Portugal Packaging Market Size, Share, Trends and Forecast by Material, Product Type, Packaging Type, End Use Industry, and Region, 2026-2034

Portugal Packaging Market Summary:

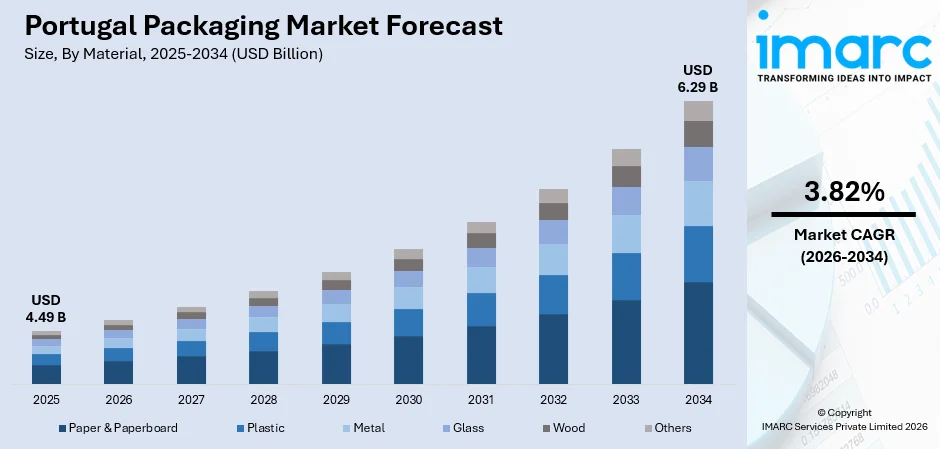

The Portugal packaging market size was valued at USD 4.49 Billion in 2025 and is projected to reach USD 6.29 Billion by 2034, growing at a compound annual growth rate of 3.82% from 2026-2034.

The Portugal packaging market is advancing steadily, underpinned by the country's robust food processing industry, growing e-commerce penetration, and stringent European Union sustainability mandates. Increasing consumer preference for eco-friendly and recyclable packaging formats is encouraging manufacturers to invest in innovative materials and production technologies. Moreover, expansion in the retail sector, rising tourism-driven demand, and modernization of supply chain logistics are reinforcing domestic packaging consumption, contributing to Portugal packaging market share.

Key Takeaways and Insights:

- By Material: Paper and paperboard dominate the market with a share of 38.7% in 2025, driven by increasing regulatory pressure to reduce plastic usage and rising consumer demand for recyclable, biodegradable packaging alternatives that align with circular economy principles.

- By Product Type: Flexible packaging leads the market with a share of 42.9% in 2025, owing to its lightweight nature, superior cost-efficiency, extended shelf-life capabilities, and growing adoption across food, beverage, and personal care sectors in Portugal.

- By Packaging Type: Primary packaging represents the largest segment with a market share of 55.4% in 2025, reflecting its essential role in direct product containment, consumer safety, and regulatory compliance across food, pharmaceutical, and consumer goods industries.

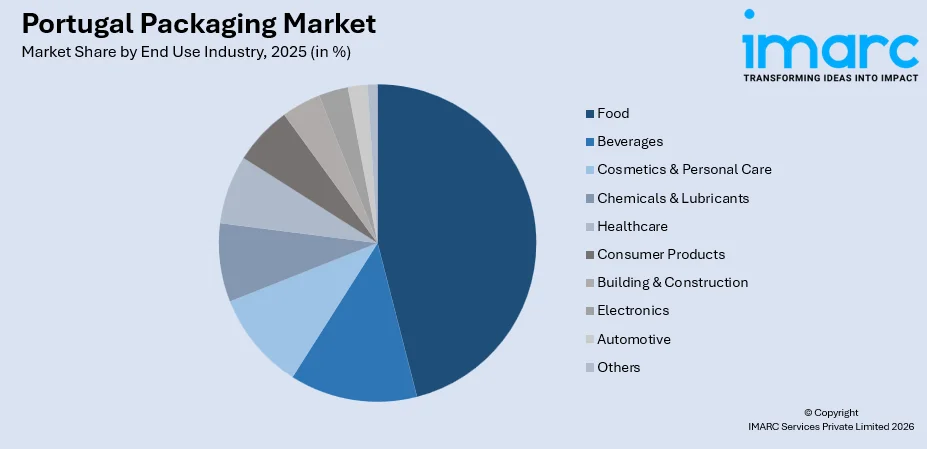

- By End Use Industry: Food exhibits a clear dominance in the market with 46.1% share in 2025, underpinned by Portugal's strong agricultural heritage, expanding processed food production, and growing demand for convenience-oriented packaging solutions across retail channels.

- By Region: A. M. Lisboa comprises the largest region with 34.5% share in 2025, driven by the concentration of Portugal's economic activity, consumer base, and logistics infrastructure within the metropolitan capital area and its surrounding industrial zones.

- Key Players: The market is moderately fragmented, with established local converters competing alongside multinational groups. Competition centers on cost efficiency, sustainable materials, lightweight designs, and compliance with EU circular economy rules. Flexible packaging and paper-based solutions are gaining traction, intensifying innovation and consolidation pressures.

To get more information on this market Request Sample

The Portugal packaging market is progressing as sustainability mandates, evolving consumer preferences, and technological innovation converge to reshape the industry landscape. The European Union's Packaging and Packaging Waste Regulation, adopted in December 2024 and entering into force in February 2025, establishes directly applicable requirements for recyclability, reuse, and recycled content across all member states, including Portugal. This regulatory framework is prompting domestic manufacturers to accelerate investments in paper-based, compostable, and mono-material packaging solutions. For instance, in 2024, the Portuguese Green Dot System, in collaboration with Logoplaste Innovation Lab and Bureau Veritas Certification, launched the RecyClass recyclability certification scheme to assess the recyclability of plastic packaging, supporting brand compliance with EU packaging requirements. Growing e-commerce activity, retail modernization, and rising demand for convenient food packaging are further reinforcing market expansion. Besides this, continued investments in circular economy infrastructure and material innovation are expected to sustain Portugal's packaging market trajectory over the forecast period.

Portugal Packaging Market Trends:

Accelerating Transition Toward Sustainable and Paper-Based Packaging

Portugal is witnessing a decisive shift toward sustainable packaging solutions as regulatory mandates and consumer preferences converge. The country's alignment with EU circular economy directives is accelerating adoption of recyclable and compostable materials. For instance, in May 2025, The Navigator Company approved a EUR 30 Million investment to convert its PM3 paper machine in Setúbal to produce low-grammage flexible packaging papers in the 30–90 gsm range, targeting sustainable alternatives for food and non-food applications. This trend supports long-term Portugal packaging market growth.

Rising Adoption of Smart and Functional Packaging Technologies

Smart packaging technologies incorporating QR codes, near-field communication tags, and functional barrier coatings are gaining traction across Portuguese supply chains. These innovations enhance traceability, extend product shelf life, and improve consumer engagement. For instance, from January 2025, companies selling packaged goods in Portugal face new mandatory environmental labelling obligations under the country's extended producer responsibility regime, requiring clear disposal guidance on all packaging to support higher recycling performance and EU circularity goals.

Growing Demand for Flexible Packaging in Food and Beverage Sectors

Flexible packaging formats, including stand-up pouches, sachets, and resealable bags, are experiencing robust demand in Portugal's food and beverage industry due to their cost-efficiency and versatility. For instance, in February 2025, Mondi partnered with Proquimia to launch paper-based stand-up pouches for dishwashing tablets in Spain and Portugal, using re/cycle FunctionalBarrier Paper with over 85% paper share, designed to meet the recyclability requirements of both countries and reduce carbon emissions compared with plastic alternatives.

Market Outlook 2026-2034:

Portugal's packaging market is positioned for sustained expansion, supported by regulatory harmonization, sustainability-driven innovation, and rising end-use demand. In accordance with this, the implementation of the EU Packaging and Packaging Waste Regulation is expected to accelerate investments in recyclable materials, circular design, and advanced waste management systems. Similarly, growing food processing output, expanding e-commerce logistics, and increasing consumer preference for convenience-oriented packaging are anticipated to drive higher revenue streams. As such, in July 2025, Portuguese Logistics as a Service platform Lyzer raised over EUR 10 Million to support international expansion and technology development. Backed by existing investors and new partner C2 Capital, Lyzer provides integrated logistics tools for retailers. With strong traction in Iberia, it plans European growth and AI-powered feature launches. Continued modernization of manufacturing capabilities, coupled with strategic partnerships and capacity expansion by domestic producers, will further strengthen the market trajectory across the forecast period. The market generated a revenue of USD 4.49 Billion in 2025 and is projected to reach a revenue of USD 6.29 Billion by 2034, growing at a compound annual growth rate of 3.82% from 2026-2034.

Portugal Packaging Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Material |

Paper and Paperboard |

38.7% |

|

Product Type |

Flexible Packaging |

42.9% |

|

Packaging Type |

Primary Packaging |

55.4% |

|

End Use Industry |

Food |

46.1% |

|

Region |

A. M. Lisboa |

34.5% |

Material Insights:

- Plastic

- Paper & Paperboard

- Metal

- Glass

- Wood

- Others

Paper and paperboard dominates the market with a share of 38.7% of the total Portugal packaging market in 2025.

The paper and paperboard segment leads Portugal's packaging market, driven by escalating regulatory requirements under the EU Packaging and Packaging Waste Regulation and rising consumer preference for renewable, recyclable packaging materials. Government initiatives promoting extended producer responsibility and circular economy principles are compelling manufacturers to transition from plastic to fiber-based solutions.

Paper-based packaging offers advantages including biodegradability, high printability, and compatibility with existing recycling infrastructure, making it well-suited for food, beverage, and consumer goods applications. The growing shift toward paper-based alternatives for wraps, bags, and pouches is supported by advances in barrier coating technologies that maintain product protection without compromising recyclability. A such, in October 2025, the European Investment Bank signed a EUR 40 Million green finance facility with The Navigator Company to accelerate decarbonization and support innovative moulded fibre packaging production at its Aveiro facility.

Product Type Insights:

- Rigid Packaging

- Boxes & Containers

- Bottles & Jars

- Pails & Cans

- Trays & Pallets

- Caps & Closures

- Tubes

- Others

- Flexible Packaging

- Bags & Sacks

- Films & Wraps

- Labels

- Sachets & Pouches

- Tapes

- Others

Flexible packaging leads with a share of 42.9% of the total Portugal packaging market in 2025.

Flexible packaging continues to lead Portugal’s packaging market, driven by its lightweight nature, cost efficiency, and broad application across food, pharmaceuticals, and personal care. Its adaptable design supports diverse product needs while helping manufacturers lower transportation expenses and reduce overall material usage. This efficiency also contributes to sustainability goals, as flexible formats generate less waste and often require fewer resources compared to rigid alternatives, strengthening their long-term market appeal.

The expansion of flexible packaging is further driven by rising consumer demand for convenience-oriented formats such as resealable pouches, portion-controlled sachets, and lightweight wraps. Advances in barrier technologies and sustainable material development are enabling flexible packaging to serve perishable food and sensitive product categories with improved shelf-life performance. Portugal's growing processed food industry and increasing retail modernization are creating sustained demand for flexible packaging solutions that balance functionality, cost, and environmental compliance across the supply chain.

Packaging Type Insights:

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

Primary packaging is the largest segment, accounting for 55.4% of the total Portugal packaging market in 2025.

Primary packaging commands the highest share in Portugal's packaging market owing to its indispensable role in direct product containment, protection, and consumer interaction. Stringent food safety regulations and pharmaceutical compliance standards mandate the use of high-quality primary packaging that ensures product integrity from production through retail display. In 2024, a consortium of 79 companies and entities led by Vangest launched a EUR 105 Million sustainable packaging initiative, partially funded through Portugal's Recovery and Resilience Plan, focused on redesigning packaging materials for reuse and recyclability across the entire lifecycle.

Primary packaging formats including bottles, jars, pouches, trays, and blister packs are experiencing sustained demand across Portugal's food, beverage, healthcare, and personal care industries. The growing emphasis on shelf appeal, product differentiation, and consumer convenience is driving manufacturers to develop primary packaging solutions with enhanced barrier properties, tamper-evident features, and recyclable construction.

End Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Food

- Dairy Products

- Meat, Poultry, and Seafood

- Agricultural Produce

- Others

- Beverages

- Alcoholic Beverages

- Non-alcoholic Beverages

- Cosmetics & Personal Care

- Skin Care

- Hair Care

- Others

- Chemicals & Lubricants

- Healthcare

- Pharmaceuticals

- Medical Devices

- Others

- Consumer Products

- Building & Construction

- Electronics

- Automotive

- Others

Food holds the largest share at 46.1% of the total Portugal packaging market in 2025.

The food segment maintains its leading position in Portugal's packaging market, driven by the country's thriving food processing industry, strong agricultural traditions, and expanding retail distribution networks. Packaging demand spans dairy, meat, seafood, bakery, and fresh produce categories, with growing emphasis on shelf-life extension and food safety compliance. Portugal's supermarket sector generated over €24 billion in revenue in 2023, with private-label products now accounting for over 40% of supermarket sales, increasing demand for differentiated packaging formats across domestic food retail channels.

The expansion of online grocery shopping and quick-commerce services in Portugal is further stimulating food packaging demand, particularly for protective, insulated, and portion-controlled formats suitable for delivery logistics. Consumer preference for convenience foods, ready-to-eat meals, and sustainable packaging is reshaping food packaging design priorities. Portugal's geographical position as a significant seafood and agricultural producer within Europe creates sustained packaging requirements for export-oriented processing, cold chain logistics, and compliance with EU food contact material regulations across domestic and international supply chains.

Regional Insights:

- Norte

- Centro

- A. M. Lisboa

- Alentejo

- Others

A. M. Lisboa accounts for the highest revenue share of 34.5% of the total Portugal packaging market in 2025.

The Lisbon Metropolitan Area commands the largest regional share in Portugal's packaging market, supported by its position as the country's economic, logistical, and demographic center. The region generates approximately 36% of Portugal's gross domestic product and houses nearly 3 million residents, creating concentrated demand for consumer goods and associated packaging solutions. The Lisbon Metropolitan Area anchored by services, food processing, retail, and tourism sectors collectively generate substantial packaging consumption across primary, secondary, and tertiary formats.

The concentration of major food retailers, distribution centers, and e-commerce fulfillment hubs in the Lisbon metropolitan region drives sustained packaging demand across corrugated, flexible, and rigid formats. DS Smith invested over EUR 50 Million in its Portuguese packaging facilities over three years, including upgrading a corrugator unit at its Lisbon plant, enhancing production of sustainable corrugated cardboard solutions for transportation and heavy-duty applications. The region's status as Portugal's primary tourism hub and its growing quick-commerce activity further amplify packaging requirements for food service, hospitality, and last-mile delivery operations.

Market Dynamics:

Growth Drivers:

Why is the Portugal Packaging Market Growing?

Strengthening Regulatory Framework for Sustainable Packaging

The European Union's regulatory agenda is a primary catalyst for Portugal's packaging market expansion, compelling manufacturers and brand owners to invest in recyclable, reusable, and compostable packaging solutions. Accordingly, Portugal introduced mandatory packaging recycling labels from January 2025 under its EPR overhaul. All packaging must provide clear material and disposal instructions. Companies can choose formats, but compliance is enforced by APA, supporting improved recycling and EU sustainability goals. Portugal has been proactively aligning with these directives through national policies on extended producer responsibility and environmental labelling. These regulatory developments are stimulating demand for innovative packaging materials and production processes, encouraging industry-wide investments in design-for-recyclability, lightweight construction, and biodegradable alternatives that support market expansion.

Expanding Food Processing and Retail Modernization

Portugal's dynamic food processing sector and rapidly modernizing retail landscape are generating sustained demand for diverse packaging solutions. The country's strong agricultural heritage, combined with growing processed food production and retail expansion, creates robust consumption across flexible, rigid, and corrugated packaging formats. Increasing private-label penetration and new store openings by leading supermarket chains are driving demand for differentiated cost-effective packaging that enhances shelf appeal and brand positioning. The growing demand for convenience foods, ready-to-eat meals, and premium food products across Portuguese supermarkets and specialty stores is sustaining packaging consumption growth across multiple material categories and formats.

Rising E-Commerce Activity and Last-Mile Delivery Demand

Portugal's expanding e-commerce sector is creating new packaging demand streams, particularly for protective, transit, and last-mile delivery packaging formats. The country's digital commerce market reached approximately EUR 4.1 Billion in 2024, reflecting a 13.8% increase over the prior year, with food and beverage segments showing strong growth potential. This expansion necessitates robust packaging solutions for product protection, thermal insulation, and efficient shipping across diverse product categories. The concentration of e-commerce activity in the Lisbon and Porto metropolitan areas is driving investments in fulfillment infrastructure and packaging optimization. Quick-commerce pilots promising sub-30-minute delivery in urban centers are intensifying requirements for right-sized, protective packaging that minimizes void space while ensuring product integrity. The growing adoption of omnichannel retail strategies by Portuguese businesses is further expanding packaging demand across both physical retail and digital commerce channels.

Market Restraints:

What Challenges the Portugal Packaging Market is Facing?

Escalating Raw Material Costs and Supply Chain Volatility

Fluctuating prices of key raw materials including pulp, polymers, metals, and glass resins are creating cost pressures across Portugal's packaging value chain. Global supply chain disruptions, energy price volatility, and geopolitical uncertainties are amplifying input cost variability, compressing manufacturer margins and complicating pricing strategies. These cost fluctuations challenge smaller producers who lack the scale to absorb or pass through price increases effectively.

Regulatory Compliance Complexity and Transitional Costs

The evolving regulatory landscape, including the EU Packaging and Packaging Waste Regulation's phased implementation through 2035, imposes significant compliance burdens on Portuguese packaging manufacturers. Companies must invest in redesigning packaging for recyclability, incorporating recycled content, implementing digital labelling systems, and adapting to substance-of-concern restrictions. Small and medium-sized enterprises face disproportionate challenges in meeting these requirements due to limited capital resources and technical expertise.

Low Circular Material Utilization Rates

Portugal’s circular material use rate remains among the lowest in the European Union, highlighting structural weaknesses in the country’s transition toward a more circular packaging economy. Persistent gaps in recycling infrastructure, collection efficiency, and material recovery systems continue to limit progress. Inadequate sorting facilities and constrained domestic recycling capacity create supply bottlenecks, restricting access to high-quality recycled feedstock. These limitations slow the integration of secondary raw materials into packaging production and reduce overall circular performance.

Competitive Landscape:

The Portugal packaging market features a competitive landscape characterized by a mix of multinational corporations and domestic producers operating across material categories and end-use sectors. Market participants are increasingly differentiating through sustainability-driven innovation, investments in recyclable and fiber-based packaging solutions, and expansion of production capacities. Competition is also driven by technological advancements in barrier coatings, digital printing, and smart packaging functionalities. Strategic partnerships, facility modernization, and vertical integration are enabling market players to enhance operational efficiency, strengthen supply chain resilience, and capture growing demand across food, beverage, healthcare, and e-commerce packaging applications throughout Portugal.

Recent Developments:

- In October 2025, Dow, Zermatt, and Nature’s Variety launched a recyclable pet food pouch containing 10% advanced recycled content, now available in Spain, France, and Portugal. The mono-material PE design supports EU recyclability standards and helps meet 2030 PPWR targets, with plans to reach 30% recycled content by 2030.

- In March 2025, Portugal planned to launch a national Deposit Return Scheme for single-use beverage packaging in 2026, managed by SDR Portugal with Sensoneo providing the IT system. The scheme will include thousands of collection points and integrate HoReCa venues, aiming to improve container collection and recycling rates nationwide.

Portugal Packaging Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Materials Covered |

Plastic, Paper & Paperboard, Metal, Glass, Wood, Others |

|

Product Types Covered |

|

|

Packaging Types Covered |

Primary Packaging, Secondary Packaging, Tertiary Packaging |

|

End Use Industries Covered |

|

|

Regions Covered |

Norte, Centro, A. M. Lisboa, Alentejo, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Portugal Packaging Market Report

The Portugal packaging market size was valued at USD 4.49 Billion in 2025.

The Portugal packaging market is expected to grow at a compound annual growth rate of 3.82% from 2026-2034 to reach USD 6.29 Billion by 2034.

Paper and paperboard dominated the market with a share of 38.7%, driven by regulatory support for recyclable materials, growing environmental awareness, and increasing adoption of fiber-based packaging across food and consumer goods sectors.

Key factors driving the Portugal packaging market include strengthening EU sustainability regulations, expanding food processing and retail modernization, rising e-commerce activity, growing consumer preference for eco-friendly packaging, and increasing investments in circular economy infrastructure.

Major challenges include escalating raw material costs, regulatory compliance complexity under phased EU packaging regulations, low circular material utilization rates, limited domestic recycling infrastructure, and cost pressures on small and medium-sized packaging manufacturers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade