Philippines Warehousing Market Size, Share, Trends and Forecast by Type, End User, and Region, 2026-2034

Philippines Warehousing Market Size, Share, Trends & Forecast (2026-2034)

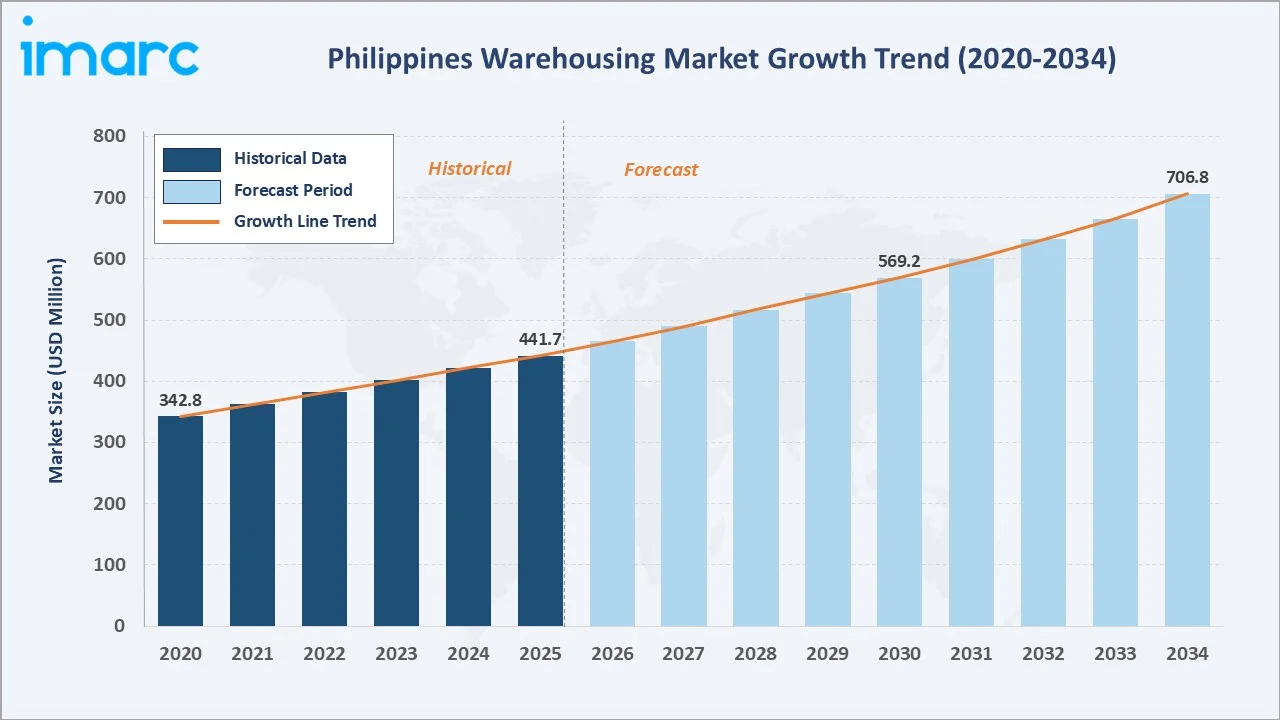

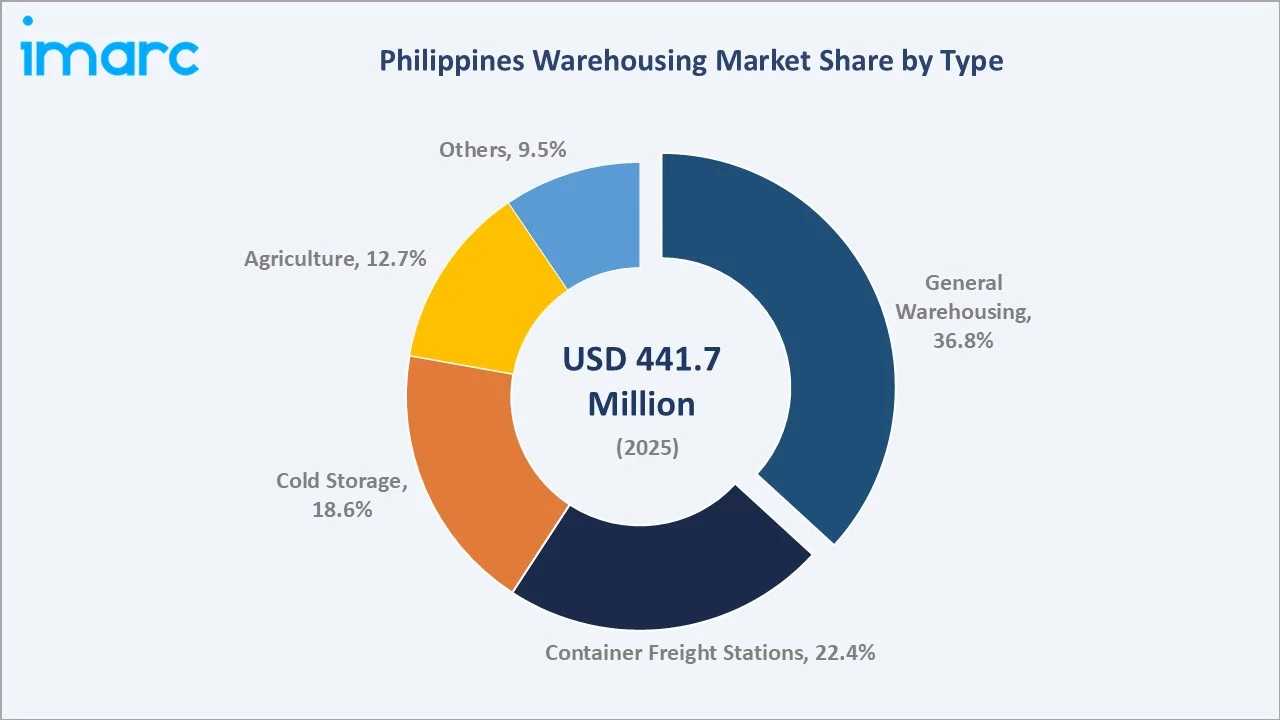

The Philippines warehousing market reached USD 441.7 Million in 2025 and is projected to reach USD 706.8 Million by 2034, growing at a CAGR of 5.20% during 2026-2034. Numerous collaborations between key players, the thriving e-commerce industry, rising focus on supply chain optimization, government infrastructure investment under the Build Better More program, and growing demand for cold chain facilities to support food safety and pharmaceutical distribution are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 441.7 Million |

|

Forecast Market Size (2034) |

USD 706.8 Million |

|

CAGR (2026-2034) |

5.20% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

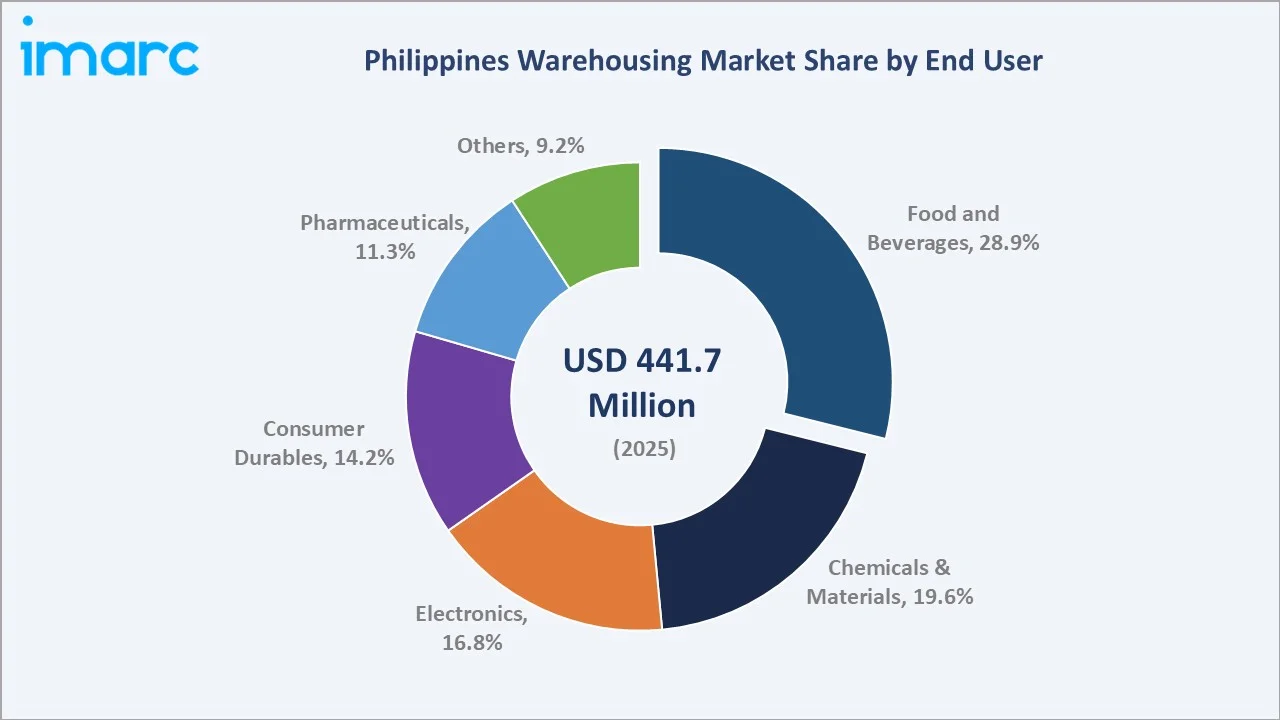

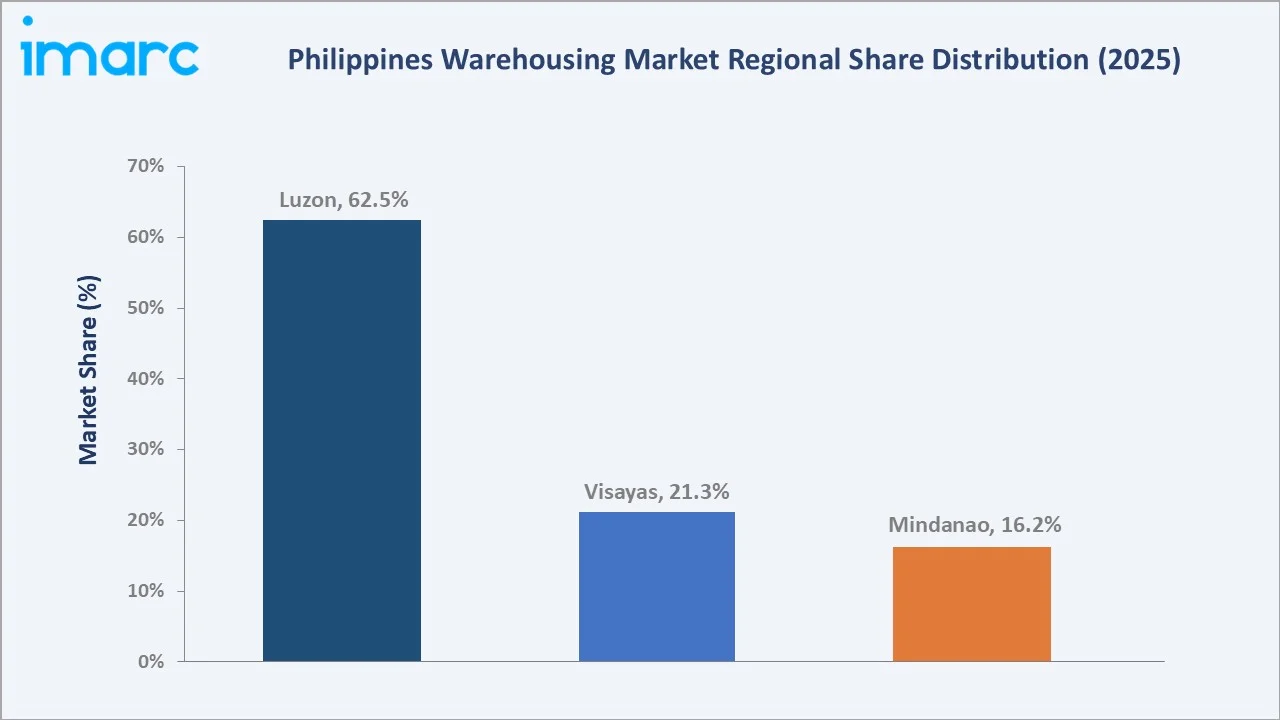

Luzon leads regionally with a 62.5% market share in 2025, anchored by Metro Manila’s commercial hub, the Cavite-Laguna-Batangas (CALABA) industrial corridor, and the concentration of large-scale distribution centers near Clark International Airport and major seaports. The food and beverages sector commands the largest end-user share at 28.9%, while general warehousing remains the dominant facility type at 36.8% in 2025.

To get more information on this market, Request Sample

The Philippines warehousing market is underpinned by three structural forces: the e-commerce sector’s projected to reach USD 86.2 Billion in 2034, creating massive fulfillment center demand; the government’s USD 26 Billion in 2024 for infrastructure allocation driving logistics park development, and the food and pharmaceutical sectors’ cold chain investment responding to international quality standards.

Executive Summary

The Philippines warehousing market is experiencing steady, broad-based expansion driven by the convergence of rapid e-commerce growth, government-led infrastructure development, and increasing supply chain complexity across food, pharmaceutical, and electronics sectors. The market was valued at USD 441.7 Million in 2025 and is forecast to reach USD 706.8 Million by 2034, growing at a CAGR of 5.20%.

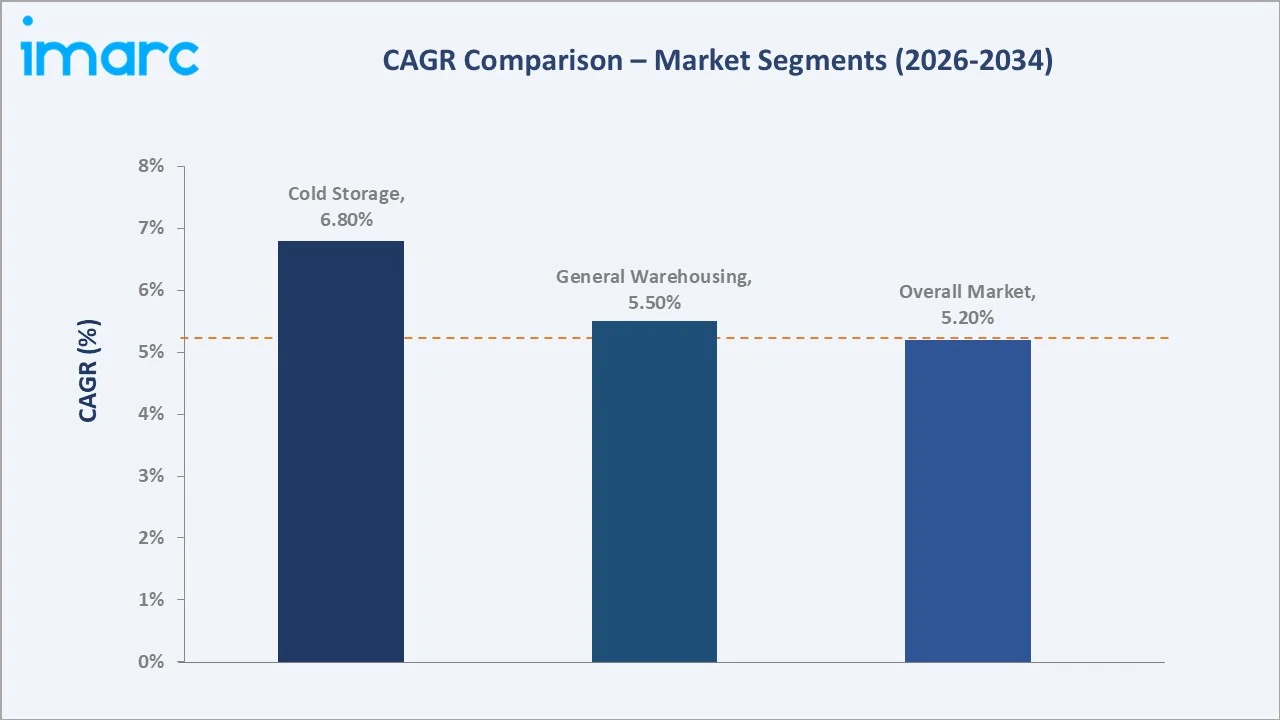

Food and beverages dominate end-user demand at 28.9% in 2025, driven by FMCG companies’ expansion of regional distribution networks and mandatory cold chain requirements for perishable goods. General warehousing maintains the largest facility type share at 36.8%, though cold storage is growing fastest at approximately 6.80% CAGR, supported by pharmaceutical cold chain regulations, retail food safety standards, and the expanding poultry, seafood, and dairy distribution networks.

Luzon accounts for 62.5% of national warehousing capacity in 2025, concentrated in the NCR, CALABA corridor, and Clark Freeport Zone. Key players, including United Parcel Service of America, Inc., DHL Group, Ayala Land, Inc., and Fast Logistics, collectively define the competitive dynamics across facility types and end-user sectors.

Key Market Insights

|

Insight |

Data |

|

Largest End-User Segment |

Food and Beverages – 28.9% share (2025) |

|

Fastest Growing Segment |

Cold Storage – ~6.80% CAGR (2026-2034) |

|

Largest Facility Type |

General Warehousing – 36.8% share (2025) |

|

Fastest Growing Facility Type |

Cold Storage – ~6.80% CAGR (2026-2034) |

|

Leading Region |

Luzon – 62.5% share (2025) |

|

Top Companies |

United Parcel Service of America, Inc., DHL Group, Ayala Land, Inc., and Fast Logistics |

Key Analytical Observations Supporting the Above Data:

- Food and beverages command 28.9% of end-user demand in 2025. Retail sales of packaged food in the Philippines amounted to approximately US$17.8 billion in 2024. It requires extensive ambient and temperature-controlled warehousing across the 7,641-island archipelago.

- General warehousing leads facility types at 36.8% in 2025, driven by the broadest demand base, spanning consumer goods, chemicals, electronics, and agricultural products, requiring standard dry storage across multiple temperature-ambient environments.

- Cold storage at 18.6% is the fastest-growing facility type, growing at approximately 6.80% CAGR, driven by pharmaceutical distribution requiring GDP-compliant temperature-controlled storage, seafood and poultry export processing facilities, and the post-pandemic acceleration of online grocery platforms requiring same-day cold chain fulfillment capabilities.

- Luzon’s 62.5% regional share reflects the CALABA corridor’s status as the Philippines’ primary industrial and logistics belt. The Cavite-Laguna-Batangas corridor’s industrial vacancy rate has declined significantly due to increased demand from FMCG companies, with UPS’ Clark International Airport logistics hub representing the corridor’s ongoing investment pull.

Philippines Warehousing Market Overview

The Philippines warehousing market encompasses all commercial facilities used for storing, handling, and distributing goods across the supply chain, including general dry-storage warehouses, container freight stations (CFS), cold storage and refrigerated facilities, agricultural storage depots, and specialized hazardous materials warehouses.

The market is structurally supported by the Philippine government’s USD 26 Billion 2024 infrastructure allocation, the Logistics Sector Roadmap under the Supply Chain Improvement Agenda (SCIA), and the Clark International Airport logistics hub development anchored by UPS’ March 2024 construction announcement. The archipelagic geography creates inherent logistics complexity, ensuring sustained warehousing infrastructure investment as supply chains expand from Metro Manila into secondary cities across all three island groups.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

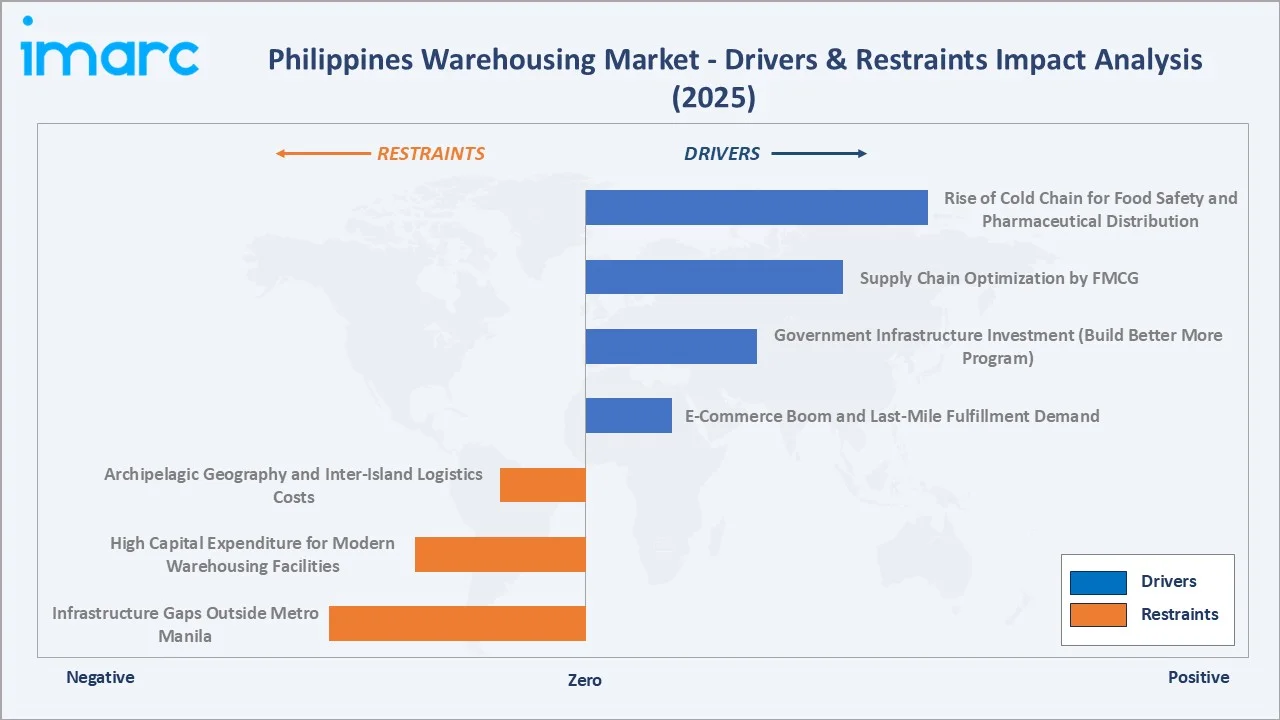

- E-Commerce Boom and Last-Mile Fulfillment Demand: The Philippines’ e-commerce market is projected to reach USD 86.2 Billion in 2034, driven by 73.91 million active online users and rapid platform growth by Shopee, Lazada, and TikTok Shop. Online sellers grew from 1,700 in March 2020 to 93,318 by January 2021 (DTI), creating massive and sustained demand for fulfillment centers near urban consumption hubs.

- Government Infrastructure Investment (Build Better More Program): Clark International Airport’s industrial estate, with 100% foreign ownership permitted under the Clark Freeport Zone, is emerging as a multi-modal logistics hub, with UPS’ March 2024 construction announcement reinforcing the area’s warehousing investment appeal.

- Supply Chain Optimization by FMCG: Major FMCG companies including Nestlé Philippines, Procter & Gamble, and Universal Robina Corporation are rationalizing distribution networks, consolidating from fragmented regional depots to hub-and-spoke warehouse systems, driving demand for larger, modern Grade-A facilities with advanced WMS integration.

- Rise of Cold Chain for Food Safety and Pharmaceutical Distribution: The Philippines’ seafood export sector (retail sales grew from USD 6.8 billion to USD 7.9 billion between 2020 & 2024) and rapidly expanding pharmaceuticals industry require compliant cold chain infrastructure from farm gate through distribution.

Market Restraints

- Archipelagic Geography and Inter-Island Logistics Costs: The Philippines’ 7,641-island geography creates structural inter-island logistics challenges, with roll-on/roll-off (RORO) ferry networks and air freight being the only viable inter-island goods transport modes for Visayas and Mindanao.

- High Capital Expenditure for Modern Warehousing Facilities: Grade-A warehousing construction in the Philippines costs approximately PHP 15,000 to PHP 30,000 per square meter. Electricity prices in the Philippines stand at around USD 0.18 per kWh, significantly higher than rates in Thailand (USD 0.13 per kWh), Indonesia (USD 0.10 per kWh), Vietnam (USD 0.08 per kWh), and Malaysia (USD 0.03 per kWh).

- Infrastructure Gaps Outside Metro Manila: Road quality, power grid reliability, and port efficiency in Visayas and Mindanao remain significantly below Luzon’s standards. The World Bank’s Logistics Performance Index 2023 ranked the Philippines 43rd overall, an improvement but still below regional leaders Singapore and Thailand.

Market Opportunities

- E-Commerce Fulfillment Center Expansion into Regional Cities: The e-commerce sector’s geographic expansion from Metro Manila into Cebu, Davao, Cagayan de Oro, and Iloilo is creating demand for purpose-built fulfillment centers in Visayas and Mindanao.

- Cold Chain Infrastructure Investment for Pharmaceutical and Food Export: The FDA’s GDP-aligned cold chain mandate for pharmaceutical distributors and the Department of Agriculture’s National Cold Chain System rollout are expected to create a USD 150–200 Million incremental cold chain investment opportunity through 2030.

Market Challenges

- Port Congestion and Customs Clearance Delays: Metro Manila’s Manila International Container Terminal (MICT) and Manila South Harbor regularly experience peak-period congestion, with average container dwell times of 4–6 days versus Singapore’s < 1-day standard. Port congestion directly impacts container freight station (CFS) utilization, increasing demurrage costs for importers and reducing effective warehousing throughput.

- Skilled Workforce Shortage for Warehouse Automation and Operations: The Philippines’ warehousing sector faces a growing shortage of warehouse management system (WMS) operators, cold chain technicians, and forklift-certified handlers. As facilities upgrade from manual to semi-automated operations, the mismatch between available technical skills and modern warehouse operational requirements constrains adoption of automation technologies.

Emerging Market Trends

1. Collaborations Between Logistics Developers and Real Estate Companies

Warehousing developers are collaborating with logistics companies to design and construct custom-built facilities that meet specific operational requirements. Real estate developers, including Ayala Land, Inc., Robinsons Land Corporation, and SM Prime Holdings, are partnering with institutional investors in joint ventures to finance large-scale warehouse park projects in the CALABA corridor.

2. Technology Integration and Warehouse Management System Adoption

Philippine warehousing operators are increasingly deploying Warehouse Management Systems (WMS), real-time inventory tracking platforms, and automated barcode/RFID systems to improve inventory accuracy and fulfillment velocity. Ninja Van Philippines’ September 2023 3,700 sq m Cabuyao warehouse launch, specifically designed for small business fulfillment with integrated last-mile delivery, exemplifies the sector’s technology-driven service evolution.

3. Cold Chain Expansion for Food Safety and Pharmaceutical Compliance

Brenntag’s December 2023 Mamplasan, Laguna facility, featuring temperature-controlled, dangerous goods, and ambient storage zones within a single 4,000 sq m footprint, represents the sector’s shift toward multi-temperature, multi-use cold chain infrastructure. The Department of Agriculture’s National Cold Chain System program targets a network of regional cold storage hubs in Luzon, Visayas, and Mindanao to reduce post-harvest losses estimated at 20–40% for high-value perishables.

4. Regional Warehousing Hub Development Beyond Metro Manila

Developers are establishing logistics parks in emerging corridors including the Batangas Industrial Estate, Bulacan Economic Zone, and Subic Bay Freeport, offering lower land costs, tax incentives under BOI/PEZA regimes, and multi-modal infrastructure connecting road, sea, and air freight. This geographic diversification is directly driving Visayas and Mindanao market growth projected at 12–14% CAGR, outpacing Luzon’s growth rate through 2034.

Industry Value Chain Analysis

The Philippines warehousing value chain spans raw material and inventory sourcing through end-consumer delivery, with each stage encompassing specialized operators whose performance directly determines supply chain efficiency, product integrity, and distribution cost across the country’s three island groups.

|

Stage |

Key Participants / Examples |

|

Raw Material & Inventory Sourcing |

Agricultural producers, FMCG manufacturers, pharmaceutical companies, chemical importers, and electronics assemblers |

|

Inbound Logistics |

International port terminal operators, customs brokers and freight forwarders, domestic trucking and intermodal transport providers, and international express freight operators |

|

Warehousing & Storage Facilities |

General dry-storage warehouse operators, container freight station (CFS) operators, temperature-controlled and cold storage facilities, and agricultural commodity depots |

|

Inventory & Order Management |

Warehouse management system (WMS) software providers, third-party logistics (3PL) operators, RFID and barcode technology integrators, and AI-driven inventory optimization |

|

Outbound Distribution |

Domestic express parcel carriers, last-mile delivery service providers, inter-island shipping and RORO freight operators, and on-demand logistics platforms |

|

End Users & Consumers |

Food and beverage retailers, pharmaceutical distributors and retail chains, electronics and appliance distributors, FMCG companies, e-commerce platforms |

Technology Landscape in the Philippines Warehousing Industry

Warehouse Management Systems (WMS) and Automation

Leading WMS platforms including SAP Extended Warehouse Management, Oracle WMS Cloud, and locally-integrated solutions are being deployed by Fast Logistics’ TMS/WMS suite. Semi-automated systems, including conveyor sortation for parcel handling and mobile racking systems for space optimization, are gaining adoption in high-throughput e-commerce fulfillment centers in Laguna and Cavite.

Cold Chain Technology and Temperature-Controlled Monitoring

IoT-enabled temperature monitoring systems with real-time alerting, pharmaceutical GDP-compliant data loggers, and automated cold room controllers are becoming standard in Philippine cold storage facilities. Launched in 2020, the Philippine Cold Chain Roadmap aims to expand the country’s cold storage capacity by 10% to 15% each year, adding around 50,000 pallet positions annually.

Digital Port and Smart Logistics Management Technology

International Container Terminal Services, Inc. (ICTSI) launched a suite of digital services and a new mobile application designed to improve visibility, efficiency, and customer experience across its port and logistics operations. The platform provides real-time tracking of containers, vessels, and terminal activities, helping port users streamline cargo movement and operational planning.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

End User |

Food and Beverages |

28.9% |

2025 |

|

Type |

General Warehousing |

36.8% |

2025 |

|

Region |

Luzon |

62.5% |

2025 |

By End User

Food and beverages dominate the end-user segment with a 28.9% share in 2025, the highest of any sector, reflecting the Philippines’ food retail density, with 120,000+ grocery, wet market, and convenience store outlets requiring regular ambient and refrigerated replenishment. The FMCG distribution model’s hub-and-spoke architecture requires large-format distribution centers near major consumption hubs alongside smaller cross-docking facilities serving regional markets.

To access detailed market analysis, Request Sample

Chemicals and materials at 19.6% is the second-largest end-user segment, led by international chemical distributors including Brenntag Philippines, which operate specialized hazardous materials warehouses with segregated storage for flammable, corrosive, and toxic chemicals, compliant with the Chemical Control Order (CCO) and International Fire Code requirements.

By Type

General warehousing leads with a 36.8% share in 2025, representing the broadest facility type serving ambient storage requirements across multiple end-user sectors. This segment encompasses bonded warehouses, public warehousing facilities, and private distribution centers, with the e-commerce sector’s rapid growth driving demand for large-format (15,000–60,000 sq m) fulfillment centers equipped with modern racking systems, conveyor integration, and parcel sortation technology.

Container freight stations at 22.4% represent the second-largest facility type, serving import/export consolidation at Manila, Cebu, and Davao ports. Cold storage at 18.6% is growing fastest at ~6.80% CAGR as pharmaceutical GDP requirements and online grocery fulfillment drive new investment.

Regional Market Insights

Luzon’s dominant 62.5% share (2025) is anchored by the CALABA corridor’s status as the Philippines’ primary manufacturing and logistics belt, hosting PEZA-registered industrial estates in Laguna, Cavite, and Batangas that house major FMCG, electronics, and chemical manufacturers requiring proximity to their warehouse supply chains.

Visayas at 21.3% is growing at approximately 12% CAGR, driven by Cebu City’s emergence as the Visayas’ commercial and e-commerce hub. The region’s growing BPO sector, expanding tourism-linked food supply chains, and the Mactan Export Processing Zone’s electronics manufacturing complex are creating sustained demand for modern warehousing facilities that remain underserved by current Grade-A supply.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Luzon |

62.5% |

Dominance of the Cavite-Laguna-Batangas industrial corridor as the country's primary manufacturing and logistics belt; development of multi-modal logistics hubs within special economic and freeport zones offering 100% foreign ownership |

|

Visayas |

21.3% |

Cebu City's emergence as the Visayas' primary commercial and e-commerce fulfillment hub; international airport cargo infrastructure supporting time-sensitive goods distribution |

|

Mindanao |

16.2% |

Agricultural commodity warehousing serving major crop-producing regions including high-value fruit, grain, and seafood export corridors; cold chain infrastructure investment for seafood and perishable agricultural produce |

Competitive Landscape

The Philippines warehousing market is moderately fragmented, with global logistics players (United Parcel Service of America, Inc., DHL Group) dominating the high-specification, integrated logistics segment, while domestic companies (Fast Logistics) command the regional distribution and last-mile warehousing segments.

|

Company Name |

Service Focus |

Market Position |

Core Strength |

|

United Parcel Service of America, Inc. |

Distribution Solutions, Warehousing & Distribution Value-Added Services, UPS Supply Chain Symphony, UPS eCommerce Fulfillment |

Market Leader |

Clark International Airport logistics hub construction; global network integration; integrated air-ground warehousing for e-commerce and healthcare |

|

DHL Group |

Contract Logistics |

Market Leader |

Cebu express cargo capacity; healthcare GDP-compliant cold chain warehousing for pharma distribution |

|

Ayala Land, Inc. |

Leasing & warehousing |

Strong Challenger |

CALABA logistics estate development; Grade-A warehouse park management; strategic PEZA-adjacent positioning in Laguna and Batangas |

|

Fast Logistics |

Warehousing & Distribution |

Challenger |

Prominent domestic 3PL operator; FMCG and consumer goods distribution across multiple provincial hubs; nationwide cold chain coverage |

Industrial real estate developers (Ayala Land, Inc.) are shaping warehouse park supply through large-scale logistics estate developments in the CALABA corridor and Visayas emerging markets.

Key Company Profiles

United Parcel Service of America, Inc.

United Parcel Service of America, Inc. operates UPS Philippines, a leading global integrated logistics operator providing express delivery and supply chain management services.

- Product Portfolio: Distribution Solutions, Warehousing & Distribution Value-Added Services, UPS Supply Chain Symphony, UPS eCommerce Fulfillment.

- Recent Developments: In March 2024, UPS announced the development of a new logistics hub at Clark International Airport in the Philippines to strengthen its express, supply chain, and healthcare logistics operations across Asia Pacific.

- Strategic Focus: Clark Freeport Zone logistics hub buildout; healthcare cold chain warehousing for pharmaceutical clients; e-commerce B2C fulfilment integration with Shopee and Lazada platforms.

Ayala Land, Inc.

Ayala Land, Inc. operates AyalaLand Logistics Holdings Corp., which further operates ALogis ready-built warehouse facilities for lease with spaces ranging from 500–1,500 sq m at sites in Biñan and Calamba (Laguna), Naic (Cavite), Santo Tomas (Batangas), and Porac (Pampanga), with strong presence in Luzon and future expansion into Visayas and Mindanao.

- Product Portfolio: ALogis (ready-built warehouse facilities for lease), Artico (cold storage facilities with temperatures ranging from 5°C to -25°C), Industrial Parks (Pampanga Technopark), and Retail/Office commercial estates (Tutuban Center, South Park Center).

- Recent Developments: In September 2024, VS Industry Philippines, Inc. (VSIP) signed a lease agreement with AyalaLand Logistics Holdings Corp. (ALLHC) for over 52,700 sq. meters. of space at ALogis Santo Tomas in Batangas, marking VSIP’s first operational facility in the Philippines.

- Strategic Focus: Nationwide cold storage network expansion under the Artico brand targeting food safety, pharmaceutical GDP compliance, and perishable export sectors; ALogis ready-built facility expansion into Visayas and Mindanao.

Market Concentration Analysis

The Philippines warehousing market exhibits moderate fragmentation across facility types and geographic segments. Global 3PL operators (United Parcel Service of America, Inc. and DHL Group) dominate the high-specification integrated logistics segment, collectively holding an estimated 25–30% of high-grade warehousing revenue in 2025.

Industrial real estate developers (Ayala Land, Inc.) are consolidating Grade-A warehouse supply development, shifting from multi-tenant spec builds toward build-to-suit arrangements for anchor tenants including Shopee, Lazada, and major FMCG companies. This developer consolidation is occurring alongside end-user concentration: the top 10 FMCG companies collectively account for an estimated 35–40% of general warehousing demand.

Investment & Growth Opportunities

Fastest Growing Segments

Cold storage (~6.80% CAGR), pharmaceutical warehousing (~6.50% CAGR), and e-commerce fulfillment centers (~7.20% CAGR implied through specialized general warehousing growth) represent the highest-growth investment vectors through 2034. Together, these sub-categories address an incremental addressable market of approximately USD 120–150 Million within the Philippines warehousing ecosystem by 2034—driven by cold chain compliance mandates, online grocery expansion, and pharmaceutical GDP requirements.

Emerging Market Expansion

Cebu (Visayas e-commerce and FMCG distribution hub), Davao (Mindanao agricultural and seafood cold chain), and Clark-Pampanga (100% foreign ownership under Freeport Zone) represent the highest-potential investment corridors outside CALABA. Entry strategies include build-to-suit anchored facilities for blue-chip FMCG or pharmaceutical tenants, co-investment with PEZA-registered industrial estate developers, and acquisition of existing but upgrading-ready ambient warehousing facilities in regional cities.

Venture and Institutional Investment Trends

- Philippine e-commerce, projected at USD 86.2 Billion in 2034, is driving venture capital into logistics technology (WMS, TMS, last-mile routing AI) with Fast Logistics’ USD 125 Million investment through CVC Capital Partners leading the sector.

- The government’s USD 27 Billion 2024 infrastructure allocation and the Build Better More program’s logistics corridor investments create long-duration institutional real estate investment opportunities in logistics parks adjacent to new airport, port, and highway infrastructure.

- Cold chain infrastructure investment, estimated at USD 150–200 Million incremental need through 2030, is attracting specialist cold chain REITs and logistics-focused private equity from Japan, South Korea, and Singapore, attracted by the Philippines’ growing pharmaceutical export ambitions and modern retail food safety standards.

Future Market Outlook (2026-2034)

The Philippines warehousing market is positioned for sustained growth through 2034. From a base of USD 441.7 Million in 2025, the market is projected to reach USD 706.8 Million by 2034, representing total incremental value creation of USD 265.1 Million at a CAGR of 5.20%. This growth is structurally underpinned by the e-commerce sector’s continued expansion, pharmaceutical GDP compliance investments creating cold chain demand, and the government’s infrastructure program driving logistics park development across three island groups.

Cold storage’s share of total warehousing is projected to rise from 18.6% in 2025 to approximately 23–25% by 2034 as pharmaceutical and food safety compliance requirements intensify. General Warehousing’s share may moderate from 36.8% to 33–34% as specialized facility types capture a larger proportion of new supply. Visayas and Mindanao are projected to grow at 2–3 percentage points above Luzon’s CAGR as geographic diversification of e-commerce fulfillment and agricultural cold chain investment accelerates through 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 80 industry participants in 2024–2025, including warehousing facility developers, 3PL operators, FMCG supply chain directors, pharmaceutical logistics managers, real estate advisors, and government logistics policy officials. Expert input validated market sizing, facility type adoption rates, and regional development patterns.

Secondary Research

Secondary research encompassed company annual reports, Philippine Economic Zone Authority (PEZA) industrial estate data, Philippine Ports Authority cargo statistics, IMARC Group Philippines logistics market data, ITA e-commerce projections, Colliers Philippines industrial market reports, and news coverage of major warehouse development announcements.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating industrial real estate supply pipelines, end-user sector growth trajectories, facility type utilization rates, and announced warehousing investment commitments. A base-case CAGR of 5.20% reflects consensus estimates validated against warehousing rental rate trends, industrial vacancy data, and supply chain investment patterns from 2020 to 2025.

Philippines Warehousing Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | General Warehousing, Container Freight, Cold Storage, Agriculture, Others |

| End Users Covered | Food and Beverages, Chemicals and Materials, Electronics, Pharmaceutical, Consumer Durables, Others |

| Regions Covered | Luzon, Visayas, Mindanao |

| Comapnies Covered | United Parcel Service of America, Inc., DHL Group, Ayala Land, Inc., Fast Logistics, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Philippines warehousing market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Philippines warehousing market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Philippines warehousing industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Philippines Warehousing Market Report

The Philippines warehousing market reached USD 441.7 Million in 2025 and is projected to reach USD 706.8 Million by 2034.

The market is expected to grow at a CAGR of 5.20% during 2026-2034, driven by e-commerce expansion, government infrastructure investment, cold chain compliance requirements, and supply chain optimization by FMCG, pharmaceutical, and electronics sectors.

Luzon leads with a 62.5% share in 2025, anchored by the CALABA industrial corridor (Cavite, Laguna, Batangas), Metro Manila’s distribution centers, and the Clark Freeport Zone’s emerging logistics hub anchored by UPS’ airport logistics facility under construction.

Food and Beverages leads with a 28.9% share in 2025, reflecting the Philippines’ food retail density, FMCG distribution network expansion, and mandatory cold chain requirements for perishable goods from the Department of Agriculture and FDA.

Cold Storage is the fastest-growing segment at approximately 6.80% CAGR, driven by pharmaceutical GDP compliance requirements, online grocery platform expansion, and the seafood/poultry export sector’s cold chain infrastructure needs across Luzon, Visayas, and Mindanao.

Key players include United Parcel Service of America, Inc., DHL Group, Ayala Land, Inc., and Fast Logistics.

E-commerce platforms require large-format fulfillment centers near urban consumption centers and last-mile delivery hubs in peri-urban corridors, directly driving warehouse construction in Bulacan, Laguna, Cavite, and Cebu.

Key challenges include the archipelagic geography’s inter-island logistics cost premium, high construction costs for Grade-A facilities, port congestion at Manila with 4–6 day average container dwell times, high electricity tariffs for refrigerated facilities, and a skilled workforce shortage for WMS operation and cold chain technology maintenance.

Key investment opportunities include cold storage development targeting the pharmaceutical GDP compliance market, e-commerce fulfillment centers in Cebu and Davao serving underserved regional markets, and WMS and logistics technology platforms serving the rapidly modernizing domestic 3PL sector.

Philippine warehousing is transitioning from manual, labor-intensive operations to technology-integrated facilities deploying WMS, RFID-based inventory tracking, IoT-enabled cold chain monitoring, and parcel sortation automation.

The competitive landscape is evolving toward greater specialization and real estate institutionalization. Industrial developers are transitioning from speculative multi-tenant builds to build-to-suit anchored developments with long-term FMCG and e-commerce tenants.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)