Philippines Orphan Drugs Market Size, Share, Trends and Forecast by Drug Type, Disease Type, Phase, Top Selling Drugs, Distribution Channel, and Region, 2026-2034

Philippines Orphan Drugs Market Overview:

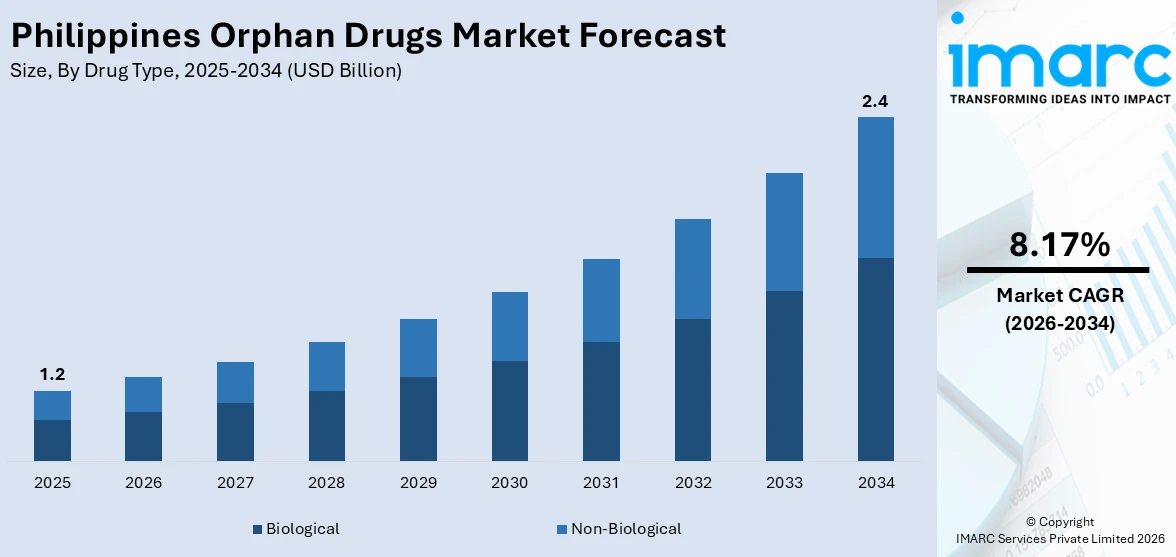

The Philippines orphan drugs market size reached USD 1.2 Billion in 2025. Looking forward, the market is expected to reach USD 2.4 Billion by 2034, exhibiting a growth rate (CAGR) of 8.17% during 2026-2034. The market is fueled by heightened awareness about rare diseases, enhanced healthcare infrastructure, and a surge in government initiatives for the management of rare diseases. Collaboration between public health organizations and pharmaceutical companies is also increasing access to life-saving treatments among underserved patient groups. Rise of patient advocacy groups has helped push for better funding and availability of orphan drugs, which further contribute significantly to the expansion of the Philippines orphan drugs market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 1.2 Billion |

| Market Forecast in 2034 | USD 2.4 Billion |

| Market Growth Rate 2026-2034 | 8.17% |

Philippines Orphan Drugs Market Trends:

Evolving Legislative Framework and Policy Support

In the Philippines, the orphan drugs market is being shaped significantly by the evolving legislative environment and increasing government backing for rare disease initiatives. The passing of regulations and laws in form specifically to support rare disease treatment and diagnosis has given clear direction for those who require access to orphan drugs. This regulatory development is most notable within the archipelago, where geographic isolation and health inequalities had previously undermined prompt treatment for rare disease victims. Government agency collaboration with specialized healthcare facilities has encouraged the development of patient registries and enhanced diagnostics, particularly in the principal regional hospitals located outside Metro Manila. Policy improvements have enabled the addition of orphan medicines in public health benefit packages and led pharmaceutical companies to register and market rare disease treatments with more confidence. Consequently, underprivileged communities throughout Luzon, Visayas, and Mindanao are gradually achieving better access to sophisticated treatments. This legislative drive reflects the Philippines' interest in meeting the needs of its rare disease population and paves the way for more private and public sector participation along with Philippines orphan drugs market growth.

To get more information on this market Request Sample

Patient Advocacy and Community Mobilization

The increasing power of patient advocacy organizations has become a strong force in directing orphan drug trends in the Philippines. Rare disease-affected families, from metabolic disorders to pediatric conditions, have mobilized themselves into engaged communities, often using social media platforms to advocate for awareness, exchange of resources, and focus on the need for access to orphan drugs. These advocacy networks conduct frequent outreach activities in both metropolitan areas and provincial municipalities, establishing relationships with local government units and medical doctors to enable educational seminars and community screenings. They also serve to bridge the information gap that usually occurs in rural areas, where families lack exposure to expert healthcare knowledge. Through their partnerships with non-governmental organizations and health institutions, the groups have been able to effectively lobby for the development of diagnostic hubs in areas outside the capital, facilitating patients with rare diseases to be diagnosed and referred faster. In the long term, their efforts have been able to foster a sense of collective urgency and solidarity that has led to increased public compassion and policy initiative that keep resonating across the country's orphan drug market.

Local Production, Partnerships, and Access Innovations

A salient feature of the Philippines' orphan drugs regime is the developing emphasis on local production, strategic partnerships, and supply chain innovations in pursuit of enhanced accessibility. Though multinational drug firms have long controlled the orphan drug supply in the nation, collaborative agreements with local drug makers and compounding pharmacies during the past few years are making possible production locally or even importation under special licensing agreements. This change diminishes both procurement expense and logistics simplicity, making therapies more accessible to patients in the Philippines. Furthermore, innovative distribution alliances, particularly with hospital groups and provincial community health facilities, mean that even isolated areas have access to life-saving products. Facilities in parts of the country such as Central Visayas and Northern Mindanao become better suited to provide these therapies, a decentralization that complements the archipelago's scattered healthcare infrastructure. Moreover, the emergence of telemedicine and electronic health platforms is facilitating clinicians in remote islands to consult with experts based in Manila or Cebu, allowing proper prescription and monitoring of orphan drug treatments. Collectively, these market forces, based on local collaboration, process transformation, and digital extension, are shaping the way to more inclusive and sustainable orphan drug access across the Philippines.

Philippines Orphan Drugs Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on drug type, disease type, phase, top selling drugs, and distribution channel.

Drug Type Insights:

- Biological

- Non-Biological

The report has provided a detailed breakup and analysis of the market based on the drug type. This includes biological and non-biological.

Disease Type Insights:

- Oncology

- Hematology

- Neurology

- Cardiovascular

- Others

The report has provided a detailed breakup and analysis of the market based on the disease type. This includes oncology, hematology, neurology, cardiovascular, and others.

Phase Insights:

- Phase I

- Phase II

- Phase III

- Phase IV

A detailed breakup and analysis of the market based on the phase have also been provided in the report. This includes phase I, phase II, phase III, and phase IV.

Top Selling Drugs Insights:

- Revlimid

- Rituxan

- Copaxone

- Opdivo

- Keytruda

- Imbruvica

- Avonex

- Sensipar

- Soliris

- Others

A detailed breakup and analysis of the market based on the top selling drugs have also been provided in the report. This includes Revlimid, Rituxan, Copaxone, Opdivo, Keytruda, Imbruvica, Avonex, Sensipar, Soliris, and others.

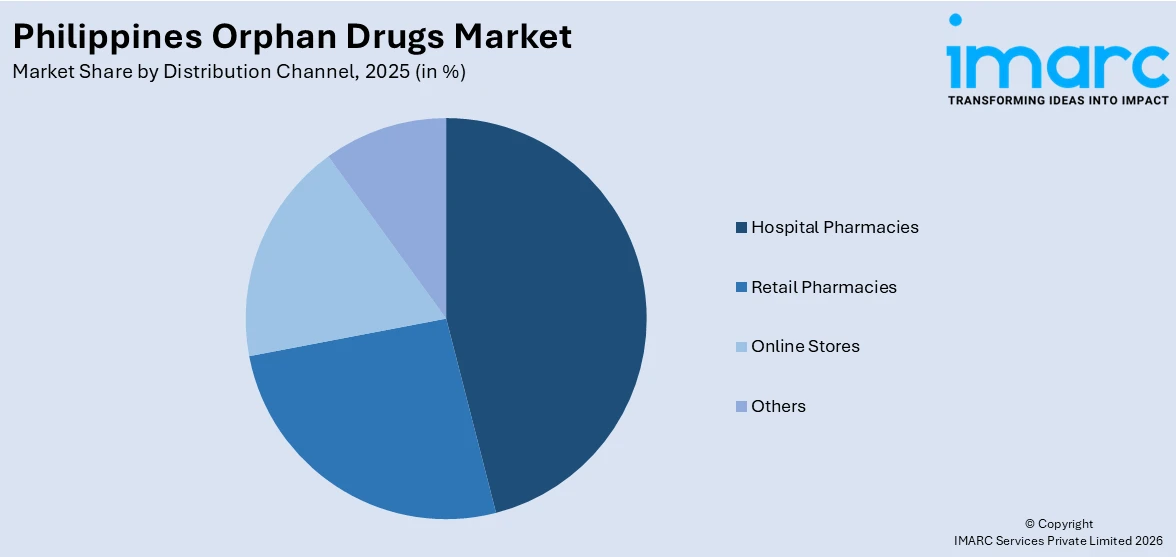

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Hospital Pharmacies

- Retail Pharmacies

- Online Stores

- Others

A detailed breakup and analysis of the market based on the distribution channel have also been provided in the report. This includes hospital pharmacies, retail pharmacies, online stores, and others.

Regional Insights:

- Luzon

- Visayas

- Mindanao

The report has also provided a comprehensive analysis of all the major regional markets, which includes Luzon, Visayas, and Mindanao.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Philippines Orphan Drugs Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Drug Types Covered | Biological, Non-Biological |

| Disease Types Covered | Oncology, Hematology, Neurology, Cardiovascular, Others |

| Phases Covered | Phase I, Phase II, Phase III, Phase IV |

| Top Selling Drugs Covered | Revlimid, Rituxan, Copaxone, Opdivo, Keytruda, Imbruvica, Avonex, Sensipar, Soliris, Others |

| Distribution Channels Covered | Hospital Pharmacies, Retail Pharmacies, Online Stores, Others |

| Regions Covered | Luzon, Visayas, Mindanao |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Philippines orphan drugs market performed so far and how will it perform in the coming years?

- What is the breakup of the Philippines orphan drugs market on the basis of drug type?

- What is the breakup of the Philippines orphan drugs market on the basis of disease type?

- What is the breakup of the Philippines orphan drugs market on the basis of phase?

- What is the breakup of the Philippines orphan drugs market on the basis of top selling drugs?

- What is the breakup of the Philippines orphan drugs market on the basis of distribution channel?

- What is the breakup of the Philippines orphan drugs market on the basis of region?

- What are the various stages in the value chain of the Philippines orphan drugs market?

- What are the key driving factors and challenges in the Philippines orphan drugs market?

- What is the structure of the Philippines orphan drugs market and who are the key players?

- What is the degree of competition in the Philippines orphan drugs market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Philippines orphan drugs market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Philippines orphan drugs market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Philippines orphan drugs industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)