Philippines Telecommunications Market Size, Share, Trends and Forecast by Component, Enterprise Size, Industry, and Region, 2026-2034

Philippines Telecommunications Market Overview:

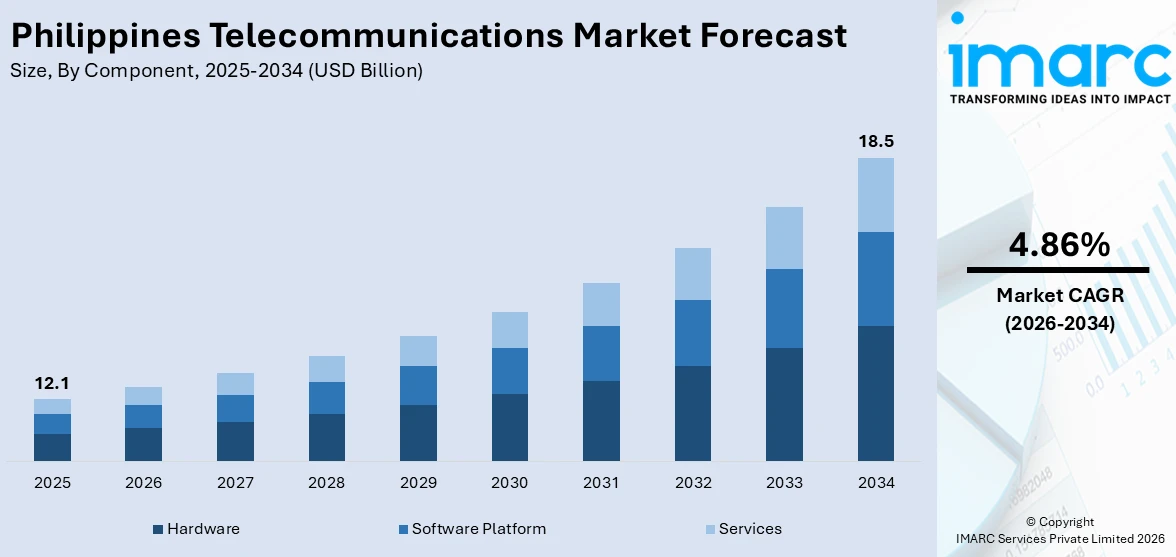

The Philippines telecommunications market size reached USD 12.1 Billion in 2025. Looking forward, the market is expected to reach USD 18.5 Billion by 2034, exhibiting a growth rate (CAGR) of 4.86% during 2026-2034. The expanding mobile connectivity, rising smartphone adoption, surging data demand, enhancing rural coverage, e-commerce growth, ongoing digital transformation, 5G deployment, increased government support and strong investments in network infrastructure and fiber optic expansion are some of the key factors positively impacting the Philippines telecommunications market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 12.1 Billion |

| Market Forecast in 2034 | USD 18.5 Billion |

| Market Growth Rate (2026-2034) | 4.86% |

Key Trends of Philippines Telecommunications Market:

Rapid Expansion of 5G Networks:

The rollout of 5G networks is boosting internet speeds, cutting latency and transforming the telecommunications landscape in the Philippines. According to the latest industry report, nearly half of mobile connections in the Philippines are expected to be over 5G technology by 2030, a significant increase from just 6% of connections in 2023. Telecom operators are expanding 5G infrastructure in urban areas to meet the growing demand for high-speed data services in the region. This technology is enabling advanced applications like virtual reality (VR), cloud gaming, and Internet of Things (IoT) solutions, catering to the tech-savvy consumers and businesses. Moreover, partnerships between global tech providers and telecom companies are significantly driving the widespread adoption of 5G. Additionally, government support including spectrum allocations is fostering 5G deployment and improving the connectivity across various sectors, such as healthcare, education, and e-commerce. These efforts aim to enhance user experience and strengthen the country’s position in the digital economy, thereby supporting the Philippines telecommunications market growth.

To get more information on this market Request Sample

Increasing Mobile Internet Usage:

Mobile internet usage in the Philippines is on the rise, driven by affordable smartphones and data packages. According to an industry report, the Philippines had 86.98 million internet users as of January 2024. By the beginning of 2024, the internet penetration rate among the region's population was 73.6 percent. A large portion of the population, especially younger people, depends on mobile internet for social media, streaming, and online shopping. Telecom companies are tapping into this trend by offering competitively priced data bundles, catering to different income groups. The shift toward mobile-first behaviors is also boosting the growth of fintech services, mobile apps, and digital payments, that rely on strong telecommunications infrastructure. Furthermore, the expanding mobile internet coverage in the rural areas is helping bridge the digital divide and reach underserved regions. These efforts are improving connectivity, supporting the country’s digital economy, and driving the growth of mobile services, thereby fostering the market expansion.

Growth of Fiber-Optic Connectivity:

Fiber-optic network deployment is gaining momentum due to the rising demand of consumers and businesses for more reliable and high-speed internet. Heavy investments in the fiber infrastructure are made to meet the growing demands for video conferencing, remote work, and online education. For example, on October 10, 2024, the World Bank approved EUR 268.22 Million in funding for the Philippines Digital Infrastructure Project, aiming to enhance climate-resilient, secure, and inclusive broadband connectivity nationwide. This initiative will complete the national fiber optic backbone, extend middle-mile infrastructure to underserved regions, and develop last-mile connections in currently unserved areas. Additionally, the surging need for data-intensive services and applications is driving the demand for faster and stable connections. Furthermore, collaborations with real estate developers and local governments are helping with the faster installation of fiber lines in both residential and commercial areas. Moreover, fiber-optic connectivity is expanding, reshaping the broadband landscape and reducing reliance on traditional digital subscriber line (DSL) and wireless solutions, which is positively influencing the Philippines telecommunications market outlook.

Growth Drivers of Philippines Telecommunications Market:

Private Sector Investments and Modernization of Infrastructure

The Philippines telecom market has recorded significant expansion boosted by extensive private sector investments and large-scale modernization of infrastructure. The archipelagic nature of the country previously presented a real challenge to expanding and making a stable telecom network. Nevertheless, there has been heightened investment in upgrading and expanding fiber optic cables and cell towers in both urban areas and rural islands by major telecommunications firms in the recent past. This pressure has been aided by new entrants into the market, disrupting the historic duopoly and encouraging more ambitious infrastructure rollouts. Firms are now investing heavily in 4G and 5G technology, with a view to filling digital gaps and enhancing internet speeds. The government has also aided this shift by making the process of obtaining permits for constructing telecom towers streamlined, thus eliminating bureaucratic delays that had stalled growth in the past. This public-private undertaking is facilitating greater and rapid connectivity across the nation, setting the stage for an inclusive digital economy and further driving telecom market expansion.

Digital Lifestyle Transition and Higher Mobile Penetration

One of the key drivers of growth in the Philippines telecom market is the transition toward a digital lifestyle and the high level of mobile phone penetration of the population. Filipinos are some of the most internet and social media active users globally, and mobile phones have been the leading device for internet access. This strong penetration of mobile technology in everyday life has ignited interest in better and cheaper mobile data services. From digital banking and online learning to mobile gaming and streaming, life in the Philippines has shifted online, and there is a heavy reliance on mobile networks. E-commerce, ride-hailing, and food delivery apps have also compelled consumers to have stable mobile connectivity. This trend has encouraged telecom companies to develop more adaptive data plans, launch innovative digital platforms, and invest in communication, entertainment, and financial services-integrated apps. The Philippines' youth-driven digital culture continues to sustain fast-paced growth in mobile telecom consumption and overall market growth.

Government Policies and Regional Connectivity Programs

According to the Philippines telecommunications market analysis, the government has introduced a sequence of policy and regulatory reforms that are directly leading to the expansion of the telecommunications sector. One such initiative is the creation of the Department of Information and Communications Technology (DICT), which is primarily responsible for formulating the digital infrastructure of the country. The National Broadband Plan seeks to enhance internet access, especially in underserved remote and rural regions, by establishing a government-operated backbone network. Furthermore, public Wi-Fi initiatives have been introduced to offer free internet in schools, public squares, and government buildings. Another significant development is the demand for a competitive telecom sector, including the arrival of a third major telecom operator, aimed at enhancing services and cutting consumers' bills. Such government initiatives for decentralization of digital access and market competition are crucial in a nation with wide regional imbalances. By focusing on inclusive digital transformation, the government is helping to ensure that telecom growth reaches all sectors of society.

Opportunity of Philippines Telecommunications Market:

Expanding Rural Connectivity and Underserved Markets

A major opportunity in the Philippines telecommunications market lies in expanding connectivity to rural and underserved areas. The country’s geography, with over 7,000 islands, creates logistical and infrastructural challenges, which has resulted in uneven network coverage. Although major cities like Metro Manila, Cebu, and Davao enjoy strong telecom infrastructure, most rural provinces lag with poor signals, sluggish internet connections, or no connectivity at all. Filling this digital gap is a large growth opportunity for telecom operators. Since education, healthcare, and financial transactions are becoming increasingly dependent on digital platforms, there is growing demand for connectivity even in remotest areas. Telcos that can provide stable, cheap solutions, be it through satellite, wireless broadband, or community-based infrastructure, are poised to gain market share and customer loyalty. Additionally, local governments are themselves actively looking for public-private partnerships to enhance digital connectivity, and this is the opportune moment for telecom operators to invest in decentralized and inclusive network extension, which further leads to the growth of Philippines telecommunications market demand.

Digital Transformation of Enterprises and MSMEs

Another major opportunity in the Philippines telecom market is facilitating the digitalization of domestic businesses, particularly micro, small, and medium enterprises (MSMEs). The MSMEs make up the backbone of the Philippines economy and are increasingly adopting digital solutions to connect with customers, run operations, and boost efficiency. As the MSMEs migrate to e-commerce platforms, cloud-based solutions, and digital payment networks, they need stable internet connectivity and digital communication networks. Telecom operators can capitalize on this demand by providing customized packages that encompass broadband, VoIP, cloud storage, and cyber security solutions. The forced adoption of remote work and hybrid business models during the COVID-19 pandemic has further compounded the demand for resilient telecom services. Enterprises today are investing in digital infrastructure as a long-term investment, establishing a new and emerging market segment for telcos. With proper assistance, the telecom operators can become the focal point for empowering local businesses and pushing national economic resilience via digital tools.

Expansion in Digital Services and Fintech Integration

The quick adoption of digital services like e-wallets, online banking, telemedicine, and streaming services presents new opportunities for telecom operators in the Philippines. As digital activity becomes ubiquitous to daily life, telcos can look to move beyond classical connectivity and become integrated digital service providers. One compelling opportunity in the Philippine market is the high take-up of fintech solutions, mobile wallets and QR payments specifically, even among the unbanked. Telcos that collaborate with, or build, digital financial services can enhance customer interaction and generate new income streams. Further, digital content, particularly video streaming, mobile gaming, and e-learning, continues to fuel intense data usage, and hence it is lucrative for telcos to package content with data packs. The Philippines' youthful, tech-savvy population and strong mobile-first culture make it a fertile ground for the growth of value-added services, positioning telecom companies as key players in the country’s digital ecosystem.

Government Initiatives of Philippines Telecommunications Market:

National Broadband Plan and Infrastructure Development

The Philippine government has recognized the critical role of telecommunications in national development and launched the National Broadband Plan (NBP) to address long-standing issues such as poor internet connectivity and high service costs. This program, championed by the Department of Information and Communications Technology (DICT), aims to create a government-owned and operated broadband network that enhances internet infrastructure throughout the nation. By minimizing reliance on private-sector backbone infrastructure, the government hopes to make connectivity cheaper and accessible, especially in remote provinces and island communities. One important element of the strategy is the installation of fiber-optic and wireless technologies to link national and local government units, schools, health centers, and public institutions. This underlying infrastructure also opens the way for private telecommunications operators to extend services effectively, especially in far-flung and underserved areas. The NBP facilitates digital inclusion and boosts the nation's preparedness for smart governance and digital public services.

Free Wi-Fi for All and Digital Inclusion Programs

As a step toward bridging the digital divide and ensuring equal access to the internet, the Philippine government has instituted the "Free Wi-Fi for All" program, whose objective is to offer internet connectivity for free in public areas. These include transportation terminals, schools, government offices, hospitals, and public parks throughout the Philippines. The program gives top priority to geographically remote and disadvantaged regions, where commercial internet companies have no motive to establish infrastructure because of low profitability. The initiative also assists the government's wider digital literacy agenda by facilitating more citizens' access to online learning, digital government services, and e-commerce. Supplementing this program are initiatives for raising digital literacy through training and information campaigns, particularly among senior citizens, farmers, and tribesmen. These initiatives are intended to make the digital economy accessible and beneficial to all Filipinos, wherever they may be, whatever their socioeconomic status. Such policies make the telecommunications market better by enlarging the base of users and demand for connectivity.

Market Liberalization and Promotion of Competition

Among the most effective government initiatives in recent times is the liberalization of the telecommunication industry with the goal of ending the traditional duopoly and promoting sustainable competition in the market. Directly resulting from this thrust was the entry of the third major telecommunication player, supported by regulation and spectrum allocation from the government. This has led to incumbent operators enhancing service quality, reducing prices, and heavily investing in network upgrades to keep up with the competition. Furthermore, rules have been established to simplify the process of getting permits for constructing cell towers and other telecommunications infrastructure, which used to result in lengthy delays. The government's focus on "ease of doing business" in the industry facilitates both domestic and foreign investors to access the market with greater ease. These reforms stimulate innovation and consumer choice and accelerate nationwide digital transformation. As the regulatory environment becomes more supportive and transparent, the telecommunications market in the Philippines stands to grow stronger and more competitive.

Challenges of Philippines Telecommunications Market:

Geographical Barriers and Infrastructure Limitations

One of the most persistent challenges facing the telecommunications market in the Philippines is its complex geography, which includes over 7,000 islands scattered across the archipelago. This dispersed geography makes it hard and costly to roll out telecommunications infrastructure like fiber-optic cable, cell towers, and base stations. Due to rough terrain, sparse roads, and high freight cost of shipping equipment and materials in most far-flung and rural communities, expansion is greatly slowed down or discouraged. Consequently, they experience poor or no connectivity, estranging millions of Filipinos from digital inclusion. Moreover, natural calamities like typhoons, earthquakes, and floods often destroy telecom infrastructure, particularly in coastal and hilly areas. These eco-vulnerabilities add to the challenges of providing service quality uniformly. Though metropolitan cities like Metro Manila are advanced in networks, the gap between urban and rural coverage is a significant impediment to pursuing digital inclusivity and reliability countrywide.

Regulatory and Bureaucratic Obstacles

Even with recent initiatives aimed at simplifying procedures, bureaucratic and regulatory issues remain to impede growth and efficiency in the Philippine telecommunication industry. Traditionally, telecommunication firms have encountered time-consuming and complicated permitting processes when trying to construct new towers or extend existing infrastructure. Approvals generally involve a series of government agencies and local government entities, each having their own requirements and procedures. These inefficiencies prolong infrastructure projects while also deterring potential investors, both domestic and international. In other instances, local political realities or intermittent policies further complicate the regulatory environment. While the government has instituted reforms to simplify these obstacles, such as curbing the number of permits that must be obtained for tower construction, where adherence to and enforcement of these policies vary between locations. Consequently, telecommunication firms frequently find themselves grappling with inefficient scaling of their businesses. Overcoming these regulatory brakes is crucial to realizing the market's full value and facilitating timely infrastructure build-out throughout the archipelago.

Affordability, Service Quality, and Consumer Trust

The other critical challenge in the Philippines telecom market is matching service affordability with quality, as well as consumer trust building. Most Filipinos, especially those from low-income and rural segments, continue to perceive internet and mobile services as expensive compared to their purchasing capacity. Budgetary limitations tend to push consumers to use prepaid data promos or low-bandwidth plans, potentially constraining the user experience and deterring more intensive digital use. Concurrently, slow internet speed, call drops, and congestion complaints are still prevalent even in the urban areas. These service quality matters also lead to consumer frustration and diminished trust in telecom operators. Additionally, data privacy, cyberattacks, and online scams have become greater concerns with greater internet usage, and this has underscored the necessity for enhanced consumer education and robust cyber security mechanisms. Telecom operators must tackle these challenges to succeed in the long term by providing improved service quality consistency, competitive pricing, and customer care and data protection across all user categories.

Philippines Telecommunications Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the regional level for 2026-2034. Our report has categorized the market based on component, enterprise size, and industry.

Component Insights:

- Hardware

- Broadcast Communication Equipment

- Telecoms Infrastructure Equipment

- Consumer Premise Equipment

- Software Platform

- On-premises

- Cloud

- Services

- Telecommunication Services

- Installation and Integration Services

- Repair and Maintenance Services

- Managed Services

The report has provided a detailed breakup and analysis of the market based on the component. This includes hardware (broadcast communication equipment, telecoms infrastructure equipment, and consumer premise equipment), software platform (on premises, and cloud), and services (telecommunication services, installation and integration services, repair and maintenance service, and manages services)

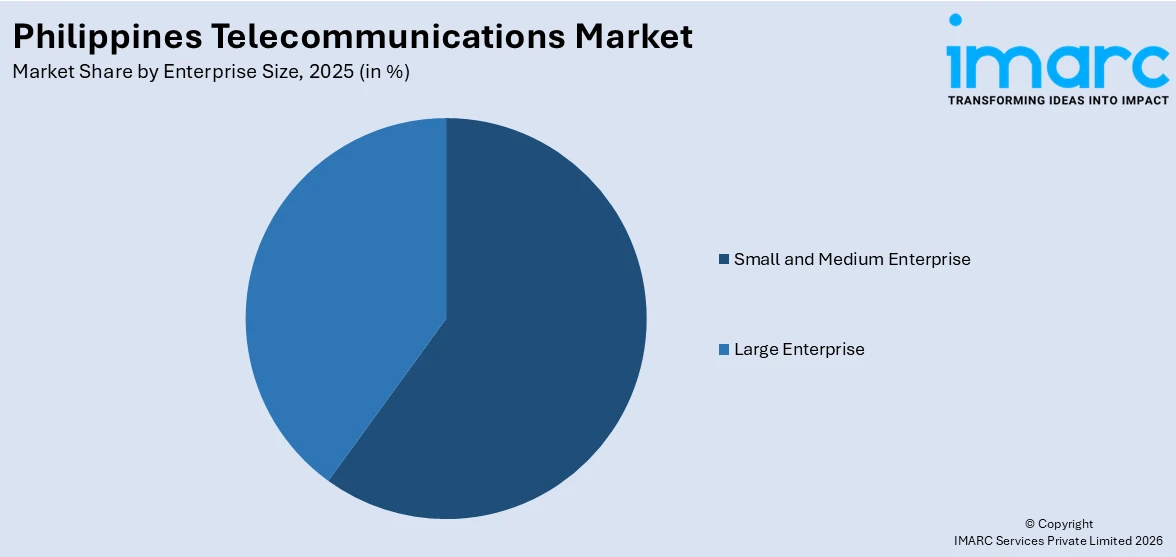

Enterprise Size Insights:

Access the comprehensive market breakdown Request Sample

- Small and Medium Enterprise

- Large Enterprise

A detailed breakup and analysis of the market based on the enterprise sizes have also been provided in the report. This includes small and medium enterprises, and large enterprises.

Industry Insights:

- Retail and E-commerce

- IT and ITES

- Aerospace

- Healthcare and Pharmaceutical

- Media and Entertainment

- Hospitality

- Automotive and Manufacturing

- Transportation and Logistics

- Others

The report has provided a detailed breakup and analysis of the market based on the industry. This includes retail and e-commerce, IT and ITES, aerospace, healthcare and pharmaceutical, media and entertainment, hospitality, automotive and manufacturing, transportation and logistics, and others.

Regional Insights:

- Luzon

- Visayas

- Mindanao

The report has also provided a comprehensive analysis of all the major regional markets, which include Luzon, Visayas, and Mindanao.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Philippines Telecommunications Market News:

- In November 2024, Macquarie, a shareholder in PhilTower, announced its intent to sell their telecom tower assets in the Philippines, a move that would foster the market growth, enhance infrastructure, and support the expansion of mobile and internet services in the country.

- In October 2024, Vitro partnered with HGC to strengthen the data center connectivity in the Philippines, improving digital infrastructure and network performance to support better cloud services and drive the country's digital economy growth.

Philippines Telecommunications Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Enterprise Sizes Covered | Small and Medium Enterprises, Large Enterprises |

| Industries Covered | Retail and E-commerce, IT and ITES, Aerospace, Healthcare and Pharmaceutical, Media and Entertainment, Hospitality, Automotive and Manufacturing, Transportation and Logistics, Others |

| Regions Covered | Luzon, Visayas, Mindanao |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Philippines telecommunications market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Philippines telecommunications market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Philippines telecommunications industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Philippines Telecommunications Market Report

The Philippines telecommunications market was valued at USD 12.1 Billion in 2025.

The Philippines telecommunications market is projected to exhibit a CAGR of 4.86% during 2026-2034.

The Philippines telecommunications market is expected to reach a value of USD 18.5 Billion by 2034.

The Philippines telecommunications market is witnessing trends like rapid 5G rollout, growing demand for fiber-optic broadband, and increased use of mobile wallets and digital platforms. Telcos are diversifying into fintech and content services. Hybrid work, online learning, and streaming are also driving higher data consumption and service innovation across sectors.

The Philippines telecommunications market is driven by rising mobile and internet usage, a young digital-savvy population, and growing demand for online services. Government initiatives, infrastructure investments, and market liberalization support expansion. Increased adoption of e-commerce, remote work, and digital education further fuels the need for reliable, high-speed connectivity nationwide.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)