Philippines ICT Market Size, Share, Trends and Forecast by Spending, Technology, and Region, 2026-2034

Philippines ICT Market Size, Share, Trends & Forecast (2026-2034)

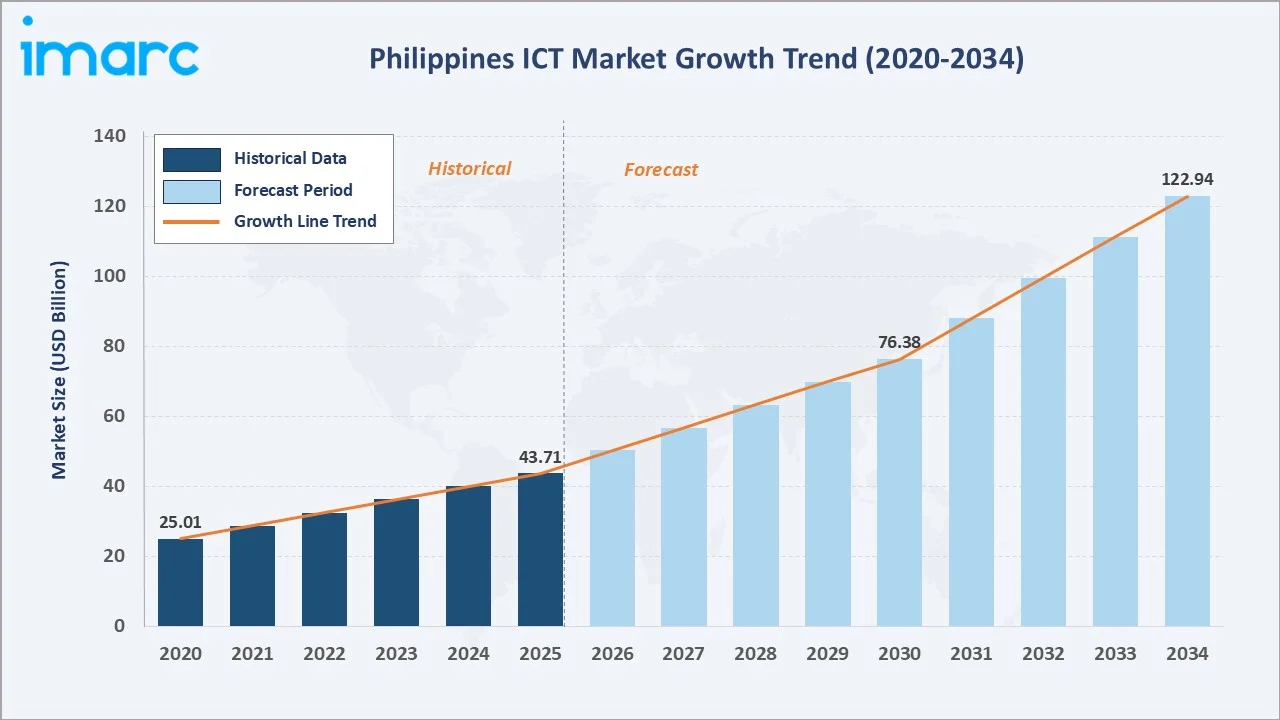

The Philippines ICT market reached USD 43.71 Billion in 2025 and is projected to reach USD 122.94 Billion by 2034, growing at a CAGR of 11.81% during 2026-2034. Substantial public and private investments in digital infrastructure, rapid cloud adoption by enterprises, government-led digital transformation initiatives, the expansion of the business process outsourcing (BPO) sector, and rising mobile and internet penetration across urban and rural areas are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 43.71 Billion |

|

Forecast Market Size (2034) |

USD 122.94 Billion |

|

CAGR (2026-2034) |

11.81% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

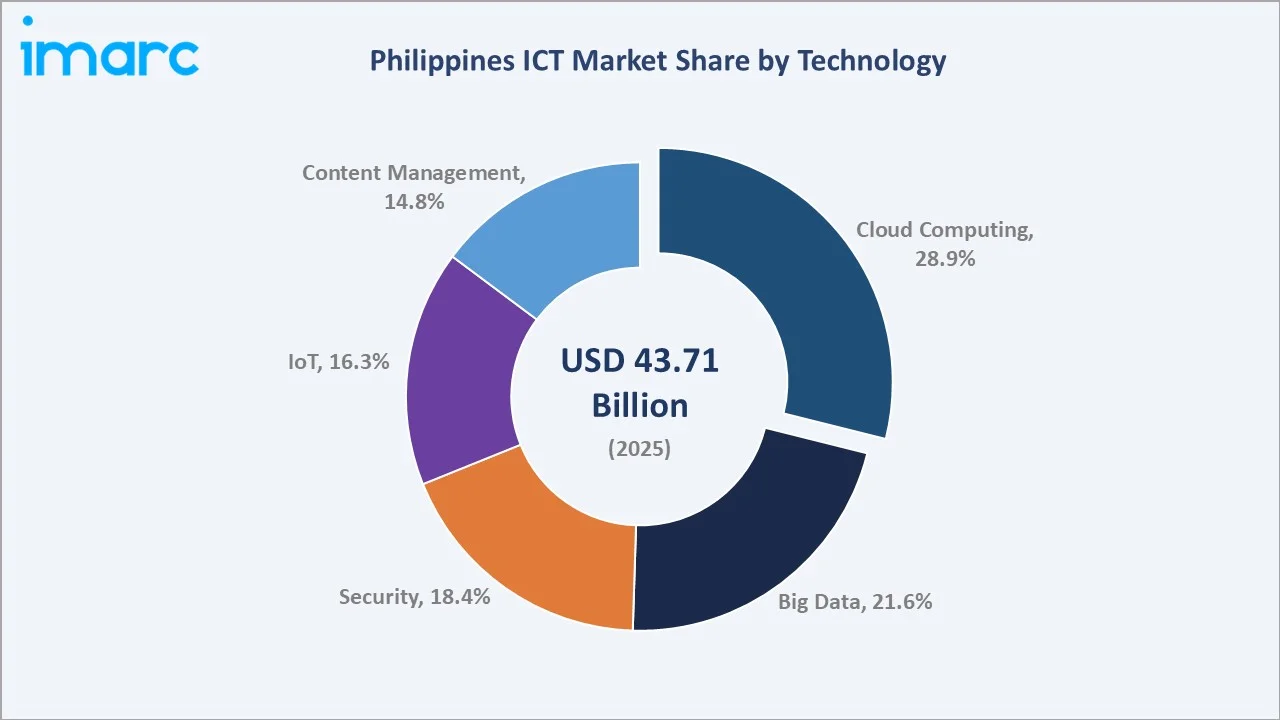

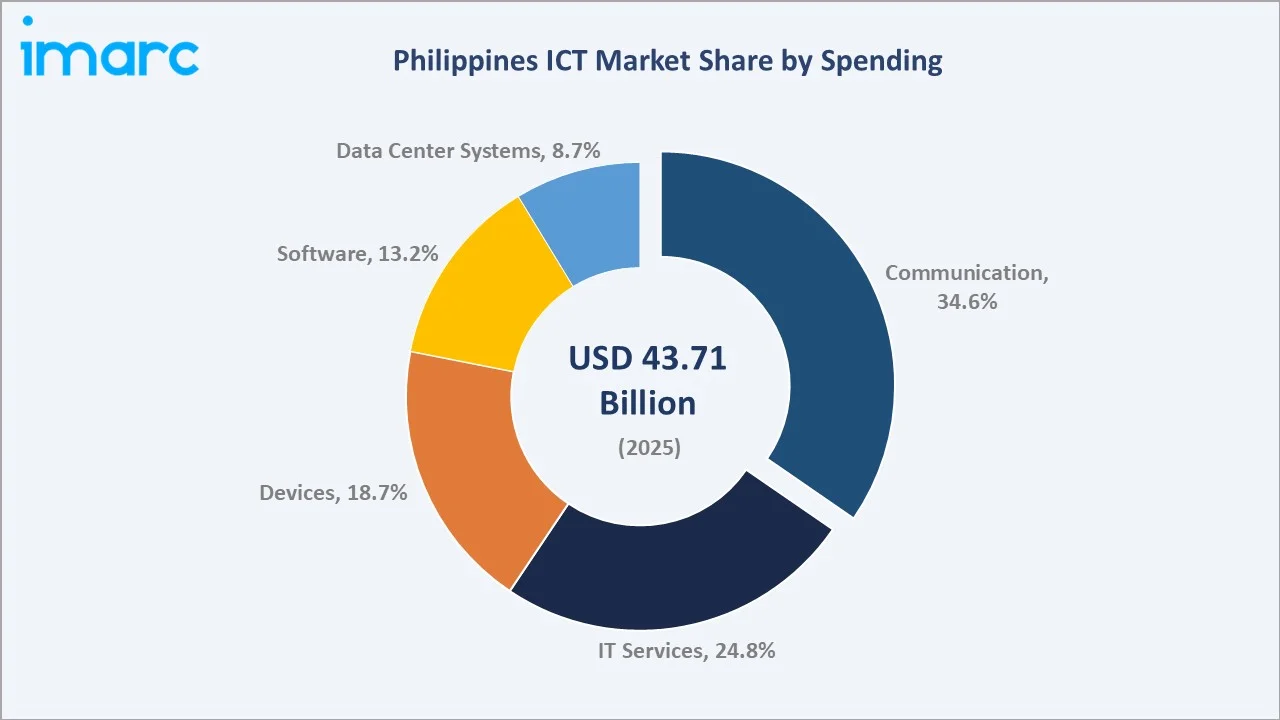

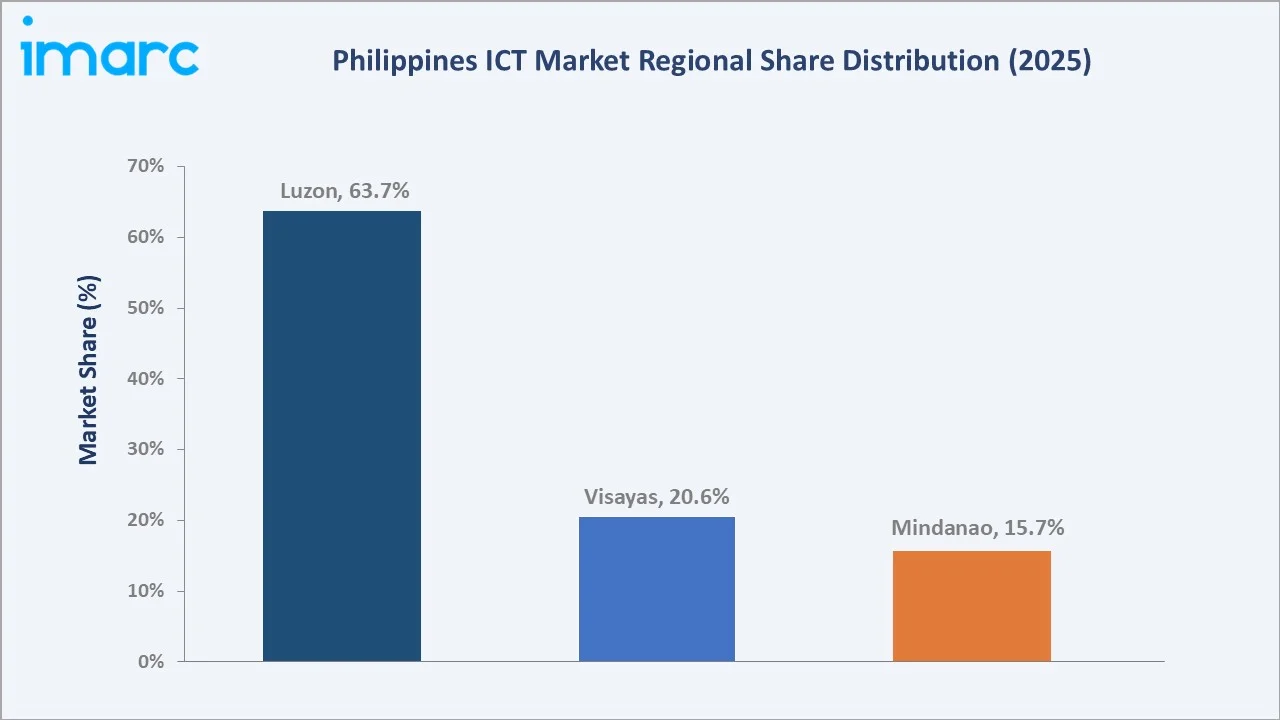

Luzon leads regionally with a 63.7% market share in 2025, anchored by Metro Manila’s dense ICT ecosystem and concentration of BPO, BFSI, and government digital infrastructure. The communication segment commands a dominant 34.6% share of ICT spending, while cloud computing retains the largest technology segment share at 28.9% in 2025.

To get more information on this market, Request Sample

The Philippines ICT market is underpinned by three structural forces: the National Economic and Development Authority’s PHP 16.1 Billion Philippine Digital Infrastructure Plan (PDIP), BPO sector-driven sustained demand for IT services and connectivity, and the government’s mandate for digital transformation across public services.

Executive Summary

The Philippines ICT market is experiencing broad-based, accelerated expansion driven by the convergence of government digital transformation mandates, surging enterprise cloud adoption, and the country’s globally recognized BPO sector creating sustained demand for advanced IT infrastructure. The market was valued at USD 43.71 Billion in 2025 and is forecast to reach USD 122.94 Billion by 2034, growing at a CAGR of 11.81%. The digital economy contributed approximately USD 35.4 Billion to Philippine GDP in 2023, representing 8.4% of national output, establishing ICT as a structural pillar of the country’s economic growth model.

Cloud computing leads the technology segment with a 28.9% share in 2025, driven by enterprises across BFSI, retail, and manufacturing transitioning workloads to scalable cloud platforms. Communication dominates the spending segment at 34.6%, reflecting the country’s high mobile penetration and ongoing investment by Globe Telecom, PLDT/Smart, and DITO Telecommunity in 5G networks and broadband expansion.

Luzon accounts for 63.7% of national ICT spending in 2025, anchored by Metro Manila’s hyperscale data center clusters, BPO campuses, and government digital infrastructure. Key players, including Globe Telecom, Inc., PLDT Inc., Microsoft, IBM Corporation, and Cisco Systems Inc., collectively define the competitive dynamics across all ICT segments.

Key Market Insights

|

Insight |

Data |

|

Largest Technology Segment |

Cloud Computing – 28.9% share (2025) |

|

Fastest Growing Technology |

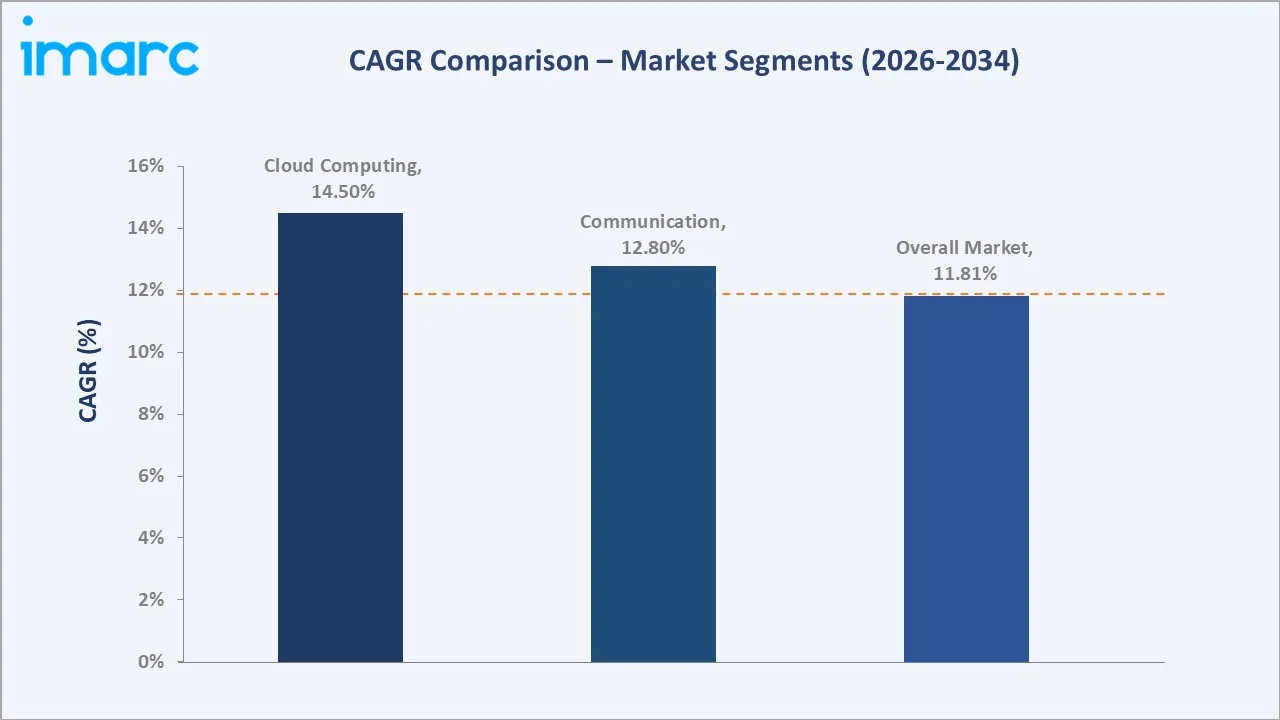

Cloud Computing – ~14.50% CAGR (2026-2034) |

|

Largest Spending Segment |

Communication – 34.6% share (2025) |

|

Fastest Growing Spending Segment |

Communication – ~12.80% CAGR (2026-2034) |

|

Leading Region |

Luzon – 63.7% share (2025) |

|

Top Companies |

Globe Telecom, Inc., PLDT Inc., Microsoft, IBM Corporation, and Cisco Systems Inc. |

Key Analytical Observations Supporting the Above Data:

- Cloud computing commands 28.9% of the technology segment in 2025. This dominance reflects the accelerating transition of Philippine enterprises from on-premise IT infrastructure to scalable cloud platforms, driven by hybrid and multi-cloud adoption across BFSI, BPO, retail, and manufacturing.

- Communication leads the spending segment at 34.6%, reflecting the Philippines’ high mobile penetration and the telecom sector’s capital-intensive 5G rollout. Globe surpassed 100 additional sites in Geo-Isolated and Disadvantaged Areas (GIDA) in 2025, directly expanding addressable ICT spending on connectivity infrastructure.

- Luzon accounts for 63.7% of national ICT market share, anchored by Metro Manila’s concentration of hyperscale data centers, BPO campuses, and government digital infrastructure. PLDT inaugurated a data center in Sta. Rosa in April 2025, while ST Telemedia Global Data Centers’ 124 MW facility and the ENDECGROUP’s 300 MW campus collectively add more than 200 MW IT load in Luzon.

- Big Data represents 21.6% of technology spending in 2025, driven by the financial services and BPO sectors’ growing reliance on real-time analytics, fraud detection, and customer intelligence platforms. GCash’s 94 million users as of mid- 2025 and digital wallet penetration reaching 52.8% are generating massive transaction datasets requiring advanced analytics infrastructure.

Philippines ICT Market Overview

The Philippines ICT market encompasses the entire spectrum of information and communication technology products, services, and infrastructure, spanning telecommunications networks, hardware devices, software solutions, IT services, data center systems, cloud platforms, cybersecurity, and emerging technologies including IoT, Big Data, and AI. The market serves enterprise, government, SME, and consumer segments across Luzon, Visayas, and Mindanao, with the BPO sector representing a uniquely large institutional demand driver with approximately 1.7 million direct employees and contributing around USD 35 Billion annually to the economy.

Macroeconomic drivers include the Philippine Statistics Authority’s measurement of the digital economy at USD 35.4 Billion (8.4% of GDP) in 2023, NEDA’s PHP 16.1 Billion Philippine Digital Infrastructure Plan (PDIP) approved in June 2024, and approved foreign investments in Q4 2024 reaching a total value of PHP 57.70 billion. The convergence of government digital transformation mandates, 5G network expansion by the telecom duopoly, and cloud-first strategies by multinationals operating in the Philippines creates a compounding growth engine sustaining the market’s above-average CAGR trajectory through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

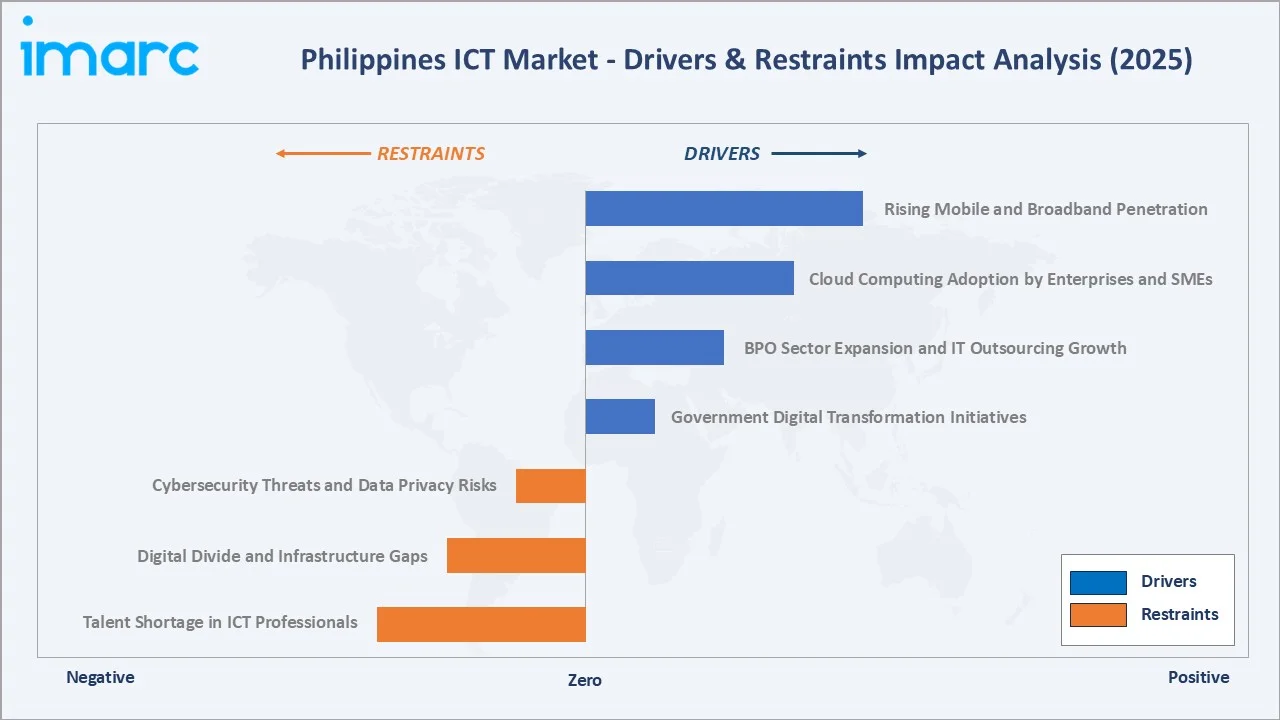

Market Drivers

- Government Digital Transformation Initiatives: The Philippine government has committed to broad-based ICT investment through the PHP 16.1 Billion PDIP, the E-Government Master Plan 2022–2028, and the Open Access in Data Transmission Act enabling competitive broadband. The Department of Information and Communications Technology (DICT) is mandating digital services for government agencies to implement a unified and standards-driven framework for ICT planning through their Information Systems Strategic Plans (ISSPs).

- BPO Sector Expansion and IT Outsourcing Growth: The Philippines remains the world’s premier BPO destination with contributions of over USD 35 Billion annually, representing around 8.4% of the country’s GDP. BPO operations generate structural demand for enterprise communication systems, cloud infrastructure, cybersecurity platforms, and IT services. The sector’s transition toward higher-value knowledge process outsourcing (KPO) is accelerating demand for AI, analytics, and cloud-native applications.

- Cloud Computing Adoption by Enterprises and SMEs: Philippine enterprises across BFSI, retail, and manufacturing are transitioning workloads to cloud platforms to lower infrastructure expenses, enhance operational efficiency, and support remote work. SMEs representing 99% of Philippine businesses are leveraging cloud services for access to high-quality IT capabilities without high upfront costs.

- Rising Mobile and Broadband Penetration: The Philippines recorded around 142 million active cellular mobile connections in early 2025, representing approximately 122% of the country’s total population. DICT’s Free Public WiFi program extended to 50,000 sites in 2025, accelerating connectivity-driven ICT consumption in underserved communities.

Market Restraints

- Cybersecurity Threats and Data Privacy Risks: More than 80% of organizations in the Philippines reportedly faced an average of three cybersecurity incidents during 2024, highlighting the growing cyber threat landscape across the country. Compliance with the Data Privacy Act of 2012 (Republic Act 10173) requires enterprises to invest in data protection infrastructure, adding ICT cost burdens for SMEs.

- Digital Divide and Infrastructure Gaps: Despite rapid urban ICT development, approximately 18 million Filipinos in rural and island communities lack reliable internet access. Mobile internet remains the dominant mode of connectivity in the Philippines, while fixed broadband penetration is limited to only around 33% of households. Geographic fragmentation across 7,641 islands creates high infrastructure deployment costs, with last-mile connectivity remaining underinvested across Mindanao and Eastern Visayas regions.

- Talent Shortage in ICT Professionals: The Philippines faces a deficit of approximately 180,000 ICT professionals, with high-skill roles in cloud architecture, data science, AI engineering, and cybersecurity most severely understaffed. Brain drain of Filipino IT talent to international outsourcing destinations and domestic wage inflation in the BPO sector create competitive pressure on domestic enterprise ICT capabilities.

Market Opportunities

- 5G Private Networks and Edge Computing: The expansion of 5G private networks to logistics, mining, and precision agriculture represents a USD 2–3 Billion incremental ICT opportunity by 2030. PLDT’s data center in Sta. Rosa and the planned mega-campus in Cavite introduce sub-10 ms latency edge nodes critical for smart-factory analytics and high-frequency trading workloads.

- Fintech and E-Commerce Digital Infrastructure: Digital wallet penetration reaching 52.8% and GCash’s 94 million users are catalyzing demand for payment infrastructure, fraud detection AI, and real-time data processing platforms. This is creating a structural demand anchor for fintech-oriented ICT investments across cloud, APIs, and cybersecurity.

Market Challenges

- Regulatory Complexity and Spectrum Policy: The ICT sector navigates overlapping regulatory jurisdictions from the National Telecommunications Commission (NTC), DICT, National Privacy Commission, and the Bangko Sentral ng Pilipinas (BSP) for fintech. The Konektadong Pinoy bill’s dark-fiber leasing provisions remain under legislative review, limiting open-access infrastructure development.

- Power Grid Reliability for Data Center Operations: The rapid rise in data center construction is placing increasing pressure on the Philippines’ already fragile power grid, fueling concerns over higher electricity prices and greater dependence on coal-based power generation. Businesses in the Philippines incur average electricity costs of around USD 0.155 per kWh, significantly higher than rates in China (USD 0.108 per kWh), Indonesia (USD 0.07 per kWh), and Vietnam (USD 0.078 per kWh).

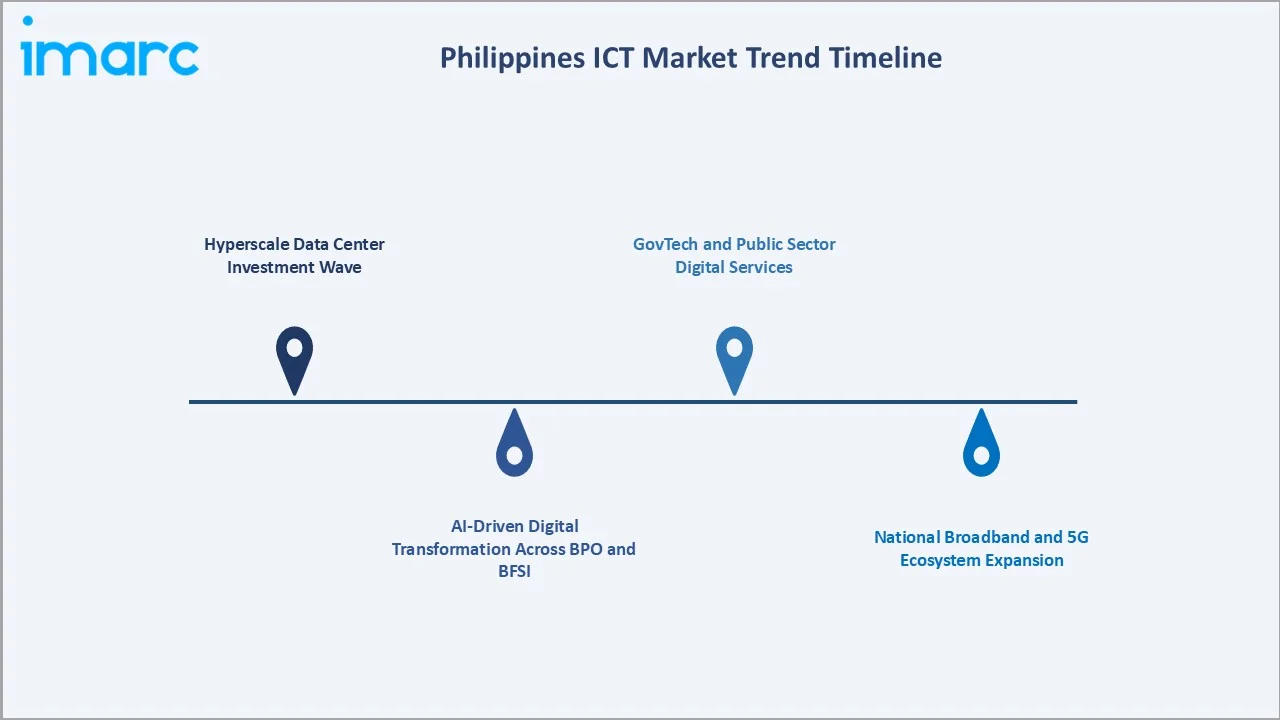

Emerging Market Trends

1. Hyperscale Data Center Investment Wave

Open-equity rules now allowing 100% foreign ownership in Philippine data centers have unlocked capacity additions from STT GDC, PLDT, and other operators. VITRO Sta. Rosa operates with a power capacity of up to 50 MW, while the combined capacity of ePLDT’s VITRO data center network stands at nearly 100 MW, supporting emerging AI and high-frequency trading workloads.

2. AI-Driven Digital Transformation Across BPO and BFSI

Philippine enterprises are rapidly integrating AI and generative AI into BPO workflows, with Accenture Philippines, IBM, and Cognizant deploying large language model solutions for customer service automation and knowledge process outsourcing. In April 2026, the Philippine government announced finalizing an Artificial Intelligence Governance Framework within two months, aimed at strengthening innovation, improving AI regulation, and accelerating the country’s digital transformation initiatives.

3. National Broadband and 5G Ecosystem Expansion

Philippines Digital Infrastructure Project, worth EUR 268.22 million (USD 287.24 million), combined with InfiniVAN Inc. and IPS Inc., partnered with the DICT on a P5.6-billion international gateway investment, is fundamentally transforming national connectivity. Mid-band 5G spectrum allocation is enabling sub-10 ms latency services across Philippine cities, with open-RAN deployments by Globe Telecom diversifying vendor ecosystems and reducing radio infrastructure costs.

4. GovTech and Public Sector Digital Services

The Philippine government’s E-Government Master Plan mandates digital-first service delivery across 500 agencies, creating a PHP 25–30 Billion annual procurement pipeline for cloud, ERP, identity management, and cybersecurity solutions. The Department of Trade and Industry’s partnership with INCIT to deploy the Smart Industry Readiness Index nationwide signals the government’s commitment to evidence-based industrial digitalization policy.

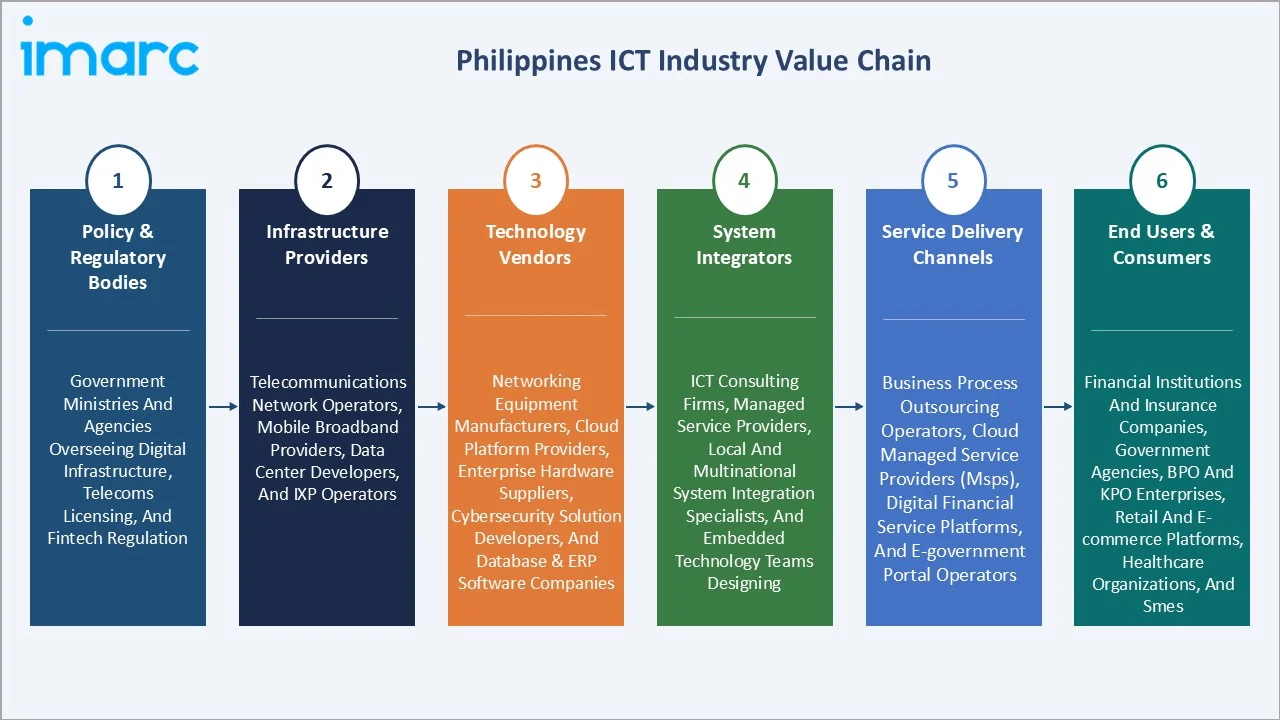

Industry Value Chain Analysis

The Philippines ICT value chain spans policy and regulatory oversight through end-user consumption across enterprise, government, and consumer segments, with each stage occupied by specialized domestic and global players whose capabilities directly determine the quality, cost, and reach of digital services.

|

Stage |

Key Participants / Examples |

|

Policy & Regulatory Bodies |

Government ministries and agencies overseeing digital infrastructure, telecommunications licensing, and financial technology regulation |

|

Infrastructure Providers |

Telecommunications network operators, fixed-line and mobile broadband providers, data center developers and operators, and internet exchange point (IXP) operators |

|

Technology Vendors |

Networking equipment manufacturers, cloud platform providers, enterprise hardware suppliers, cybersecurity solution developers, and database & ERP software companies |

|

System Integrators |

ICT consulting firms, managed service providers, local and multinational system integration specialists, and embedded technology teams designing |

|

Service Delivery Channels |

Business process outsourcing operators, cloud managed service providers (MSPs), digital financial service platforms, and e-government portal operators |

|

End Users & Consumers |

Financial institutions and insurance companies, government agencies, BPO and KPO enterprises, retail and e-commerce platforms, healthcare organizations, and SMEs |

Technology Landscape in the Philippines ICT Industry

Cloud Computing and Hybrid Cloud Infrastructure

Cloud computing dominates at 28.9% of the technology segment, with Azure, AWS, and Google Cloud each maintaining dedicated Philippine points of presence (PoPs) to reduce latency for enterprise clients. The hybrid cloud model, combining on-premise infrastructure with public cloud scalability, is the preferred approach for regulated Philippine industries including banking, insurance, and government, driven by BSP’s cloud computing guidelines requiring data residency compliance.

Big Data and Analytics Platforms

Big Data represents 21.6% of technology spending in 2025, accelerating as GCash’s 94 million-user ecosystem, BSP’s real-time payment rails, and BPO clients’ customer intelligence mandates generate unprecedented data volumes. IBM’s Watson analytics, Microsoft’s Azure Synapse, and Oracle’s Autonomous Database are the leading platforms, while local fintech players leverage open-source tools including Apache Spark and Hadoop for cost-effective data warehousing.

Cybersecurity Solutions

The NPC’s 741 personal breach notifications from 2022 to August 2024 catalyzed board-level security investment across BFSI, BPO, and government agencies. Cisco Systems Inc, Microsoft (Defender suite), and Palo Alto Networks (QRadar/Cortex XSIAM) are the leading solution providers, while local MSSPs are scaling managed detection and response services for the SME and mid-market segments underserved by global vendors.

IoT and Connected Infrastructure

IoT represents 16.3% of technology spending, with smart city deployments in Quezon City and Makati, smart port projects at the Manila Port Authority, and precision agriculture pilots in Mindanao driving demand. PLDT’s 5G private network deployments in logistics and mining create connected asset monitoring use cases requiring IoT edge devices, sensor networks, and real-time data pipelines.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Technology |

Cloud Computing |

28.9% |

2025 |

|

Spending |

Communication |

34.6% |

2025 |

|

Region |

Luzon |

63.7% |

2025 |

By Technology

Cloud computing leads the technology segment with a 28.9% share in 2025, encompassing IaaS, PaaS, and SaaS deployments across enterprise and government sectors. Its leadership reflects the capital-intensive transition by Philippine BPO firms, banks, and retailers from legacy on-premise infrastructure to scalable, cost-efficient cloud platforms. The segment is growing fastest at approximately 14.50% CAGR, driven by multi-cloud strategies, hybrid cloud adoption in regulated industries, and the government’s cloud-first procurement policy.

To access detailed market analysis, Request Sample

Big Data at 21.6% is the second-largest technology segment, driven by BFSI institutions, e-commerce platforms, and BPO analytics capabilities. Security at 18.4% is the fastest-growing technology sub-segment by investment urgency, as regulatory requirements intensify. IoT at 16.3% is expanding rapidly through 5G private networks in industrial and agricultural contexts, while content management at 14.8% underpins BPO workflow automation, digital media platforms, and e-government portals.

By Spending

Communication dominates ICT spending at 34.6% in 2025, encompassing fixed-line broadband, mobile data services, enterprise WAN/MPLS, and 5G connectivity. This segment’s leadership reflects the Philippines’ high mobile penetration rate and the telecom sector’s multi-billion-dollar 5G infrastructure investment by Globe and PLDT/Smart.

IT Services at 24.8% is the second-largest spending category, representing the country’s BPO-driven professional services economy, managed IT outsourcing, and consulting engagements by Accenture, IBM, and Cognizant. Devices at 18.7% encompass smartphones, PCs, servers, and networking hardware, growing moderately as enterprises refresh infrastructure for cloud-ready deployments.

Regional Market Insights

Luzon’s dominant 63.7% share (2025) reflects Metro Manila’s status as Southeast Asia’s premier BPO hub, home to the majority of the country’s ICT infrastructure, data centers, and enterprise IT investment. PLDT’s Sta. Rosa data center, STT GDC’s 124 MW Fairview facility, and planned hyperscale campuses in Cavite collectively place the Luzon corridor at the center of the Philippine ICT expansion cycle through 2034.

Visayas at 20.6% is the fastest-growing regional market, anchored by Cebu City’s established IT Park BPO ecosystem accommodating 270,000 workers and Fujitsu’s August 2024 launch of its first Southeast Asia Digital Innovation Hub. The Visayas’ growing offshore connectivity via the Apricot cable’s regional landing stations is reducing latency for BPO voice and data operations, improving the region’s competitiveness as an ICT investment destination alongside Metro Manila.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Luzon |

63.7% |

Concentration of BPO and IT-BPM operations in the region; hyperscale data center development in peri-urban industrial corridors; government digital infrastructure investment and e-services deployment |

|

Visayas |

20.6% |

Cebu City's established BPO and IT Park ecosystem driving sustained enterprise ICT demand; growing digital innovation hub activity attracting technology investment. |

|

Mindanao |

15.7% |

Smart city digital infrastructure initiatives in major urban centers; agricultural IoT and precision farming technology adoption; large-scale fiber optic rollout connecting hundreds of cities and municipalities to national broadband backbone |

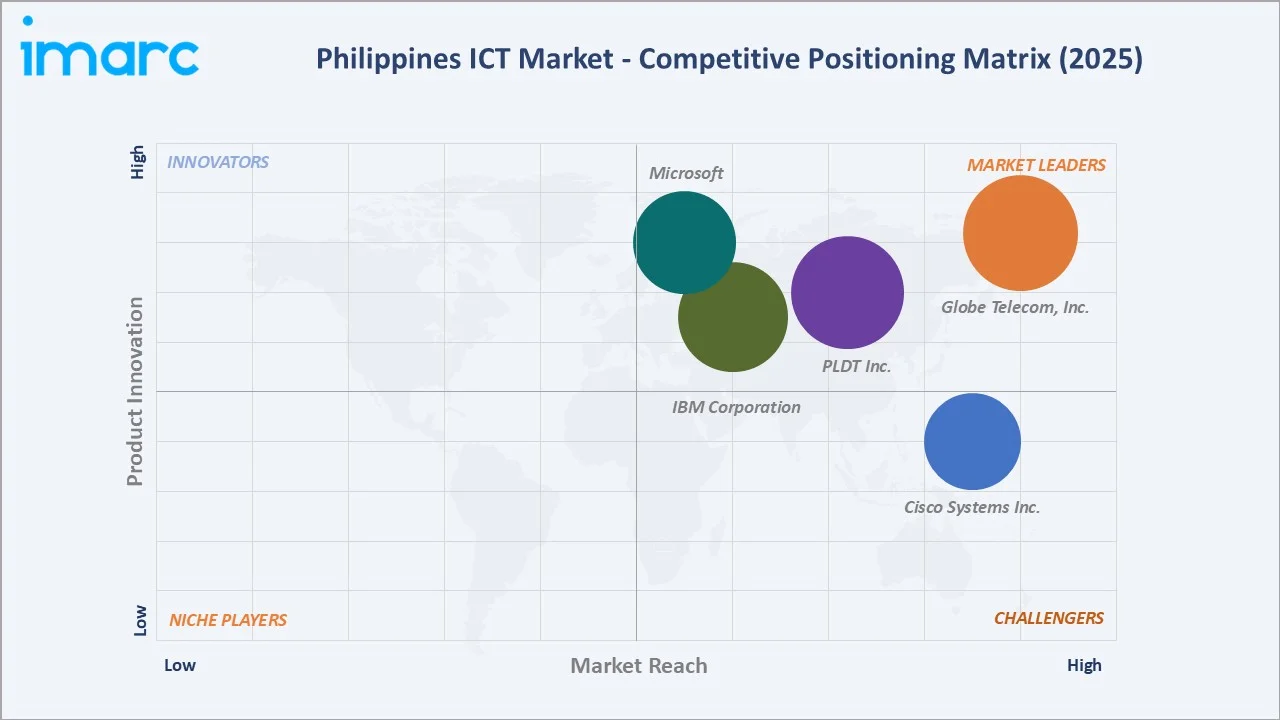

Competitive Landscape

The Philippines ICT market exhibits a dual-tier competitive structure: a highly concentrated telecommunications infrastructure layer where Globe Telecom, Inc. and PLDT Inc. collectively exceed 80% national mobile and fixed-line market share.

|

Company Name |

Brand/Service |

Market Position |

Core Strength |

|

Globe Telecom, Inc. |

GlobeOne, GCash, AutoloadMax, Platinum GPlan, Platinum GPlan Plus, GFiber |

Market Leader |

Dominant mobile/fixed-line operator; GCash fintech ecosystem |

|

PLDT Inc. |

Smart, FiberBiz, Affordaboost, PLDT Enterprise |

Market Leader |

Fixed broadband leadership; 11 data centers nationwide; National Broadband Plan anchor |

|

Microsoft |

Azure, Microsoft 365, Microsoft Teams |

Market Leader |

Cloud and productivity suite market leadership; Teams adoption across 1M+ BPO seats |

|

IBM Corporation |

watsonx Orchestrate, IBM Cloud Pak |

Market Leader |

Hybrid cloud consulting leadership; Watson AI for BPO automation |

|

Cisco Systems Inc. |

Cisco Nexus One, Webex |

Strong Challenger |

Enterprise networking dominance; Webex UC platform for BPO; security portfolio for regulated enterprises |

A more fragmented enterprise ICT services and solutions layer where global players (Microsoft, IBM Corporation, Cisco Systems Inc.) compete alongside domestic operators and regional integrators. The market remains moderately concentrated overall, with the top five vendors (Globe Telecom Inc., PLDT Inc., Microsoft, IBM Corporation, Cisco Systems Inc.) collectively holding approximately 45–50% of total ICT revenue.

Key Company Profiles

Globe Telecom, Inc.

Globe Telecom, Inc., headquartered in Taguig City, Metro Manila, is the Philippines’ largest telecommunications and digital services company by mobile revenue, serving approximately 65 million mobile subscribers through its brands. Globe also operates GCash, the country’s dominant digital payments platform with 90+ million registered users as of mid-2025.

- Product Portfolio: Globe mobile (4G/5G), GlobeOne fiber broadband, GCash digital wallet, AutoloadMax, Platinum GPlan, Platinum GPlan Plus, and GFiber.

- Recent Developments: In January 2025, Globe Telecom launched the Philippines’ first fully operational Private 5G Network designed for B2B connectivity, offering enterprises dedicated bandwidth, enhanced security, and low-latency performance for mission-critical operations.

- Strategic Focus: 5G network densification; GCash ecosystem monetization; enterprise cloud and security services through Globe Business; digital financial inclusion through GFi Ventures.

PLDT Inc.

PLDT Inc., headquartered in Makati City, is the Philippines’ largest fixed-line operator and a leading data center developer. Its subsidiary Smart Communications operates the second-largest mobile network. PLDT’s PLDTCloud and 11-data-center portfolio anchor the country’s cloud and colocation infrastructure.

- Product Portfolio: Smart mobile (4G/5G), PLDT Fiber broadband, FiberBiz, Affordaboost, PLDT Enterprise, PLDT data centers (11 nationwide), and Smart enterprise IoT services.

- Recent Developments: In March 2025, PLDT Enterprise renewed its ICT partnership with Coca-Cola Europacific Aboitiz Philippines (CCEAP) to enhance nationwide operations through improved connectivity, mobile communication, and data security solutions.

- Strategic Focus: Data center capacity leadership; cloud-first enterprise solutions; National Broadband Plan copper-to-fiber migration; green financing for sustainable infrastructure.

Market Concentration Analysis

The Philippines ICT market exhibits a highly concentrated telecommunications infrastructure sub-market alongside a moderately fragmented enterprise ICT services market. DITO Telecommunity’s market entry in 2021 has introduced competitive pressure in the consumer connectivity segment, with DITO reaching 15 million subscribers by 2025.

In the cloud and enterprise software sub-segment, the top three hyperscalers (Microsoft Azure, Amazon AWS, Google Cloud) collectively hold approximately 60–65% of Philippine cloud market revenue, with IBM maintaining a strong position in hybrid cloud consulting. Consolidation is occurring through cloud vendor partnerships: Converge ICT–NAVER Cloud (May 2024) and PLDT–AWS (cloud-first enterprise agreement).

Investment & Growth Opportunities

Fastest Growing Segments

Cloud computing (~14.50% CAGR), cybersecurity platforms (~13.80% CAGR), AI and analytics software (~14.20% CAGR), and data center infrastructure (~13.50% CAGR) represent the highest-growth investment vectors through 2034. Together, these sub-categories address a combined incremental addressable market of approximately USD 30–35 Billion within the Philippines ICT ecosystem by 2034, as cloud-first transformation, regulatory compliance mandates, and AI adoption converge.

Emerging Market Expansion

Cebu (Visayas BPO anchor), Davao (Mindanao smart city), and Clark-Pampanga (emerging ICT corridor with Clark Freeport’s 100% foreign ownership advantage) represent incremental ICT market opportunities beyond Metro Manila. Entry strategies include BPO client-led expansion, government GovTech procurement partnerships, and joint ventures with established domestic telcos for last-mile ICT service delivery in underserved communities targeted by the DICT’s Free WiFi Act implementation.

Venture and Institutional Investment Trends

- USD 10+ Billion in announced data center capacity additions from STT GDC, PLDT, ENDECGROUP, and others (2025–2028) creates a direct procurement pipeline for power infrastructure, cooling systems, and networking equipment vendors targeting the Philippine hyperscale market.

- The Philippine government’s PHP 16.1 Billion PDIP and PHP 25–30 Billion annual GovTech procurement pipeline represent a stable institutional demand anchor for cloud, cybersecurity, identity management, and enterprise application software vendors through 2028.

Future Market Outlook (2026-2034)

The Philippines ICT market is positioned for sustained, high-growth expansion through 2034. From a base of USD 43.71 Billion in 2025, the market is projected to reach USD 122.94 Billion by 2034, representing total incremental value creation of USD 79.23 Billion at a CAGR of 11.81%. This growth is structurally assured by the country’s USD 10+ Billion data center investment pipeline, the BPO sector’s continued evolution toward AI-augmented knowledge services, and government-mandated digital transformation across all public service delivery channels.

Cloud computing’s share of ICT technology spending is projected to rise from 28.9% in 2025 to approximately 38–42% by 2034 as hybrid cloud becomes the de facto enterprise architecture standard. Communication’s share within ICT spending may moderate from 34.6% to 30–32% as 5G infrastructure investment peaks and software and IT services capture a larger share of growing ICT budgets. Luzon’s regional dominance will persist, though Visayas and Mindanao are projected to grow at 12–13% CAGR as BPO decentralization and government digital infrastructure investment accelerate beyond Metro Manila.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 100 industry participants in 2024–2025, including telco executives, cloud solution providers, enterprise IT decision-makers, government CIOs, BPO technology leaders, and institutional investors tracking the Philippine digital economy. Expert input validated market sizing, technology adoption rates, and regional deployment patterns.

Secondary Research

Secondary research encompassed company annual reports, DICT digital economy statistics, Philippine Statistics Authority ICT survey data, BSP digital payment reports, IBPAP BPO industry data, NEDA PDIP documentation, NTC telecom infrastructure data, and industry publications including IDC Philippines, Gartner APAC, and Business World Technology.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating digital economy GDP contribution projections, ICT spending per capita growth trajectories, technology adoption rates by sector, and announced investment commitments by major players. A base-case CAGR of 11.81% reflects consensus estimates validated against PSA digital economy measurement data from 2020 to 2025.

Philippines ICT Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Spendings Covered | Devices, Software, IT Services, Data Center Systems, Communication |

| Technologies Covered | IOT, Big Data, Cloud Computing, Content Management, Security |

| Regions Covered | Luzon, Visayas, Mindanao |

| Companies Covered | Globe Telecom, Inc., PLDT Inc., Microsoft, IBM Corporation, Cisco Systems Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Philippines ICT market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Philippines ICT market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Philippines ICT industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Philippines ICT Market Report

The Philippines ICT market reached USD 43.71 Billion in 2025 and is projected to reach USD 122.94 Billion by 2034.

The market is expected to grow at a CAGR of 11.81% during 2026-2034, driven by government digital transformation initiatives, cloud adoption, BPO sector expansion, and rising mobile and broadband penetration across urban and rural areas.

Cloud Computing leads with a 28.9% share in 2025, growing at approximately 14.50% CAGR during 2026–2034, the fastest among all technology segments, driven by enterprise cloud adoption across BFSI, BPO, retail, and government.

Communication dominates with a 34.6% share in 2025, reflecting the Philippines’ high mobile penetration rate, multi-billion-dollar 5G investments by Globe and PLDT/Smart, and the National Broadband Program’s backbone expansion program.

Luzon leads with a 63.7% share in 2025, anchored by Metro Manila’s BPO concentration, hyperscale data centers in Laguna and Cavite, and the government’s ICT infrastructure investment in the National Capital Region.

Key players include Globe Telecom, Inc., PLDT Inc., Microsoft, IBM Corporation, and Cisco Systems Inc.

Ransomware targeting government agencies and BFSI institutions, phishing attacks exploiting high smartphone penetration, and data privacy compliance costs under the Data Privacy Act of 2012 are the primary cybersecurity challenges, collectively driving above-market growth in the Security segment.

Cloud computing is enabling Philippine enterprises to access enterprise-grade IT capabilities at reduced capital expenditure, with Azure, AWS, and Google Cloud all maintaining Philippine PoPs as of 2025. The BSP’s cloud banking guidelines have unlocked regulated financial institution cloud adoption.

Key investment opportunities include hyperscale data, fintech ICT infrastructure for digital payments (USD 3–5 Billion), GovTech digital services, 5G private network deployments in logistics and agriculture, cybersecurity managed services for underserved SMEs and mid-market enterprises, and cloud managed services for BPO operators transitioning from on-premise to hybrid architectures.

The competitive landscape is evolving toward greater enterprise cloud competition as Azure, AWS, and Google Cloud each expand Philippine infrastructure, reducing hyperscaler concentration and improving enterprise pricing. DITO Telecommunity’s infrastructure build-out is introducing price competition in the telco duopoly, while Converge ICT’s fiber expansion is disrupting fixed broadband.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)