Physical Security Market Report by Component (System, Services), Enterprise Size (Large Enterprises, Small and Medium-sized Enterprises), Industry Vertical (Retail, Transportation, Residential, IT and Telecom, BFSI, Government, and Others), and Region 2026-2034

Global Physical Security Market:

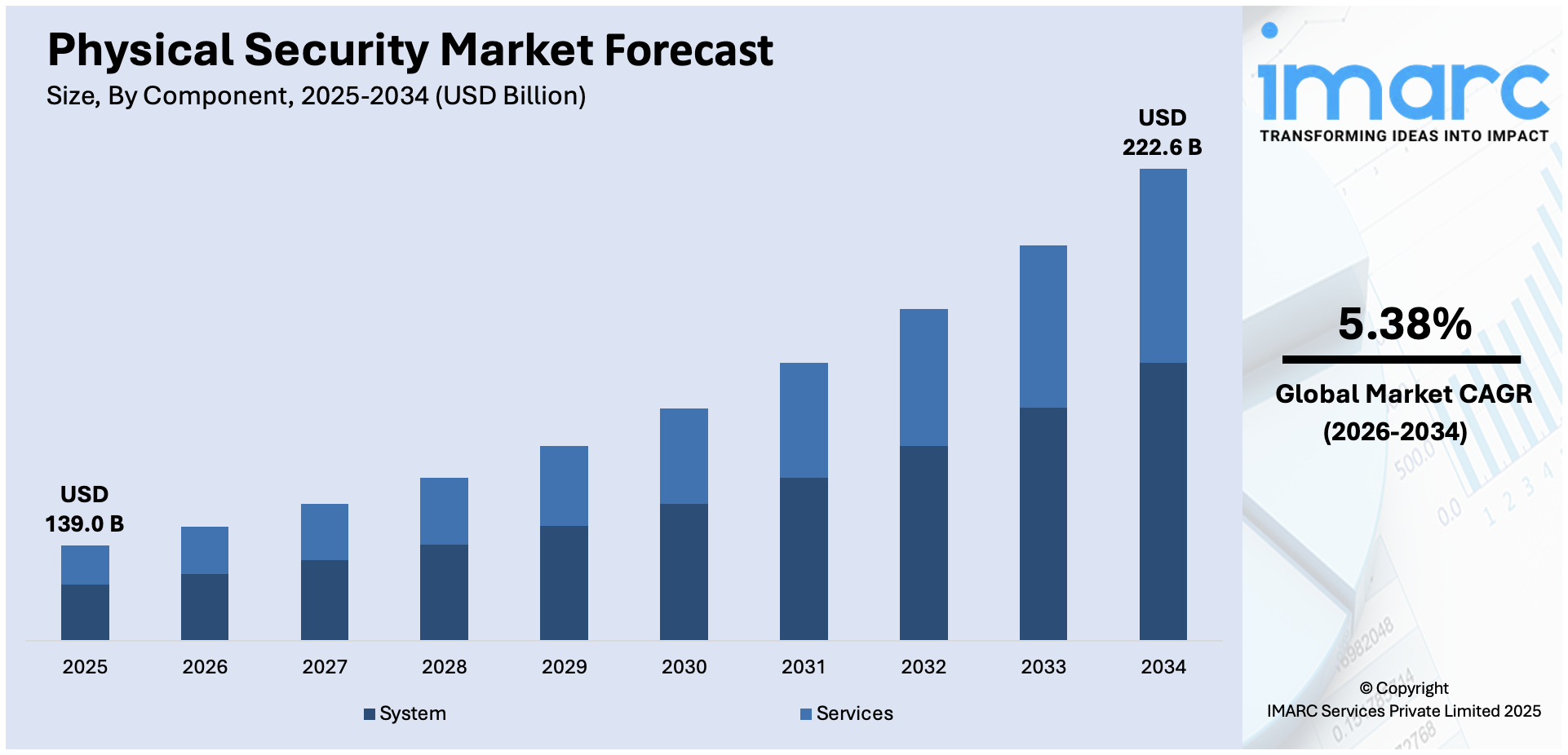

The global physical security market size reached USD 139.0 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 222.6 Billion by 2034, exhibiting a growth rate (CAGR) of 5.38% during 2026-2034. North America currently dominates the market in 2025. The rising security concerns among individuals, coupled with the emergence of video surveillance solutions for efficient monitoring of large areas, are primarily augmenting the market across the globe.

Market Size & Forecasts:

- Physical security market was valued at USD 139.0 Billion in 2025.

- The market is projected to reach USD 222.6 Billion by 2034, at a CAGR of 5.38% from 2026-2034.

Dominant Segments:

- Component: System leads the physical security market because it includes essential solutions like surveillance, access control, and alarms, which are widely adopted to prevent threats. Organizations prefer integrated systems for better monitoring, control, and faster response to security breaches.

- Enterprise Size: Large enterprises dominate the market as they have higher security needs, larger infrastructure, and greater budgets. They are investing in advanced systems to protect assets, employees, and sensitive data, ensuring operational safety across multiple locations.

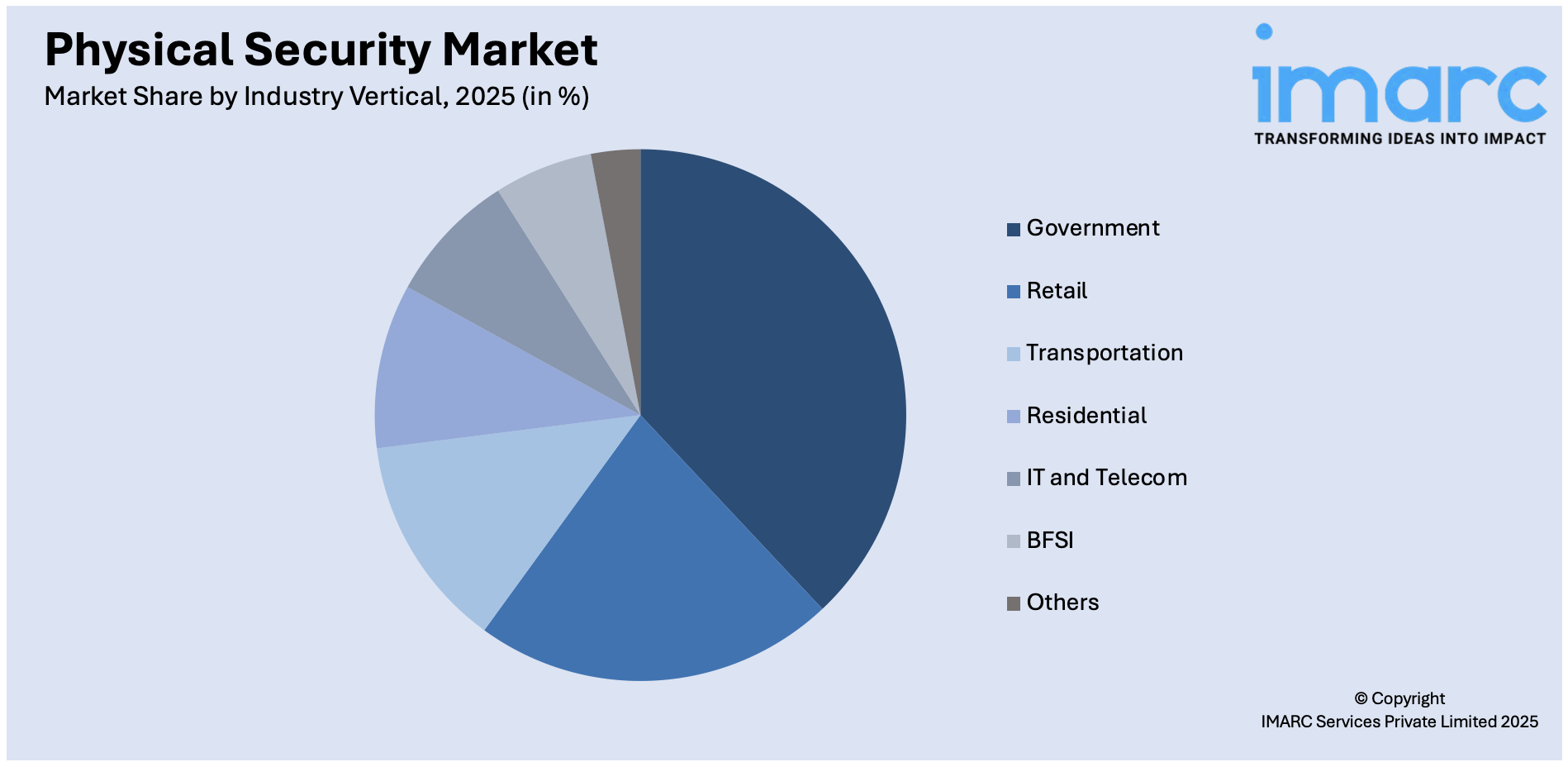

- Industry Vertical: Government accounts for the largest market share due to its need to secure public spaces, critical infrastructure, and sensitive data. High investments in surveillance, access control, and emergency response systems are driving strong demand across defense, transportation, and administrative facilities.

- Region: North America leads the physical security market, driven by strong technological adoption, strict security regulations, and high spending on safety solutions. The presence of key players and demand from sectors like government, commercial, and critical infrastructure is further stimulating regional growth.

Key Players:

- The leading companies in physical security market include ADT Inc., Axis Communications AB, Cisco Systems, Inc., Genetec Inc., Hangzhou Hikvision Digital Technology Co., Ltd., HID Global Corporation (Assa Abloy AB), Honeywell International Inc., Johnson Controls, KEENFINITY Group, Pelco, Senstar Corporation, Siemens AG, etc.

Key Drivers of Market Growth:

- Growing Demand for Integrated Security Solutions: Businesses prefer unified platforms combining surveillance, access control, and alarms. These systems improve efficiency, reduce costs, and offer better protection through centralized monitoring and faster, coordinated threat responses.

- Increased Investment in Critical Infrastructure Protection: Government agencies and organizations are prioritizing securing energy grids, transport hubs, and data centers. This is catalyzing the demand for advanced surveillance, access control, and intrusion systems to prevent physical threats and ensure public safety.

- Expansion in Commercial and Industrial Sectors: New offices, factories, and retail spaces require strong protection. Businesses are investing in surveillance, access control, and alarm systems to safeguard assets and meet regulatory compliance.

- Rising Adoption of Artificial Intelligence (AI): AI aids in enabling smart surveillance, real-time threat detection, and automated responses. AI-oriented systems analyze data efficiently, reduce human error, and improve decision-making, making security solutions more accurate, proactive, and cost-effective.

- Availability of Advanced Analytics for Threat Detection: Advanced analytics assist in enhancing real-time monitoring and incident prediction. These tools help identify suspicious behavior and minimize false alarms, making security systems more reliable, efficient, and effective.

Future Outlook:

- Strong Growth Outlook: The physical security market is expected to see sustained expansion, driven by rising security concerns, smart technology adoption, and high investments across industries. Increased demand for integrated systems and real-time monitoring continues to drive innovations and market expansion globally.

- Market Evolution: The sector is anticipated to shift from traditional lock-and-key systems to advanced surveillance, access control, and integrated solutions. Technological advancements, rising security threats, and digital transformation across industries are driving this transition, making physical security smarter, more efficient, and widely adopted.

The market is growing due to the rising adoption of integrated security systems, where businesses prefer unified platforms combining surveillance, access control, and alarm systems for better efficiency and centralized control. Increased investments in critical infrastructure protection are also driving the demand, as government agencies and private organizations are focusing on securing energy plants, transportation hubs, and data centers. The expansion of commercial and industrial sectors is positively influencing the market, with more factories, offices, and complexes requiring advanced security solutions to protect property and personnel. In addition, the rising use of AI enhances security by enabling real-time threat detection, facial recognition, and automated alerts. Cloud-based security management systems are gaining popularity for their remote access and scalability. Strict government regulations and industry standards are also encouraging organizations to upgrade their security systems. The growing awareness about workplace safety and emergency preparedness is leading to higher utilization of physical security technologies.

To get more information on this market Request Sample

Global Physical Security Market Trends:

Rising concerns over theft

Increasing concerns over theft are fueling the market growth. According to the Office for National Statistics, the Crime Survey for England and Wales (CSEW) projected 9.6 Million occurrences of headline crime, which encompassed theft, computer misuse, robbery, criminal damage, fraud, and violence with or without injury, in 2024. With increasing incidents of burglary, shoplifting, equipment loss, and unauthorized access, there is a higher demand for reliable security systems. Organizations are investing in video surveillance, intrusion alarms, access control, and motion detection to deter theft and monitor activities in real time. As crime rates and security threats are rising in urban areas, the need for proactive protection is becoming more urgent. This is encouraging both the public and private sectors to implement advanced technologies that offer quick alerts and detailed records.

Increasing Adoption of Internet of Things (IoT)

Rising adoption of IoT is positively influencing the market. As per industry reports, the IoT market size value reached 64.8 Billion in 2024. IoT allows various security devices like cameras, sensors, alarms, and access controls to communicate in real-time, creating a unified network. This improves monitoring, threat detection, and response speed. With IoT, users can remotely manage and control security systems through smartphones or computers, increasing convenience and situational awareness. Smart analytics and automation reduce human errors and enhance decision-making. In industrial settings, IoT-oriented security systems offer better data collection and integration, leading to proactive threat management. As businesses and government agencies are seeking more advanced solutions, IoT helps modernize traditional setups and improve overall security performance.

Broadening of retail outlets

The expansion of the retail sector is stimulating the market growth. As per the IBEF, in 2024, the Indian retail industry witnessed the launch of more than 750 new outlets and an overall revenue of INR 12,000 Crore (USD 1.38 Billion) secured. Retail businesses need strong security systems to protect merchandise, prevent theft, monitor customer activity, and ensure employee safety. As retail spaces are expanding in size and number, the risk of shoplifting, vandalism, and internal theft is increasing, creating the need for advanced surveillance, access control, and alarm systems. Physical security solutions help retailers decrease losses, maintain order, and provide a safe shopping experience. Integration with analytics and real-time monitoring allows store managers to respond quickly to incidents. With 24/7 operations, especially in large stores and chains, round-the-clock security is becoming essential. This increasing focus on asset protection and loss prevention in the thriving retail industry is significantly contributing to the growth of the market.

Key Growth Drivers of Physical Security Market:

Growing demand for integrated security solutions

Rising need for integrated security systems is propelling the market growth. Instead of using separate systems, businesses prefer unified platforms that combine video surveillance, access control, intrusion detection, and alarm systems. These integrated solutions offer a more complete and streamlined approach to security management. They help improve real-time monitoring, speed up response times, and reduce operational costs by centralizing control. Users benefit from better data sharing and coordination between different security layers, which enhances overall safety. Integrated systems also support automation and remote access, making them suitable for modern workplaces and large infrastructures. As threats are becoming more complex, end-users value the convenience, scalability, and effectiveness that these unified platforms provide.

Increased investment in critical infrastructure protection

Safeguarding energy grids, transportation hubs, government buildings, and data centers from physical threats remains a key priority for national security. To address these risks, there is a rising demand for advanced and reliable security technologies such as surveillance systems, access control, perimeter protection, and emergency response solutions. These critical sites require constant monitoring and quick incident detection, promoting the adoption of high-end, integrated systems. As infrastructure is becoming more complex and interconnected, the need for comprehensive physical security is growing. This leads to continuous funding and upgrades in security infrastructure. The demand for strong, scalable, and intelligent solutions is making critical infrastructure protection a major contributor to the market expansion.

Expansion in commercial and industrial sectors

As more buildings, retail outlets, manufacturing units, and industrial facilities are being developed, especially in emerging economies, the need to safeguard assets, employees, and intellectual property from theft, vandalism, and unauthorized access is rising. As businesses are scaling operations, they are investing in security solutions, such as alarm systems and perimeter protection. These tools help ensure safe operations and regulatory compliance while minimizing risks. With rising urbanization and infrastructure development, companies are placing greater importance on physical safety. Security systems also support better workplace management and emergency preparedness. Consequently, the continuous expansion of commercial and industrial zones is directly contributing to the high demand for advanced and reliable physical security technologies.

Physical Security Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on component, enterprise size and industry vertical.

Breakup by Component:

- System

- Services

System currently accounts for the majority of the global market share

The report has provided a detailed breakup and analysis of the market based on the component. This includes system and services. According to the report, system accounted for the largest market share.

Some of the common sub-segments of systems are video surveillance systems, perimeter intrusion detection and prevention, physical access control systems (PACS), physical security information management (PSIM), physical identity and access management (PIAM), fire and life safety plus. Besides this, the introduction of institutional and commercial infrastructures across numerous countries is escalating the demand for video surveillance, which, in turn, is fueling the growth of this segment. For example, in March 2022, Hexagon AB and Ouster Inc., which develops and manufacturers security systems, introduced a joint security solution, Ouster×Accur8vision, a video surveillance software for monitoring and protecting critical infrastructures, such as commercial buildings, crowded settings, residential properties, airports, etc. This enhanced existing security systems by adding a layer of awareness to detect future threats.

Breakup by Enterprise Size:

- Large Enterprises

- Small and Medium-sized Enterprises

Large enterprises exhibit clear dominance in the market

The report has provided a detailed breakup and analysis of the market based on the enterprise size. This includes large enterprises and small and medium-sized enterprises. According to the report, large enterprises accounted for the largest market share.

Large enterprises are focusing on protecting their data from cyberattacks, thefts, and unauthorized access, which is propelling the demand for physical security solutions. Moreover, the growing prevalence of cyber threats that target businesses that store essential personal and sensitive information is also augmenting the market growth in this segment. According to the physical security industry statistics, in October 2021, Alert Enterprise Inc., a software development company and cyber-physical security provider, partnered with Bio Connect Inc., which is a prominent provider of biometric devices and technologies.

Breakup by Industry Vertical:

Access the comprehensive market breakdown Request Sample

- Retail

- Transportation

- Residential

- IT and Telecom

- BFSI

- Government

- Others

Government sector holds the largest market share

The report has provided a detailed breakup and analysis of the market based on the industry vertical. This includes retail, transportation, residential, IT and telecom, BFSI, government, and others. According to the report, government represented the largest segment.

Government bodies across the globe are emphasizing on upgrading their security defenses while working with legacy equipment and staying within budget, owing to the changing and complex environment, which is propelling the market growth in the segment. For example, in July 2022, The European Commission, the European Union (EU), and the European Parliament agreed on a European guideline on critical entity resilience. This was done to protect essential providers of the process by enhancing their stability. Furthermore, according to IFSEC Global, a media production company based in London, the government in London provides consultation on how to regulate the use of construction products to ensure that fire protection is prioritized. New standards have been implemented to provide impartial advice on new guidance for construction products.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest physical security market share.

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

North America is a significant region in the physical security market. In line with this, numerous public transportation systems and facilities, such as railways, airports, seaports, bus stations, etc., are focusing on protecting their infrastructure through security layers, which will continue to drive the North America physical security market. For example, in January 2022, Allied Universal, a U.S.-based security provider company, acquired Norred & Associates Inc., (Allied Universal) a security firm. The acquisition enabled Allied Universal to provide a full range of security services to railways, bus stations, and airports in the region, including security consulting, manned guarding, investigation, pre-employment screening, etc.

Leading Key Players in the Physical Security Industry:

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- ADT Inc.

- Axis Communications AB

- Cisco Systems, Inc.

- Genetec Inc.

- Hangzhou Hikvision Digital Technology Co., Ltd.

- HID Global Corporation (Assa Abloy AB)

- Honeywell International Inc.

- Johnson Controls

- KEENFINITY Group

- Pelco

- Senstar Corporation

- Siemens AG

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Global Physical Security Market News:

- July 2025: Genetec Inc., the worldwide pioneer in enterprise physical security software, revealed new enhancements to Security Center SaaS, the firm’s enterprise-level Security-as-a-Service (SaaS) offering. It integrated video monitoring, access management, forensic analysis, intrusion detection, automation, and various other sophisticated features in one solution. Security Center SaaS differentiated itself by consolidating physical security features on one platform, consistently introducing new cloud-native functions while accommodating the hardware and deployment methods that organizations depended on.

- May 2025: David Mussington, CISA’s assistant director for infrastructure security, revealed that the agency formulated physical security performance objectives. Once the interagency could provide input, the firm would coordinate with stakeholders across various industry sectors to ensure that the company’s goals and practices were tailored and refined according to the unique needs of each industry.

- March 2025: HID unveiled the HID Integration Service, a platform that combined physical security, cybersecurity, and digital identity management. This integration platform-as-a-service (IPaaS) was created to enable solution integrators, application developers, and software vendors to effortlessly and quickly incorporate vital physical security systems, simplifying workflows and improving system compatibility.

- March 2025: Hexagon’s Safety, Infrastructure & Geospatial division revealed the expansion and rebranding of its physical security solutions portfolio to HxGN dC3. The updated name, representing ‘Detect, Command, Control, and Collaborate,’ showcased the company’s strategy for safeguarding individuals, property, and assets by facilitating the complete lifecycle of an incident to reduce its effects.

- February 2025: Corporate Security Advisors (CSA), a consultancy focused on corporate security, revealed its selection as the inaugural ‘Preferred Physical Security Advisory Services Provider’ in the respected American Hospital Association (AHA) Preferred Cybersecurity and Risk Provider Program. CSA would be essential in assisting hospitals and healthcare systems across the country to improve their physical security measures to safeguard patients, employees, and facilities.

- January 2025: Spot AI released the first remote video AI agent for physical security in the industry. Remote Security Agent integrated contextual understanding with automated responses to address the increasing issues of organized retail crime and property theft.

Physical Security Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Segment Coverage | Component, Enterprise Size, Industry Vertical, Region |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ADT Inc., Axis Communications AB, Cisco Systems, Inc., Genetec Inc., Hangzhou Hikvision Digital Technology Co., Ltd., HID Global Corporation (Assa Abloy AB), Honeywell International Inc., Johnson Controls, KEENFINITY Group, Pelco, Senstar Corporation, Siemens AG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the physical security market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global physical security market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the physical security industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Physical Security Market Report

The global physical security market was valued at USD 139.0 Billion in 2025.

We expect the global physical security market to exhibit a CAGR of 5.38% during 2026-2034.

The growing adoption of physical security across several industries, such as transportation, retail, Information Technology (IT), telecommunications, etc., as it protects software, hardware, networks, and property from events that could cause profound loss or damage, is primarily driving the global physical security market.

The sudden outbreak of the COVID-19 pandemic has led to the increasing utilization of physical security for preventing unauthorized access to facilities and maintaining trust and confidence, during the remote working scenario.

Based on the component, the global physical security market can be divided into system and services, where system currently accounts for the majority of the global market share.

Based on the enterprise size, the global physical security market has been segregated into large enterprises and small and medium-sized enterprises. Currently, large enterprises exhibit clear dominance in the market.

Based on the industry vertical, the global physical security market can be bifurcated into retail, transportation, residential, IT and telecom, BFSI, government, and others. Among these, the government sector holds the largest market share.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global physical security market include ADT Inc., Axis Communications AB, Cisco Systems, Inc., Genetec Inc., Hangzhou Hikvision Digital Technology Co., Ltd., HID Global Corporation (Assa Abloy AB), Honeywell International Inc., Johnson Controls, KEENFINITY Group, Pelco, Senstar Corporation, and Siemens AG.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)