Plastic Compounding Market Size, Share, Trends and Forecast by Product, Application, and Region, 2026-2034

Plastic Compounding Market Size and Share:

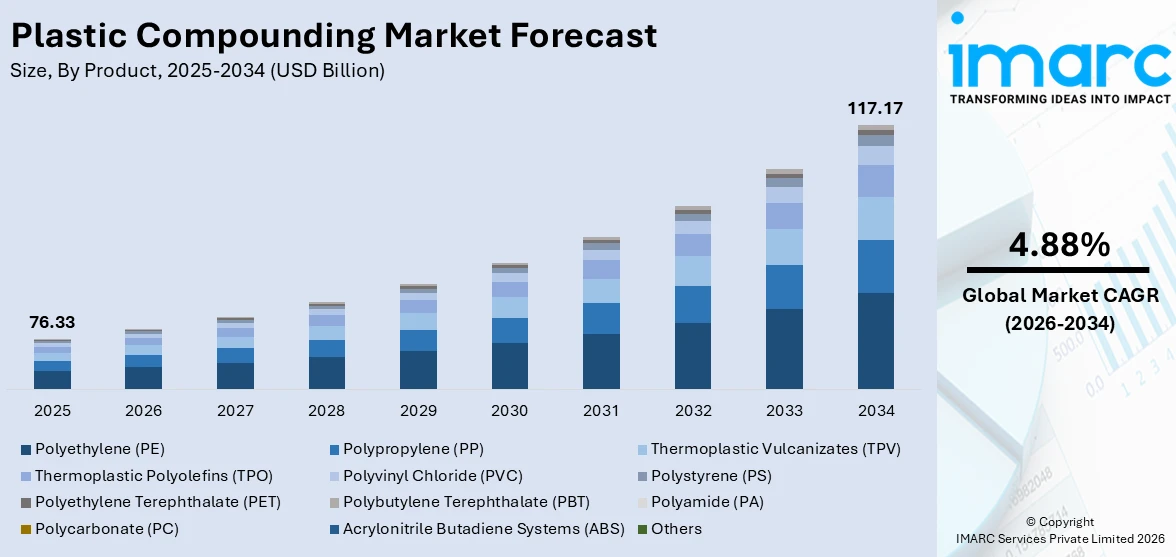

The global plastic compounding market size was valued at USD 76.33 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 117.17 Billion by 2034, exhibiting a CAGR of 4.88% from 2026-2034. North America currently dominates the market, holding a market share of 37% in 2025. The region’s prominence is underpinned by its robust automotive manufacturing ecosystem, well-established construction industry, widespread adoption of advanced polymer technologies, and intensifying regulatory frameworks promoting the use of sustainable and high-performance compounded materials, all of which expand the plastic compounding market share.

The global market is experiencing sustained growth driven by a convergence of industrial, environmental, and technological forces. Escalating demand from the automotive sector for lightweight, durable, and thermally resistant polymer materials has significantly expanded compounded plastic consumption, as vehicle manufacturers increasingly replace conventional metals to enhance fuel efficiency and reduce emissions. The rapid expansion of construction and infrastructure projects, particularly in developing economies, is generating consistent demand for polyvinyl chloride, polyethylene, and polypropylene compounds used in pipes, insulation, window profiles, and floor coverings. Additionally, the rapid proliferation of consumer electronics and electric vehicles is amplifying requirements for specialty compounds with superior flame retardancy and electrical insulation properties. The plastic compounding market growth is further supported by expanding healthcare applications, with specialized compounds finding increasing adoption in medical device manufacturing and pharmaceutical packaging, collectively broadening the demand landscape.

The United States has emerged as a major region in the market owing to many factors. The country's deeply entrenched automotive sector continues to drive demand for lightweight, high-performance compounded plastics, particularly as manufacturers accelerate production of electric and hybrid vehicles requiring advanced polymer solutions for battery enclosures, interior components, and structural parts. Strong construction and renovation activity across commercial and residential segments is further generating demand for PVC, polyethylene, and polypropylene compounds in pipes, fittings, and insulation. The expansion of packaging, electronics, and medical device industries within the US is broadening the application base for engineered plastic compounds. The plastic compounding market outlook in the US remains highly favorable, supported by government-backed industrial investments. For instance, in May 2024, the US government allocated USD 79.90 million to support a new electrically conductive polymer manufacturing facility near Charlotte, North Carolina, reinforcing the country's commitment to advanced materials manufacturing and innovation.

To get more information on this market Request Sample

Plastic Compounding Market Trends:

Rising Automotive Sector Demand and EV Adoption

The plastic compounding market is witnessing robust expansion driven by the automotive industry's accelerating shift toward lightweight, high-performance polymer materials. Automakers are progressively substituting conventional metal components with advanced compounded plastics, including polypropylene, polyamide, and thermoplastic polyolefins, to achieve meaningful weight reductions, thereby improving fuel economy and lowering tailpipe emissions in line with increasingly stringent global environmental standards. This transition is particularly pronounced in the electric vehicle (EV) segment, where compounded plastics serve critical functions in battery housings, thermal management systems, connectors, and structural components. The need for materials combining lightweight properties with superior flame resistance, dielectric strength, and mechanical durability is steering formulation innovation across the compound value chain. Regulatory pressure across North America, Europe, and key Asia-Pacific markets to reduce vehicle carbon footprints is amplifying compounding demand. For instance, in January 2025, a major Covestro announced an investment in the low triple-digit million Euro range to expand a US manufacturing facility with new production lines for tailored polycarbonate compounds and blends, reflecting the scale of automotive-driven demand.

Expanding Sustainable and Circular Compounding Solutions

Among the most significant plastic compounding market trends reshaping the industry is the accelerating transition toward sustainable, circular, and bio-based compounding solutions. Driven by tightening regulatory mandates compounders are investing heavily in recycled-content formulations and bio-based polymer blends. Post-consumer recycled content is increasingly being incorporated into polyolefin and engineering resin compounds for automotive and packaging applications, enabling manufacturers to meet minimum recycled content thresholds while maintaining material performance standards. Bioplastics and biodegradable compounds are gaining traction in consumer goods and packaging segments because of rising consumer environmental awareness and retailer sustainability commitments. Digital process optimization and AI-assisted formulation tools are also advancing the efficiency and quality of sustainable compounding operations. In September 2025, Borealis invested over €100 million to expand its polypropylene compounding operations in Schwechat, Austria, with commercial production scheduled for H2 2026, underscoring the industry's commitment to scaling sustainable compound supply.

Growing Construction and Electrical Industries

The plastic compounding market forecast points to sustained momentum driven by the expanding construction and electrical and electronics sectors globally. Compounded plastics are indispensable in construction, finding application in pipes, cable insulation, window profiles, floor coverings, and weatherproof cladding due to their corrosion resistance, design flexibility, and durability. Governments in Asia, the Middle East, Latin America, and Africa are channeling substantial investments into urban infrastructure, transportation networks, and affordable housing projects, generating persistent demand for PVC, polyethylene, and polypropylene compounds. Concurrently, the proliferation of 5G infrastructure, data centers, and consumer electronics is driving demand for specialty compounds with enhanced electrical insulation, heat resistance, and electromagnetic shielding properties. Miniaturization trends in electronics are pushing compounders to develop high-precision formulations with tighter tolerances and specialized performance profiles. The integration of flame-retardant, UV-resistant, and weather-resistant additives is further expanding compound applicability across diverse climates and conditions. According to the World Economic Forum, in 2025, 69% of industry stakeholders regard sustainable construction as a priority, reinforcing the long-term demand trajectory for high-performance compounded plastics in the construction sector.

Plastic Compounding Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global plastic compounding market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product and application.

Analysis by Product:

- Polyethylene (PE)

- Polypropylene (PP)

- Thermoplastic Vulcanizates (TPV)

- Thermoplastic Polyolefins (TPO)

- Polyvinyl Chloride (PVC)

- Polystyrene (PS)

- Polyethylene Terephthalate (PET)

- Polybutylene Terephthalate (PBT)

- Polyamide (PA)

- Polycarbonate (PC)

- Acrylonitrile Butadiene Systems (ABS)

- Others

Polyethylene (PE) holds 20% of the market share. Polyethylene is one of the most versatile and widely produced synthetic thermoplastics, valued for its exceptional chemical resistance, flexibility, low moisture absorption, and cost-effective production from petrochemical feedstocks. Within plastic compounding, polyethylene serves as a foundational resin that is blended with functional additives such as UV stabilizers, antioxidants, colorants, and reinforcing fillers to tailor its mechanical, thermal, and optical properties for specific end-use applications. PE compounds are extensively used across packaging, construction, agricultural films, and pipe manufacturing, offering a balance of processability and performance. The growing emphasis on the plastic compounding market forecast for sustainable packaging is accelerating the development of recycled-content polyethylene compounds, where post-consumer PE is reprocessed and enhanced with compatibilizers and performance additives to meet the demands of circular packaging applications. Low-density, high-density, and linear low-density variants of polyethylene are each compounded differently to serve distinct market needs.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Automotive

- Building & Construction

- Electrical & Electronics

- Packaging

- Consumer Goods

- Industrial Machinery

- Medical Device

- Optical Media

- Others

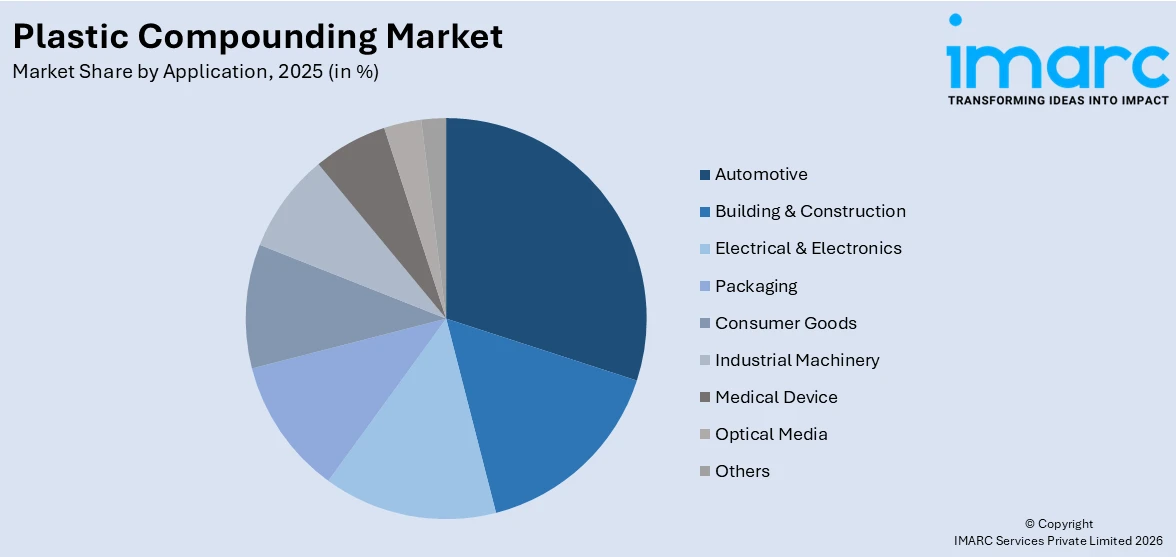

Automotive leads the market with a share of 25%. The automotive application segment is the primary driver of demand within the plastic compounding market, reflecting the industry's deep and growing reliance on engineered polymer materials to replace metals, reduce vehicle weight, and meet progressively stringent fuel efficiency and emissions regulations. Compounded plastics are deployed across a wide range of vehicle systems, including dashboards, bumpers, door panels, under-hood components, cable insulation, battery casings, and structural panels. Polypropylene, polyamide, thermoplastic polyolefins, and acrylonitrile butadiene styrene dominate automotive compound consumption due to their superior strength-to-weight ratios, thermal stability, and ease of processing. The accelerating global adoption of electric and hybrid vehicles is further amplifying compounding demand, as EVs require advanced polymer solutions for thermal management, battery integration, and lightweight structural components. Regulatory momentum toward net-zero vehicle fleets is compelling automakers worldwide to partner with compounders on next-generation lightweight material solutions.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 37% of the share, enjoys the leading position in the market. The region's dominance in global plastic compounding is anchored by its expansive automotive manufacturing base, which sustains large-scale demand for polypropylene, polyamide, and thermoplastic polyolefin compounds. The United States and Canada together host a mature and technologically advanced chemicals and polymer industry that supports sophisticated compound development for automotive, construction, packaging, electronics, and healthcare applications. Strong government emphasis on sustainable manufacturing and recycled-content materials is driving investment in bio-based and recycled polymer compounding facilities. The construction sector's continued expansion, supported by infrastructure renewal programs and housing investment, sustains steady demand for PVC, polyethylene, and polystyrene compounds used in pipes, profiles, and insulation. The rapid adoption of electric vehicles in the region is generating significant compounding demand for battery-grade and lightweight structural polymer materials. In March 2025, Plastic Recycling Inc. (PRI) significantly expanded its extruder systems and laboratory infrastructure to increase capacity for compounding with high-grade recycled resins targeting automotive and electronics applications, highlighting North America's growing circular compounding ecosystem.

Key Regional Takeaways:

United States Plastic Compounding Market Analysis

United States represents the most dynamic and technologically advanced plastic compounding market in North America, underpinned by its mature industrial base across automotive, construction, packaging, electronics, and medical device manufacturing sectors. The country's automotive industry is a dominant demand driver, as producers increasingly source lightweight and high-performance compounded plastics to meet corporate average fuel economy standards and support EV production lines. Federal and state-level infrastructure investment programs are fueling construction-related demand for PVC, polyethylene, and polypropylene compounds. The packaging sector's ongoing shift toward recyclable and recycled-content materials is accelerating the adoption of compounded post-consumer resins. The US government's commitment to reshoring advanced manufacturing is also catalyzing domestic compounding capacity expansions. The country's deep network of polymer research institutions and chemical innovators supports continuous formulation advancement. In 2024, Finnish compounder Premix Oy inaugurated an office on May 3 at the location of its inaugural US facility, situated just outside Charlotte, NC, to manufacture electrically conductive (EC) plastic compounds and masterbatches. Production is set to start in early 2025, featuring two compounding lines that can ultimately yield approximately 45 million pounds annually of black masterbatches made from polyethylene and polypropylene.

Europe Plastic Compounding Market Analysis

Europe represents a significant and innovation-driven market for plastic compounding, characterized by stringent environmental regulations and a strong industrial tradition across automotive, electronics, packaging, and construction. The European Union's Green Deal framework and Packaging and Packaging Waste Regulation are compelling manufacturers to adopt recycled-content and bio-based compounded plastics, fundamentally reshaping regional compound formulation strategies. Germany's robust automotive and machinery industries generate consistent demand for engineering-grade PA, PC, and PP compounds, while France, Italy, and Spain contribute automotive and consumer goods compounding demand. Sustainable compounding capacity is expanding rapidly across the continent, driven by circular economy mandates that require minimum recycled content in automotive and packaging applications. The transition to electric vehicles across EU member states is further amplifying demand for advanced polymer compounds in battery systems, lightweight structural components, and electronic housings. In 2025, Envalior announced its plans to invest in a Polyphenylene Sulfide compounding facility in Europe.

Asia-Pacific Plastic Compounding Market Analysis

Asia-Pacific is the largest and fastest-growing region in the global plastic compounding market, driven by rapid industrialization, massive automotive production, booming electronics manufacturing, and large-scale construction activity. China, Japan, India, South Korea, and Indonesia collectively account for the bulk of regional demand, with compounded plastics serving automotive OEMs, electronics assemblers, and packaging producers across these markets. Regional manufacturers are investing in capacity expansions and sustainability-focused formulations to meet growing regulatory and market requirements. In 2024, LyondellBasell (LYB) revealed the launch of a new production line at the Dalian location of its Advanced Polymer Solutions (APS) division, enhancing its footprint in China. The new manufacturing line will generate a diverse array of high-performance, top-quality polypropylene compounds, primarily serving the automotive sector. The new production line, designated as the second at the Dalian site and with an annual capacity of 20,000 tonnes, will double the existing production capacity of the site, improving the company’s capability to satisfy the increasing market demand. At present, the APS business manages five locations in China, featuring a range of PP compounding, engineered plastics, and masterbatch products.

Latin America Plastic Compounding Market Analysis

Latin America is emerging as a growth-oriented market for plastic compounding, driven by industrialization, rising consumer spending, and expanding construction and automotive activities across Brazil, Mexico, and Colombia. Mexico's proximity to major North American automotive production networks is positioning it as an increasingly important source of compounded plastic components for the regional supply chain. Construction and infrastructure investment across urban centers is driving demand for PVC and polyethylene compounds in pipes, fittings, and insulation. Brazil's manufacturing sector is growing steadily, supported by government-led industrial programs.

Middle East and Africa Plastic Compounding Market Analysis

The Middle East and Africa market for plastic compounding is experiencing gradual but meaningful growth, supported by infrastructure development, a diversifying industrial base, and petrochemical integration advantages in the Gulf Cooperation Council countries. Saudi Arabia, the UAE, and South Africa are the primary compounding demand centers, with the automotive, construction, and packaging sectors driving consumption of polyolefin and engineering resin compounds. Petrochemical-rich Gulf nations benefit from feedstock cost advantages, positioning regional compounders favorably in global supply chains. Saudi Arabia's Vision 2030 initiative has attracted over USD 100 billion in manufacturing-related foreign direct investment through 2025, bolstering construction and industrial activity that in turn strengthens demand for plastic compounds across diverse end-use sectors.

Competitive Landscape:

The global plastic compounding market is characterized by the presence of numerous multinational corporations alongside regional and specialty compounders competing across product type, geography, and application expertise. Leading players are continuously expanding their portfolios through research and development focused on high-performance, sustainable, and bio-based formulations tailored to the evolving demands of the automotive, packaging, electronics, and construction industries. Strategic mergers, acquisitions, and capacity expansions are reshaping the landscape as major participants seek to consolidate positions and access new geographies. Companies are investing in advanced compounding technologies, including twin-screw extrusion platforms and AI-assisted inline quality monitoring, to improve production efficiency and meet stringent material specifications. Sustainability-driven differentiation has become a primary competitive lever, with players developing certified-circular compounds and recycled-content grades to satisfy regulatory and customer requirements. Collaboration with end-use industry OEMs is driving accelerated innovation in specialty and application-specific compound development, positioning compounders as integral strategic partners across the global manufacturing ecosystem.

The report provides a comprehensive analysis of the competitive landscape in the plastic compounding market with detailed profiles of all major companies, including:

- Adell Plastics Inc.

- AKRO-PLASTIC GmbH

- Aurora Material Solutions

- Covestro AG

- Kraton Corporation

- Kuraray Co., Ltd

- LyondellBasell Industries Holdings B.V.

- Polyvisions, Inc.

- Ravago Manufacturing Group of Companies

Latest News and Developments:

- May 2025: DOMO Chemicals, a top worldwide provider of high-performance solutions under the TECHNYL® brand, has officially increased its compounding activities in Mumbai, India. This strategic growth enhances DOMO’s role as a solutions provider in the area and broadens its collection of engineered materials derived from polyamides and various resins.

- April 2025: Star Plastics® is a top custom compounder of engineering-grade thermoplastics and has introduced six new polycarbonate compounds that do not contain per- and polyfluoroalkyl substances (PFAS). This expands the company’s total of PFAS-free products to eight, available in both recycled and raw material forms.

Plastic Compounding Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Polyethylene (PE), Polypropylene (PP), Thermoplastic Vulcanizates (TPV), Thermoplastic Polyolefins (TPO), Polyvinyl Chloride (PVC), Polystyrene (PS), Polyethylene Terephthalate (PET), Polybutylene Terephthalate (PBT), Polyamide (PA), Polycarbonate (PC), Acrylonitrile Butadiene Systems (ABS), Others |

| Applications Covered | Automotive, Building and Construction, Electrical and Electronics, Packaging, Consumer Goods, Industrial Machinery, Medical Device, Optical Media, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Adell Plastics Inc., AKRO-PLASTIC GmbH, Aurora Material Solutions, Covestro AG, Kraton Corporation, Kuraray Co., Ltd, LyondellBasell Industries Holdings B.V., Polyvisions, Inc., Ravago Manufacturing Group of Companies, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the plastic compounding market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global plastic compounding market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the plastic compounding industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Plastic Compounding Market Report

The plastic compounding market was valued at USD 76.33 Billion in 2025.

The plastic compounding market is projected to exhibit a CAGR of 4.88% during 2026-2034, reaching a value of USD 117.17 Billion by 2034.

The plastic compounding market is propelled by escalating demand from the automotive sector for lightweight and durable polymer materials, growing construction and infrastructure investment globally, rising adoption of electric vehicles, expanding electronics manufacturing, stringent sustainability regulations encouraging recycled and bio-based compounds, and increasing medical device production requiring specialized high-performance polymer formulations.

North America currently dominates the market, accounting for a share of 37%. The region benefits from a robust automotive manufacturing base, active construction and infrastructure investment, widespread adoption of sustainable compounded materials, and strong regulatory frameworks that consistently drive demand for advanced polymer compound solutions.

Some of the major players in the plastic compounding market include Adell Plastics Inc., AKRO-PLASTIC GmbH, Aurora Material Solutions, Covestro AG, Kraton Corporation, Kuraray Co., Ltd, LyondellBasell Industries Holdings B.V., Polyvisions, Inc., Ravago Manufacturing Group of Companies, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)