Philippines Salmon Market Size, Share, Trends and Forecast by Type, Species, End Product Type, Distribution Channel, and Region, 2026-2034

Philippines Salmon Market Summary:

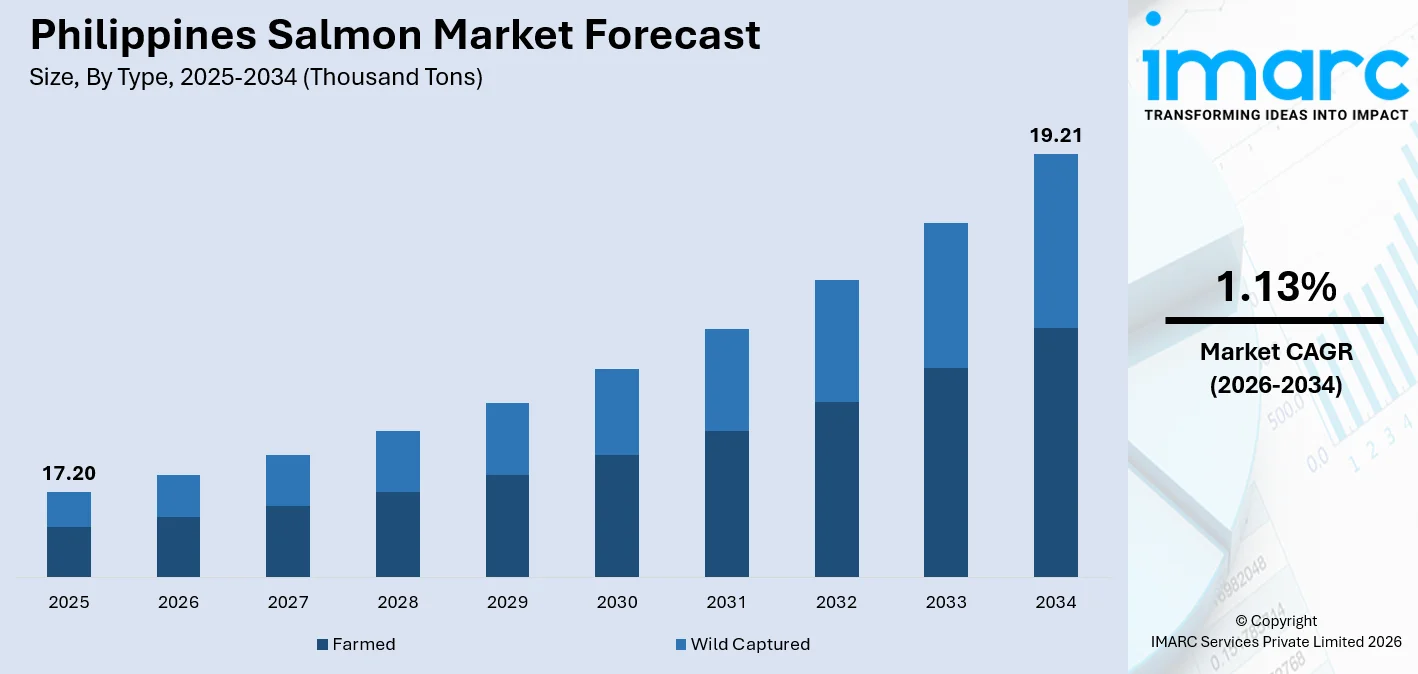

The Philippines salmon market size reached 17.20 Thousand Tons in 2025 and is projected to reach 19.21 Thousand Tons by 2034, growing at a compound annual growth rate of 1.13% from 2026-2034.

The Philippines salmon market is experiencing steady growth, supported by increasing health awareness among consumers and ongoing urban development. Expanding middle-class purchasing power and the rising popularity of Asian-inspired cuisines are boosting demand for salmon across households and dining establishments. At the same time, improvements in cold chain infrastructure are enhancing product availability and quality nationwide. These factors are collectively making salmon more accessible and widely consumed, contributing to the continued expansion of the market across diverse consumer segments.

Key Takeaways and Insights:

- By Type: Farmed salmon dominates the market with a share of 72.5% in 2025, owing to consistent year-round supply availability, stable pricing, and reliable product quality delivered through advanced controlled aquaculture practices.

- By Species: Atlantic salmon leads the market with a share of 68.5% in 2025, favored for its superior flavor profile, rich marbling, high omega-3 content, and wide availability across both foodservice and retail channels.

- By End Product Type: Fresh salmon holds the largest share of 48.5% in 2025, reflecting strong consumer preference for high-quality, minimally processed protein in restaurants, hotels, and premium retail outlets.

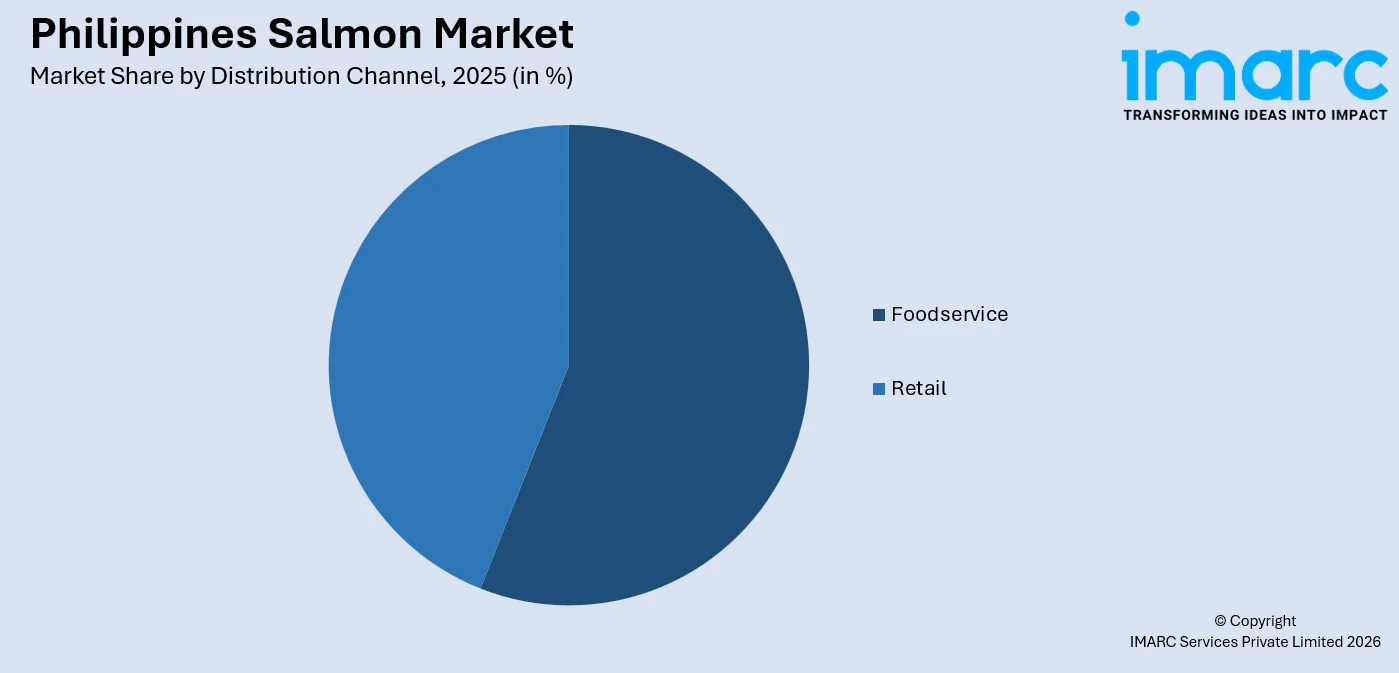

- By Distribution Channel: Foodservice accounts for 55.5% of the market in 2025, driven by the rapid expansion of sushi restaurants, hotel dining facilities, and international fast-casual chains across major urban centers.

- By Region: Luzon represents the leading regional segment with a 68.5% share in 2025, supported by the concentration of the country's largest urban populations, premium foodservice establishments, and sophisticated retail infrastructure in Metro Manila and surrounding cities.

- Key Players: The Philippines salmon market features a competitive landscape of international importers and domestic distributors competing on product freshness, supply chain reliability, and pricing. Market participants are focusing on cold chain investments, expanding partnerships with foodservice operators and modern retailers, and leveraging traceability systems to differentiate their offerings.

To get more information on this market Request Sample

The Philippines salmon market is sustained by growing urbanization, rising health awareness, and a vibrant foodservice sector. Filipino consumers increasingly associate salmon with nutritious eating, fueling demand across restaurants, hotels, and grocery chains. The expansion of modern supermarket networks, including chains operating over 300 stores nationwide, has improved salmon accessibility for urban households. Cold chain infrastructure is also improving; the Philippines' National Cold Chain Roadmap allocates approximately PHP 8 billion toward expanding refrigerated logistics, extending the fresh salmon shipping window and enabling distribution to previously underserved tier-2 cities. Imports from key supplying countries such as Chile and Norway continue to underpin salmon availability in the Philippines. Supported by rising consumer preference for nutrient-rich protein sources, these supply dynamics are contributing to sustained growth and strengthening the overall market outlook.

Philippines Salmon Market Trends:

Growing Integration of Salmon into Filipino Foodservice Culture

Salmon has become a cornerstone ingredient in the Philippines' rapidly expanding foodservice sector. Sushi restaurants, Japanese dining chains, and Western-influenced casual establishments across Metro Manila and major provincial cities have incorporated salmon dishes as menu staples. Younger Filipino consumers, driven by exposure to Korean and Japanese food culture through social media and travel, are actively seeking premium seafood experiences. This cultural shift is reinforcing sustained demand from the hospitality sector and encouraging chefs to develop locally adapted salmon recipes, further normalizing salmon as a prominent everyday protein contributing to Philippines salmon market growth.

Cold Chain Modernization Enhancing Fresh Salmon Distribution

Investment in cold chain infrastructure is transforming the availability and quality of fresh salmon across the Philippines. The Philippines' National Cold Chain Roadmap allocates PHP 8 billion toward refrigerated logistics, extending the fresh salmon shipping window and unlocking distribution in previously underserved tier-2 cities. From 2021 to 2024, private cold storage developers added nearly 150,000 new leasable pallet positions, expanding national cold storage capacity by 32 percent. These logistics improvements are enabling faster, more reliable delivery of chilled salmon products, directly supporting the dominance of the fresh product segment in the market.

Rising Health and Nutrition Awareness Driving Premium Seafood Demand

Filipino consumers are increasingly shifting toward health-focused diets, positioning salmon as a preferred premium protein choice. Rising awareness of the cardiovascular and cognitive benefits associated with omega-3 fatty acids is influencing purchasing behavior, particularly among urban households and working professionals. Health-oriented retail formats, improved nutrition labeling, and wellness-driven merchandising are reinforcing salmon’s perception as a nutritious option. Supermarkets and foodservice outlets are expanding fresh seafood offerings to align with these preferences, supporting sustained demand for salmon across both retail and dining segments.

Market Outlook 2026-2034:

The Philippines salmon market is positioned for steady expansion through the forecast period, supported by a maturing foodservice industry, improving cold chain infrastructure, and a health-conscious consumer base. Rising disposable incomes in urban centers, growing exposure to international food trends, and investments in salmon distribution logistics are expected to sustain consistent consumption growth across the country. Additionally, the expanding presence of premium retail formats and organized seafood distribution channels will further enhance product availability and market penetration. The market size was estimated at 17.20 Thousand Tons in 2025 and is expected to reach 19.21 Thousand Tons by 2034, reflecting at a compound annual growth rate of 1.13% over the forecast period 2026-2034.

Philippines Salmon Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Farmed |

72.5% |

|

Species |

Atlantic |

68.5% |

|

End Product Type |

Fresh |

48.5% |

|

Distribution Channel |

Foodservice |

55.5% |

|

Region |

Luzon |

68.5% |

Type Insights:

- Farmed

- Wild Captured

Farmed salmon dominates the market share with a 72.5% of the total of Philippines salmon market in 2025.

Farmed salmon accounts for the largest share of the Philippines salmon market due to its consistent availability, standardized quality, and reliable supply from major exporting countries. Unlike wild-caught varieties, farmed salmon can be produced year-round under controlled conditions, ensuring steady import volumes that meet the needs of both foodservice operators and retail channels. Its uniform size, texture, and fat content make it particularly suitable for a wide range of culinary applications, supporting its widespread adoption across restaurants, supermarkets, and institutional buyers.

Additionally, farmed salmon is generally more cost-effective and easier to distribute compared to wild-caught alternatives, making it more accessible to a broader consumer base. Efficient aquaculture practices and well-established global supply chains enable importers to maintain stable pricing and consistent quality. This affordability, combined with its suitability for mass consumption and versatility in preparation, reinforces its dominance in the market, particularly as demand continues to rise among urban consumers seeking convenient and nutritious protein options.

Species Insights:

- Atlantic

- Pink

- Chum/Dog

- Coho

- Sockeye

- Others

Atlantic leads the market share with a 68.5% of the total of Philippines salmon market in 2025.

Atlantic salmon holds the leading share in the Philippines salmon market due to its consistent availability through well-established global aquaculture systems. Sourced primarily from major producing countries, it benefits from year-round production, ensuring reliable supply for importers and distributors. Its uniform size, appealing color, and balanced fat content make it highly suitable for a wide range of culinary applications, including sushi, grilling, and baking. This consistency is particularly valued by foodservice operators and retailers seeking dependable quality for large-scale and repeat consumption.

Additionally, Atlantic salmon offers a favorable balance between quality and affordability, making it accessible to a broader segment of consumers compared to other salmon varieties. Its mild flavor and tender texture align well with local taste preferences and diverse cooking styles, further supporting its popularity. Strong cold chain networks and efficient distribution systems also facilitate its widespread availability across supermarkets and restaurants, reinforcing its dominant position in the market as demand for premium seafood continues to grow.

End Product Type Insights:

- Frozen

- Fresh

- Canned

- Others

Fresh represent the largest share of 48.5% in the Philippines salmon market in 2025.

Fresh salmon holds the largest share in the Philippines market, driven by strong demand from upscale restaurants, hotel kitchens, and premium retail outlets that prioritize quality and sensory appeal. Its superior texture, flavor, and visual appeal compared to frozen alternatives make it the preferred choice for sashimi and other high-end culinary applications. Enhancements in cold chain logistics and temperature-controlled distribution have improved product freshness and shelf life, enabling wider availability of fresh salmon across major urban centers and supporting its growing adoption.

Premium supermarkets in urban areas actively position fresh salmon as a high-value product, catering to health-conscious and affluent consumers seeking nutritious, high-quality seafood options. Carefully curated fresh seafood selections and a focus on wellness-driven consumption trends further strengthen its appeal. At the same time, strong demand from the restaurant sector, where fresh salmon is often featured in premium menu offerings, reinforces its leading position. These combined retail and foodservice dynamics continue to support the dominance of fresh salmon in the Philippine market.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Foodservice

- Retail

Foodservice lead the highest revenue share of 55.5% in the Philippines salmon market in 2025.

The foodservice channel drives the majority of salmon consumption in the Philippines, fueled by a rapidly expanding restaurant landscape in Metro Manila and major urban centers. Japanese dining establishments, international hotel chains, and fast-casual sushi concepts have collectively mainstreamed salmon as a key menu ingredient. The Bureau of Fisheries and Aquatic Resources' strategic plan for 2023–2028 includes strengthening post-harvest cold chain technologies and food safety standards, initiatives that are improving supply chain integrity and giving foodservice operators greater confidence in sourcing fresh and frozen salmon consistently throughout the year.

Hotels, catering companies, and upscale dining establishments represent the most significant sub-segment of the foodservice channel, where per-plate premium pricing for salmon dishes justifies higher procurement costs. With international hotel chains penetrating provincial Philippine cities and with domestic restaurant chains launching menus based on Japanese cuisine, salmon consumption is now making inroads beyond Metro Manila into the secondary urban markets. The further growth of the HORECA segment, related to its continued spending on kitchen capacity and the diversification of the menu, sustains the dominance of the foodservice channel over the forecast period, which in turn secures the position of salmon as a high-end staple in the changing food culture in the country.

Regional Insights:

- Luzon

- Visayas

- Mindanao

Luzon exhibits clear dominance with a 68.5% share of the total Philippines salmon market in 2025.

Luzon's commanding share of the Philippines salmon market is anchored by the demographic and economic concentration of Metro Manila and surrounding urban growth corridors. The National Capital Region hosts thousands of restaurants, international hotels, and modern supermarket branches, creating a dense network of high-volume salmon consumers. The region's superior cold chain infrastructure, proximity to major import ports, and well-developed food distribution networks facilitate efficient salmon delivery from importers to end buyers.

The growing middle-class and young urban professional population in Metro Manila drives premium seafood consumption, particularly fresh Atlantic salmon for Japanese and Western cuisine. Luzon also benefits from private sector cold chain expansion; Ayala Corporation's cold storage subsidiary Artico is adding over 10,000 new pallet positions across planned facilities in Santa Rosa, Laguna and Consolacion, Cebu, improving salmon storage and distribution efficiency. These infrastructure investments, combined with robust restaurant sector activity and premium retail expansion in Luzon's central business districts, reinforce the region's dominant position within the Philippine salmon market.

Market Dynamics:

Growth Drivers:

Why is the Philippines Salmon Market Growing?

Rising Consumer Health Awareness and Demand for Nutritious Seafood

The increasing health consciousness among Filipino consumers is one of the major drivers of the demand for salmon in the country. As society is becoming very conscious of lifestyle diseases (like heart diseases and well-being), consumers are moving to products that contain high nutrient levels, where the health value is high. The main advantage of salmon is that it is commonly viewed as a high-quality and healthy choice, which can contribute to its increasing popularity among urban families, employees, and younger buyers who are guided by the trends of digital healthiness. Retailers are keeping pace with this trend by increasing their fresh seafood selections and focusing on health-oriented positioning, which is aiding in incorporating salmon into the daily meals as well as assisting in sustaining the growth in demand both on the retail and foodservice sides.

Rapid Expansion of Modern Foodservice and Restaurant Sector

The Philippines' foodservice industry continues its robust expansion, anchored by the proliferation of Japanese dining establishments, international hotel operations, and casual dining chains that feature salmon as a key menu ingredient. Metro Manila hosts a dense concentration of sushi restaurants, omakase venues, and international cuisine outlets where salmon dishes command strong consumer interest and premium pricing. The growing influence of Japanese and Korean food culture, amplified through social media and travel, has normalized salmon consumption among younger Filipinos who actively seek authentic culinary experiences. Beyond Metro Manila, provincial cities are witnessing the emergence of Japanese-inspired restaurants and multi-cuisine establishments featuring salmon, creating new demand pockets that extend the market's geographic reach. This broad-based foodservice expansion is driving consistent, high-volume salmon procurement from importers and directly fueling Philippines salmon market growth.

Improving Cold Chain Infrastructure Supporting Wider Distribution

The Philippines’ evolving cold chain infrastructure is significantly improving salmon accessibility beyond major urban centers. Ongoing investments in refrigerated logistics and storage facilities are enabling more efficient transportation and handling of perishable seafood products. Both public and private sector initiatives are strengthening nationwide cold storage networks, allowing distributors to reach emerging cities with greater reliability. These advancements are reducing spoilage risks and maintaining product quality during transit. As a result, fresh and frozen salmon are becoming more widely available across a broader geographic area, supporting market expansion and increasing consumption beyond traditional high-demand locations.

Market Restraints:

What Challenges the Philippines Salmon Market is Facing?

High Price Point Limiting Mass Market Penetration

Salmon remains a premium product category in the Philippines, with retail prices significantly higher than locally available seafood species such as milkfish and tilapia. This pricing differential restricts consistent salmon consumption to middle- and upper-income households, constraining penetration among the broader population. In price-sensitive regional markets outside Metro Manila, the cost barrier slows volume growth and prevents salmon from becoming a mainstream protein choice for most Filipino families.

Complete Dependence on Imported Supply Creating Market Vulnerability

The Philippines does not produce salmon domestically, making the market entirely reliant on imports from Chile, Norway, and other producing nations. This dependency exposes the market to supply disruptions caused by currency fluctuations, shipping delays, trade policy changes, and aquaculture production challenges in source countries. Any deterioration in bilateral trade relations or external logistics disruptions can affect product availability and pricing stability, creating inherent vulnerability within the market's supply chain structure.

Cold Chain Gaps Restricting Distribution in Secondary Markets

Despite ongoing infrastructure investment, the Philippine cold chain remains underdeveloped in many provincial areas. The Bureau of Fisheries and Aquatic Resources highlights significant postharvest losses driven by limited cold storage and blast freezing capacity. These infrastructure gaps constrain salmon distribution to major urban areas, limiting expansion into smaller cities where demand for premium imported seafood is gradually rising.

Competitive Landscape:

The Philippines salmon market features a competitive distribution environment led by specialized seafood importers and food distributors sourcing primarily from international suppliers. Competition centers on supply chain reliability, strong cold chain infrastructure, consistent product freshness, and a diverse range of salmon offerings tailored to foodservice and retail needs. Market participants are actively expanding their distribution reach, building partnerships with hotels and restaurant chains, and enhancing temperature-controlled logistics to strengthen their positioning. At the same time, premium retail channels are emerging as key competitive spaces, with modern grocery formats increasingly offering imported fresh salmon to meet the preferences of health-conscious urban consumers.

Philippines Salmon Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Thousand Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Farmed, Wild Captured |

| Species Covered | Atlantic, Pink, Chum/Dog, Coho, Sockeye, Others |

| End Product Types Covered | Frozen, Fresh, Canned, Others |

| Distribution Channels Covered | Foodservice, Retail |

| Regions Covered | Luzon, Visayas, Mindanao |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Philippines Salmon Market Report

The Philippines salmon market size reached 17.20 Thousand Tons in 2025.

The Philippines salmon market is expected to grow at a compound annual growth rate of 1.13% from 2026-2034 to reach 19.21 Thousand Tons by 2034.

Farmed salmon, holding the largest share of 72.5% in 2025, dominates the Philippines salmon market owing to its consistent year-round supply, predictable quality, and competitive pricing compared to wild-caught alternatives, making it the preferred choice across both foodservice and retail distribution channels.

Key factors driving the Philippines salmon market include rising health consciousness among Filipino consumers, the rapid expansion of the foodservice and restaurant sector, improving cold chain infrastructure, growing middle-class incomes, and the increasing cultural acceptance of salmon as a premium everyday protein across urban markets.

Major challenges facing the Philippines salmon market include the premium price point that limits mass market penetration, complete dependence on imported supply which creates vulnerability to trade and logistics disruptions, inadequate cold chain infrastructure in secondary markets, and significant postharvest loss rates that constrain product quality and availability outside major urban centers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)