Philippines Electric Vehicle Charging Station Market Size, Share, Trends and Forecast by Charging Station Type, Vehicle Type, Installation Type, Charging Level, Connector Type, Application, and Region, 2026-2034

Philippines Electric Vehicle Charging Station Market Size, Share, Trends & Forecast (2026-2034)

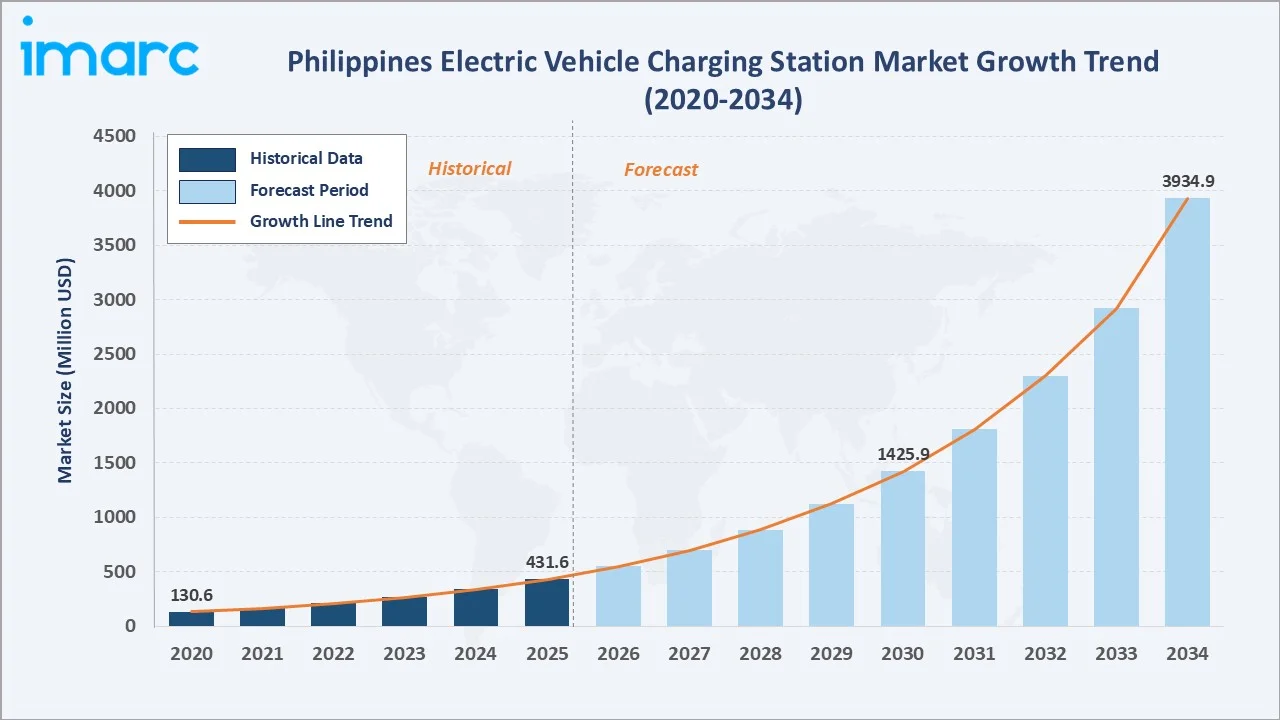

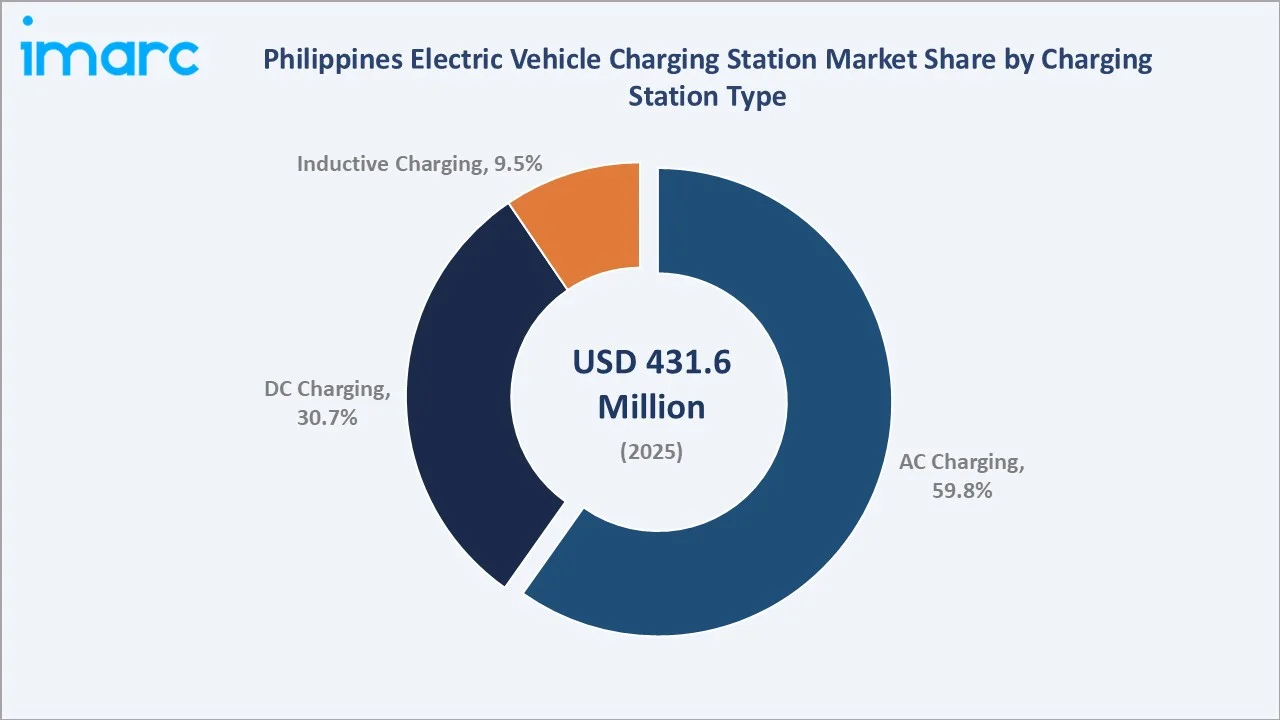

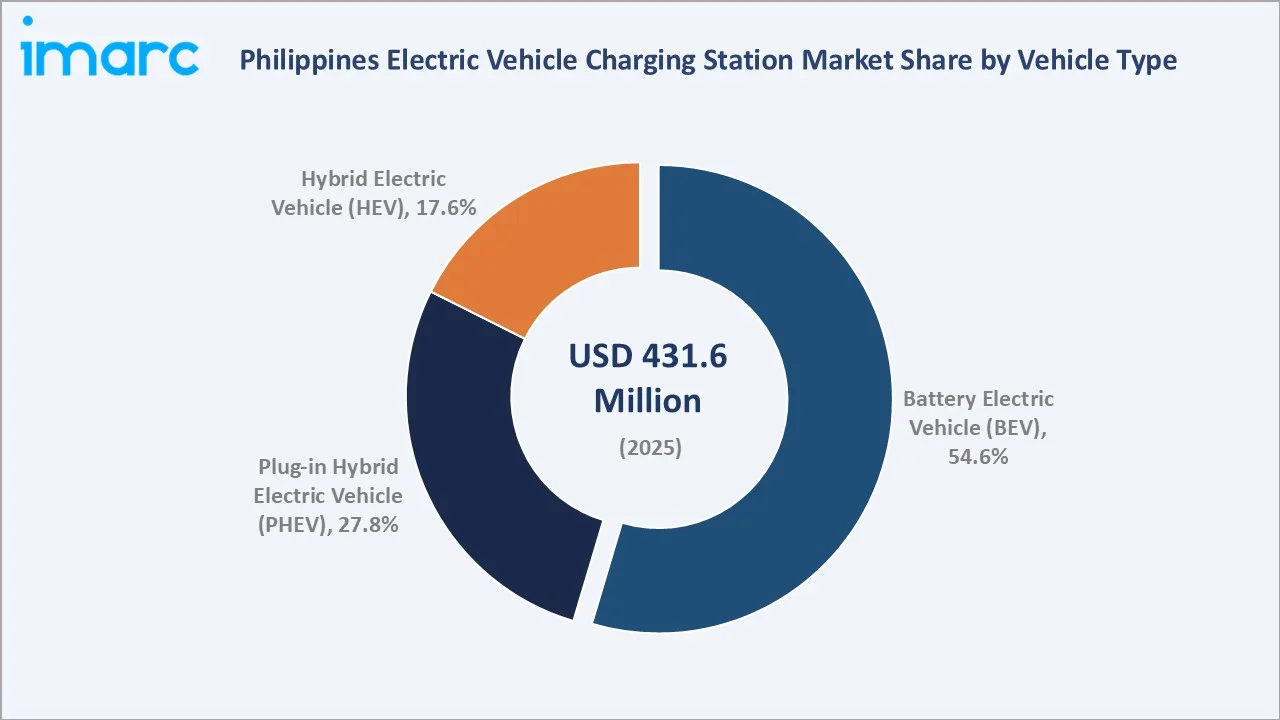

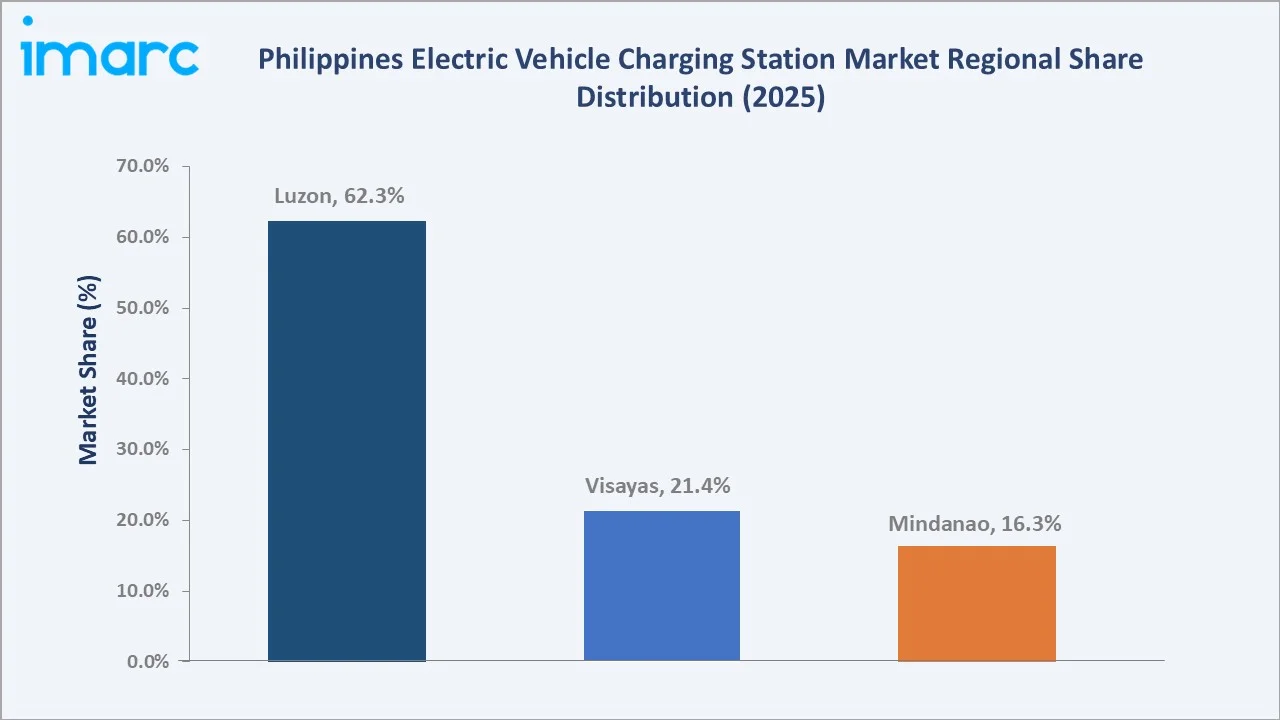

The Philippines electric vehicle charging station market was valued at USD 431.6 Million in 2025 and is projected to reach USD 3,934.9 Million by 2034, exhibiting a CAGR of 27.00% during 2026-2034. Rising electric vehicle adoption, strong policy support, surging urbanization in Metro Manila and key provincial hubs, and accelerating deployment of DC fast chargers are the primary drivers shaping the market growth.

AC charging leads the charging station type segment at 59.8%, battery electric vehicle (BEV) dominates the vehicle type segment at 54.6%, and Luzon commands 62.3% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 431.6 Million |

|

Forecast Market Size (2034) |

USD 3934.9 Million |

|

CAGR (2026-2034) |

27.00% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Luzon (62.3%, 2025) |

|

Second Largest Region |

Visayas (21.4%, 2025) |

|

Leading Charging Station Type |

AC Charging (59.8%, 2025) |

|

Leading Vehicle Type |

Battery Electric Vehicle – BEV (54.6%, 2025) |

The Philippines electric vehicle charging station market expanded from USD 130.6 Million in 2020 to USD 431.6 Million in 2025, anchored by EVIDA-driven infrastructure mandates, growing Japanese and Korean automaker electric vehicle launches tailored for the Philippines market, and expanding digital payment integration at charging points. Grounded at USD 1425.9 Million in 2030, the forecast to USD 3934.9 Million by 2034 is supported by accelerating DC fast charger rollout along the expressway network, fleet electrification by logistics and ride-hailing operators, and deepening private sector participation in charging network ownership.

To get more information on this market, Request Sample

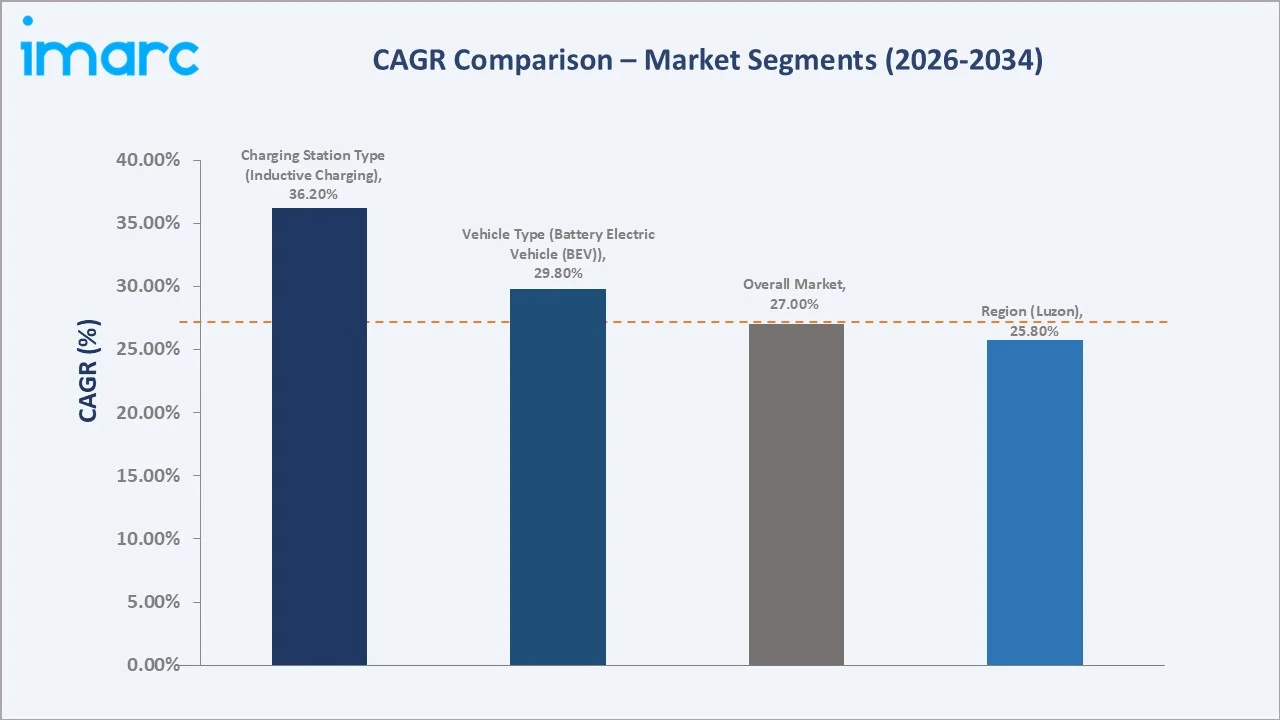

CAGR trajectories across charging station type and vehicle type sub-segments show DC charging and inductive charging expanding faster than the overall 27.00% market CAGR, driven by highway charging demand, fleet operators, and growing consumer preference for faster charge cycles.

Executive Summary

The Philippines electric vehicle charging station market is on a strong growth trajectory from USD 130.6 Million in 2020 to USD 3934.9 Million by 2034. The segment has rapidly transitioned from a nascent, developer-led pilot phase to a policy-mandated, commercially driven infrastructure buildout across commercial real estate, transport hubs, and expressway corridors.

AC charging dominates the charging station type segment at 59.8% in 2025, supported by lower installation costs, compatibility with residential and commercial building electrical systems, and suitability for overnight and workplace charging scenarios. Battery electric vehicle (BEV) leads the vehicle type segment at 54.6%, fueled by expanding model availability and growing consumer preference for fully electric transportation. In May 2026, Green SM (Green Smart Mobility) revealed it entered into MOUs and deposit agreements with 75 transportation firms and cooperatives in the Philippines, intending to launch a shared fleet of as many as 18,497 VinFast BEVs for passenger transport throughout the nation by the end of the year. Luzon commands 62.3% of regional market share, propelled by its high urbanization rate and ongoing investments in public and private charging infrastructure.

Key Market Insights

|

Insight |

Data |

|

Leading Charging Station Type |

AC Charging – 59.8% share (2025) |

|

Second Largest Charging Station Type |

DC Charging – 30.7% share (2025) |

|

Leading Vehicle Type |

Battery Electric Vehicle (BEV) – 54.6% share (2025) |

|

Second Largest Vehicle Type |

Plug-in Hybrid Electric Vehicle (PHEV) – 27.8% share (2025) |

|

Leading Region |

Luzon – 62.3% share (2025) |

|

Second Largest Region |

Visayas – 21.4% share (2025) |

|

Top Companies |

Ayala Corporation, Delta Electronics, Inc., ABB, Schneider Electric |

Key Analytical Observations Supporting the Above Data:

- AC charging dominance at 59.8% is driven by compatibility with standard commercial and residential electrical infrastructure, lower equipment and installation costs, and suitability for overnight, workplace, and retail destination charging.

- DC charging at 30.7% is expanding rapidly as expressway corridor deployments, logistics fleet electrification, and ride-hailing operator charging hubs demand faster energy replenishment cycles. Its share is projected to increase significantly through 2034 as DC fast charger costs decline and grid capacity along national highways improves.

- Battery electric vehicle (BEV) leadership at 54.6% reflects strong consumer preference for zero-emission, fully electric drivetrains in the Philippines market, supported by a growing model lineup from Japanese and Korean automakers tailored for local road conditions and commuting patterns.

- Plug-in hybrid electric vehicle (PHEV) at 27.8% represents dual-powertrain electric vehicle adopters who value extended range alongside electric efficiency, particularly in areas with limited public charging coverage outside Metro Manila.

- Luzon at 62.3% remains the dominant region, anchored by Metro Manila and Central Luzon, which together account for a large concentration of registered electric vehicles, commercial real estate developments, and expressway infrastructure in the country.

Philippines Electric Vehicle Charging Station Market Overview

Electric vehicle charging station refers to fixed or portable infrastructure that supplies electrical energy to recharge battery-powered electric vehicles, including BEVs, PHEVs, and hybrid electric vehicles. The market encompasses AC charging units, DC fast chargers, and emerging inductive or wireless charging systems deployed across residential, commercial, retail, transport, and highway locations.

The Philippine ecosystem integrates charging equipment manufacturers, energy distribution utilities and generation companies, electric vehicle automakers and importers, network software and payment platform providers, property developers and facility operators, government regulators, and end users ranging from private electric vehicle owners to commercial fleet operators. Together, they support a rapidly expanding national charging network under the EVIDA implementation framework.

Market Dynamics

To evaluate market opportunities, Request Sample

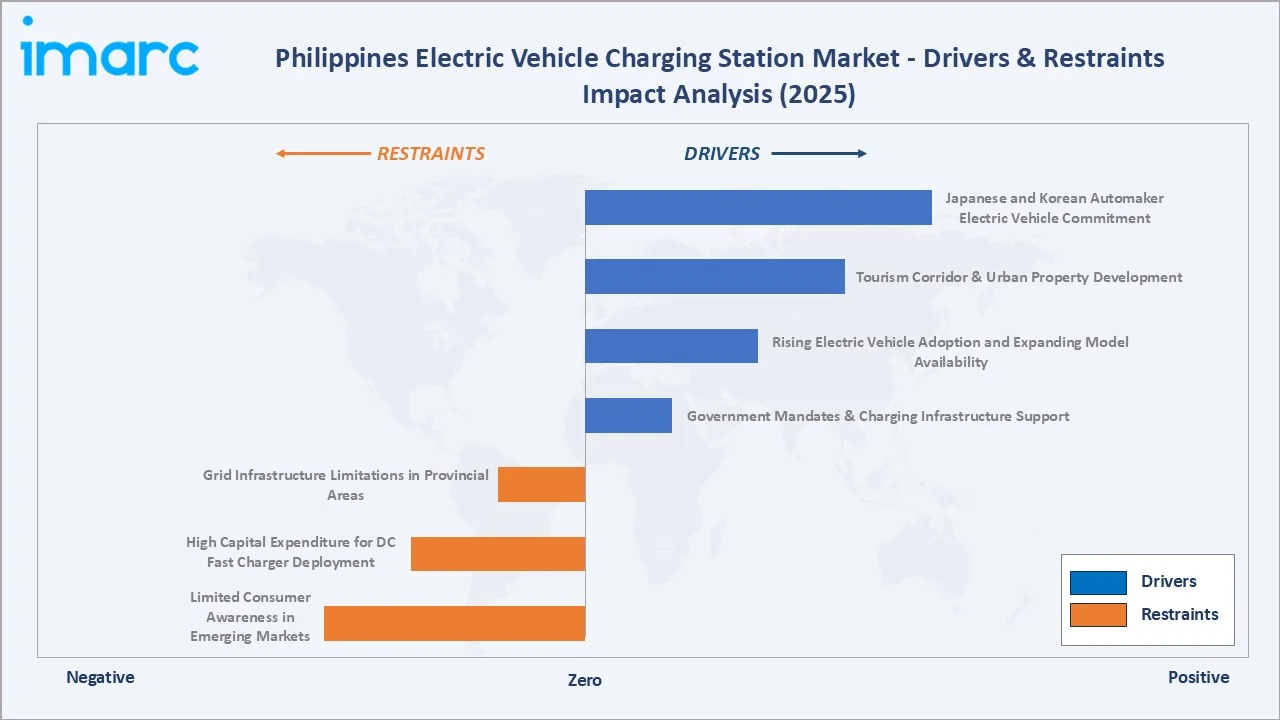

Market Drivers

- Government Mandates and Charging Infrastructure Support: Government regulations requiring the integration of electric vehicle charging facilities in commercial establishments, public institutions, and residential developments are creating a stable and long-term demand base for charging infrastructure. In addition, supportive policies, such as investment incentives, tax benefits on EV-related imports, and financial assistance for charging station deployment, are reducing investment barriers and encouraging greater participation from developers and network operators.

- Rising Electric Vehicle Adoption and Expanding Model Availability: Growing consumer access to affordable BEVs and PHEVs from key brands expanding into the domestic market is directly expanding the addressable base of electric vehicle owners requiring charging infrastructure. Sales of electric vehicles in the Philippines surged by 36% during the first quarter of 2026. Fleet operators in ride-hailing, delivery, and government transport are accelerating electrification to reduce fuel costs, further broadening demand across commercial charging use cases.

- Tourism Corridor and Urban Property Development: Property developers in Metro Manila and key tourism corridors are integrating electric vehicle charging as a value-added building amenity, driven by EVIDA compliance requirements and competitive differentiation in premium commercial and mixed-use real estate projects. The expressway network across Luzon and growing inter-city road connectivity are also creating strong demand for highway fast-charging nodes.

- Japanese and Korean Automaker Electric Vehicle Commitment to the Philippines: Major automakers with established dealer networks in the Philippines are launching electric vehicle and PHEV variants tailored for local road conditions and commuting distances. Their investment in model localization and dealer-integrated charging solutions is creating pull-through demand for branded and third-party charging infrastructure across their retail networks.

Market Restraints

- Grid Infrastructure Limitations in Provincial Areas: The Philippine power grid, particularly in the Visayas and Mindanao regions, continues to face reliability and capacity constraints that limit the feasibility of DC fast charger deployment outside major urban centers. Grid stability issues during peak demand periods and the cost of grid upgrades required to support high-power charging infrastructure create barriers to equitable national charging network expansion.

- High Capital Expenditure for DC Fast Charger Deployment: DC fast charging stations require significantly higher upfront investment than AC Level 2 units, including transformer upgrades, dedicated power feeds, and civil works. This creates a substantial capital barrier for smaller network operators and limits the pace of premium charging infrastructure rollout in secondary cities.

- Limited Consumer Awareness in Emerging Markets: Outside Metro Manila and major provincial cities, consumer familiarity with electric vehicle ownership, charging etiquette, and the location of charging stations remains low. This limits early-stage organic demand for public charging infrastructure in Mindanao and parts of the Visayas, slowing the commercial viability of network operator investments in these regions.

Market Opportunities

- Fleet Electrification and Commercial Depot Demand: Fleet electrification across ride-hailing, logistics, and public utility vehicle modernization programs creates captive demand for commercial fast-charging depots with high asset utilization rates, offering stable, recurring revenue opportunities for network operators.

- Renewable Energy-Integrated Charging Solutions: Renewable energy integration, including solar-powered charging stations at commercial and industrial facilities, presents a sustainable and cost-competitive charging model aligned with the Philippines' energy transition goals and net metering policy framework.

Market Challenges

- Interoperability and Cross-Network Roaming: Interoperability between charging equipment from different manufacturers and network software platforms remains a technical challenge that complicates the user experience and limits cross-network roaming for electric vehicle drivers across the country.

- Urban Permitting and Site Development Complexity: Land acquisition and permitting complexity for standalone charging stations in dense urban settings, including Metro Manila barangay-level coordination, adds time and cost to site deployment timelines for network operators.

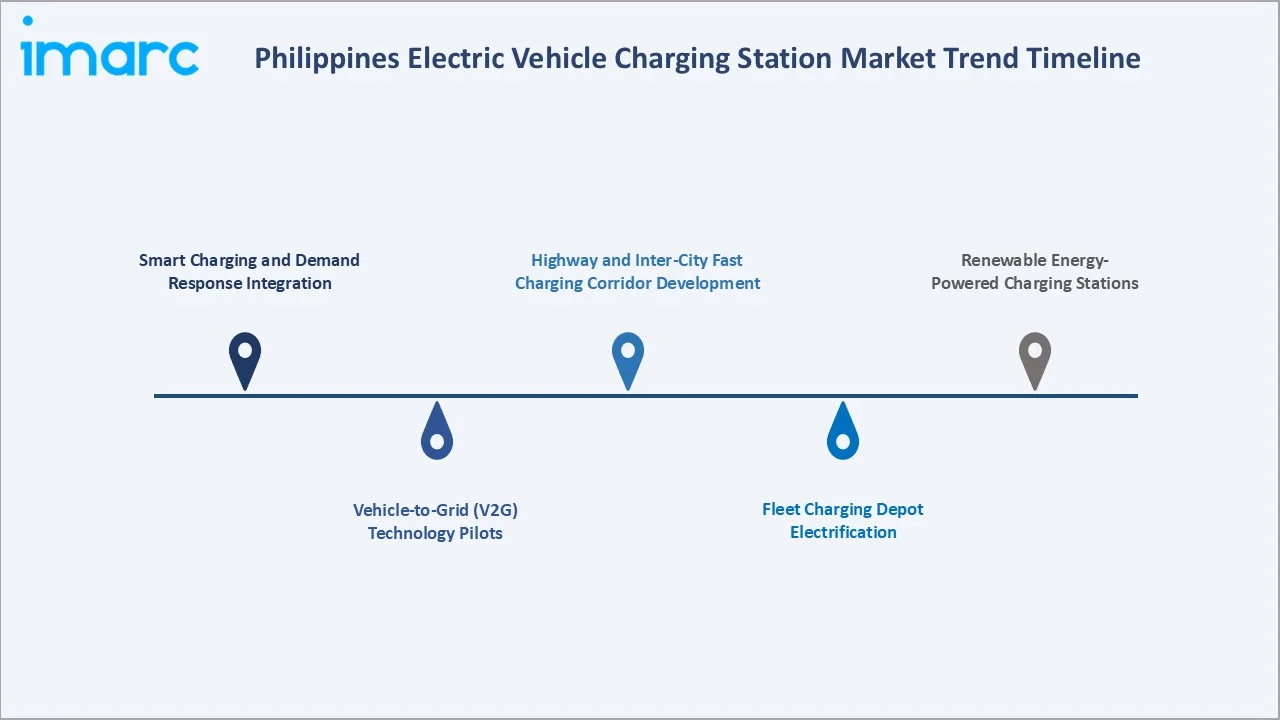

Emerging Market Trends

1. Smart Charging and Demand Response Integration

Charging station operators and energy companies are deploying smart charging management systems that enable dynamic load balancing, time-of-use tariff optimization, and remote diagnostics. These systems are increasingly being integrated with building energy management platforms and utility demand response programs, allowing operators to reduce peak demand charges and improve station profitability.

2. Vehicle-to-Grid (V2G) Technology Pilots

Early-stage V2G pilots are being explored in the Philippines in partnership with utilities, allowing compatible electric vehicles to discharge stored energy back to the grid during peak demand periods. These initiatives are helping assess the role of electric vehicles in enhancing grid stability, supporting renewable energy integration, and creating new value streams for electric vehicle owners through bidirectional charging capabilities.

3. Highway and Inter-City Fast Charging Corridor Development

Expressway operators and private charging network companies are accelerating the deployment of DC fast chargers at service areas along the North Luzon Expressway, South Luzon Expressway, and emerging Mindanao highway corridors. These highway charging nodes are critical to reducing range anxiety, enabling long-distance electric vehicle travel, and unlocking tourism-driven electric vehicle use cases that extend the addressable market beyond daily urban commuting.

4. Fleet Charging Depot Electrification

Logistics companies, ride-hailing platforms, and public utility vehicle modernization program (PUVMP) participants are investing in dedicated fleet charging depots that combine high-power AC and DC chargers, energy storage systems, and fleet management software. These integrated depot solutions are becoming a standard feature of large-scale fleet electrification contracts in the Philippines.

5. Renewable Energy-Powered Charging Stations

Solar-integrated electric vehicle charging stations are gaining commercial traction, particularly in commercial and industrial facilities where rooftop solar generation can directly offset grid electricity consumption at charging points. This trend is supported by the Philippines' net metering policy and the declining cost of solar photovoltaic systems, making solar-powered charging increasingly cost-competitive for property developers seeking to minimize charging operational costs.

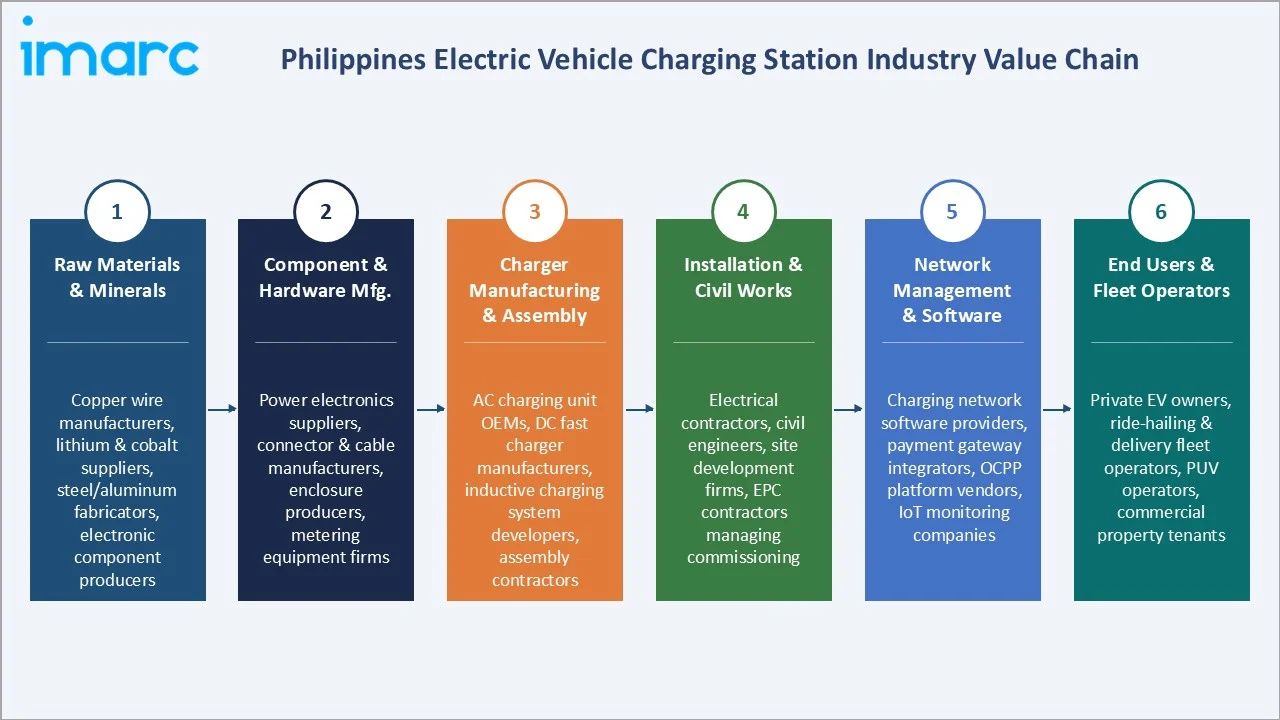

Industry Value Chain Analysis

The Philippines electric vehicle charging station value chain spans six stages from raw materials through end-user engagement and network lifecycle management. Charging equipment manufacturing, network software, and site installation and civil works capture the highest value-add, while grid connectivity and regulatory compliance increasingly determine competitive positioning for network operators.

|

Stage |

Key Players / Examples |

|

Raw Materials & Minerals |

Copper wire manufacturers, lithium and cobalt mineral suppliers, steel and aluminum fabricators, and electronic component producers supplying inputs for charging hardware |

|

Component & Hardware Manufacturing |

Power electronics suppliers, connector and cable manufacturers, enclosure producers, and metering equipment firms providing sub-components to charger OEMs |

|

Charger Manufacturing & Assembly |

AC charging unit OEMs, DC fast charger manufacturers, inductive charging system developers, and private-label assembly contractors producing finished charging equipment |

|

Installation & Civil Works |

Electrical contractors, civil engineers, site development firms, and EPC contractors managing site preparation, transformer installation, and charging station commissioning |

|

Network Management & Software |

Charging network software providers, payment gateway integrators, OCPP platform vendors, remote monitoring companies, and energy management system suppliers |

|

End Users & Fleet Operators |

Private electric vehicle owners, ride-hailing and delivery fleet operators, public utility vehicle operators, commercial property tenants, and government fleet managers utilizing charging services |

Vertically integrated players, particularly those owning proprietary charging hardware, network management software, and direct end-user relationships, are positioned to capture greater value than partners reliant on third-party infrastructure.

Technology Landscape in the Philippines Electric Vehicle Charging Station Industry

AC Charging Technology and Smart Level 2 Systems

AC Level 2 chargers remain the workhorse of the Philippine public and commercial charging network. Modern smart AC units integrate Wi-Fi or 4G connectivity, OCPP compliance, real-time energy monitoring, and dynamic load management, enabling operators to optimize energy consumption and offer app-based payment and reservation features to end users.

Inductive and Wireless Charging

Inductive charging technology, though currently representing only 9.5% market share, is gaining attention in the Philippines for fleet bus and commercial vehicle applications where automated charging without manual connector plug-in offers operational efficiency benefits. Pilot programs in the public transport modernization space are expected to drive early adoption of inductive charging pads in bus terminal and depot environments.

Network Software, Payments, and IoT Integration

Charging network operators in the Philippines are deploying IoT-connected station management systems that integrate real-time occupancy monitoring, predictive maintenance alerts, mobile app navigation, and fleet management dashboards. Cloud-based network management platforms with open APIs are enabling multi-operator roaming agreements and aggregated real-time charging availability data for electric vehicle drivers nationwide.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Charging Station Type |

AC Charging |

59.8% |

2025 |

|

Vehicle Type |

Battery Electric Vehicle (BEV) |

54.6% |

2025 |

|

Installation Type |

🔒 |

🔒 |

2025 |

|

Charging Level |

🔒 |

🔒 |

2025 |

|

Connector Type |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

Luzon |

62.3% |

2025 |

By Charging Station Type

AC charging commands a 59.8% majority share in 2025, driven by lower equipment cost, widespread compatibility with residential and commercial building electrical systems, and the suitability of Level 2 charging for overnight, workplace, and retail destination use cases.

To access detailed market analysis, Request Sample

DC charging at 30.7% in 2025 is the second largest segment, fueled by expressway fast charging demand, fleet operator depot requirements, and the growing availability of DC-compatible BEV models from mainstream automakers in the Philippines.

By Vehicle Type

Battery electric vehicle (BEV) dominates with 54.6% share in 2025, reflecting strong consumer and fleet operator preference for fully electric drivetrains supported by an expanding BEV model lineup from key brands. The segment is directly driving demand for both AC home charging and DC public fast charging infrastructure.

Plug-in hybrid electric vehicle (PHEV) at 27.8% in 2025 attracts buyers who value extended range alongside electric efficiency, particularly in provincial areas with limited public charging coverage.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Luzon |

62.3% |

High urban population density, EVIDA mandate compliance in Metro Manila commercial real estate, expressway fast charging network, and largest concentration of registered electric vehicles in the country |

|

Visayas |

21.4% |

Growing electric vehicle adoption in Cebu City and Iloilo, expanding tourism-driven charging infrastructure, increasing commercial property development, and rising consumer awareness of electric mobility |

|

Mindanao |

16.3% |

Emerging electric vehicle market with expanding government fleet electrification, improving power grid reliability, rising disposable incomes in Davao and Cagayan de Oro, and increasing inter-city road connectivity |

Luzon at 62.3% in 2025 leads the regional landscape, anchored by Metro Manila, CALABARZON, and Central Luzon. Dense commercial real estate development, high concentration of registered electric vehicles in the country, an expanding expressway fast charging network, and strong EVIDA implementation enforcement across building permit processes support sustained regional leadership through the forecast period.

Mindanao at 16.3% is the second largest region. Improving power grid infrastructure, expanding government fleet electrification programs, and rising urban consumer awareness in Davao and Cagayan de Oro are driving accelerating electric vehicle adoption and charging infrastructure demand through 2034.

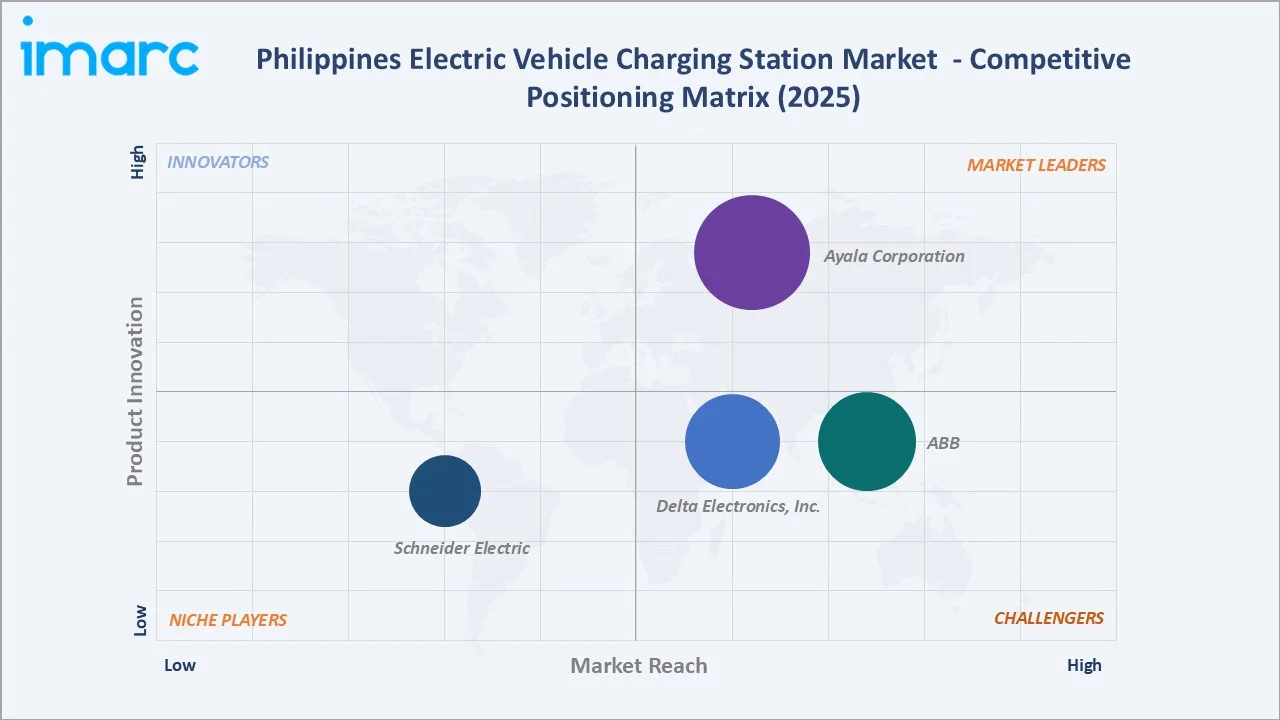

Competitive Landscape

The Philippines electric vehicle charging station market is moderately fragmented, with global charging equipment manufacturers, local property developer-backed networks, and utility-affiliated operators competing for market share. Brand credibility, equipment reliability, network software capability, and access to utility grid interconnection approvals form the key competitive moats in this rapidly scaling market.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Ayala Corporation |

ACMobility (Philippine EV Spine) |

Leader |

Leading electric vehicle charging network operator in the Philippines; expanding through partnerships and infrastructure investments |

|

Delta Electronics, Inc. |

DeltaGrid EVM |

Challenger |

Safety-certified electric vehicle charger supplier; providing AC and DC charging solutions with solar and energy storage integration |

|

ABB |

Terra 360 |

Challenger |

Supplying DC fast charging equipment to commercial, fleet, and expressway corridor operators through local distribution partnerships |

|

Schneider Electric |

EVlink |

Niche Player |

Supplying integrated electric vehicle charging and building energy management solutions to commercial property developers and industrial facilities |

Key players include Ayala Corporation, Delta Electronics, Inc., ABB, and Schneider Electric, among others.

Key Company Profiles

Ayala Corporation

Ayala Corporation is one of the Philippines' oldest and most diversified conglomerates, with interests spanning real estate, banking, telecommunications, infrastructure, and mobility. Headquartered in Makati City, the company operates through a network of subsidiaries and affiliates that serve both domestic and international markets.

- Product Portfolio: ACMobility operates the Philippine EV Spine, spanning Luzon, Visayas, and Mindanao. The portfolio includes AC Level 2 and DC fast chargers at commercial, highway, and hospitality locations and end-to-end electric vehicle infrastructure deployment services for commercial and institutional partners.

- Recent Developments: In May 2025 , ACMobility revealed its latest electric vehicle charging stations in Makati City, equipped with 240 kW SuperFast and 480 kW UltraFast chargers. In collaboration with the Makati Commercial Estate Association (MACEA) and Ayala Land, Inc. (ALI), the new high-performance chargers began functioning at the Corinthians Carpark, with the Leviste Carpark scheduled to come next.

- Strategic Focus: Expanding the Philippine EV Spine into a comprehensive national fast-charging network, leveraging Ayala's property assets and utility partnerships.

Delta Electronics, Inc.

Delta Electronics, Inc. is a global provider of power and thermal management solutions, industrial automation, building automation, and electric vehicle charging infrastructure. The company operates across a broad range of energy-related segments and maintains an active presence in Southeast Asia, including the Philippines, where it supplies electric vehicle charging equipment and energy management systems to commercial, industrial, and public-sector clients.

- Product Portfolio: The company's electric vehicle charging portfolio includes AC chargers, DC fast chargers for commercial and public deployment, and the DeltaGrid® EVM smart charging management system that integrates electric vehicle chargers with solar generation, energy storage, and building energy management platforms.

- Recent Developments: Delta Electronics has maintained an active presence in the market, participating in industry events and expanding its network of commercial and institutional installations. The company provides electric vehicle charging solutions to fuel retailers and commercial property operators across the country.

- Strategic Focus: Providing locally safety-certified, smart-energy-integrated electric vehicle charging solutions to commercial property developers, fuel retailers, and industrial facility operators across the Philippines, with a focus on solar-plus-storage charging deployments and OCPP-compliant smart charging management.

ABB

ABB is a multinational technology corporation specializing in electrification, automation, and motion, with a global presence across several countries. The company is a recognized global leader in electric vehicle charging infrastructure, offering a comprehensive range of AC and DC charging solutions through its electrification business segment.

- Product Portfolio: ABB's electric vehicle charging portfolio includes the Terra 360 ultra-fast DC charger and the Terra AC wallbox for commercial and residential applications.

- Recent Developments: ABB continues to expand its Terra Series product line globally, with the Terra 360 charger being positioned as the flagship product for commercial and highway charging deployments.

- Strategic Focus: Supplying high-reliability DC fast charging equipment and network management technology to commercial property operators, expressway service area operators, and fleet charging depot managers across the Philippines through local distribution and EPC contractor partnerships.

Market Concentration Analysis

The Philippines electric vehicle charging station market is moderately fragmented, with no single operator commanding a dominant share of the total installed charging station base. The top four players collectively represent the majority of commercial and highway charging deployments, with the market characterized by a mix of global equipment manufacturers, utility-affiliated network operators, and private property developer-backed networks.

Barriers to entry include grid connection approval requirements from distribution utilities, building permit coordination under EVIDA implementation rules, the need for locally certified and serviceable equipment, and the capital intensity of DC fast charger deployments. These factors favor established global equipment suppliers and well-capitalized local network operators.

Consolidation is beginning to emerge as network operators seek scale to improve station utilization rates and reduce per-site operating costs. Partnerships between equipment manufacturers and property developer networks, as well as between utility companies and charging network operators, are expected to drive further consolidation through the forecast period.

Investment & Growth Opportunities

Fastest-Growing Segments

DC charging is the fastest-growing charging station type, driven by highway corridor deployment, fleet operator depot requirements, and growing consumer demand for rapid charging. Inductive charging, while currently nascent, represents the highest long-term growth potential as public transport electrification and automated vehicle charging use cases scale up through 2034.

Emerging Markets

Mindanao is the fastest-growing region, driven by improving power grid reliability, government fleet electrification programs, and rising urban consumer awareness of electric vehicle benefits. Visayas at 21.4% also presents significant untapped opportunity, particularly in Cebu City and Iloilo, where tourism-driven electric vehicle adoption and expanding commercial real estate development are creating new charging infrastructure demand.

Venture & Investment Trends

Investment is concentrated in highway fast-charging corridor development, fleet depot electrification, solar-integrated commercial charging systems, and network software platforms enabling multi-operator roaming and payment interoperability.

Future Market Outlook (2026-2034)

The Philippines electric vehicle charging station market is forecast to expand from USD 431.6 Million in 2025 to USD 3934.9 Million by 2034 at a CAGR of 27.00%, adding approximately USD 3503.3 Million in incremental market value over the forecast period.

Four forces will shape the market through 2034: the deepening implementation of EVIDA and evolving DOE charging infrastructure standards; the rapid scaling of DC fast charging along the national expressway network; the electrification of commercial fleets across logistics, ride-hailing, and public transport; and the growing integration of electric vehicle charging with renewable energy systems and smart grid infrastructure.

By 2034, the Philippines electric vehicle charging market is expected to be defined by a mature national public charging network, widespread fleet depot electrification, and increasing V2G capability linked to grid stability programs. Policy enforcement under EVIDA, private sector investment at scale, and declining DC fast charger equipment costs are together expected to accelerate the transformation of the Philippines into one of Southeast Asia's most advanced electric vehicle charging ecosystems.

Research Methodology

Primary Research

Primary research included structured interviews with electric vehicle charging network operators, property developers, DOE and LGU regulatory officials, electric vehicle automaker representatives, utility company executives, and fleet electrification managers. These interviews validated market sizing, regional demand trends, charging station type adoption patterns, and competitive positioning across the Philippines electric vehicle charging ecosystem.

Secondary Research

Secondary sources included the Philippine Department of Energy EV and Charging Infrastructure Registry, BOI investment promotion publications, CAMPI vehicle registration statistics, DOE National Renewable Energy Program updates, and annual reports, press releases, and technical documentation from major charging equipment manufacturers and network operators.

Forecasting Models

Market forecasts used top-down and bottom-up models combining registered electric vehicle counts, charging station deployment rates, average revenue per station, grid capacity expansion scenarios, and EVIDA mandate compliance timelines. Scenario analysis addressed regulatory enforcement pace, DC fast charger cost trajectory, grid upgrade investment timelines, and the rate of fleet electrification across key commercial vehicle segments.

Philippines Electric Vehicle Charging Station Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Charging Station Types Covered | AC charging, DC charging, Inductive charging |

| Vehicle Types Covered | Battery electric vehicle (BEV), Plug-in hybrid electric vehicle (PHEV), Hybrid electric vehicle (HEV) |

| Installations Covered | Portable charger, Fixed charger |

| Levels Covered | Level 1, Level 2, Level 3 |

| Connector Types Covered | Combined charging station (CCS), CHAdeMO, Normal charging, Tesla Supercharger, Type-2 (IEC 621196), Others |

| Applications Covered | Residential, Commercial |

| Regions Covered | Luzon, Visayas, Mindanao |

| Companies Covered | Ayala Corporation, Delta Electronics, Inc., ABB, Schneider Electric, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Philippines electric vehicle charging station market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Philippines electric vehicle charging station market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Philippines electric vehicle charging station industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Philippines Electric Vehicle Charging Station Market Report

The Philippines electric vehicle charging station market was valued at USD 431.6 Million in 2025, driven by EVIDA mandate enforcement, rising electric vehicle adoption, and expanding public and commercial charging infrastructure across Luzon, Visayas, and Mindanao.

The market is projected to grow at a CAGR of 27.00% during 2026-2034, reaching USD 3934.9 Million, supported by DC fast charger expansion, fleet electrification, and sustained government policy enforcement.

AC charging leads with 59.8% share in 2025, driven by lower installation costs and EVIDA-driven building-integrated demand.

Battery electric vehicle (BEV) dominates with 54.6% share in 2025, supported by growing BEV model availability from key brands.

Luzon commands 62.3% of market share in 2025, anchored by Metro Manila, CALABARZON, and Central Luzon, where electric vehicle adoption, expressway charging, and EVIDA-compliant commercial real estate are most concentrated.

Leading players include Ayala Corporation, Delta Electronics, Inc., ABB, and Schneider Electric, among others.

Key drivers include EVIDA policy mandates, rising electric vehicle sales, Japanese and Korean automaker model launches, highway fast-charging corridor development, fleet electrification, and increasing solar-integrated charging deployments across commercial properties.

Grid infrastructure limitations in Visayas and Mindanao, high DC fast charger capital costs, permitting complexity in dense urban areas, and limited consumer awareness in provincial markets are the primary restraints on market expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)