Philippines Silicon Wafer Market Size, Share, Trends and Forecast by Wafer Size, Type, Application, End Use, and Region, 2026-2034

Philippines Silicon Wafer Market Summary:

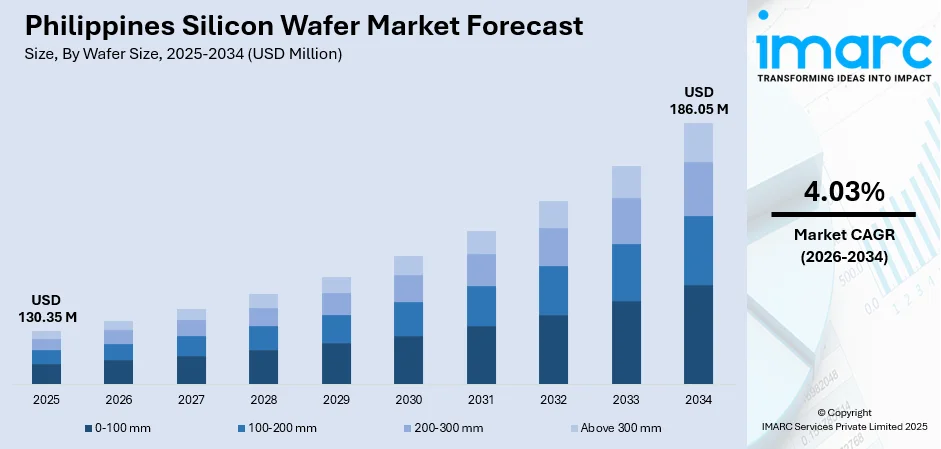

The Philippines silicon wafer market size was valued at USD 130.35 Million in 2025 and is projected to reach USD 186.05 Million by 2034, growing at a compound annual growth rate of 4.03% from 2026-2034.

The market is driven by the expanding electronics manufacturing sector, increasing demand for semiconductor components, and growing investments in technology infrastructure development. Rising adoption of advanced electronic devices, coupled with the flourishing automotive electronics segment and renewable energy applications, is propelling market expansion. Government initiatives supporting digital transformation and the establishment of manufacturing facilities are further strengthening the Philippines silicon wafer market share.

Key Takeaways and Insights:

-

By Wafer Size: 200-300 mm dominates the market with a share of 40.06% in 2025, driven by manufacturing efficiency, broad equipment compatibility, and high demand from integrated circuit manufacturers seeking larger wafers for optimized yield.

-

By Type: N-Type leads the market with a share of 60.04% in 2025, owing to superior electron mobility, enhanced high-performance efficiency, growing preference in advanced semiconductor fabrication, and adoption in next-generation solar cells requiring premium electrical properties.

-

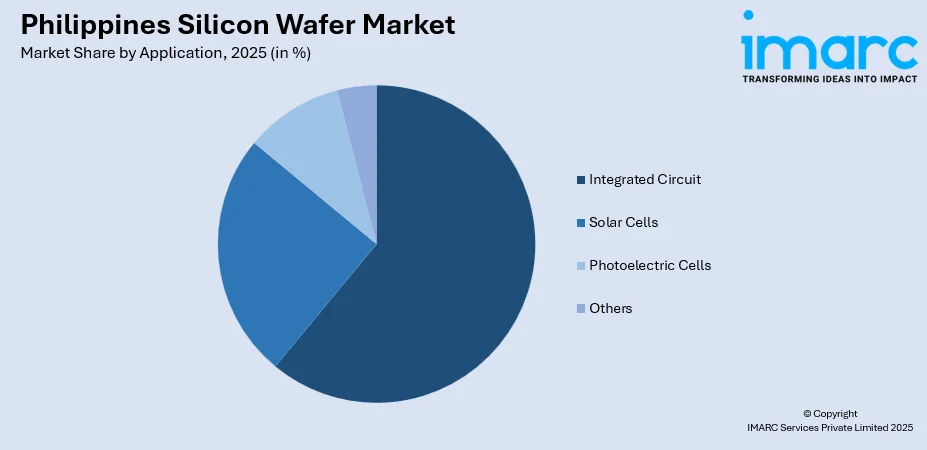

By Application: Integrated circuit represents the largest segment with a market share of 60.12% in 2025, driven by rising demand for microprocessors, memory chips, consumer electronics expansion, automotive semiconductor growth, and deployment of smart devices requiring advanced IC components.

-

By End Use: Consumer electronics dominates the market with a share of 40.1% in 2025, owing to increasing smartphone penetration, higher laptop and tablet demand, smart home device adoption, and a growing digital entertainment sector boosting silicon wafer consumption.

-

Key Players: The Philippines silicon wafer market exhibits a moderately consolidated competitive landscape, with established semiconductor material suppliers competing alongside regional manufacturers. Market participants focus on technological innovation, strategic partnerships, and capacity expansion to strengthen their positioning across various wafer specifications and application segments.

To get more information on this market Request Sample

The Philippines silicon wafer market is experiencing robust growth, propelled by the nation's strategic positioning as a semiconductor manufacturing hub in Southeast Asia. The expanding electronics manufacturing services sector is generating substantial demand for high-quality silicon wafers across diverse applications. Government initiatives promoting technology investments and favorable policies encouraging foreign direct investment in semiconductor facilities are accelerating market development. As per sources, in July 2025, PANJIT International inaugurated a new semiconductor manufacturing facility in Cabuyao, Laguna, Philippines, enhancing backend production capabilities, supply chain resilience, and support for automotive, industrial, and consumer electronics sectors. Furthermore, the rising adoption of advanced technologies, including artificial intelligence (AI), Internet of Things (IoT), and electric vehicles (EVs), is creating significant demand for sophisticated semiconductor components. The country's skilled workforce and competitive manufacturing costs continue attracting global technology companies, further stimulating silicon wafer consumption across integrated circuits, solar cells, and photoelectric applications.

Philippines Silicon Wafer Market Trends:

Transition Toward Larger Wafer Diameters

The market is witnessing a significant shift toward larger diameter silicon wafers as manufacturers seek enhanced production efficiency and improved economies of scale. Fabrication facilities are increasingly investing in equipment capable of processing larger wafer formats to maximize output per production cycle. In February 2025, US-based Amkor Technology announced expansion of its Philippine operations, enhancing semiconductor device manufacturing, supporting IC design, and leveraging the country’s skilled workforce to strengthen local semiconductor industry capabilities. Moreover, this transition enables higher chip yields per wafer, reducing per-unit manufacturing costs while meeting escalating demand for semiconductor components. The adoption of advanced wafer handling technologies and precision processing equipment supports this trend, allowing manufacturers to maintain stringent quality standards while processing larger substrates for diverse electronic applications.

Growing Emphasis on Advanced Semiconductor Materials

Manufacturers are increasingly focusing on developing silicon wafers with enhanced purity levels and improved crystalline structures to meet the demanding specifications of next-generation electronic devices. The integration of advanced material processing techniques enables the production of wafers with superior electrical properties and reduced defect densities. Research and development initiatives are concentrating on optimizing wafer characteristics for emerging applications requiring exceptional performance reliability. As per sources, in 2025, the Philippine government established the Semiconductor and Electronics Industry Advisory Council to enhance competitiveness, guide strategic growth, and support advanced semiconductor materials and technology development nationwide. This emphasis on material advancement is driving innovation in wafer manufacturing processes, enabling the production of substrates suitable for cutting-edge semiconductor technologies and sophisticated electronic systems.

Integration of Sustainable Manufacturing Practices

The silicon wafer industry is experiencing increasing adoption of environmentally responsible manufacturing methodologies aimed at reducing resource consumption and minimizing waste generation. Manufacturers are implementing water recycling systems, energy-efficient processing equipment, and advanced filtration technologies to decrease environmental impact throughout production operations. The utilization of renewable energy sources in fabrication facilities is gaining momentum as companies pursue sustainability objectives. In October 2025, SEIPI hosted the 20th PSECE in Pasay City, featuring 178 exhibitors and 7,460 trade visitors, highlighting sustainable and intelligent manufacturing in the Philippine semiconductor and electronics industry. These initiatives extend to supply chain optimization, with emphasis on responsible sourcing practices and circular economy principles that promote material recovery and recycling throughout the wafer manufacturing lifecycle.

Market Outlook 2026-2034:

The Philippines silicon wafer market is poised for substantial revenue growth throughout the forecast period, supported by expanding semiconductor manufacturing activities and increasing technology investments. The market is anticipated to generate significant revenue as demand escalates across consumer electronics, automotive, industrial, and telecommunications sectors. Strategic government initiatives promoting digital infrastructure development and technology ecosystem expansion will contribute to market advancement. Rising investments in fabrication facilities and growing partnerships between global semiconductor companies and local manufacturers are expected to strengthen the market trajectory through the forecast duration. The market generated a revenue of USD 130.35 Million in 2025 and is projected to reach a revenue of USD 186.05 Million by 2034, growing at a compound annual growth rate of 4.03% from 2026-2034.

Philippines Silicon Wafer Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Wafer Size |

200-300 mm |

40.06% |

|

Type |

N-Type |

60.04% |

|

Application |

Integrated Circuit |

60.12% |

|

End Use |

Consumer Electronics |

40.1% |

Wafer Size Insights:

- 0-100 mm

- 100-200 mm

- 200-300 mm

- Above 300 mm

The 200 - 300 mm dominates with a market share of 40.06% of the total Philippines silicon wafer market in 2025.

The 200-300 mm commands the leading market position, driven by its optimal balance between manufacturing complexity and production efficiency. This wafer diameter range offers significant advantages in integrated circuit fabrication, enabling manufacturers to produce a higher number of chips per wafer while maintaining acceptable defect rates. The widespread availability of processing equipment designed for these wafer dimensions facilitates adoption across established and emerging fabrication facilities, supporting consistent market demand.

Manufacturing infrastructure investments continue favoring the 200-300 mm segment as facilities seek to maximize return on capital expenditure through optimized production volumes. The compatibility of these wafer sizes with advanced lithography systems and processing technologies enables the production of sophisticated semiconductor devices meeting contemporary performance requirements. Furthermore, supply chain maturity for this wafer category ensures reliable material availability and competitive pricing, reinforcing its dominant market positioning across diverse application segments.

Type Insights:

- N-Type

- P-Type

N-type leads with a share of 60.04% of the total Philippines silicon wafer market in 2025.

N-type dominate the market owing to their superior electron mobility characteristics and enhanced performance attributes in demanding semiconductor applications. These wafers exhibit excellent conductivity properties achieved through phosphorus or arsenic doping, making them particularly suitable for high-frequency and high-power electronic devices. The growing adoption of N-type substrates in advanced photovoltaic applications, where they demonstrate improved efficiency and reduced degradation, further strengthens this segment's market leadership. As per sources, in May 2025, Gstar Subic, Philippines, officially launched its first N-type high-efficiency solar module with 183.75mm cells, 595W peak output, and 23.03% conversion efficiency, marking the factory’s operational start.

The preference for N-type extends across integrated circuit manufacturing, where their electrical properties enable the production of high-performance processors and memory components. Research advancements continue optimizing N-type wafer characteristics for emerging applications requiring exceptional carrier lifetime and reduced light-induced degradation. The expanding base of manufacturing facilities equipped for N-type wafer processing supports market growth, while ongoing material science innovations enhance the competitive advantages of this wafer type across consumer electronics and industrial applications.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Solar Cells

- Integrated Circuit

- Photoelectric Cells

- Others

Integrated circuit exhibits a clear dominance with a 60.12% share of the total Philippines silicon wafer market in 2025.

Integrated circuit represent the dominant application segment, reflecting the fundamental role of silicon wafers in semiconductor device manufacturing. The escalating demand for microprocessors, memory chips, and system-on-chip solutions across computing, communications, and consumer electronics sectors drives substantial wafer consumption in this category. Manufacturing complexity continues advancing as circuit dimensions shrink, requiring increasingly precise wafer specifications and superior material quality to enable next-generation device production.

The proliferation of smart devices, expansion of data center infrastructure, and growth in automotive electronics are amplifying integrated circuit demand and corresponding silicon wafer requirements. Moreover, advanced packaging technologies and heterogeneous integration approaches are creating additional wafer consumption as semiconductor architectures evolve. The Philippines' strategic positioning in the global electronics manufacturing ecosystem positions local and international manufacturers to capitalize on growing integrated circuit production, sustaining the dominant position of this application segment.

End Use Insights:

- Consumer Electronics

- Automotive

- Industrial

- Telecommunication

- Others

Consumer electronics dominates with a market share of 40.1% of the total Philippines silicon wafer market in 2025.

Consumer electronics represent the largest end-use segment, driven by pervasive demand for smartphones, tablets, laptops, and smart home devices requiring sophisticated semiconductor components. The continuous evolution of consumer devices toward enhanced functionality, improved processing capabilities, and extended connectivity features necessitates advanced silicon wafers for component manufacturing. Rising disposable incomes and increasing technology adoption rates across the Philippines population sustain robust demand growth in this segment.

The segment benefits from accelerating product refresh cycles and expanding device categories as manufacturers introduce innovative products addressing evolving consumer preferences. Gaming consoles, wearable devices, and personal entertainment systems contribute additional demand for silicon wafer-based semiconductor components. The established presence of electronics manufacturing services companies in the Philippines creates direct linkages between consumer electronics production and silicon wafer consumption, reinforcing this segment's market leadership position throughout the forecast period. As per sources, in January 2025, the Philippines secured new leads from US semiconductor and electronics supply chain companies during CES 2025, highlighting potential investments and strengthening the country’s role in the global consumer electronics ecosystem.

Regional Insights:

- Luzon

- Visayas

- Mindanao

Luzon dominates the Philippines silicon wafer market, benefiting from concentrated electronics manufacturing infrastructure in Metro Manila and surrounding industrial zones. The region hosts major semiconductor assembly and testing facilities, creating substantial silicon wafer demand. Advanced transportation networks, skilled workforce availability, and proximity to international shipping ports strengthen Luzon's position as the primary hub for semiconductor-related activities and technology investments.

Visayas represents an emerging market for silicon wafers, supported by growing electronics manufacturing presence in Cebu and expanding industrial development initiatives. The region offers competitive operational costs and improving infrastructure that attract technology investments. Government programs promoting regional economic development and technology sector expansion are encouraging establishment of semiconductor-related facilities, gradually increasing silicon wafer consumption across the Visayas island group.

Mindanao presents growth opportunities for the silicon wafer market as economic development programs advance industrial capabilities across the region. Improving infrastructure connectivity and government incentives supporting manufacturing investments are creating favorable conditions for electronics sector expansion. The region's competitive labor costs and available industrial land position Mindanao for future silicon wafer market development as technology manufacturing activities diversify geographically throughout the Philippines.

Market Dynamics:

Growth Drivers:

Why is the Philippines Silicon Wafer Market Growing?

Expanding Electronics Manufacturing Services Sector

The Philippines has established itself as a prominent destination for electronics manufacturing services, creating substantial demand for silicon wafers across semiconductor production activities. Major global technology companies continue expanding their manufacturing presence in the country, leveraging competitive labor costs, favorable investment policies, and established supply chain networks. This expansion encompasses semiconductor assembly, testing, and packaging operations that require consistent silicon wafer supplies. In March 2024, US State Secretary Antony Blinken visited Amkor Technology Philippines, highlighting increased EMS-SMS investments, reinforcing semiconductor assembly, packaging, and testing expansion, and supporting the country’s growing silicon wafer and electronics manufacturing sector. Further, the growth trajectory of electronics manufacturing services directly correlates with silicon wafer consumption, as increased production volumes necessitate proportionally higher substrate inputs. Government initiatives supporting foreign direct investment and technology sector development further accelerate manufacturing expansion.

Rising Demand for Consumer Electronic Devices

Escalating consumer demand for smartphones, tablets, laptops, and smart home devices is driving significant silicon wafer consumption throughout the Philippine market. As per sources, in October 2025, Home Credit Philippines reported financing 2.5 Million smartphones since early 2024 averaging 5,000 devices daily by August 2025 highlighting strong consumer electronics demand nationwide. Moreover, the growing middle-class population with increasing purchasing power demonstrates strong appetite for advanced electronic products requiring sophisticated semiconductor components. Device manufacturers are responding with expanded product portfolios featuring enhanced specifications that demand higher-quality silicon substrates. The proliferation of connected devices and Internet of Things applications creates additional consumption channels for silicon wafer-based components. Furthermore, shortened product lifecycle and frequent model updates sustain continuous semiconductor production requirements, maintaining robust demand for silicon wafer supplies across consumer electronics applications.

Government Support for Semiconductor Industry Development

Philippine government initiatives promoting semiconductor industry development are creating favorable conditions for silicon wafer market expansion. Strategic policies encouraging technology investments, tax incentives for manufacturing facilities, and infrastructure development programs support semiconductor ecosystem growth. The government's recognition of electronics manufacturing as a priority sector has resulted in dedicated programs facilitating industry advancement. Investment promotion agencies actively attract semiconductor-related businesses through comprehensive support packages and streamlined regulatory processes. These supportive measures extend to workforce development programs producing skilled technicians and engineers essential for semiconductor manufacturing operations, thereby strengthening the foundation for sustained silicon wafer market growth. As per sources, in June 2025, the Philippine government launched the Semiconductor and Electronics Industry Advisory Council (SEIAC) to strengthen semiconductor and IC design development, support EMS-ATP growth, and enhance workforce skills nationwide.

Market Restraints:

What Challenges the Philippines Silicon Wafer Market is Facing?

High Capital Investment Requirements

Silicon wafer manufacturing and processing require substantial capital investments in specialized equipment, cleanroom facilities, and precision instrumentation. These significant upfront costs create barriers for new market entrants and limit expansion capabilities for smaller manufacturers. The technological complexity of wafer production necessitates continuous equipment upgrades to maintain competitiveness, further increasing financial burdens on industry participants and potentially constraining market development.

Supply Chain Vulnerabilities and Import Dependencies

The Philippine silicon wafer market exhibits significant dependence on imported materials and manufacturing equipment from international suppliers. This reliance creates exposure to global supply chain disruptions, currency fluctuations, and geopolitical uncertainties that can impact material availability and pricing stability. Logistics complexities and extended lead times for specialized components introduce operational planning difficulties for manufacturers requiring consistent silicon wafer supplies.

Technical Workforce Availability Constraints

Despite overall workforce availability, specialized technical expertise required for advanced silicon wafer processing remains relatively scarce in the Philippine market. Semiconductor manufacturing demands highly trained personnel proficient in cleanroom operations, precision measurement, and quality control methodologies. Competition for qualified technicians and engineers among electronics manufacturers creates recruitment difficulties and increases operational costs for facilities requiring specialized semiconductor expertise.

Competitive Landscape:

The Philippines silicon wafer market features a moderately consolidated competitive structure characterized by the presence of established international semiconductor material suppliers and regional manufacturing participants. Market competition centers on product quality, technical specifications, pricing strategies, and supply reliability. Leading participants leverage technological capabilities, manufacturing scale, and distribution networks to maintain competitive positioning. Strategic partnerships between global wafer producers and local electronics manufacturers facilitate market access and strengthen customer relationships. Innovation initiatives focus on developing wafers meeting evolving performance requirements for advanced semiconductor applications. Companies are investing in expanded production capacities and enhanced quality control systems to address growing market demand while meeting stringent industry specifications.

Recent Developments:

-

In February 2024, the Philippine government, through the Board of Investments, announced plans to establish a lab-scale wafer fabrication plant to support semiconductor design, prototyping, and workforce training, aiming to develop 128,000 engineers and technicians by 2028, with US assistance under the CHIPS Act for assembly, testing, and packaging.

Philippines Silicon Wafer Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Wafer Size Covered | 0-100 mm, 100-200 mm, 200-300 mm, Above 300 mm |

| Type Covered | N-Type, P-Type |

| Application Covered | Solar Cells, Integrated Circuit, Photoelectric Cells, Others |

| End Use Covered | Consumer Electronics, Automotive, Industrial, Telecommunication, Others |

| Regional Covered | Luzon, Visayas, Mindanao |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Philippines Silicon Wafer Market Report

The Philippines silicon wafer market size was valued at USD 130.35 Million in 2025.

The Philippines silicon wafer market is expected to grow at a compound annual growth rate of 4.03% from 2026-2034 to reach USD 186.05 Million by 2034.

The 200-300mm held the largest share of the Philippines silicon wafer market, driven by its optimal balance of manufacturing efficiency, broad compatibility with fabrication equipment, and strong demand from integrated circuit manufacturers seeking higher yield.

Key factors driving the Philippines silicon wafer market include expanding electronics manufacturing services sector, rising consumer electronics demand, government support for semiconductor industry development, growing automotive electronics applications, and increasing technology infrastructure investments.

Major challenges include high capital investment requirements for manufacturing facilities, supply chain vulnerabilities and import dependencies, technical workforce availability constraints, intense global competition, and technology transfer limitations affecting domestic production capabilities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)