Plasma Fractionation Market Report by Product (Immunoglobulins, Albumin, Coagulation factor VIII, Coagulation factor IX), Sector (Private Sector, Public Sector), Application (Neurology, Immunology, Hematology, and Others), End User (Hospitals and Clinics, Clinical Research Laboratories, Academic Institutes), and Region 2026-2034

Global Plasma Fractionation Market:

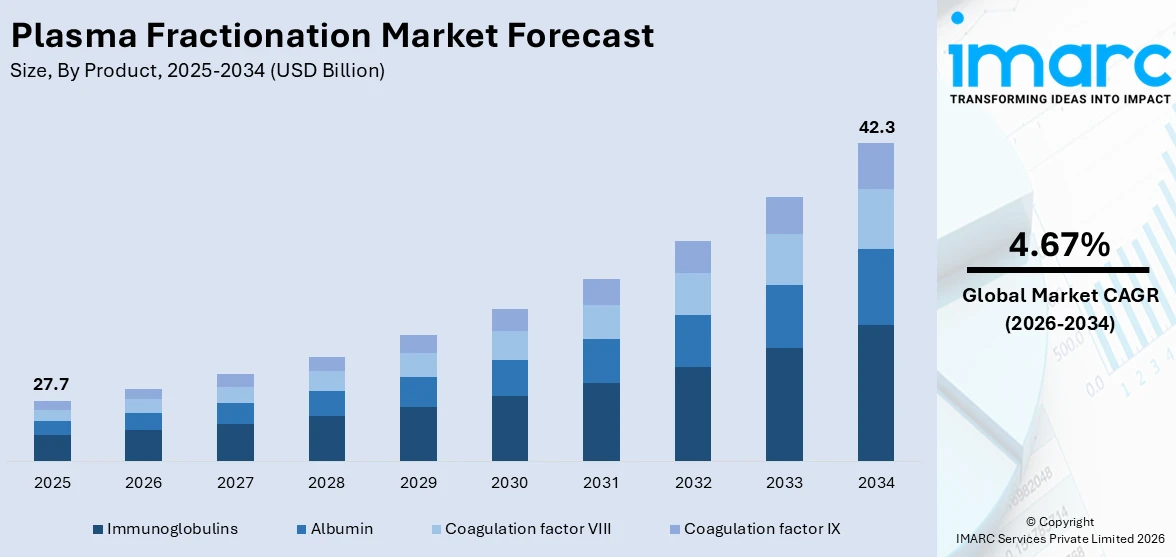

The global plasma fractionation market size reached USD 27.7 Billion in 2025. Looking forward, the market is expected to reach USD 42.3 Billion by 2034, exhibiting a growth rate (CAGR) of 4.67% during 2026-2034. The rising prevalence of chronic diseases, technological advancements, and the increasing investment in healthcare are some of the major factors driving the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 27.7 Billion |

|

Market Forecast in 2034

|

USD 42.3 Billion |

| Market Growth Rate 2026-2034 | 4.67% |

Plasma Fractionation Market Analysis:

- Major Market Drivers: The rising need for preventing, managing, and treating infections, congenital deficiencies, rare blood disorders, immunologic disorders, and autoimmune diseases is driving the market growth.

- Key Market Trends: Key players across countries are investing in R&D activities to enhance plasma production technology for product efficacy and recovery of immunoglobulin G (IgG) to isolate new plasma proteins, which is one of the emerging trends bolstering the market.

- Competitive Landscape: Some of the prominent companies in the market include ADMA Biologics Inc., Boccard, CSL, Grifols, S.A., Intas Pharmaceuticals Ltd., Kedrion, LFB, Octapharma AG, PlasmaGen BioSciences Pvt. Ltd., and Sartorius AG, among many others.

- Geographical Trends: North America currently dominates the global market due to the region's advanced healthcare infrastructures, high demand for plasma-derived products, and the development of affordable viral inactivation and processing technologies.

- Challenges and Opportunities: One of the primary challenges hindering the market is the growing concerns over ensuring a stable and sufficient supply of plasma. However, the increasing donor recruitment efforts are expected to fuel the market in the coming years.

To get more information on this market Request Sample

Plasma Fractionation Market Trends:

Rising Geriatric Population

As people age, they are more prone to various health conditions, such as immune deficiencies, neurological disorders, and chronic diseases, thereby propelling the need for plasma products. For instance, according to an article published by the World Health Organization (WHO), by 2030, one in every six persons in the world will be 60 or older. Moreover, the global population of individuals aged 60 and above will be approximately 2.1 billion by 2050. Besides this, as per the National Library of Medicine, about 21% of the elderly in India suffer from at least one chronic condition. Hypertension and diabetes are responsible for approximately 68% of all chronic illnesses. Plasma products derived from fractionation are essential for treating many of these conditions effectively. These therapies play a crucial role in managing symptoms and improving the quality of life in these cases. These factors are contributing to the plasma fractionation market share.

Prevalence of Rare Chronic Diseases

The rising prevalence of rare chronic diseases is significantly driving the growth of the market. For instance, according to an article published by the Food & Drug Administration (FDA) in December 2022, more than 30 million people suffer from more than 7,000 rare diseases in the U.S. Moreover, many rare chronic diseases require specialized treatments, including therapies derived from plasma fractionation. These treatments are essential for managing symptoms, improving quality of life and providing life-saving interventions. For instance, according to an article published by Invest India, there are many therapeutic applications for plasma fractionation, such as the treatment of congenital or immunological deficiency diseases, trauma blood volume restoration, and the very efficient inactivation of viral contaminants like HIV and hepatitis viruses. Besides this, regulatory approvals for new plasma-derived products and expanding indications also stimulate market growth, allowing more patients access to these treatments. For example, in June 2024, Takeda announced that the Ministry of Health, Labour, and Welfare in Japan approved the use of CUVITRU as replacement therapy for patients aged two years and older with agammaglobulinemia or hypogammaglobulinemia disorders characterized by extremely low or absent antibody levels and an increased risk of serious recurring infection caused by primary immunodeficiency (PID) or secondary immunodeficiency (SID).

Advancements in Purification Techniques

Advancements in purification techniques have significantly enhanced the quality, safety, and efficiency of plasma-derived products. One of the most critical advancements is in the methods of viral inactivation and removal. Techniques, such as solvent/detergent treatment, pasteurization, and nanofiltration, have been refined to effectively eliminate viruses while preserving therapeutic proteins in plasma products. This ensures higher safety standards and reduces the risk of viral transmission. For instance, according to an article published by the National Library of Medicine, therapeutic plasma proteins, including human albumin, coagulation factors, immunoglobulins, and enzyme inhibitors, are pasteurized at 60°C for 10 hours to kill blood-borne viruses of concern. Moreover, modern chromatographic techniques, including affinity chromatography and ion exchange chromatography, have improved the purification process by allowing for more precise separation of plasma proteins based on their specific characteristics. This results in higher purity and yield of therapeutic proteins like immunoglobulins, albumin, and clotting factors. For instance, in November 2023, Cytiva, one of the life science companies headquartered in the United States, launched the Cytiva Protein Select technology, which streamlines and accelerates recombinant protein purification. The self-cleaving traceless tag and complementary affinity chromatography resin standardize purification for any protein, thereby eliminating the need for protein-specific affinity binding partners.

Global Plasma Fractionation Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market report, along with forecasts at the global, regional, and country levels from 2026-2034. Our report has categorized the market based on product, sector, application, and end user.

Breakup by Product:

- Immunoglobulins

- Albumin

- Coagulation factor VIII

- Coagulation factor IX

Immunoglobulins currently exhibit a clear dominance in the market

The report has provided a detailed breakup and analysis of the market based on the product. This includes immunoglobulins, albumin, coagulation factor VIII, and coagulation factor IX. According to the report, immunoglobulins represented the largest market segmentation.

Immunoglobulins, also known as antibodies, play a dominant role in plasma fractionation due to their widespread therapeutic applications and high demand. Immunoglobulins are used to treat various medical conditions, including primary and secondary immunodeficiencies, autoimmune diseases, inflammatory disorders, and neurological diseases. They are essential for boosting immune function and managing symptoms in patients with these conditions. For instance, in September 2022, Grifols, one of the plasma medicines providers, signed a long-term agreement with Canada's national blood authority to increase the country's self-sufficiency in immunoglobulin significantly (Ig) medicines that are used to treat a variety of immunodeficiencies and other medical conditions.

Breakup by Sector:

- Private Sector

- Public Sector

Private sector accounts for the majority of the total market share

The report has provided a detailed breakup and analysis of the market based on the sector. This includes the private sector and the public sector. According to the report, the private sector represented the largest market segmentation.

In the private sector, plasma fractionation plays a crucial role in producing essential plasma-derived therapies, which are vital for treating various medical conditions, such as immunodeficiencies, hemophilia, and autoimmune disorders. Private companies are pivotal in advancing the fractionation process through investment in cutting-edge technologies and infrastructure, ensuring high-quality and efficient production. They also drive innovation by developing new therapeutic products and improving existing ones, thereby expanding treatment options for patients. Additionally, the private sector contributes significantly to the global plasma supply chain, enhancing the availability of these life-saving therapies. Through strategic partnerships and robust distribution networks, private companies facilitate the timely delivery of plasma-derived products to healthcare providers and patients worldwide, underscoring their indispensable role in the healthcare ecosystem.

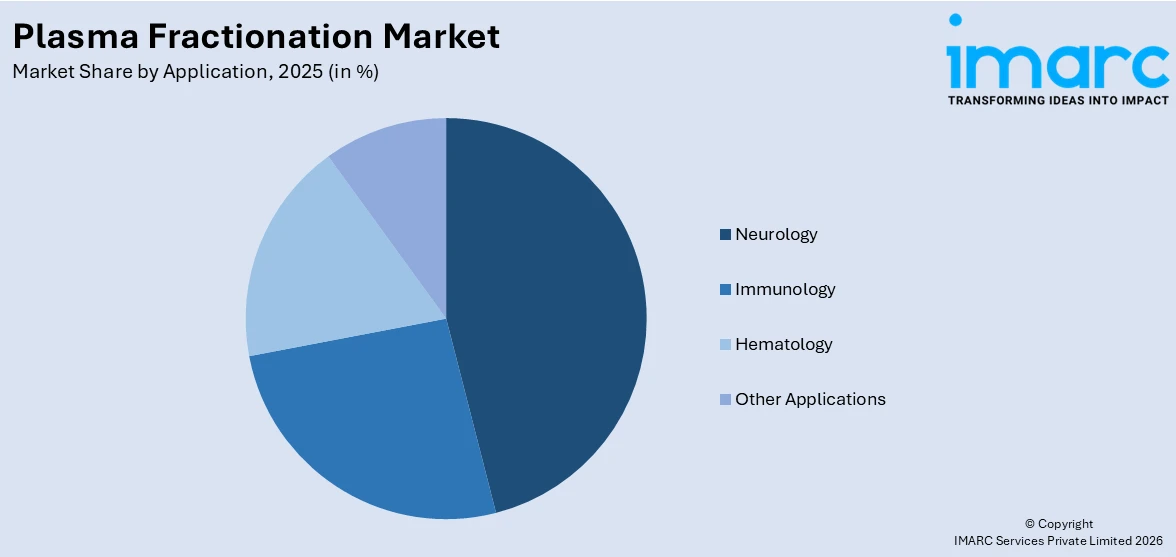

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Neurology

- Immunology

- Hematology

- Other Applications

Neurology currently holds the largest market share

The report has provided a detailed breakup and analysis of the market based on the application. This includes neurology, immunology, hematology, and other applications. According to the report, neurology represented the largest market segmentation.

Neurology represented the largest segment in the market due to the high demand for plasma-derived therapies in treating neurological disorders. Conditions, including chronic inflammatory demyelinating polyneuropathy (CIDP), Guillain-Barré syndrome, and multifocal motor neuropathy, require immunoglobulins derived from plasma for effective management. For example, intravenous immunoglobulin (IVIG) therapy, which is critical in treating CIDP, helps reduce inflammation and improve muscle strength and function in patients. The prevalence of such neurological conditions and the effectiveness of plasma-derived therapies in their treatment drive significant demand in this segment, highlighting the critical role of plasma fractionation in neurology.

Breakup by End User:

- Hospitals and Clinics

- Clinical Research Laboratories

- Academic Institutes

Hospitals and clinics exhibit a clear dominance in the market

The report has provided a detailed breakup and analysis of the market based on the end user. This includes hospitals and clinics, clinical research laboratories, and academic institutes. According to the report, hospitals and clinics represented the largest market segmentation.

Hospitals and clinics accounted for the largest market share, as they are the primary end-users of plasma-derived therapies, which are essential for treating a wide range of medical conditions. These healthcare facilities frequently administer treatments like intravenous immunoglobulins (IVIG) for immune deficiencies, albumin for hypovolemia, and clotting factors for hemophilia patients. For instance, in cases of severe trauma or surgery, hospitals rely on albumin to restore blood volume and stabilize patients. The constant need for such critical therapies in acute care settings underscores the substantial demand from hospitals and clinics, making them the largest consumers in the plasma fractionation market. Their pivotal role in delivering comprehensive patient care drives the growth and prominence of this segment.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America exhibits a clear dominance

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

North America, particularly the United States, boasts advanced healthcare infrastructure with a well-established network of hospitals, clinics, and specialized treatment centers. This infrastructure supports the extensive use and distribution of plasma-derived therapies. Moreover, the region has a high demand for plasma-derived products due to a large patient population requiring treatments for various medical conditions, such as immunodeficiencies, hemophilia, autoimmune diseases, and neurological disorders. For instance, in March 2021, BPL sold 25 Grifols plasma facilities in the United States, resulting in an additional one million liters for plasma fractionation. Thus, such activities by leading industry players are expected to fuel market growth over the forecasted period.

Competitive Landscape:

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major plasma fractionation companies have also been provided. Some of the key players in the market include:

- ADMA Biologics Inc.

- Boccard

- CSL

- Grifols, S.A.

- Intas Pharmaceuticals Ltd.

- Kedrion

- LFB

- Octapharma AG

- PlasmaGen BioSciences Pvt. Ltd.

- Sartorius AG

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Plasma Fractionation Market Recent Developments:

- June 2024: Takeda announced that the Ministry of Health, Labour, and Welfare in Japan approved the use of CUVITRU, a replacement therapy in patients aged two years and older with agammaglobulinemia.

- June 2024: Grifols, one of the global healthcare firms, announced that its subsidiary Biotest received its first FDA approval with the intravenous immunoglobulin (Ig) treatment.

- June 2024: Takeda expanded additional plasma fractionation capacity of up to 2 million liters.

Plasma Fractionation Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Immunoglobulins, Albumin, Coagulation factor VIII, Coagulation factor IX |

| Sectors Covered | Private Sector, Public Sector |

| Applications Covered | Neurology, Immunology, Hematology, and Others |

| End Users Covered | Hospitals and Clinics, Clinical Research Laboratories, Academic Institutes |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ADMA Biologics Inc., Boccard, CSL, Grifols, S.A., Intas Pharmaceuticals Ltd., Kedrion, LFB, Octapharma AG, PlasmaGen BioSciences Pvt. Ltd., Sartorius AG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the plasma fractionation market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global plasma fractionation market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the plasma fractionation industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Plasma Fractionation Market Report

The global plasma fractionation market was valued at USD 27.7 Billion in 2025.

We expect the global plasma fractionation market to exhibit a CAGR of 4.67% during 2026-2034.

The sudden outbreak of the COVID-19 pandemic has led to the growing requirement for plasma fractionation to downstream processing of donated plasma for treating the coronavirus-infected patients.

The rising adoption of plasma fractionation to prevent, manage, and treat life-threatening conditions, such as infections, congenital deficiencies, rare blood disorders, etc., is primarily driving the global plasma fractionation market.

Based on the product, the global plasma fractionation market has been divided into immunoglobulins, albumin, coagulation factor VIII, and coagulation factor IX. Among these, immunoglobulins currently exhibit a clear dominance in the market.

Based on the sector, the global plasma fractionation market can be categorized into private sector and public sector. Currently, the private sector accounts for the majority of the total market share.

Based on the application, the global plasma fractionation market has been segregated into neurology, immunology, hematology, and other applications, where neurology currently holds the largest market share.

Based on the end user, the global plasma fractionation market can be bifurcated into hospitals and clinics, clinical research laboratories, and academic institutes. Currently, hospitals and clinics exhibit a clear dominance in the market.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global plasma fractionation market include ADMA Biologics Inc., Boccard, CSL, Grifols, S.A., Intas Pharmaceuticals Ltd., Kedrion, LFB, Octapharma AG, PlasmaGen BioSciences Pvt. Ltd., and Sartorius AG.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)