Philippines Health Insurance Market Size, Share, Trends and Forecast by Provider, Type, Plan Type, Demographics, Provider Type, and Region, 2026-2034

Philippines Health Insurance Market Overview:

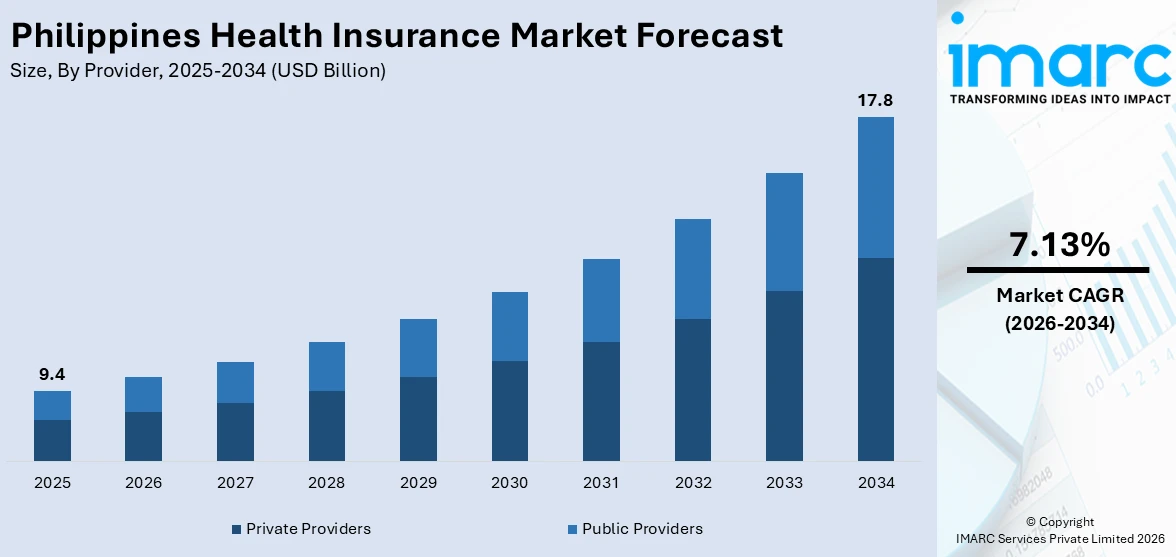

The Philippines health insurance market size reached USD 9.4 Billion in 2025. The market is projected to reach USD 17.8 Billion by 2034, exhibiting a growth rate (CAGR) of 7.13% during 2026-2034. The market consists of public and private sectors offering diverse plans tailored to various consumer needs. Coverages range from a variety of policy types addressing different segments and regional needs. The market is transforming with increased demand for easy access, digitalization, and customized health plans. Growing awareness of healthcare and insurance benefits is fueling growth, complemented by government support and enhanced distribution channels. These trends are defining the entire growth and dynamics of the Philippines health insurance market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 9.4 Billion |

| Market Forecast in 2034 | USD 17.8 Billion |

| Market Growth Rate 2026-2034 | 7.13% |

Philippines Health Insurance Market Trends:

Expansion of Public Insurance Infrastructure

The Philippines has made meaningful progress in strengthening public health insurance infrastructure, notably through enhanced access and modernization of service delivery. Universal enrollment under the national health insurance program has continued to expand through local Health Insurance Offices and related support networks. In May 2025, the Department of Health announced that over 50 BUCAS (Bagong Urgent Care and Ambulatory Service) centers are now operational far surpassing the initial goal of 28 bringing essential outpatient and urgent care services closer to underserved communities across the country. This network not only provides free or subsidized services for low-income and elderly Filipinos but also serves as a touchpoint for promoting health insurance awareness and registration. The increased visibility and accessibility of these centers help reinforce trust in the public insurance system and enable smooth onboarding for beneficiaries. Policy modernization, combined with improved infrastructure, is enhancing both coverage and actual usability of health insurance programs. Collectively, these developments pave the way for deeper institutional reach and inclusive service delivery, fueling potential future momentum for Philippines health insurance market growth.

To get more information on this market Request Sample

Rising Healthcare Costs and Evolving Policy Design

Healthcare expenses in the Philippines have been steadily increasing, placing more pressure on both insurers and policyholders. This upward trend in medical costs has prompted regulators to encourage more inclusive and tailored health insurance products. In April 2025, the Insurance Commission urged the adoption of gender-responsive policies aimed at addressing specific health needs such as maternal care, reproductive health, and critical illness coverage. These calls for more nuanced policy design reflect the broader effort to create insurance products that better align with diverse demographic needs while keeping premiums sustainable. Health Maintenance Organizations (HMOs) and insurers are actively developing options that cater to evolving consumer expectations and regulatory requirements. This adaptability is vital in balancing affordability with comprehensive coverage in a market that faces increasing demand for quality healthcare services. Taken together, these policy shifts and regulatory initiatives highlight key drivers behind the Philippines health insurance market trends, as the industry works to remain responsive to both economic pressures and social health priorities.

Embracing Digital Innovation for Efficiency

The Philippines health insurance market is increasingly adopting digital solutions to enhance operational efficiency and member satisfaction. In 2024, PhilHealth launched an AI-based claims processing system that is intended to largely minimize the time spent on reimbursements, allowing healthcare providers to spend more time attending to patients and not paperwork. This is one of the larger digital transformation trends in the insurance sector, which seeks to automate workflows and reduce administrative expenses. Furthermore, the Insurance Commission and National Privacy Commission entered a data privacy accord in 2024 to promote secure processing of member data with the increasing use of digital tools. These improvements not only increase the speed and precision of claims but also instill consumer confidence in the security and dependability of the system. With growing digital uptake, the sector is in a stronger position to provide hassle-free services that satisfy contemporary expectations. This emphasis on technology-driven innovation is transforming the way health insurance providers deliver services, enabling a more streamlined and consumer-friendly setting throughout the Philippines.

Philippines Health Insurance Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on provider, type, plan type, demographics, and provider type.

Provider Insights:

- Private Providers

- Public Providers

The report has provided a detailed breakup and analysis of the market based on the provider. This includes private providers and public providers.

Type Insights:

Access the comprehensive market breakdown Request Sample

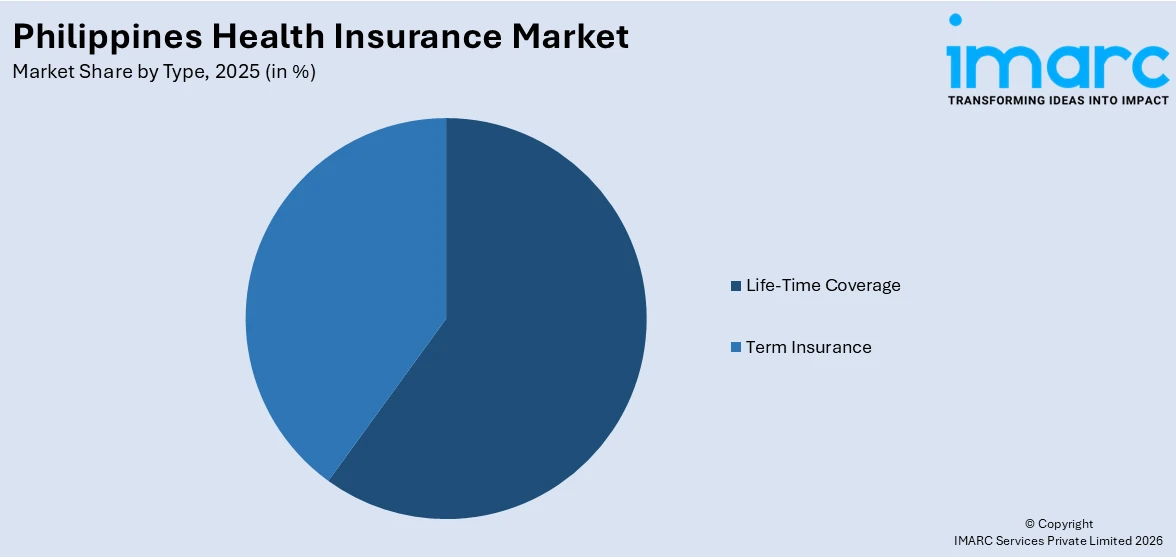

- Life-Time Coverage

- Term Insurance

A detailed breakup and analysis of the market based on the type have also been provided in the report. This includes life-time coverage and term insurance.

Plan Type Insights:

- Medical Insurance

- Critical Illness Insurance

- Family Floater Health Insurance

- Others

The report has provided a detailed breakup and analysis of the market based on the plan type. This includes medical insurance, critical illness insurance, family floater health insurance, and others.

Demographics Insights:

- Minor

- Adults

- Senior Citizen

A detailed breakup and analysis of the market based on the demographics have also been provided in the report. This includes minor, adults, and senior citizen.

Provider Type Insights:

- Preferred Provider Organizations (PPOs)

- Point of Service (POS)

- Health Maintenance Organizations (HMOs)

- Exclusive Provider Organizations (EPOs)

The report has provided a detailed breakup and analysis of the market based on the provider type. This includes preferred provider organizations (PPOs), point of service (POS), health maintenance organizations (HMOs), and exclusive provider organizations (EPOs).

Regional Insights:

- Luzon

- Visayas

- Mindanao

The report has also provided a comprehensive analysis of all the major regional markets, which include Luzon, Visayas, and Mindanao

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Philippines Health Insurance Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Providers Covered | Private Providers, Public Providers |

| Types Covered | Life-Time Coverage, Term Insurance |

| Plan Types Covered | Medical Insurance, Critical Illness Insurance, Family Floater Health Insurance, Others |

| Demographics Covered | Minor, Adults, Senior Citizen |

| Provider Types Covered | Preferred Provider Organizations (PPOs), Point of Service (POS), Health Maintenance Organizations (HMOs), Exclusive Provider Organizations (EPO) |

| Regions Covered | Luzon, Visayas, Mindanao |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Philippines health insurance market performed so far and how will it perform in the coming years?

- What is the breakup of the Philippines health insurance market on the basis of provider?

- What is the breakup of the Philippines health insurance market on the basis of type?

- What is the breakup of the Philippines health insurance market on the basis of plan type?

- What is the breakup of the Philippines health insurance market on the basis of demographics?

- What is the breakup of the Philippines health insurance market on the basis of provider type?

- What is the breakup of the Philippines health insurance market on the basis of region?

- What are the various stages in the value chain of the Philippines health insurance market?

- What are the key driving factors and challenges in the Philippines health insurance market?

- What is the structure of the Philippines health insurance market and who are the key players?

- What is the degree of competition in the Philippines health insurance market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Philippines health insurance market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Philippines health insurance market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Philippines health insurance industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)