Philippines Fruits & Vegetables Market Size, Share, Trends and Forecast by Product, Distribution Channel, and Region, 2026-2034

Philippines Fruits & Vegetables Market Overview:

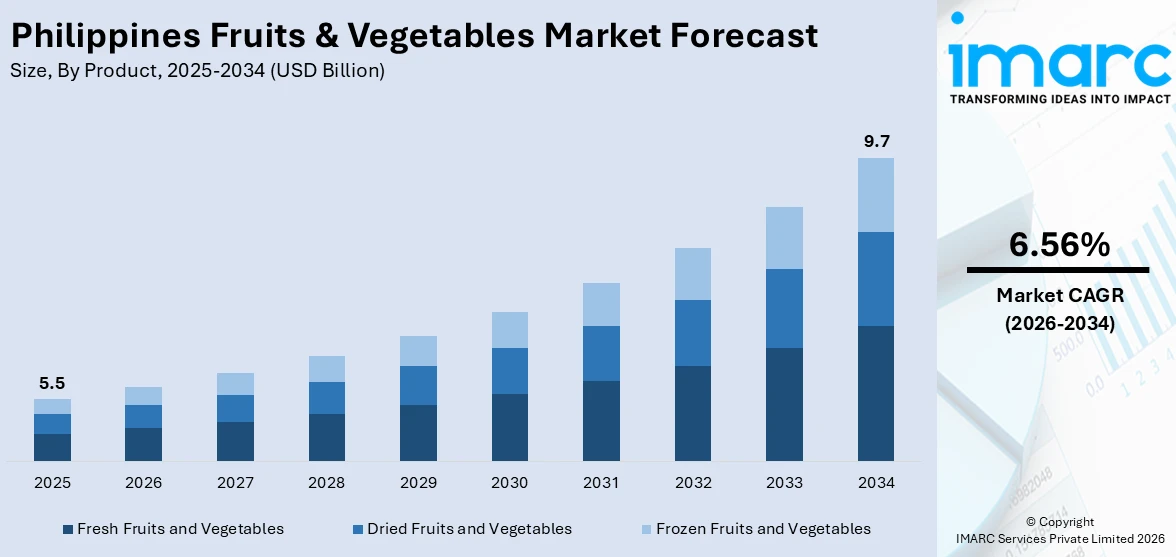

The Philippines fruits and vegetables market size reached USD 5.5 Billion in 2025. Looking forward, the market is expected to reach USD 9.7 Billion by 2034, exhibiting a growth rate (CAGR) of 6.56% during 2026-2034. The market is propelled by the increasing domestic demand for nutritious foods due to the growing awareness about health and wellness, growing export market for tropical fruits such as bananas, pineapples, and mangoes, and advancements in agricultural technology and practices.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 5.5 Billion |

| Market Forecast in 2034 | USD 9.7 Billion |

| Market Growth Rate (2026-2034) | 6.56% |

Key Trends of Philippines Fruits & Vegetables Market:

Increasing Domestic Demand for Nutritious Foods

Growing awareness about health and wellness among Filipinos is one key driver of the fruits and vegetables market. As lifestyle diseases such as obesity, diabetes, and hypertension are increasingly becoming the norm, the Philippine government and other health organizations have mounted campaigns to promote people to eat right and develop healthy lifestyle. Consumers are looking for more fresh fruits and vegetables to consume to meet their nutritional needs. According to the article published by the Philippine News Agency, programs like “Gulayan sa Barangay,” which promote local vegetable gardens, are making fruits and vegetables more accessible, especially in urban areas. The Program has expanded to 27,000 community gardens across 17 regions and 42,000 villages, aiming to address food security by turning vacant lands into productive vegetable and fruit gardens. This falls in line with a larger push for access to fresh, locally sourced produce. Healthy living is becoming more prevalent in the Philippines. Millennials and Gen Z consumers are moving toward plant-based diets, and social media is amplifying the benefits of clean eating. Another market factor in demand growth is supermarkets and online platforms offering organic and locally sourced products that health-conscious buyers can purchase.

To get more information on this market Request Sample

Growing Export Market for Tropical Fruits

The Philippines' export market for tropical fruits such as bananas, pineapples, and mangoes is a vital driver for the fruits and vegetables industry. Countries like Japan, China, and South Korea are primary markets for these exports due to their preference for high-quality and competitively priced Philippine produce. As per the Department of Trade and Industry, in 2024, Philippine fruit exporters attained unusual sales at the China-ASEAN Expo, securing USD 49 million in negotiated sales, the highest in the history of the country. The indicates the growing demand for Philippine produce in China. The tropical fruits of the country are found to be among the top exporters due to rich biodiversity and favorable climate. Government programs such as the Regional Comprehensive Economic Partnership (RCEP) are helping Filipino farmers to get better access on international markets. Investments in cold storage facilities, logistics, and post-harvest technology further enhance export potential with spoilage at lower levels by as long as possible ensuring the produce reaches global markets fresh.

Growth Drivers of Philippines Fruits & Vegetables Market:

Government Infrastructure Development and Policy Support

The Philippine government's strategic investments in agricultural infrastructure are creating a robust foundation for sustained market expansion. The Department of Agriculture's comprehensive roadmap emphasizes the development of food corridors near major urban centers, equipped with state-of-the-art facilities, including refrigerated storage, modern post-harvest processing systems, and efficient logistics networks. These infrastructure improvements address critical supply chain bottlenecks that have historically resulted in significant post-harvest losses, estimated at substantial portions of total production. Government initiatives such as the Farm-to-Market Road Program, with billions allocated for constructing thousands of kilometers of roadways, directly enhance market access for farmers while reducing transportation costs and delivery times. Furthermore, policy frameworks supporting the Regional Comprehensive Economic Partnership and other trade agreements are expanding market opportunities for Philippine produce in international markets. The government's White Revolution initiative, inspired by successful greenhouse farming models in South Korea, demonstrates a commitment to modernizing vegetable production through protected cultivation systems that mitigate climate-related risks and ensure a consistent year-round supply.

Rising Consumer Purchasing Power and Urbanization

The Philippines' economic growth trajectory and expanding middle class are fundamentally reshaping consumption patterns in the fruits and vegetables sector, fueling the Philippines fruits & vegetables market share. Urban populations, which continue to grow at significant rates, exhibit higher propensities to purchase fresh produce regularly compared to rural counterparts, driven by greater awareness of nutrition and easier access to modern retail channels. The proliferation of supermarkets, hypermarkets, and online grocery platforms in metropolitan areas has transformed how consumers purchase fruits and vegetables, emphasizing convenience, quality assurance, and product variety. These modern retail formats offer diverse product selections, including premium organic options, exotic fruits, and pre-packaged vegetables that cater to evolving consumer preferences for convenience and health. According to the Philippines fruits & vegetables market analysis, the growth of the food service industry, including restaurants, cafes, and quick-service establishments, creates substantial demand for fresh produce as ingredients. Rising disposable incomes enable consumers to allocate larger portions of household budgets toward fresh, nutritious foods rather than relying primarily on processed alternatives. This demographic and economic transition creates sustained demand growth that outpaces traditional consumption patterns.

Climate Adaptation and Sustainability Initiatives

The increasing urgency of climate change mitigation and adaptation is driving transformative changes in Philippine agriculture that enhance market resilience and sustainability. Extreme weather events, including typhoons, droughts, and unpredictable rainfall patterns, have historically caused significant production losses and supply disruptions in the fruits and vegetables sector. In response, both government agencies and private sector stakeholders are implementing climate-smart agricultural practices that improve crop resilience while maintaining productivity. Organic farming methodologies are gaining traction as alternatives to conventional chemical-intensive agriculture, with the Organic Agriculture Act and subsequent amendments providing institutional support for certification systems and farmer training programs. The establishment of Participatory Guarantee Systems has made organic certification more accessible and affordable for smallholder farmers, expanding the supply of certified organic produce. Additionally, investments in water management infrastructure, including irrigation systems and rainwater harvesting facilities, help farmers maintain consistent production during dry seasons. The development of drought-resistant and pest-tolerant crop varieties through agricultural research institutions enhances production stability. These sustainability-focused initiatives not only protect the environment but also create premium market segments for eco-conscious consumers willing to pay higher prices for sustainably produced fruits and vegetables.

Philippines Fruits & Vegetables Market Dynamics:

Supply Chain Volatility and Post-Harvest Loss Management

The market analysis reveals significant challenges related to supply chain inefficiencies and substantial post-harvest losses that impact market stability and profitability. Inadequate cold chain infrastructure, particularly in rural production areas, results in considerable spoilage during transportation and storage, with losses estimated at substantial percentages of total production volume. The archipelagic geography of the Philippines compounds logistical complexities, as produce must traverse multiple islands to reach major urban consumption centers, increasing transit times and handling frequency. Limited access to refrigerated transport vehicles and temperature-controlled storage facilities forces many farmers to sell immediately after harvest, often at depressed prices during peak production periods. However, ongoing investments in modern logistics infrastructure, including the establishment of regional food hubs and improved cold storage networks, are gradually addressing these inefficiencies. The development of better packaging technologies and the adoption of rapid cooling systems at the farm level are helping extend shelf life and reduce waste, thereby improving overall market dynamics and farmer profitability.

Price Fluctuations and Market Accessibility Challenges

Price volatility remains a defining characteristic of the Philippines fruits & vegetables market demand patterns, influenced by seasonal production cycles, weather-related disruptions, and supply-demand imbalances. During peak harvest seasons, oversupply frequently drives prices below production costs, while off-season scarcity results in price spikes that reduce consumer affordability and accessibility. This cyclical pattern creates income instability for farmers and unpredictability for buyers, complicating long-term business planning across the value chain. Small-scale farmers, who constitute most producers, face particular challenges accessing profitable markets due to limited bargaining power, dependence on intermediaries, and lack of market information. The presence of multiple middlemen in traditional distribution channels further compresses farm-gate prices while inflating retail costs. Government interventions through price monitoring mechanisms, direct farmer-to-consumer platforms like Kadiwa markets, and contract farming arrangements are attempting to stabilize prices and improve farmer income. Additionally, the expansion of organized retail chains and digital marketplaces is creating alternative distribution channels that potentially offer better price transparency and more equitable value distribution across supply chain participants.

Climate Vulnerability and Production Risk Factors

The Philippines fruits & vegetables market growth trajectory faces persistent threats from climate-related vulnerabilities and natural disasters that create substantial production uncertainty. The country's location in the typhoon belt exposes agricultural areas to frequent tropical storms, with 2024 alone witnessing damage exceeding PHP 57 billion across the agriculture sector, affecting over 1.4 million farmers and destroying approximately 1 million hectares of cropland. Beyond typhoons, the alternating impacts of El Niño-induced droughts and La Niña-associated flooding disrupt planting schedules, reduce yields, and damage infrastructure. Plant diseases and pest infestations, often exacerbated by climate variability, impose additional production losses despite efforts to develop resistant varieties and implement integrated pest management programs. Rising input costs, particularly for fertilizers and fuel, further constrain farmer profitability and investment capacity in resilience-building measures. However, the market is witnessing adaptive responses, including the adoption of protected agriculture systems like greenhouses that shield crops from adverse weather, diversification of planting calendars, and investment in crop insurance programs. These risk mitigation strategies, combined with improved early warning systems and disaster preparedness protocols, are gradually enhancing the sector's resilience to environmental shocks.

Philippines Fruits & Vegetables Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country level for 2026-2034. Our report has categorized the market based on product and distribution channel.

Product Insights:

- Fresh Fruits and Vegetables

- Dried Fruits and Vegetables

- Frozen Fruits and Vegetables

The report has provided a detailed breakup and analysis of the market based on the product. This includes fresh fruits and vegetables, dried fruits and vegetables, and frozen fruits and vegetables.

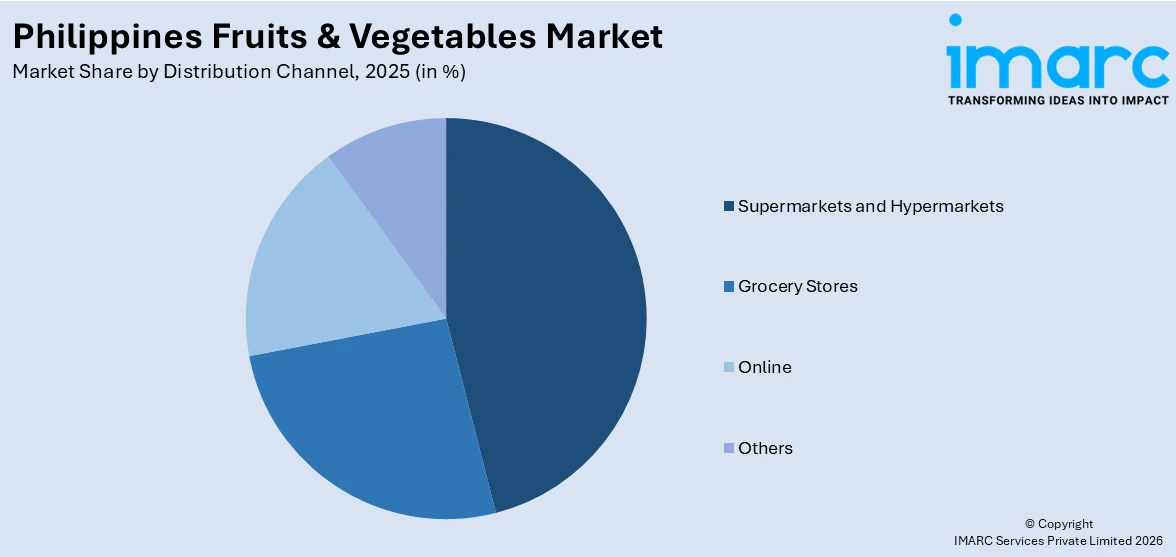

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Grocery Stores

- Online

- Others

A detailed breakup and analysis of the market based on the distribution channel have also been provided in the report. This includes supermarkets and hypermarkets, grocery stores, online, and others.

Regional Insights:

- Luzon

- Visayas

- Mindanao

The report has also provided a comprehensive analysis of all the major regional markets, which include Luzon, Visayas, and Mindanao.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Philippines Fruits & Vegetables Market News:

- February 2025: The Philippines announced that it has gained approval to export Hass avocados to Japan, which marked another significant milestone in the growth of agricultural exports in the country. Indeed, this shows the country's sincerity in upgrading farm produce and improving the quality of products. It further cements the country's status as a significant high-value fruit supplier to Japan, a market known for being selective in the consumer preferences.

- In October 2024, Sales of Philippine fruit exports including as durian, coconut, and banana goods at the annual China-Asean Expo (Caexpo) increased over fivefold to reach an all-time high of $49 million in 2024, according to the Department of Trade and Industry's (DTI) Philippine Trade and Investment Centre.

Philippines Fruits & Vegetables Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Fresh Fruits and Vegetables, Dried Fruits and Vegetables, Frozen Fruits and Vegetables |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Grocery Stores, Online, Others |

| Regions Covered | Luzon, Visayas, Mindanao |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Philippines fruits & vegetables market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Philippines fruits & vegetables market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Philippines fruits & vegetables industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Philippines Fruits & Vegetables Market Report

The fruits & vegetables market in the Philippines was valued at USD 5.5 Billion in 2025.

The Philippines fruits & vegetables market is projected to exhibit a CAGR of 6.56% during 2026-2034.

The Philippines fruits & vegetables market is projected to reach a value of USD 9.7 Billion by 2034.

The Philippines fruits and vegetables market is driven by growing demand for organic produce, farm-to-table concepts, online grocery platforms, sustainable packaging, value-added processing, and increasing consumer preference for fresh, locally sourced, and health-oriented food products.

Growth is fueled by rising health consciousness, government support for agricultural modernization, improved cold chain logistics, expanding export opportunities, increasing urban farming initiatives, technological advancements in cultivation, and higher consumer spending on nutritious and premium-quality fresh produce.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)