Portugal Vehicle Telematics Market Size, Share, Trends and Forecast by Application, Technology, Sales Channel, Vehicle Type, and Region, 2026-2034

Portugal Vehicle Telematics Market Summary:

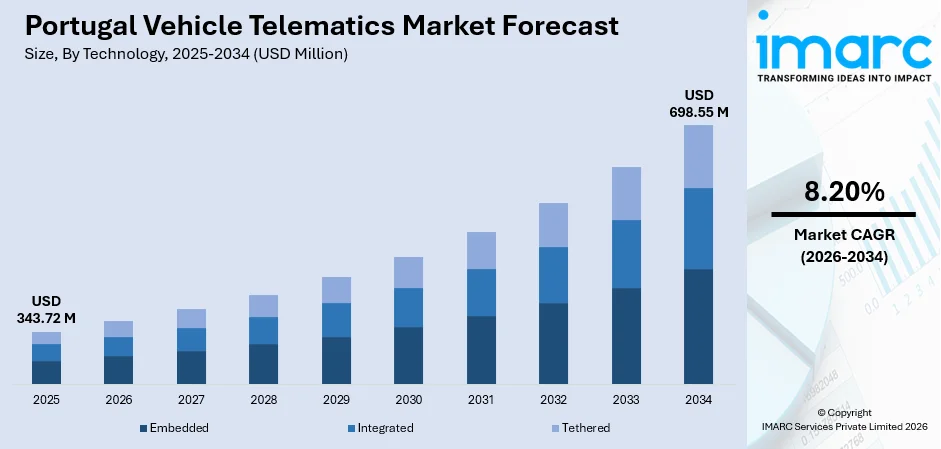

The Portugal vehicle telematics market size was valued at USD 343.72 Million in 2025 and is projected to reach USD 698.55 Million by 2034, growing at a compound annual growth rate of 8.20% from 2026-2034.

The Portugal vehicle telematics market is primarily driven by the expanding adoption of connected vehicle technologies, mandatory European Union safety regulations such as eCall, and growing demand for fleet management solutions among logistics and transportation operators. The rising penetration of embedded telematics systems in new passenger cars manufactured by leading OEMs, alongside increasing consumer awareness of usage-based insurance models and real-time navigation services, continues to strengthen the Portugal vehicle telematics market share.

Key Takeaways and Insights:

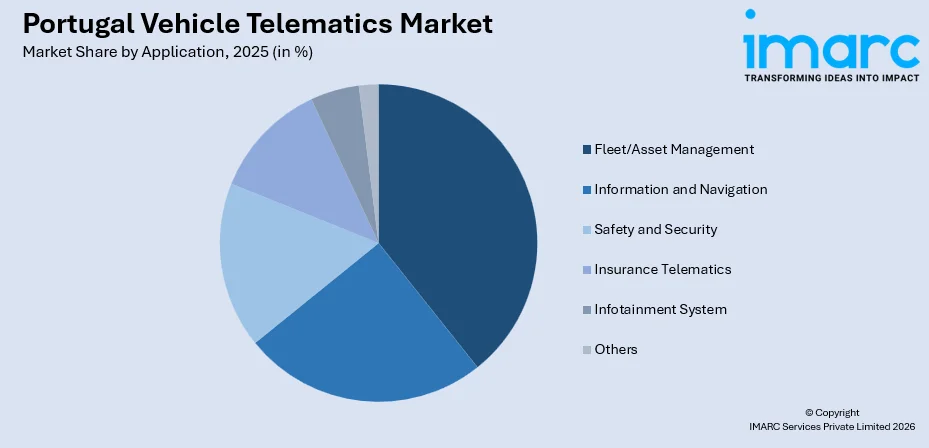

- By Application: Fleet/asset management dominates the market with a share of 39.5% in 2025, owing to the expanding logistics sector, rising adoption of real-time vehicle tracking platforms, and increasing demand for route optimization and fuel management solutions among Portuguese fleet operators.

- By Technology: Embedded leads the market with a share of 44.1% in 2025, driven by OEM integration of telematics control units during vehicle manufacturing, mandatory eCall compliance requirements, and growing consumer preference for factory-fitted connected vehicle features.

- By Sales Channel: OEM exhibits a clear dominance in the market with 61.7% share in 2025, reflecting automakers’ strategic commitment to integrating telematics hardware and software directly into new vehicles, enabling seamless connectivity and data-driven mobility services.

- By Vehicle Type: Passenger cars comprise the largest segment with 68.9% share in 2025, supported by higher production volumes, growing consumer demand for advanced connectivity features, and rising adoption of telematics-enabled insurance and navigation services in personal vehicles.

- By Region: A. M. Lisboa represents the largest region with 35.2% share in 2025, driven by the concentration of corporate headquarters, logistics hubs, and the highest vehicle density in Portugal, coupled with advanced digital infrastructure supporting connected mobility services.

- Key Players: The market is becoming increasingly competitive as global fleet-management providers, local mobility tech firms, and insurers expand connected vehicle solutions. Competition focuses on compliance tools, real-time tracking, driver behavior analytics, and AI-driven efficiency gains, supported by growing demand from logistics and transportation operators.

To get more information on this market Request Sample

The Portugal vehicle telematics market is experiencing robust growth, propelled by the convergence of regulatory mandates, technological innovation, and rising connected vehicle penetration. The European Union’s General Safety Regulation, effective from July 2024 for all new vehicles, mandates advanced driver assistance systems and embedded connectivity features, creating a strong compliance-driven demand for telematics solutions across the Portuguese automotive sector. Fleet management applications remain the dominant use case, as Portuguese logistics and transportation companies increasingly adopt real-time tracking, predictive maintenance, and route optimization platforms to enhance operational efficiency and reduce costs. The embedded technology segment benefits from automakers’ strategies to integrate telematics control units as standard features, supported by the mandatory eCall system and the upcoming Next Generation eCall requirement under EU Delegated Regulation 2024/1180, which mandates 4G/5G-compatible emergency systems in all new vehicles from January 2026. The OEM sales channel maintains dominance as manufacturers embed connectivity solutions directly during production, while the passenger car segment leads adoption due to higher registration volumes and consumer demand for connected services.

Portugal Vehicle Telematics Market Trends:

Rising OEM-integrated telematics partnerships for hardware-free fleet services

The Portuguese vehicle telematics market is witnessing a significant shift toward OEM-integrated data solutions that eliminate the need for aftermarket hardware installations. As such, in March 2025, Targa Telematics, which maintains a strong presence in Portugal, signed a strategic partnership with Volkswagen Group Info Services AG to directly integrate fleet vehicle data from six brands into its platform. This collaboration enables fleet managers to access maintenance management, stolen vehicle recovery, and driving analytics without requiring additional hardware, substantially reducing deployment costs and accelerating adoption.

Transition to Next Generation eCall accelerating embedded telematics adoption

Portugal is preparing for the mandatory transition to Next Generation eCall, as updated European regulations require new vehicles to be equipped with 4G and 5G-compatible emergency call systems. This shift is prompting automakers to upgrade embedded telematics control units across production lines to ensure compliance and uninterrupted connectivity. At the same time, the gradual phase-out of legacy 2G and 3G networks across Europe is accelerating hardware modernization, pushing fleet operators and vehicle owners to adopt advanced connected vehicle technologies.

AI-powered fleet analytics driving digital transformation in vehicle management

The integration of artificial intelligence and predictive analytics into telematics platforms is reshaping fleet management practices in Portugal. The European fleet management market reached 18.1 million active systems by the end of 2024, with projections to grow to 30.5 million units by 2029, reflecting the accelerating pace of digital fleet transformation. Portuguese fleet operators are increasingly leveraging AI-driven tools for predictive maintenance scheduling, fuel consumption optimization, and driver behavior analysis to enhance safety and reduce operational expenditures.

Market Outlook 2026-2034:

The Portugal vehicle telematics market is positioned for sustained expansion throughout the forecast period, supported by regulatory mandates, advancing connected vehicle technologies, and growing fleet digitization across the country. Similarly, the increasing adoption of embedded telematics solutions, driven by OEM strategies and EU safety requirements, is expected to create substantial opportunities for market participants. The expansion of usage-based insurance models, rising demand for real-time fleet tracking, and the proliferation of 5G connectivity infrastructure are anticipated to serve as key growth catalysts. Accordingly, in November 2025, Portuguese telecom operators plan to invest EUR 4.2 Billion over 5 years in 5G, satellites, and fibre expansion to support growth. Additionally, the Portuguese government’s commitment to decarbonizing transport, evidenced by record electric vehicle registrations reaching over 70,000 combined BEV and PHEV units in 2024, is expected to further accelerate telematics integration as electric vehicles inherently require advanced connected systems for battery management and charging optimization. The market generated a revenue of USD 343.72 Million in 2025 and is projected to reach a revenue of USD 698.55 Million by 2034, growing at a compound annual growth rate of 8.20% from 2026-2034.

Portugal Vehicle Telematics Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Application |

Fleet/Asset Management |

39.5% |

|

Technology |

Embedded |

44.1% |

|

Sales Channel |

OEM |

61.7% |

|

Vehicle Type |

Passenger Cars |

68.9% |

|

Region |

A. M. Lisboa |

35.2% |

Application Insights:

Access the comprehensive market breakdown Request Sample

- Information and Navigation

- Safety and Security

- Fleet/Asset Management

- Insurance Telematics

- Infotainment System

- Others

Fleet/asset management dominates with a market share of 39.5% of the total Portugal vehicle telematics market in 2025.

The fleet and asset management segment maintains its leading position in the Portuguese vehicle telematics market, driven by the country’s expanding logistics and transportation sector. Portuguese fleet operators are increasingly adopting comprehensive telematics platforms to achieve real-time visibility into vehicle locations, optimize delivery routes, and monitor driver behavior for safety compliance. Frotcom Lusitana, a prominent fleet management provider in Portugal, celebrated 15 years of operations in 2025 while serving over 500 Portuguese businesses across transportation, distribution, construction, and passenger services, underscoring the deep market penetration of fleet telematics solutions.

Businesses in Portugal are increasing their demand for fleet management telematics systems because they need to achieve operational efficiency and decrease their operational costs. The European fleet management market is expanding because European companies are increasing their use of digital fleet management systems. Portuguese companies use advanced fleet analytics to lower their fuel use while they create maintenance schedules and meet regulatory standards for their operations, and electric vehicle management systems which are now part of fleet platforms, will drive increased demand as commercial EV adoption in Portugal grows.

Technology Insights:

- Integrated

- Tethered

- Embedded

Embedded leads the Portugal vehicle telematics market with a share of 44.1% in 2025.

The embedded technology segment commands the largest share of the Portuguese vehicle telematics market, driven by automakers’ strategic integration of telematics control units directly into vehicle architectures during manufacturing. This approach delivers superior reliability, seamless connectivity, and enhanced functionality compared to aftermarket alternatives. The EU’s Delegated Regulation 2024/1180, adopted in February 2024, mandates Next Generation eCall compatible with 4G/5G networks in all new vehicle types from January 2026, compelling manufacturers to upgrade embedded telematics hardware and further consolidating the segment’s dominance.

The embedded telematics segment is gaining momentum through OEM partnerships that enable hardware-free service delivery via factory-installed connected vehicle systems. By integrating fleet data directly from multiple automotive brands into centralized platforms, providers eliminate the need for aftermarket device installations. This approach allows fleet operators and individual drivers in Portugal to access advanced features such as remote diagnostics, electric vehicle energy monitoring, predictive maintenance alerts, and stolen vehicle tracking. Built-in connectivity enhances efficiency, reduces installation costs, and supports seamless digital mobility services.

Sales Channel Insights:

- OEM

- Aftermarket

OEM holds the largest share with 61.7% of the total Portugal vehicle telematics market in 2025.

The OEM sales channel dominates the Portuguese vehicle telematics market as automobile manufacturers increasingly embed telematics systems as standard features in new vehicles. This trend is reinforced by EU regulatory requirements for safety and connectivity systems, including mandatory eCall and advanced driver assistance features under the General Safety Regulation effective from July 2024 for all new vehicles. Portugal registered 209,716 new vehicles in 2024, representing a 5.1% year-over-year increase, with each new registration contributing to the expanding base of OEM-equipped telematics-enabled vehicles in the country.

The OEM channel’s strength is further bolstered by manufacturers’ strategies to leverage connected vehicle data for new revenue streams and enhanced customer services. Leading automakers such as Volkswagen, Peugeot, and Mercedes-Benz, which rank among Portugal’s top-selling brands, are integrating advanced telematics platforms that support over-the-air updates, predictive maintenance alerts, and connected navigation services. This factory-integrated approach reduces deployment complexity and ensures consistent telematics coverage across the Portuguese vehicle fleet from the point of sale.

Vehicle Type Insights:

- Passenger Cars

- Commercial Vehicles

Passenger cars account for the highest revenue with a 68.9% share of the total Portugal vehicle telematics market in 2025.

The passenger car segment leads the Portuguese vehicle telematics market, driven by substantially higher production and registration volumes compared to commercial vehicles. Portugal’s passenger vehicle registrations totalled 189,533 units in the first eleven months of 2024, reflecting a 3.6% positive variation compared to the same period in the prior year. The growing consumer preference for connected in-car features, including real-time navigation, smartphone integration, and advanced safety systems, continues to drive telematics adoption across the passenger vehicle fleet nationwide.

The passenger car segment’s dominance is further reinforced by the rapid electrification of Portugal’s personal vehicle market, as electric vehicles inherently require advanced telematics for battery monitoring and charging management. In January 2025, battery electric vehicle registrations reached a record market share of 22.5% for new passenger cars in Portugal, reflecting the accelerating transition toward connected, electrified personal mobility. This EV surge creates additional demand for embedded telematics solutions that support energy management, range optimization, and integration with charging infrastructure networks.

Regional Insights:

- Norte

- Centro

- A. M. Lisboa

- Alentejo

- Others

A. M. Lisboa represents the leading region with a 35.2% share of the total Portugal vehicle telematics market in 2025.

The A. M. Lisboa metropolitan region commands the largest share of the Portuguese vehicle telematics market, supported by its position as the country’s primary economic and transportation hub. With a metropolitan population of approximately 3.01 million and contributing over 36% of Portugal’s national GDP, the Lisbon region concentrates the highest density of corporate headquarters, logistics operations, and fleet management companies. The region’s advanced digital infrastructure, dense road network, and heavy commuter traffic patterns create substantial demand for telematics-enabled navigation, fleet tracking, and insurance solutions. Lisbon’s role as a major technology adoption center further accelerates the deployment of connected vehicle services across both commercial and personal mobility segments.

In addition, the strong presence of multinational technology firms, automotive distributors, and mobility startups in the Lisbon area fosters continuous innovation in connected vehicle applications. Pilot programs for smart mobility, urban traffic management, and electric vehicle integration are frequently launched in the region, creating an ecosystem conducive to telematics expansion. High smartphone penetration, widespread 4G and 5G connectivity, and growing investment in intelligent transport systems further reinforce Lisbon’s leadership in adopting advanced vehicle tracking and data-driven mobility solutions.

Market Dynamics:

Growth Drivers:

Why is the Portugal Vehicle Telematics Market Growing?

Expanding vehicle registrations and rising connected car penetration

Steady growth in Portugal’s automotive market is expanding the base of telematics-enabled vehicles, directly supporting demand for connected mobility solutions. As new vehicle sales rise, automakers are increasingly integrating factory-fitted telematics systems as standard features, improving real-time connectivity and service access. The growing adoption of electric and hybrid vehicles is further accelerating this trend, with EV sales in Portugal increasing by 10% in 2024. These vehicles rely heavily on advanced connected platforms for battery monitoring, charging optimization, predictive maintenance, and energy management. As electrification expands, the integration of telematics becomes increasingly essential, reinforcing demand for connected vehicle technologies and supporting broader telematics market growth across the country.

Mandatory EU safety regulations driving embedded telematics deployment

The European Union’s regulatory framework remains a key driver of telematics adoption in Portugal. The General Safety Regulation requires new vehicles to incorporate advanced driver assistance systems supported by embedded sensors and connectivity. In addition, updated rules introducing Next Generation eCall standards mandate 4G and 5G-compatible emergency call systems in new vehicle models. These compliance requirements ensure that vehicles entering the Portuguese market are equipped with foundational telematics infrastructure, steadily expanding the installed base of connected vehicles nationwide.

Accelerating fleet digitization and operational efficiency demands

The growing emphasis on operational efficiency among Portuguese logistics and transportation companies is driving significant investment in fleet telematics solutions. Fleet operators are adopting comprehensive digital platforms that integrate real-time vehicle tracking, predictive maintenance scheduling, fuel consumption analysis, and driver behavior monitoring to reduce costs and improve service delivery. For example, in March 2024, Targa Telematics launched new fleet management services, Viasat Fleet Start and Advanced, designed to convert real-time vehicle data into actionable insights. The solutions help fleets reduce costs, improve operations, and protect against theft or vehicle misuse, illustrating the deep adoption of telematics-based fleet management solutions. The convergence of rising fuel costs, tightening environmental regulations, and increasing customer expectations for delivery visibility is compelling fleet operators to invest in advanced telematics infrastructure that delivers measurable operational improvements.

Market Restraints:

What Challenges the Portugal Vehicle Telematics Market is Facing?

Data privacy concerns limiting consumer willingness to share driving information

The collection and transmission of real-time driving data through telematics systems raise notable privacy concerns among Portuguese consumers and fleet operators. Many users remain cautious about continuous tracking of driving behavior, location data, and vehicle performance metrics. At the same time, the European Union’s General Data Protection Regulation imposes strict compliance obligations on telematics providers, including explicit consent requirements, data minimization standards, secure storage protocols, and limitations on cross-border data transfers, increasing deployment complexity and operational costs.

High integration costs for retrofitting legacy vehicle fleets

The significant cost burden associated with equipping existing older vehicles with aftermarket telematics devices presents a notable barrier to market expansion in Portugal. The Portuguese vehicle fleet has a substantial share of vehicles over ten years old, and retrofitting these legacy vehicles with compatible telematics hardware requires considerable investment in devices, installation labor, and ongoing maintenance. Small and medium-sized fleet operators, which constitute the majority of Portuguese logistics businesses, often lack the capital resources to undertake comprehensive fleet-wide telematics deployment.

Cybersecurity vulnerabilities in connected vehicle ecosystems

The increasing connectivity of vehicles through telematics systems expands the potential attack surface for cybersecurity threats, creating concerns among consumers, fleet operators, and regulatory authorities. Connected vehicles transmit sensitive data including location, driving patterns, and personal information through wireless networks, making them potential targets for unauthorized access and data breaches. The growing complexity of vehicle software architectures, combined with the proliferation of third-party telematics applications, requires continuous investment in security protocols and threat detection capabilities.

Competitive Landscape:

The Portugal vehicle telematics market features a competitive landscape characterized by a mix of global telematics providers, European fleet management specialists, and domestic technology companies. The market has witnessed significant consolidation activity as international players seek to strengthen their Portuguese operations through strategic acquisitions and partnerships. Companies compete across multiple dimensions including technology innovation, service coverage, OEM integration capabilities, and localized customer support. The growing complexity of connected vehicle ecosystems and evolving EU regulatory requirements are raising barriers to entry while encouraging collaboration between telematics providers, automakers, and insurance companies to deliver comprehensive mobility solutions.

Recent Developments:

- In February 2026, Berg Insight ranked Targa Telematics as Europe’s largest fleet management vendor for the third consecutive year, with 900,000 connected vehicles in 2024. Active in Portugal and across Europe, the company leverages a hardware-agnostic platform and Agentic AI to enhance fleet efficiency and decision-making.

- In October 2025, Geotab acquired Verizon Connect’s commercial fleet operations in Europe and Australia, including Portugal, to strengthen its presence in the small and mid-sized fleet segment. The deal adds around 400 staff, expands customer support, and enhances delivery of AI-driven, data-focused telematics solutions for fleet efficiency and safety.

Portugal Vehicle Telematics Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Applications Covered |

Information and Navigation, Safety and Security, Fleet/Asset Management, Insurance Telematics, Infotainment System, Others |

|

Technologies Covered |

Integrated, Tethered, Embedded |

|

Sales Channels Covered |

OEM, Aftermarket |

|

Vehicle Types Covered |

Passenger Cars, Commercial Vehicles |

|

Regions Covered |

Norte, Centro, A. M. Lisboa, Alentejo, Others |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Portugal Vehicle Telematics Market Report

The Portugal vehicle telematics market size was valued at USD 343.72 Million in 2025.

The Portugal vehicle telematics market is expected to grow at a compound annual growth rate of 8.20% from 2026-2034 to reach USD 698.55 Million by 2034.

Fleet/asset management dominated the market with a share of 39.5%, driven by growing demand for real-time vehicle tracking, route optimization, and operational efficiency among Portuguese logistics and transportation operators.

Key factors driving the Portugal vehicle telematics market include mandatory EU safety regulations, rising vehicle registrations with embedded connectivity, expanding fleet digitization, and growing adoption of usage-based insurance and connected mobility services.

Major challenges include data privacy concerns under GDPR compliance requirements, high retrofit costs for legacy vehicle fleets, cybersecurity vulnerabilities in connected ecosystems, limited telematics awareness among small fleet operators, and infrastructure constraints in rural areas.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)