Philippines Dairy Market Report by Product Type (Liquid Milk, Flavored Milk, Cream, Butter, Cheese, Yoghurt, Ice Cream, Anhydrous Milk Fat (AMF), Skimmed Milk Powder (SMP), Whole Milk Powder (WMP), Whey Protein, Lactose Powder, Curd, and Others), and Region 2026-2034

Philippines Dairy Market Overview:

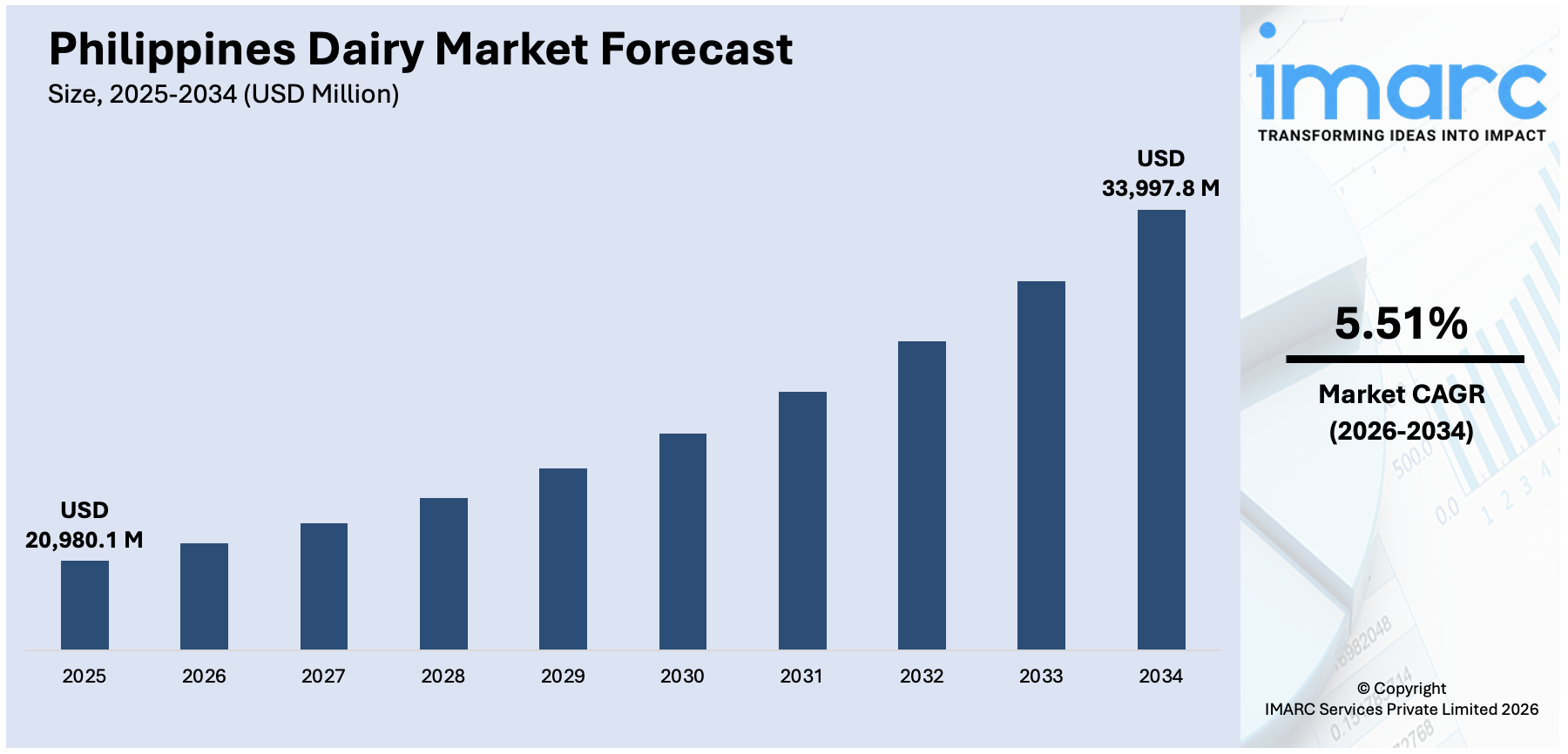

The Philippines dairy market size reached USD 20,980.1 Million in 2025. Looking forward, the market is expected to reach USD 33,997.8 Million by 2034, exhibiting a growth rate (CAGR) of 5.51% during 2026-2034. The increasing demand for nutritious and diverse dairy products, rapid urbanization, increasing disposable incomes, enhanced retail infrastructure, government initiatives supporting local dairy production, and expanding health consciousness among consumers are some of the major factors propelling the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 20,980.1 Million |

|

Market Forecast in 2034

|

USD 33,997.8 Million |

| Market Growth Rate 2026-2034 | 5.51% |

Key Trends of Philippines Dairy Market:

Rising Need for Nutritious and Protein-Rich Foods

The growing demand for nutritious and protein-rich foods among consumers is acting as a major growth-inducing factor. Dairy products such as milk, cheese, yogurt, and butter are increasingly favored for their health benefits, contributing significantly to market growth. According to the Food and Agricultural Organization (FAO), protein-energy malnutrition (PEM) and micronutrient deficiencies remain the leading nutritional problems in the Philippines. The general declining trend in the prevalence of underweight, stunting, and wasting among Filipino children noted in the past 10 years was countered by the increase in the prevalence rate in 1998. About 4 million (31.8%) of the preschool population were found to be underweight for age, 3 million (19.8%) adolescents and 5 million (13.2%) adults, including older persons were found to be underweight and chronically energy deficient, respectively.

To get more information on this market Request Sample

Growing Urbanization and Lifestyle Changes

Rapid urbanization in the Philippines is leading to lifestyle changes, with more consumers opting for convenient and ready-to-consume dairy products. The urban population tends to have higher disposable incomes and a preference for diverse and convenient food options, including dairy. According to the Asian Development Bank, the importance of cities in national development is expected to increase as the country continues to urbanize. As of 2015, 51.2% of Filipinos were already residing in urban areas. They are spread in over 7,437 urban barangays out of the country’s then total of 42,036 barangays. Overall, 67.12% of the population in all cities throughout the country are living in urban areas. From 2010 to 2020, the total population in all 146 cities nationwide has increased by 19.27%, on average. Along with the increase in the number of urban dwellers is the rise in the number of cities throughout the country over the years.

Growth Drivers of Philippines Dairy Market:

Expanding Food Service and Retail Sectors

The flourishing food service industry, encompassing quick-service restaurants, coffee shops, and bakeries, is substantially driving dairy consumption across the Philippines. The proliferation of international fast-food chains and local eateries has created consistent demand for cheese, butter, cream, and other dairy ingredients essential for menu offerings. The coffee shop segment particularly demonstrates remarkable growth, with establishments in Metro Manila and provincial cities requiring fresh milk daily for beverages. This expanding foodservice infrastructure, coupled with growing consumer dining-out habits and premium café culture, continues to accelerate dairy product uptake, thereby strengthening market fundamentals and creating sustained growth momentum.

Rising Disposable Incomes and Middle-Class Expansion

Growing household incomes and the expanding middle-class population are fundamentally transforming dairy consumption patterns throughout the Philippines. As economic prosperity increases, Filipino families allocate larger portions of their budgets toward nutritious food products, including premium dairy items. This demographic shift is particularly evident in urban centers where consumers increasingly purchase imported cheese varieties, Greek yogurt, flavored milk beverages, and specialty dairy products that were previously considered luxury items. The correlation between income growth and dairy consumption is well-established, with higher-earning households demonstrating significantly greater per capita dairy intake. This economic trajectory, supported by remittances from overseas Filipino workers and robust domestic economic activity, ensures the sustained expansion of the Philippines dairy market growth.

Government Milk Feeding Programs and Educational Initiatives

Government-mandated nutrition programs, particularly the School-Based Feeding Program (SBFP) implemented by the Department of Education, significantly boost dairy consumption among Filipino children. These institutional programs distribute milk to preschoolers and malnourished school-aged children, creating substantial demand for liquid milk products. Republic Acts 11037 and 11148 have institutionalized milk feeding initiatives, requiring regular procurement of dairy products for educational and nutrition programs nationwide. The Department of Education prioritizes locally produced dairy products in these programs, simultaneously addressing child malnutrition while supporting domestic dairy producers. This policy framework creates predictable demand patterns and encourages investment in local production capacity. The combination of public health objectives with market development strategies establishes a sustainable foundation for long-term industry growth.

Government Support of Philippines Dairy Market:

National Dairy Authority Development Programs

The National Dairy Authority (NDA), established under Republic Act 7884, provides comprehensive support to accelerate the Philippine dairy industry development. The agency actively implements herd development initiatives, including the importation of dairy cattle, artificial insemination services, and the distribution of acclimatized animals to local farmers. NDA manages stock farms across multiple provinces, with five new facilities completed by the end of 2024 to expand the national dairy herd. From January to June 2024, domestic milk production increased by 15% to 16,020 metric tons, representing 21% of the country's liquid milk supply. The authority also facilitates farmer training programs, provides technical assistance on dairy husbandry practices, and coordinates with commercial processors to ensure market access for local producers, thereby creating an enabling environment for industry expansion.

Dairy Industry Roadmap 2020-2025 Implementation

The Philippine government's comprehensive dairy industry roadmap outlines strategic policies, budgetary allocations, and implementation frameworks to boost domestic milk production. This roadmap outlines a major expansion in local milk production over the next several years, driven by coordinated efforts across farming, processing, and market development. It focuses on boosting output, improving supply chain efficiency, and strengthening industry competitiveness through targeted interventions and capacity-building initiatives. The strategic plan addresses challenges, including limited dairy cattle populations, inadequate feed supply systems, and processing infrastructure gaps, which are expected to fuel the Philippines dairy market share. The roadmap also emphasizes partnerships with international dairy companies, encourages foreign direct investment, and promotes joint ventures to transfer advanced dairy farming technologies and management systems to Filipino producers.

Investment Incentives and Foreign Partnership Facilitation

The Department of Trade and Industry (DTI), working alongside the Board of Investments (BOI), actively facilitates foreign dairy investments through streamlined regulatory processes and attractive incentive packages. Such initiatives involve whole-of-government approaches, with DTI coordinating business-to-business introductions, the Department of Agriculture identifying suitable land locations, and regulatory bodies ensuring clear labeling standards for fresh milk, UHT milk, and imported products. These coordinated efforts aim to attract substantial capital investments, technology transfers, and expertise that will significantly enhance local production capacity while advancing the nation's goal of dairy self-sufficiency.

Opportunity of Philippines Dairy Market:

Premium and Functional Dairy Product Development

Increasing health consciousness among Filipino consumers presents significant opportunities for premium dairy offerings, including probiotic yogurts, organic milk, lactose-free alternatives, and calcium-fortified products. Urban consumers, particularly millennials and Generation Z, actively seek functional foods that provide specific health benefits beyond basic nutrition. This trend creates market space for innovative dairy products addressing digestive health, bone strength, immune support, and weight management. Manufacturers can capitalize on this demand by developing localized product formulations that cater to Filipino taste preferences while incorporating functional ingredients. The premiumization trend also extends to artisanal cheese production, with small-scale producers creating gourmet cheese varieties using local milk. This segment offers attractive profit margins and differentiation opportunities for both domestic and international dairy companies entering the Philippine market.

E-commerce and Direct-to-Consumer Distribution Channels

The rapid digitalization of retail presents transformative opportunities for Philippines dairy market demand expansion through online platforms and direct delivery models. E-commerce penetration in the Philippines continues to accelerate, with consumers increasingly purchasing groceries, including perishable dairy products, through mobile apps and websites. This channel enables dairy producers and retailers to reach consumers in underserved provincial areas where traditional retail infrastructure remains limited. Direct-to-consumer models allow dairy farms to establish premium positioning, build brand loyalty, and capture higher margins by eliminating intermediaries. Subscription-based milk delivery services, farm-to-table concepts, and specialized online marketplaces for artisanal dairy products represent untapped potential. The integration of cold-chain logistics with digital platforms enables reliable delivery of fresh dairy products, thereby expanding market reach and creating new revenue streams.

Value-Added Processing and Export Market Development

The development of value-added dairy processing capabilities offers substantial opportunities for market growth and export potential. While the Philippines currently imports 99% of its dairy requirements, strategic investments in processing infrastructure can convert local raw milk into higher-value products such as specialty cheeses, yogurt cultures, whey proteins, and dairy-based ingredients for food manufacturing. The expertise gained from international partnerships, particularly with established dairy nations, can be leveraged to achieve export quality standards. Regional markets in Southeast Asia present viable export destinations for Philippine-produced dairy products, particularly those incorporating tropical flavors and formulations suited to Asian palates. Government export promotion programs, combined with improved production volumes from expanded herds, create conditions for transforming the Philippines from a net importer to a regional dairy player.

Challenges of Philippines Dairy Market:

Limited Domestic Production Capacity and Import Dependence

The Philippines faces a deep structural challenge in its dairy sector, as local production supplies only a very small share of the country’s overall needs. With limited herd size, low productivity, and underdeveloped farming systems, domestic output remains far below national consumption requirements. As a result, the country depends heavily on imported dairy products to meet demand, relying on major global producers such as New Zealand, the United States, and Australia. This dependence underscores long-standing gaps in local capacity, investment, and technology within the dairy industry. The limited production capacity stems from insufficient dairy cattle populations, as these animals are non-native to the tropical Philippines. Expanding local production requires substantial capital investments in importing breeding stock, developing climate-controlled facilities, and establishing feed production systems. According to the Philippines dairy market analysis, the country's heavy import dependence also exposes the dairy sector to international price fluctuations, supply chain disruptions, and foreign exchange rate volatility.

Climate and Land Use Constraints

Tropical climatic conditions and rapid urbanization present significant obstacles to dairy farming expansion in the Philippines. Dairy cattle, predominantly Holstein-Friesian breeds, perform optimally in temperate climates and require climate-controlled environments to maintain productivity in Philippine conditions. Heat stress reduces milk yields, increases animal mortality rates, and necessitates expensive cooling infrastructure that many small-scale farmers cannot afford. Additionally, the steady conversion of agricultural areas into commercial and residential developments has sharply reduced the land available for grazing. This ongoing decline in pastureland restricts opportunities to establish or expand dairy farms. Seasonal weather extremes and limited feed production infrastructure further strain herd nutrition, making it difficult for farmers to maintain healthy and productive animals year-round.

Price Competition from Low-Cost Imports

Local dairy producers face intense price competition from imported dairy products, particularly powdered milk and UHT products that benefit from economies of scale in major dairy-producing nations. International suppliers can offer products at prices that Filipino farmers struggle to match, given their smaller operational scales, higher production costs, and limited processing infrastructure. Imported UHT milk enjoys extended shelf life advantages and distinctive taste profiles that many Filipino consumers prefer. The price differential between local fresh milk and imported alternatives creates market access challenges for domestic producers, despite government preferences for local products in feeding programs. Mislabeling practices, where some products blur distinctions between fresh milk and reconstituted milk, further complicate fair market competition. Establishing regulatory frameworks that level the playing field while maintaining consumer access to affordable dairy products remains an ongoing challenge requiring careful policy balancing.

Philippines Dairy Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country level for 2026-2034. Our report has categorized the market based on product type.

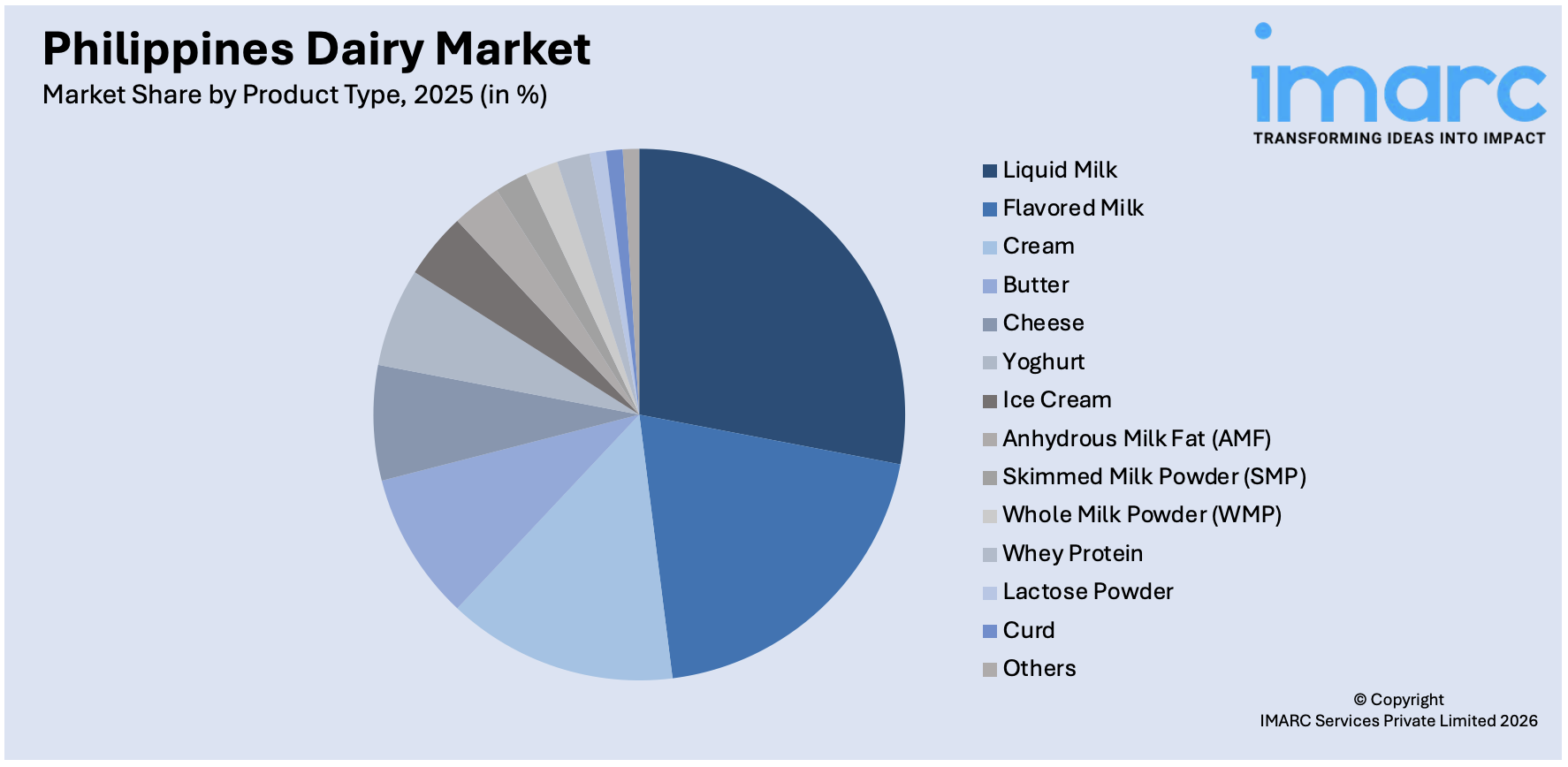

Product Type Insights:

Access the comprehensive market breakdown Request Sample

- Liquid Milk

- Flavored Milk

- Cream

- Butter

- Cheese

- Yoghurt

- Ice Cream

- Anhydrous Milk Fat (AMF)

- Skimmed Milk Powder (SMP)

- Whole Milk Powder (WMP)

- Whey Protein

- Lactose Powder

- Curd

- Others

The report has provided a detailed breakup and analysis of the market based on the product type. This includes liquid milk, flavored milk, cream, butter, cheese, yoghurt, ice cream, anhydrous milk fat (AMF), skimmed milk powder (SMP), whole milk powder (WMP), whey protein, lactose powder, curd, and others.

Region Insights:

- Luzon

- Visayas

- Mindanao

The report has also provided a comprehensive analysis of all the major regional markets, which include Luzon, Visayas, and Mindanao.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Philippines Dairy Market News:

- In May 2024, Department of Trade and Industry (DTI) Secretary Fred Pascual engaged with officials of Baladna to discuss their potential investment in establishing a large-scale, fully integrated dairy facility in the Philippines. He cited that this strategic investment aligns with the country’s pursuit of self-sufficiency in food and milk production.

- In March 2024, Qatar’s largest livestock and dairy producer, the Baladna Qatar Public Shareholding Company, announced that it is seeking business partners for its ventures in the Philippines. The Philippine Chamber of Commerce and Industry (PCCI) newsletter released on Friday said Baladna is searching for partners for its ventures here – the Safe Innovation Hub and Mariculture Park in Sual, Pangasinan; General Santos City Agro-Industrial Hub; Cotabato Agro-Industrial Park; and South Cotabato Integrated Food Terminal.

Philippines Dairy Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Liquid Milk, Flavored Milk, Cream, Butter, Cheese, Yoghurt, Ice Cream, Anhydrous Milk Fat (AMF), Skimmed Milk Powder (SMP), Whole Milk Powder (WMP), Whey Protein, Lactose Powder, Curd, Others |

| Regions Covered | Luzon, Visayas, Mindanao |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Philippines dairy market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Philippines dairy market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Philippines dairy industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Philippines Dairy Market Report

The dairy market in the Philippines was valued at USD 20,980.1 Million in 2025.

The Philippines dairy market is projected to exhibit a CAGR of 5.51% during 2026-2034.

The Philippines dairy market is projected to reach a value of USD 33,997.8 Million by 2034.

The market demonstrates strong growth driven by rising nutritional awareness, urbanization-led lifestyle changes favoring convenient dairy products, and expanding food service sectors. Health-conscious consumers increasingly seek protein-rich dairy offerings to address nutritional deficiencies. Rapid urban population growth with higher disposable incomes fuels demand for diverse dairy products including premium and functional offerings across metropolitan and emerging provincial markets.

The Philippines dairy market is driven by expanding food service sectors including quick-service restaurants and coffee shops requiring dairy ingredients, rising middle-class incomes enabling premium product purchases, and government-mandated school milk feeding programs. Urbanization patterns, increased café culture, international fast-food chain proliferation, and institutionalized nutrition initiatives for children collectively accelerate consumption. Strategic foreign investments and technology transfers further strengthen production capabilities and market expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)