditions like pastillas, polvorón, tablea chocolate, etc., also maintains demand for variations of sugar confections and fosters innovation at the interface of tradition and contemporary presentation, which also increases the Philippines confectionery market demand.

Distribution Expansion, Innovation, and Health Trends

A further force is the fast expansion of distribution networks, particularly e-commerce, social commerce, and modern retail, and the innovation that facilitates this, coupled with increasing health awareness among consumers. Since most islands and provinces are spread out, local retailers and manufacturers are using online platforms to circumvent the constraints of physical logistics to reach even distant or rural customers. Digital payment infrastructure, expedited delivery services, and social media advertising enable new product introductions and limited‑quantity or impulse products (innovative flavors, high‑visibility packaging) to be made widely known rapidly. Simultaneously, as consumers increasingly worry about sugar consumption, nutrition labeling, and health, there is increasing demand for "better-for-you" products: reduced sugar sweets, functionally formulated confectioneries, or cleaner, more natural ingredients. Local manufacturers are responding with formulations cutting sugar, adding dairy or fruit, and packaging appealing to consumers who are concerned about ingredient origin or sustainability. According to the Philippines confectionery market analysis, this thrust toward healthier indulgence, coupled with product and flavor innovation, provides opportunities for premium pricing and differentiation.

Philippines Confectionery Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the regional level for 2026-2034. Our report has categorized the market based on product type, age group, price point, and distribution channel.

Product Type Insights:

- Hard-boiled Sweets

- Mints

- Gums and Jellies

- Chocolate

- Caramels and Toffees

- Medicated Confectionery

- Fine Bakery Wares

- Others

The report has provided a detailed breakup and analysis of the market based on the product types. This includes hard-boiled sweets, mints, gums and jellies, chocolate, caramels and toffees, medicated confectionery, fine bakery wares, and others.

Age group Insights:

- Children

- Adult

- Geriatric

A detailed breakup and analysis of the market based on the age groups have also been provided in the report. This includes children, adult, and geriatric.

Price Point Insights:

- Economy

- Mid-range

- Luxury

The report has provided a detailed breakup and analysis of the market based on the price points. This includes economy, mid-range, and luxury.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

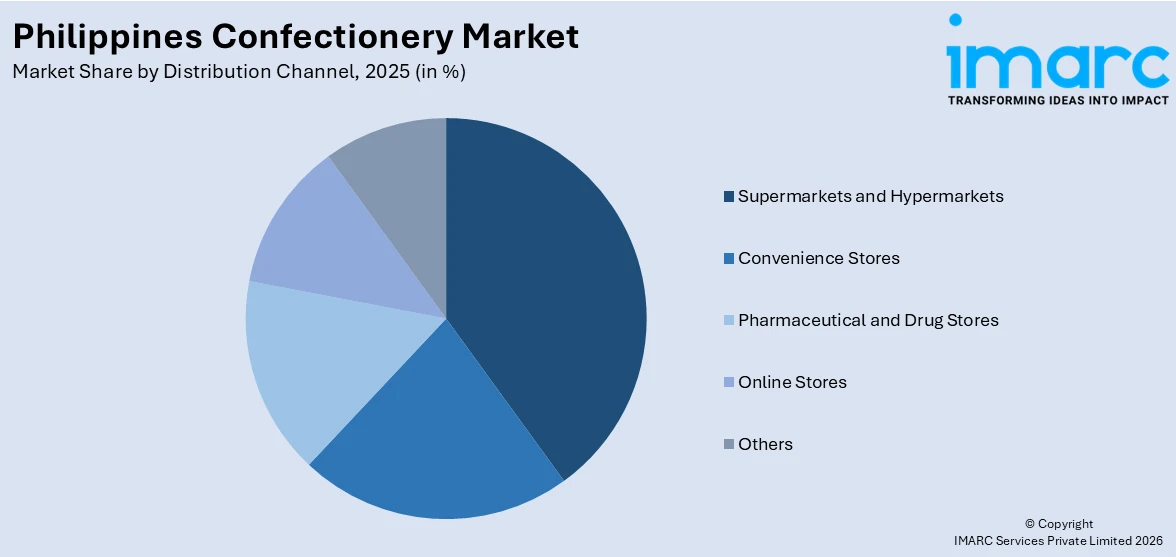

- Supermarkets and Hypermarkets

- Convenience Stores

- Pharmaceutical and Drug Stores

- Online Stores

- Others

A detailed breakup and analysis of the market based on the distribution channels have also been provided in the report. This includes supermarkets and hypermarkets, convenience stores, pharmaceutical and drug stores, online stores, and others.

Regional Insights:

- Luzon

- Visayas

- Mindanao

The report has also provided a comprehensive analysis of all the major regional markets, which include Luzon, Visayas, and Mindanao.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Philippines Confectionery Market News:

- In July 2024, the Hershey Company launched Hershey's Choco Balls in the Philippines. These creamy chocolates filled with crunchy cookie pieces were crafted to attract snack enthusiasts nationwide. They come in two varieties, ‘Cookies N Crème (white)’ and ‘Cookies N Chocolate (milk) with enhanced flavors.

- In June 2024, GLOBAL BRAND Glico, based in Osaka, aimed to expand sales of its confectionery and health food products beyond its home country, Japan. In the Philippines, where Glico operates an office, the company planned to introduce a broader selection of items under the Almond Koka brand in June.

Philippines Confectionery Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Hard-boiled Sweets, Mints, Gums and Jellies, Chocolate, Caramels and Toffees, Medicated Confectionery, Fine Bakery Wares, Others |

| Age groups Covered | Children, Adult, Geriatric |

| Price Points Covered | Economy, Mid-range, Luxury |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Pharmaceutical and Drug Stores, Online Stores, Others |

| Regions Covered | Luzon, Visayas, Mindanao |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Philippines confectionery market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Philippines confectionery market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Philippines confectionery industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Philippines Confectionery Market Report

The Philippines confectionery market reached a value of USD 886.3 Million in 2025.

The market is projected to grow at a CAGR of 2.66% during 2026-2034, reaching USD 1,122.5 Million by 2034.

Key growth drivers include rising middle-class incomes, accelerating urbanization, deep-rooted cultural gifting traditions, rapid expansion of retail networks, and health-conscious product innovation.

The report covers segmentation by product type, age group, price point, distribution channel, and region. Each segment includes detailed market size and forecast analysis.

Key trends include rising foreign brand influence, rapid e-commerce proliferation, social media-driven consumption, local flavor innovation, and premiumization of confectionery offerings.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)