Portugal Auto Insurance Market Size, Share, Trends and Forecast by Coverage, Distribution Channel, Vehicle Age, Application, and Region, 2026-2034

Portugal Auto Insurance Market Summary:

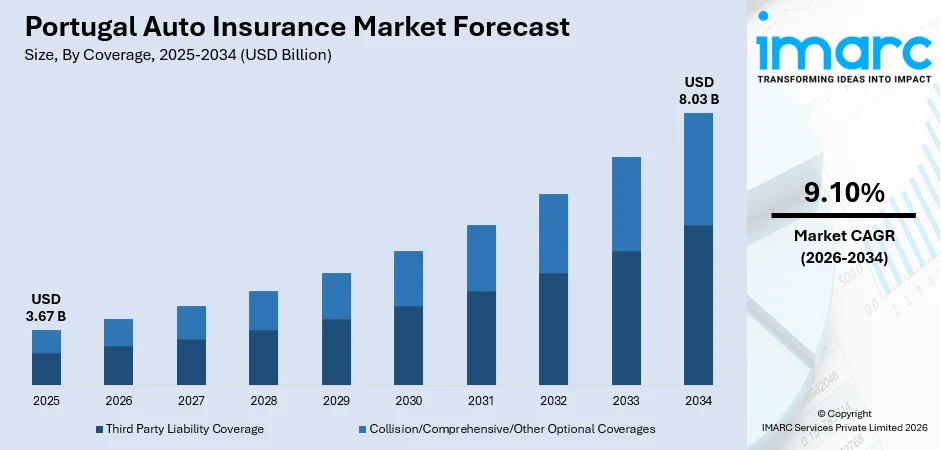

The Portugal auto insurance market size was valued at USD 3.67 Billion in 2025 and is projected to reach USD 8.03 Billion by 2034, growing at a compound annual growth rate of 9.10% from 2026-2034.

The Portugal auto insurance market is experiencing sustained momentum as regulatory reforms, rising vehicle registrations, and digital innovation reshape the industry landscape. Mandatory third-party liability requirements, expanding consumer awareness, and advancements in telematics-based coverage are strengthening policyholder engagement. Growing demand for personalized products, improved claims processing through artificial intelligence, and increasing adoption of comprehensive coverage options are driving broader participation, reinforcing the foundations for long-term Portugal auto insurance market share.

Key Takeaways and Insights:

- By Coverage: Third party liability coverage reigns the market with a share of 63.2% in 2025, owing to mandatory legal requirements for all registered vehicles, high minimum coverage thresholds, and strong regulatory enforcement by the Insurance and Pension Funds Supervisory Authority.

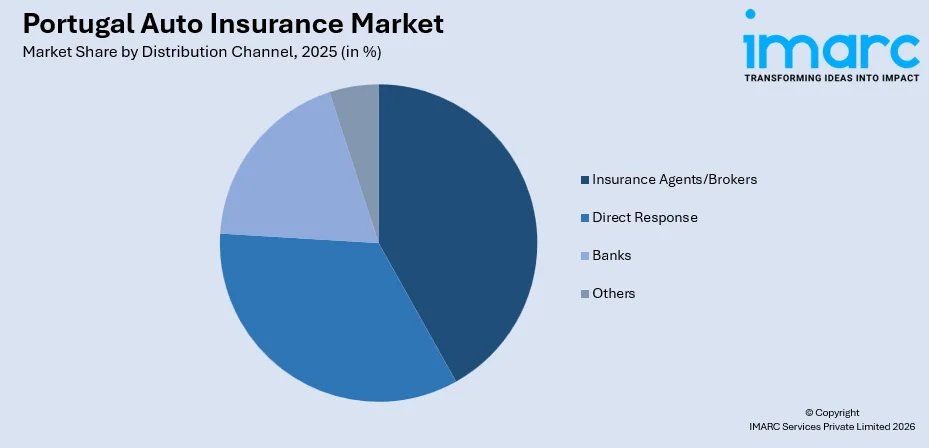

- By Distribution Channel: Insurance agents and brokers lead the market with a share of 41.8% in 2025, driven by established consumer trust in personalized advisory services, cultural preference for human interaction during policy placement, and extensive intermediary networks across the country.

- By Vehicle Age: Used vehicles represent the largest segment with a share of 57.6% in 2025, reflecting the aging composition of Portugal’s vehicle fleet, significant reliance on used car imports from the European Union, and cost-conscious consumer preferences favoring pre-owned automobiles.

- By Application: Personal dominates the market with a share of 69.3% in 2025, driven by rising individual vehicle ownership, expanding urban commuting needs, and growing consumer awareness of comprehensive coverage benefits beyond basic liability requirements.

- By Region: A. M. Lisboa comprises the biggest region with a share of 36.4% in 2025, supported by the concentration of Portugal’s population and economic activity in the Lisbon metropolitan area, higher vehicle density, and greater demand for diverse insurance products.

- Key Players: The market is competitive, led by established domestic insurers and European groups offering comprehensive coverage. Price competition is strong, supported by digital distribution and comparison platforms. Differentiation increasingly relies on bundled services, telematics-based policies, claims efficiency, and customer experience improvements.

To get more information on this market Request Sample

The Portugal auto insurance market is advancing as regulatory modernization, digital transformation, and evolving consumer expectations converge to reshape the competitive landscape. A key factor driving this momentum is the country’s strengthening regulatory framework, which enhances consumer protection and supports market transparency. For instance, in March 2025, Portugal published Decree-Law No. 26/2025, transposing the EU’s 6th Motor Insurance Directive into national law, strengthening protections for road accident victims, facilitating insurer switches, and updating minimum compulsory insurance amounts. The integration of real-time monitoring and preventive safety features is further strengthening customer retention and competitive differentiation in Portugal’s auto insurance market. Apart from this, the introduction of independent price comparison tools and non-discriminatory claims-history treatment are also encouraging more informed consumer decisions and broadening market participation across all coverage segments.

Portugal Auto Insurance Market Trends:

Accelerated Digitalization and Insurtech Integration

Portugal’s auto insurance sector is accelerating its digital shift as insurers expand mobile platforms, online quotation engines, and remote claims processing capabilities. As such, Fidelidade, the country’s largest insurer, reported that its mobile application exceeded 1.6 million registered users by mid-2024, accounting for a notable share of the population. This growing adoption of digital channels is enabling faster policy issuance, simplified renewals, real-time claims tracking, and improved customer interaction, ultimately supporting stronger efficiency, cost optimization, and sustained market growth.

Rising Adoption of AI-Powered Claims Processing

Artificial intelligence is reshaping claims management across Portugal’s motor insurance market by enhancing operational efficiency and service responsiveness. Insurers are deploying AI-driven systems to accelerate data capture, automate document verification, identify suspicious claim patterns, and improve customer communication workflows. By reducing manual intervention and minimizing errors, these technologies enable quicker assessments and faster settlements. The resulting improvements in processing speed, fraud mitigation, and transparency are strengthening customer trust while supporting cost control and long-term competitiveness within the sector.

Strengthened Motor Insurance Regulatory Framework

Portugal is reinforcing its motor insurance regulatory environment to align with European standards and enhance policyholder protection. Accordingly, in March 2025, the government published Decree-Law No. 26/2025, transposing the EU Directive 2021/2118, which updated minimum compulsory insurance amounts to EUR 6.45 Million for bodily injury and EUR 1.3 Million for material damage per accident. These measures are increasing coverage adequacy and fostering greater consumer confidence in the market.

Market Outlook 2026-2034:

Portugal’s auto insurance market is positioned for sustained expansion, supported by regulatory modernization, increasing vehicle registrations, and growing digital adoption among insurers and policyholders. In accordance with this, ongoing investments in telematics, AI-driven underwriting, and enhanced consumer protection frameworks are expected to broaden market participation and improve service delivery. As such, in January 2026, Targa Telematics launched Targa Tacho in Portugal, a digital tachograph and compliance solution for transport companies. Integrated into the Trackit platform, it automates data downloads, analyzes infractions, reduces legal risks, and improves fleet efficiency. Additionally, the rising penetration of comprehensive coverage products and expanding electric vehicle registrations are creating new revenue opportunities that will contribute to a more diversified and competitive insurance landscape. The market generated a revenue of USD 3.67 Billion in 2025 and is projected to reach a revenue of USD 8.03 Billion by 2034, growing at a compound annual growth rate of 9.10% from 2026-2034.

Portugal Auto Insurance Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Coverage |

Third Party Liability Coverage |

63.2% |

|

Distribution Channel |

Insurance Agents and Brokers |

41.8% |

|

Vehicle Age |

Used Vehicles |

57.6% |

|

Application |

Personal |

69.3% |

|

Region |

A. M. Lisboa |

36.4% |

Coverage Insights:

- Third Party Liability Coverage

- Collision/Comprehensive/Other Optional Coverages

Third party liability coverage dominates with a share of 63.2% of the total Portugal auto insurance market in 2025.

Third-party liability coverage remains the cornerstone of Portugal’s auto insurance market, as national law mandates that all registered and roadworthy vehicles carry this protection. The regulatory framework, overseen by the Insurance and Pension Funds Supervisory Authority, enforces strict compliance, ensuring broad-based policyholder participation. Rising vehicle registrations and growing awareness of legal obligations continue to sustain demand for mandatory coverage. In 2024, Portugal recorded approximately 185,345 new passenger car registrations, reflecting a 2.81% year-on-year increase that further expanded the base of insured vehicles requiring liability protection.

The dominance of third-party liability is reinforced by updated minimum coverage requirements that ensure adequate financial protection for accident victims. Consumer preference for cost-effective basic coverage, particularly among owners of older and lower-value vehicles, supports the segment’s leading position. Insurers are also enhancing their liability offerings with supplementary features such as legal assistance and roadside support, attracting policyholders seeking added value while maintaining compliance with regulatory mandates.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Insurance Agents/Brokers

- Direct Response

- Banks

- Others

Insurance agents and brokers lead the market with a revenue share of 41.8% of the total Portugal auto insurance market in 2025.

Insurance agents and brokers continue to hold a commanding position in Portugal’s auto insurance distribution landscape, benefiting from deeply entrenched consumer trust and personalized advisory services. The Portuguese insurance culture favors direct interaction with intermediaries during policy selection and claims processes. The intermediary commission pool across Portugal’s insurance market amounted to approximately EUR 1.2 Billion in 2022, reflecting the significant economic role these distribution channels play in sustaining market connectivity and consumer engagement throughout the insurance value chain.

The enduring relevance of agents and brokers is further supported by their ability to offer tailored policy recommendations, comparative pricing, and hands-on claims assistance that digital channels have yet to fully replicate. While digital distribution is gaining traction among younger demographics, the majority of Portuguese consumers still prefer human interaction for complex insurance decisions, particularly when navigating comprehensive or multi-vehicle coverage options.

Vehicle Age Insights:

- New Vehicles

- Used Vehicles

Used vehicles hold the largest share at 57.6% of the total Portugal auto insurance market in 2025.

Used vehicles dominate Portugal’s auto insurance market, reflecting the country’s aging vehicle fleet and strong consumer preference for pre-owned automobiles. According to available data, vehicles over 10 years old account for approximately 63% of the Portuguese light passenger vehicle fleet, with over a quarter exceeding 20 years of age. This aging fleet composition naturally drives higher demand for insurance coverage tailored to older vehicles, including basic third-party liability and supplementary protections.

Portugal’s used vehicle segment is further sustained by the country’s significant reliance on used car imports from European Union member states. Used light passenger vehicles imported from the EU comprised over 67% of the Portuguese car market in recent years, underscoring the role of cross-border trade in shaping insurance demand patterns. Owners of used vehicles typically favor cost-effective coverage solutions that balance affordability with essential protection requirements.

Application Insights:

- Personal

- Commercial

Personal application accounts for the highest revenue share of 69.3% of the total Portugal auto insurance market in 2025.

Personal auto insurance constitutes the largest application segment in Portugal, driven by rising individual vehicle ownership, expanding urban mobility needs, and mandatory coverage requirements for all private vehicle owners. The increasing number of passenger car registrations reflects growing consumer participation in the automotive ecosystem. Urban commuting patterns, particularly in metropolitan areas such as Lisbon and Porto, further sustain demand for personal coverage products.

The personal segment benefits from evolving consumer expectations for customized coverage options, including add-on features such as roadside assistance, glass replacement, and legal protection. Insurers are responding by developing flexible policy structures that allow individuals to tailor coverage levels to their driving habits and risk profiles, enhancing engagement and retention across the personal lines portfolio.

Regional Insights:

- Norte

- Centro

- A. M. Lisboa

- Alentejo

- Others

A. M. Lisboa represents the leading region with a 36.4% share of the total Portugal auto insurance market in 2025.

The Lisbon metropolitan area commands the largest share of Portugal’s auto insurance market, benefiting from the country’s highest population density, concentrated economic activity, and elevated vehicle usage patterns. As the national capital and primary commercial hub, A. M. Lisboa generates substantial demand for both personal and commercial auto insurance products. The region’s extensive urban road networks, higher traffic volumes, and greater incidence of commuter-driven mobility create a robust foundation for insurance uptake. For example, in September 2025, Igneo Infrastructure Partners agreed to acquire up to 100% of Portuguese road concessionaires AAVI and AENL from CVC DIF funds. The Lisbon-announced deal expands Igneo’s toll road network, creating the country’s third-largest operator, pending approvals in Q4 2025.

Additionally, Lisbon plays a central role in shaping Portugal’s auto insurance market, as it hosts the headquarters of major insurers, extensive broker networks, and fast-growing digital distribution platforms. This geographic concentration enhances consumer access to a wide range of policy options, competitive pricing models, and value-added services. The strong presence of insurers and intermediaries in the capital also supports innovation in customer engagement, accelerating product diversification and improving overall market reach for policyholders nationwide.

Market Dynamics:

Growth Drivers:

Why is the Portugal Auto Insurance Market Growing?

Mandatory Coverage Requirements and Expanding Vehicle Fleet

Portugal’s auto insurance market benefits fundamentally from the legal mandate requiring all registered and roadworthy vehicles to carry third-party liability coverage. This compulsory framework ensures a broad and stable policyholder base that expands in tandem with vehicle registrations. The national fleet continues to grow as consumer purchasing power strengthens, and mobility demands increase across urban and rural areas. Likewise, rising new car registrations and sustained used vehicle imports from European Union member states are contributing to a continuously expanding insured vehicle population. According to figures from the Portuguese Automobile Association (ACAP), new vehicle registrations in Portugal reached 264,821 in 2025, marking a 6.2% rise compared with the previous year. This growth in the vehicle fleet directly translates into higher demand for mandatory and optional insurance products, supporting consistent premium revenue generation across the market.

Digital Transformation and Technology-Driven Innovation

The adoption of digital technologies is transforming how auto insurance is distributed, underwritten, and serviced in Portugal. Insurers are increasingly deploying mobile applications, AI-powered claims tools, and telematics-based solutions to improve operational efficiency and customer experience. These innovations are reducing processing times, enhancing fraud detection, and enabling more personalized pricing models. This shift toward digital engagement is broadening market reach, attracting younger demographics, and reducing distribution costs, all of which contribute to sustained market expansion.

Evolving Regulatory Landscape and Consumer Protection Enhancements

Portugal’s regulatory environment continues to evolve in alignment with European Union directives, creating a more transparent, competitive, and consumer-friendly insurance market. The International Conference on Insurance Fraud Detection and Risk Prevention planned to take place on 25 November 2026 in Lisbon, Portugal. Organized by Research Fora, the event will gather global experts, researchers, and practitioners to discuss industry innovations and risk mitigation strategies. Regulatory reforms are strengthening policyholder protections, improving claims-handling standards, and encouraging innovation across the industry. Moreover, the Portuguese government updated minimum compulsory coverage amounts, introduced non-discriminatory treatment of cross-border claims histories, and authorized the development of independent price comparison tools. These measures are enhancing market transparency and empowering consumers to make more informed coverage decisions.

Market Restraints:

What Challenges the Portugal Auto Insurance Market is Facing?

Rising Claims Costs and Increasing Road Casualty Frequency

The Portugal auto insurance market is experiencing mounting pressure from escalating claims costs linked to higher vehicle repair expenses, rising medical treatment charges, and growing accident frequency. More complex vehicle technologies and inflation in spare parts and labor have significantly increased average claim severity. Although safety initiatives continue, accident volumes remain elevated, sustaining payout levels and administrative burdens for insurers. This environment is contributing to tighter underwriting conditions, reduced profitability margins, and gradual upward pressure on motor insurance premiums nationwide.

High Market Concentration Limiting Competitive Dynamics

The Portuguese auto insurance market remains highly concentrated, with a small group of dominant insurers controlling a substantial share of total premium income. This concentration creates structural barriers for smaller players and new entrants attempting to gain meaningful scale. Limited competitive intensity can constrain product differentiation and reduce pricing flexibility, particularly in standardized motor coverage segments. Additionally, strong brand loyalty and established broker networks reinforce incumbent advantages, making market penetration costly and slowing the pace of innovation across the sector.

Regulatory Compliance Burden and Operational Complexity

Auto insurers in Portugal face increasing regulatory complexity driven by evolving European compliance frameworks, including digital resilience requirements, anti-money laundering standards, and stricter ICT governance rules. Meeting these obligations demands substantial investment in cybersecurity infrastructure, internal controls, data reporting systems, and risk oversight mechanisms. The growing compliance workload elevates operational costs and stretches organizational resources. As insurers allocate more capital and expertise toward regulatory adherence, fewer resources remain available for product innovation, digital enhancement, and customer experience improvements.

Competitive Landscape:

The Portugal auto insurance market operates within a concentrated competitive structure, with leading insurers maintaining dominant positions through diversified product portfolios, extensive distribution networks, and continuous technology investments. Companies are competing on digital innovation, claims processing speed, and personalized coverage offerings to differentiate themselves. Strategic mergers, acquisitions, and partnerships are reshaping market positioning as domestic and international players seek to expand their footprint. The regulatory emphasis on transparency, consumer protection, and digital readiness is further intensifying competition and encouraging incumbents to modernize operations while creating selective entry opportunities for specialized insurtech firms.

Recent Developments:

- In December 2025, Great American Insurance Group planned to expand into Portugal’s casualty insurance market through its Madrid office. Specializing in commercial property and casualty coverage across multiple industries, GAIG sees strong growth potential as new operators enter the sector. The move follows its successful casualty expansion trend in Spain.

- In January 2024, Fidelidade, Portugal’s largest insurer with a 30.7% market share, launched AutoDigital, an augmented reality app to simplify car insurance claims. Built with OutSystems and supported by valantic LCS, the tool uses AR and machine learning to assess vehicle damage remotely in under five minutes.

Portugal Auto Insurance Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Coverages Covered |

Third Party Liability Coverage, Collision/Comprehensive/Other Optional Coverages |

|

Distribution Channels Covered |

Insurance Agents/Brokers, Direct Response, Banks, Others |

|

Vehicle Ages Covered |

New Vehicles, Used Vehicles |

|

Applications Covered |

Personal, Commercial |

|

Regions Covered |

Norte, Centro, A. M. Lisboa, Alentejo, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Portugal Auto Insurance Market Report

The Portugal auto insurance market size was valued at USD 3.67 Billion in 2025.

The Portugal auto insurance market is expected to grow at a compound annual growth rate of 9.10% from 2026-2034 to reach USD 8.03 Billion by 2034.

Third party liability coverage dominated the market with a share of 63.2%, driven by mandatory legal requirements for all registered vehicles, high minimum coverage thresholds, and consistent regulatory enforcement across the country.

Key factors driving the Portugal auto insurance market include mandatory coverage requirements, expanding vehicle registrations, digital transformation across distribution and claims, evolving regulatory frameworks, and rising consumer demand for comprehensive coverage products.

Major challenges include rising claims costs from increasing road accidents, high market concentration limiting competitive dynamics, mounting regulatory compliance burdens, escalating repair and medical expenses, and operational complexity from new European digital resilience requirements.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)